If anyone has studied past 4 years of this company, a clear pattern emerges. Alternate years are very good followed by flat years. For forecasting EPS for 23-24 and 24-25, I used available details like est sales of 550 Cr in FY 24-25.

Financial Year

EPS

Change

2019-20

15.71

2020-21

21.77

38.5%

2021-22

22.12

1.6%

2022-23

34.71

57.0%

2023-24 Est

37.22

7.2%

2024-25 Est

52.08

39.9%

If you plot stock prices along with this, you will notice that as earning rise, market is rerating this stock and providing higher PE. This also means current year FY 24 is the year of consolidation and stock would start moving up in FY 25 with earning and PE rising in tandem providing good 35%+ potential upside from current price. Needless to say, this assumes no geopolitical event or election related issue in US or India.

Disoclosure - Part of my long term folio held over last 3 years. Continues to add during current downturn.

Racl Geartech has been nominated as Tier I series supplier, by a Premium Car manufacturer in Germany for supply of Parking Lock Mechanism for electric cars, which is a mechanical device coupled with Electric vehicle.

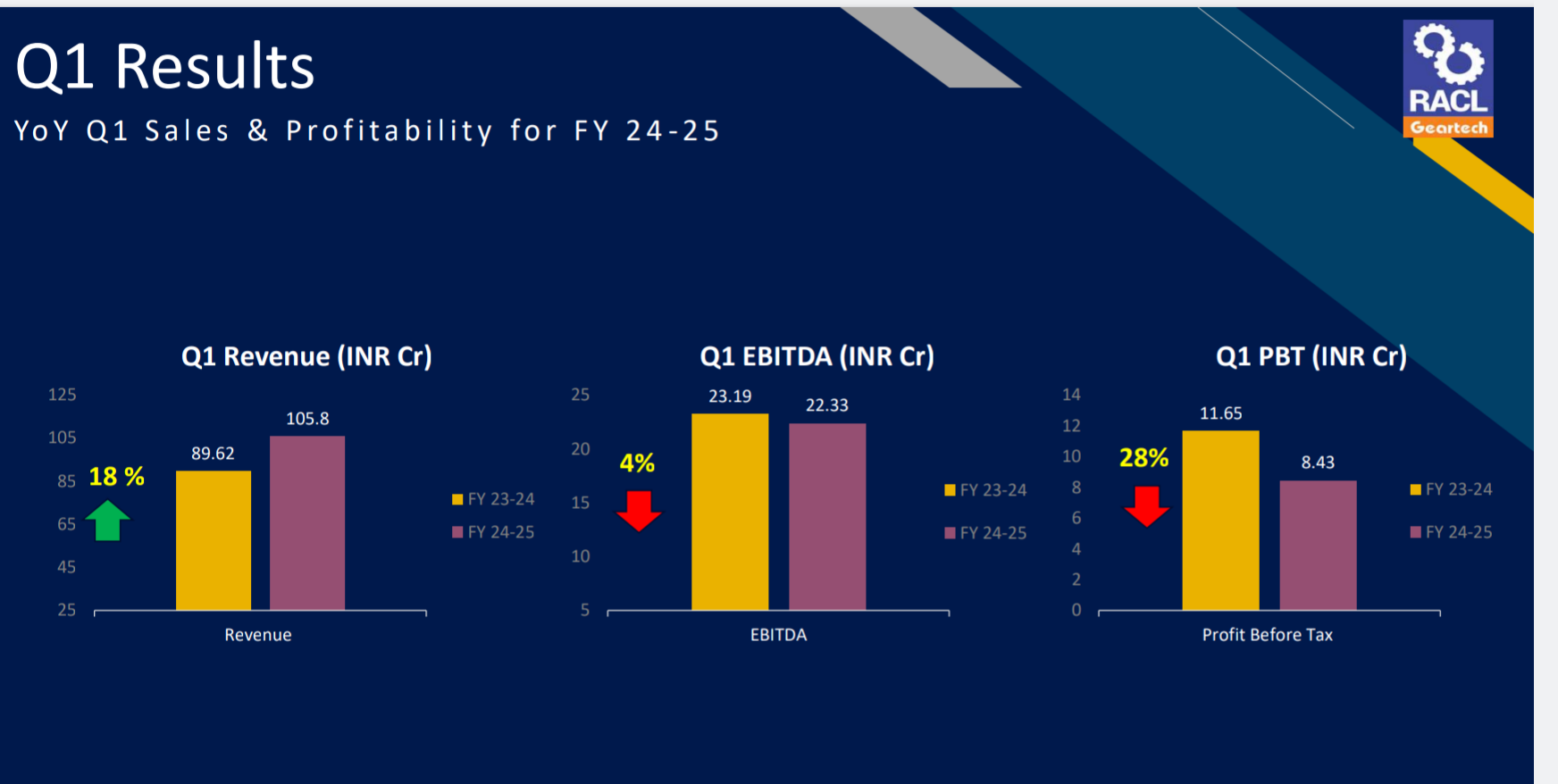

RACL continues their growth trajectory (17% sales and flat EPS) and are confident of reaching 548 cr. sales in FY25 (implying 37% absolute growth). Concall notes below.

FY24Q3

Nominated as a Tier 1 supplier for passenger car segment for the first time. This is for entire subsystem for park lock mechanism and from a new customer for an electric sports car using a new platform coming in 2027 ($38mn business over 7-8 years starting FY27). Competitors were Chinese and European companies. This can change the trajectory of RACL’s business (from 500 to 1000 cr.). Will be manufactured in Gajraula plant (which is now running on 100% green energy)

Inaugurated plant 2 in Noida (26k sq.ft vs 11k sq.ft of earlier Noida plant). Equipped with clean rooms and invested $1mn capex. Doubled manpower from 120 to 250. Will export new electric bicycle product, earlier plant was only catering to domestic market

For the electric bicycle product, their customer’s competitor is selling 2mn bikes/year

Started invoicing KTM Austria locally on a weekly just in time basis

Capex: 80-85 cr. in FY24, 60 cr. in FY25. Have invested 25 crs. in last 2-years for housing colonies for engineers and managers.

Still have 10 acres of land

Sales should reach 548 cr. in FY25

With 22 customers, RACL is present in every segment (100 cc 2-W, 49 ton truck, passenger cars, tractors, off-road vehicle for sand, snow, etc.)

With EVs and their low-weight requirements, have seen manufacturers shifting to non-ferrous materials (aluminum, titanium, etc.). Also have seen huge increase in demand for precision machining

Disclosure: Invested (position size here, bought shares in last-30 days)

Lower sales and lower margins could be due to delayed shipments as well as some impact of red sea issue. Considering the product quality and customer profile, I would not be too worried about the P&L (except interest cost)

More than margins, rising debt level is the bigger issue here. Receivables have risen faster than sales in this quarter. High inventory levels (being 75% exports company) along with increasing capex makes this a highly capital intensive company. Promoters reluctance to raise equity is making the matters worse for the company. Any steps to reduce debt burden can be positive trigger for sustainable future growth

Discl - invested for last 3 years and forms part of my core PF. Hence biased. Transactions in last 2 weeks

I have been following RACL for ~6 quarters now (with no purchases) and the company seems to be growing consistently and delivering consistent margins in the low 20s. The high gross margin is also great. The key issue here is that the return on capital is terrible and has consistently been in the mid-teens which does not point to a high quality manufacturer with significant pricing power but almost feels like they are buying business by holding inventory for their customers. There is also the question of how much of this inventory is real vs needs to be written off (since inventory days have doubled from 200 days to 350 days in 5 years). Even if one normalizes for growth, the cash flow conversion in this business is no more than 20% of EBITDA, which is quite poor. How do other folks who are invested / have spent time evaluating RACL consider this? Is it just a necessary evil in an auto anc business / fast growing company which is unable to manage inventory properly or does it point to some potential issue in the financials at a later date / structural issue in the business?

I was reading one of recent concall: their business model consist of 73% exports which accounts for higher margin and for exports generally the working capital cycle is high(since the overall manufacturing process is higher).

“I will also add what JJ said. Look, Devyansh to tell you very clearly when export

is growing, when our business is growing, Obviously working capital will

grow. So there is nothing to shy away from that WC will grow because, you

know, l our work here because if we are growing every year, 20 to 25 % and

30% obviously a major growth is coming from exports market. Obviously

export receivables, nothing is going to change for me. Because if shipping time

is 70 days, shipping time is 70 days. You will can’t really do much. Eventually

customer has to pay its own receivable time”

Thanks @DeepValue7 - I read that comment as well on the earnings call. My only contention here is that there are lots of export oriented auto ancillary companies that don’t carry 350 days of inventory and such large working capital. 135-150 days is perhaps a more reasonable number for export oriented manufacturing businesses. This is the part that makes me nervous both about the quality of the business (since their current valuation implies ~40x normalized FCF) and about whether the inventory is appropriately valued. Has anyone done any scuttlebutt on this that can provide any comfort or otherwise?

My view on the inventory build-up.

Think of RACL’s products, they are gear / gear blanks. They need to supply to the customer throughout the year, however the demand for a single SKU is not significant that they can have a Just in time sort of a process. [ refer to Sahil’s post ].

So they have a batch process where they make 10000-20000 such gears and and that gets sold over a year based on customer forecast. They also ( apparently ) keep the inventory near the customer location so the the customer does not have to wait for a incredible amount of time in case of a demand surge ( can go to upwards of 2 months). They carry the inventory on behalf of the customer and the customer is also delighted . What is important for a RACL type business is if Tier 1/ OEM start to engage with them at the design stage itself for building such relationship and maintaining quality. In the auto space this relationship is a superb moat.

Majority of the drop in EBITDA appears to be from raw material costs (up 32% vs revenue up 22%). Even that is seen in consolidated result only so this is from their Austria subsidiary where ~3.6Cr of revenue is seen compared to ~5.2 Cr of material cost.