Racl Geartech New website is live now

https://www.raclgeartech.com/

Few good videos in background about the plants and information about products.

Racl Geartech New website is live now

https://www.raclgeartech.com/

Few good videos in background about the plants and information about products.

RACL had quite an interesting call, they have been able to develop and win orders for new products from new customers. FY24 growth will likely be ~15% due to execution issues, but orders are secured and once these issues normalize, growth should improve. Concall notes below.

Sales slowdown

Customer specific

Capex

New projects

Margins

Disclosure: Invested (position size here, no transactions in last-30 days)

HI @harsh.beria93 @Worldlywiseinvestors Can you guys comment on the debt to equity ration for this, as per screener it is 1.36, I don’t feel comfortable with more .6 debt/Equity. AM I missing something here. Thank you in advance guys.

Regards,

Rajiv

RACL Geartech -

Q2 FY 24 highlights -

Sales @ 103 vs 90 cr

EBITDA @ 25 vs 23 cr ( up 9 pc, Margins at healthy 23 pc )

PAT @ 10 vs 10 cr

Product range -

Transmission gears and Shafts, Sub assemblies

Precision Machined parts

Chasis parts

Industrial gears

Product applications -

2, 3 Wheelers, TVs, CVs, Agri eqpt and industrial gears

Manufacturing facilities - 02

Warehouses - 03 in Europe

Comments from Concall -

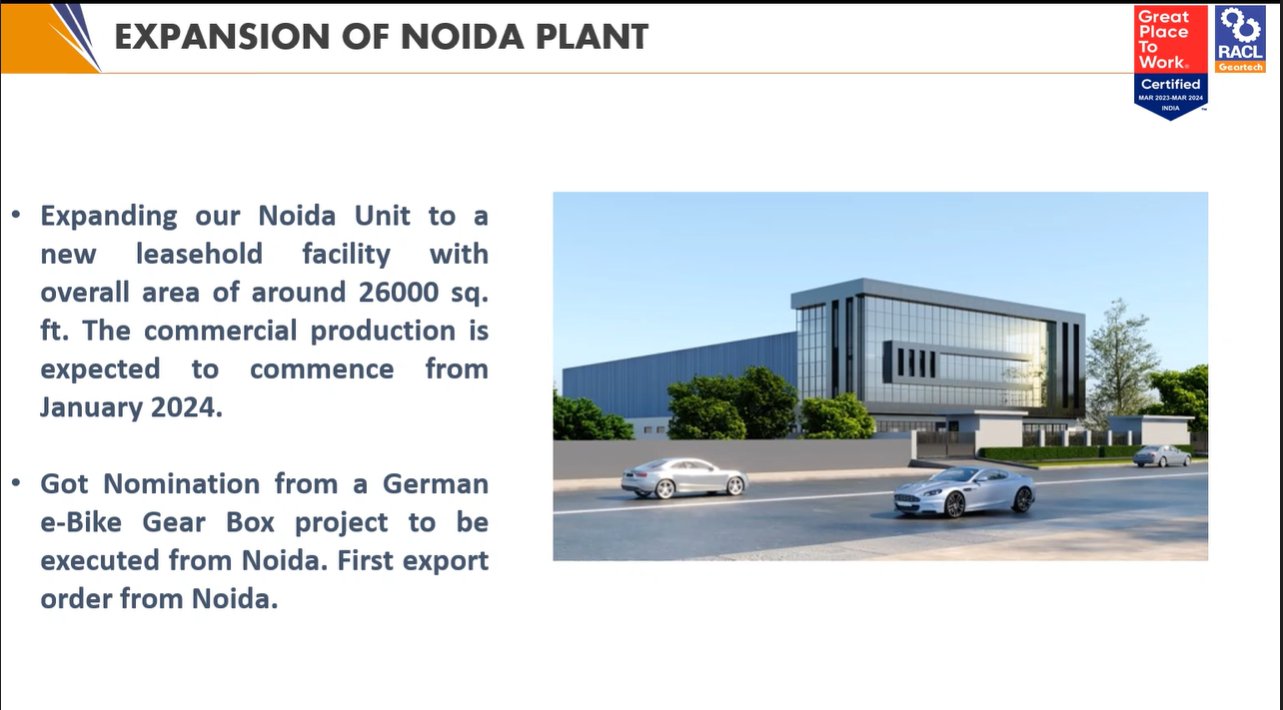

Expanding Noida facility with additional leasehold area of 26k sq ft. Commercial production to start from Q1, FY 24. Samples shall be produced in Q4 this yr

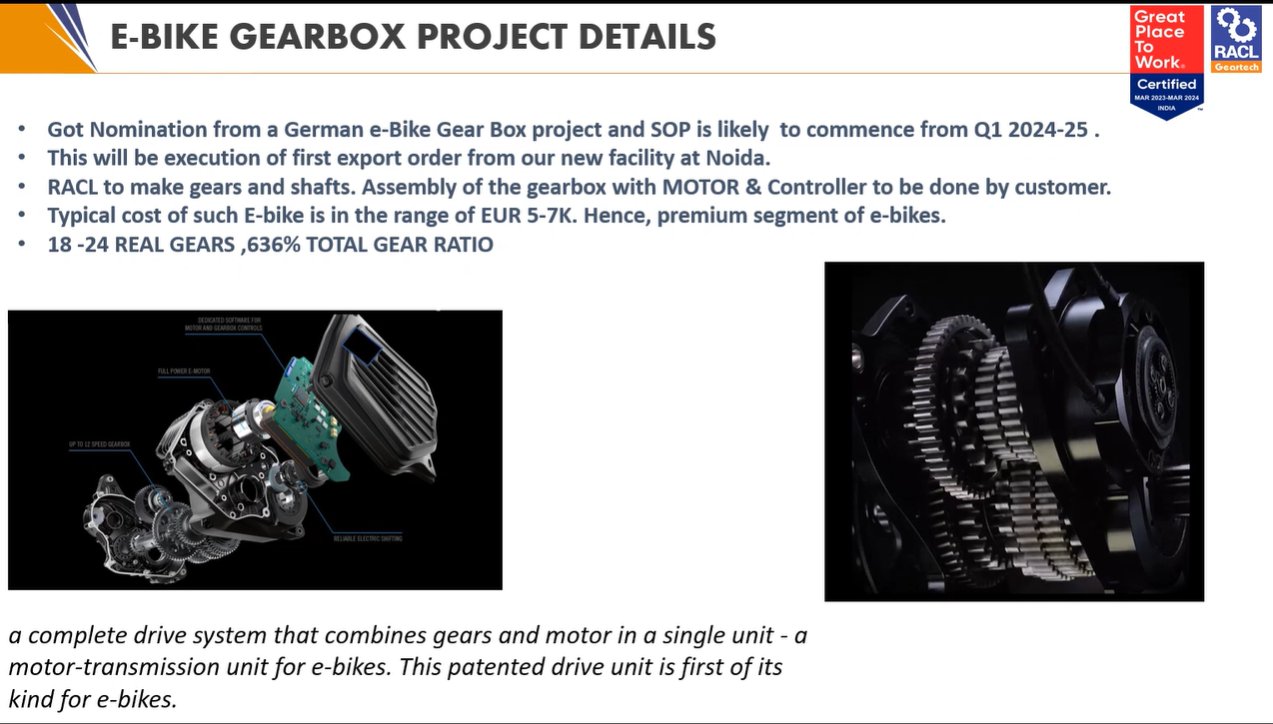

Nominated for supply for gearboxes and shafts for a German electric- bicycle player. To be made at the new expanded facility. These are premium bikes costing around 5-7k Euros. These kind of bikes are gaining huge popularity in Europe. The German customer has a patent protected technology for this bike.

Nominated for supply of wheel axle for KTM Austria for their 1300 cc super bike

Another customer of the company - MAN Trucks had some of its projects delayed in the current FY. Company supplies transmission gears and axle shafts to them. By Q4, supplies to MAN trucks should begin. Supplies to MAN should be a big growth driver in FY 25

For FY 24, growth guidance has been moderated to 15-20 pc from earlier guidance of 25 pc. Should go back to 25 pc kind of growth rates wef FY 25. Reason for the same is because the company could not get its hands on gear-grinding machinery ( very high end machinery ) due various supply bottlenecks and shortages in Europe and Japan from where they r imported. Most of the issues now stand resolved

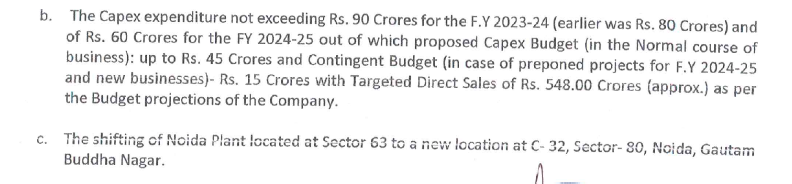

In FY 24 - company is expected to spend 80 cr on Capex. FY 25’s capex plan has not yet been finalised

The newer orders that company is getting have greater degree of value add. Hence there is an upward bias in gross margins

Company’s supplies to BMW’s R-1200

( upgraded now to R-1250 Bikes ) is a high margin, high value addition business. Its likely to continue that way till 2033 !!!

KTM has expanded into China and is doing good business there as well. RACL remains their supplier even for the bikes to be sold in China. This should help RACL grow with KTM

Still aim to hit the Rs 500 cr topline by FY 25 end while maintaining the same margins

The China + 1 sentiment and the high inflation and energy prices in Europe have been a tailwind for the company and other Indian manufacturing companies too

Disc: holding, biased, not SEBI registered

Five Rules (Pat Dorsey Page 89) probably this will help you understand. In case I am wrong others can rectify.

Thanks Vivek, I got some idea, will go through Pat dorsey page.

**Alert Good news RACL Geartech Limited has recorded the

highest ever Monthly Sales of INR 41.07 Crore in the month of December, 2023. **

https://www.bseindia.com/xml-data/corpfiling/AttachLive/a70be1b2-fc5d-4542-a0f5-a221423f3be8.pdf

a70be1b2-fc5d-4542-a0f5-a221423f3be8.pdf (178.4 KB)

I also found another news more interesting and provide more insight into management thinking. They have hired Mr. Arora as HR head who has experience of 20 years in this field. He should help in talent hunt and building leadership pipeline in the company to take it to the next level.

UP state govt awarding RACL for highest export in FY 22-23 in engineering category

CROIC (Cash return) is negative. It is (-6.92%)

Still stock is good to have in the portfolio

Hi Jeewan,

Could you explain why is CROIC negative? Is it because the company is not converting revenue into cash fast enough because of which the cash flow from operations are negative?

What is your read on the fundamental reason behind negative CROIC?

Aadhar

Hi @aadhar.aggarwal and @jeewangarg

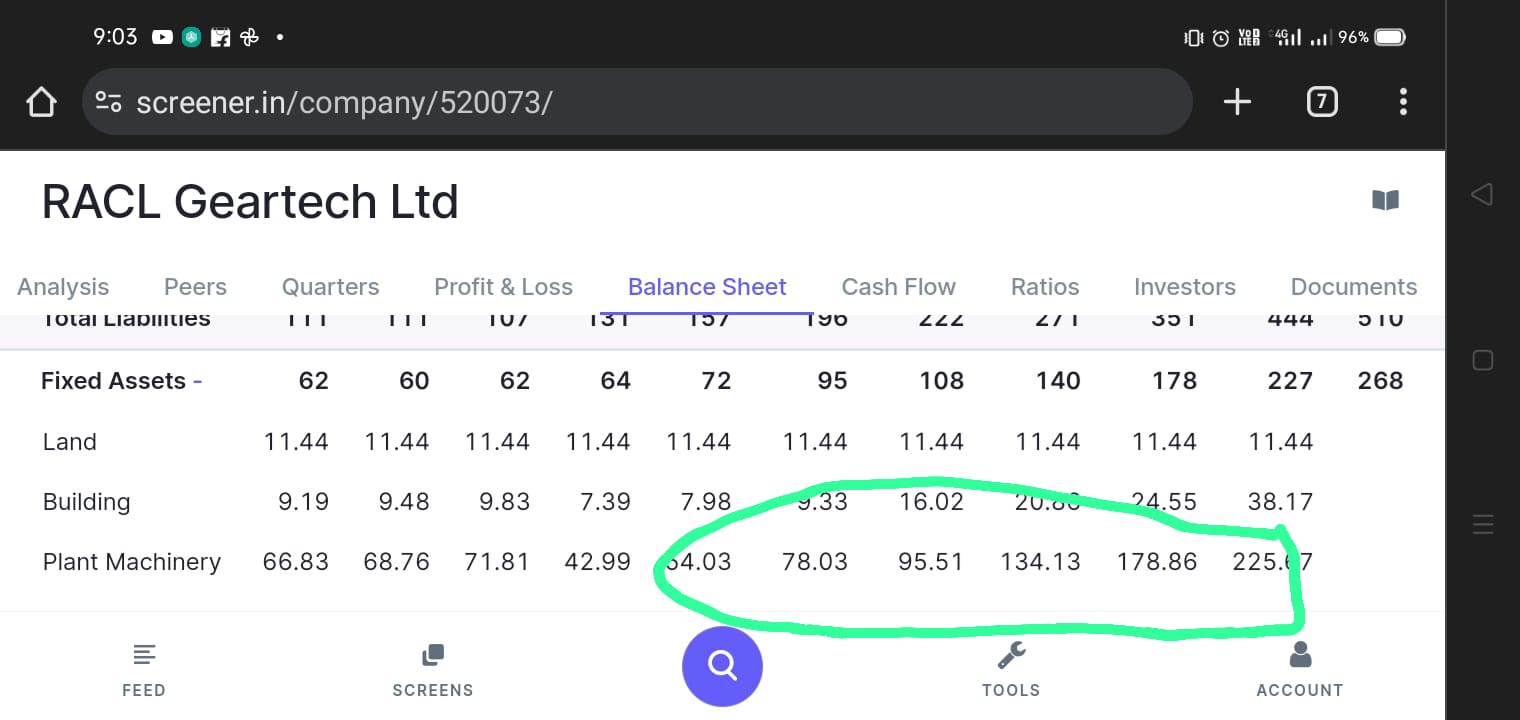

RACL cash flows from operations are positive and even if you include interest paid, they generated 40cr of free cash flow in '23 which they used up in buying fixed assets of 78 cr in '23.

I am not sure what CROIC is but I think if you look at the regular return on equity of the business it’s more than satisfactory at 25%+

Best

Ok. I think I misunderstood earlier. So you are saying that the only reason that they are not generating net free cash flow is because they are buying fixed assets more than the cash the business is generating?

CROIC is the free cash flow generated divided by the capital invested. This will be negative if the net free cash flow is negative. And I suspect in the case of RACL the net free cash flow is negative because they are buying fixed assets of a higher amount than the cash that they are generating from their business. Please corroborate.

it’s used to grow at 25% go 30% , which has come down in last quarter, so the PE is adjusting itself.

Disclosure- I was holding the stock before results and sold it next day after the result

I think the market is also becoming aware of the fact that there are some scalability issues because of the nature of the business they are in.

I understand there are substantial contract wins, and the top & bottom-line prospects of the company in the future also look good. However, it requires significant investment for the company, not just in allocating capital for fixed assets but also in a skilled workforce and retaining the same over time. The complexities of the products they build are reflected in their margins. Still, in my view, the scalability for such a business is all about execution, and with increasing size, investors cannot think of any non-linearity in the growth of the top-bottom line for this company.

Disc: small tracking position

Is there any Capex plan as per latest concall ?

Results are out. Muted one. Top line up 15% and PBT up by 4%. But more interesting parts is in the notes

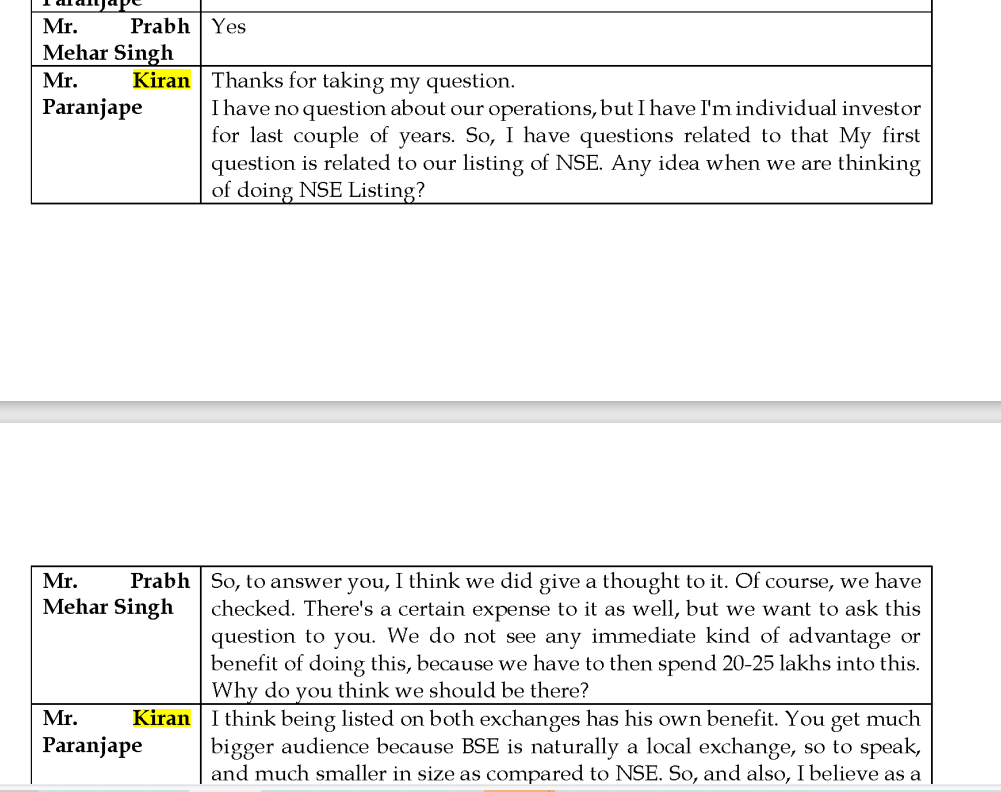

NSE listing is big news along with next year sales target of 550 Cr