RACL GEARTECH

ELEVATOR PITCH

Export Driven - Marquee International OEM Clients: RACL has emerged as a Tier1 supplier to OEMs like BMW Bikes, Kubota, KTM, Schnieder, Man Trucks, TVS (manufacturing for BMW/TVS). Highly regarded process design innovations from RACL have won it exclusive contracts like the 10 year single vendor BMW bike contract. Recently made headways towards becoming a Tier2 supplier to Mercedes, Porsche, BMW cars via ZF (started in 2020). More than 70% of Sales is export driven

RACL DNA - Strong Client Penetration Focus: Numerous examples like RACL Kubota relationship starting with 2 components in 2004 to supplying over 110 components today. RACL’s client being acquired got it a foot-in-the-door with BMW to becoming exclusive supplier for some of its products. Initial contract from ZF to deliver luxury/premium 4W OEM components (2021) to delivering three years targets within the first year. Higher manufacturing costs in Europe is providing increasing tailwinds for outsourcing of manufacturing of complex and capital intensive parts to competent suppliers like RACL. Bulk of medium-term growth is driven by committed demand from ZF, Man Truck and other marquee relationships leading the company to commit unprecedented 250 Cr Capex plans.

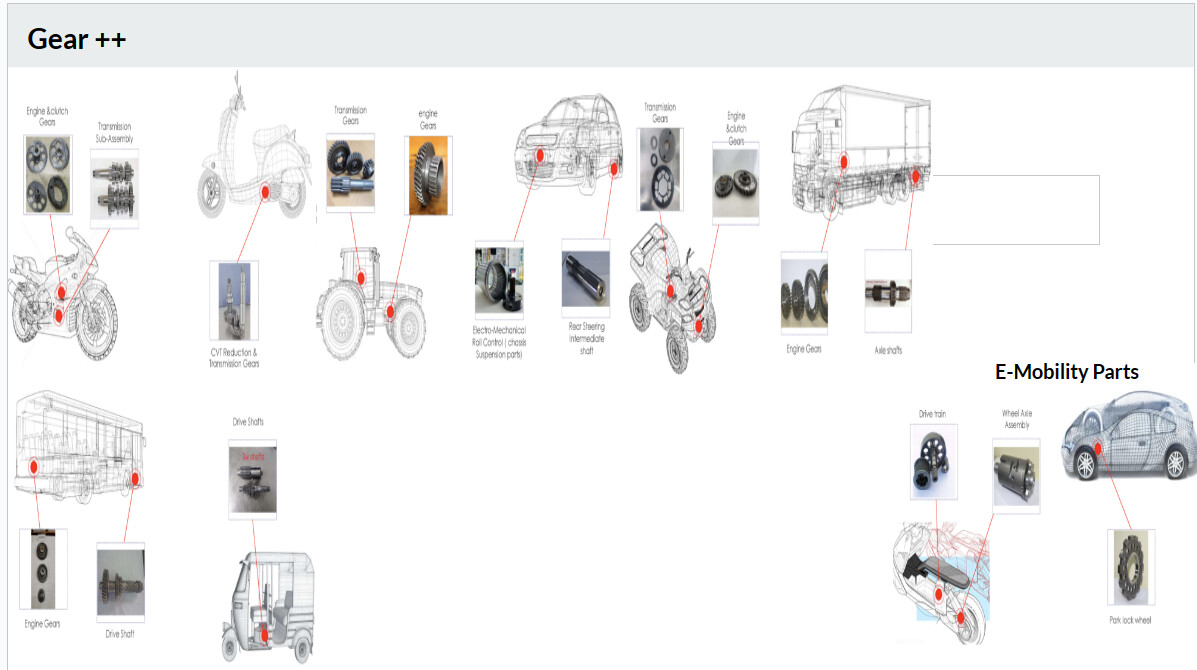

Moving up the Value Chain: RACL has moved up the value chain from pure component supplier to a Tier1 sub-system supplier for a reputed international OEM. While transmission gears is the bread and butter segment for RACL, it also manufactures industrial gears, precision machine parts, steering and suspension components, chassis, shafts, drive trains, painting. Additionally, it is getting into the forging business both as a backward integration as well as providing it as a core service to customers.

Well-Diversified Sustainable Premium Niche Markets: RACL manufactures transmission gears and other auto components across full range of 2W, 3W, 4W, CV, ATVs, Tractors, Battery Bicycles - with carefully chosen niches for high-end OEMs. The niche premium segments face lower demand cyclicality/margin pressures. Notably, RACL is already present in the EV value chain and getting future-ready for eventual migration to EV ecosystem demands of OEMs

Industry beating Quality benchmarks: Auto-Ancillary Industry operates with stringent quality norms. While typical contamination levels are set at a threshold of 100 per million (PPM) by OEMs, RACL is operating at 25 PPM - primary reason for it emerging as the preferred supplier to many premium customers. This not only reduces rejects (no recalls till now for RACL) but cements stronger relationships with OEMs and helps penetrate deeper into every account

High Working Capital/Debt challenges: RACL business model with leading OEMs entails extended receivable cycles. In order to generate cash, RACL does bill discounting with optically lower receivable days (than actuals). Product manufacturing in low-volume batches (instead of assembly-line high volumes) results in low Asset Turns. To grow the business RACL needs to continuously invest in Capex limiting its ability to reduce debt levels and/or generate free cash flows. Current debt levels are high (Sep '23 250 Cr w/o bill discounting) - probably the only real counterpoint to a strong investment case for RACL.

CURRENT MARKET/INDUSTRY TRENDS

As the company is focusing on the premium end of the market, the trends for the growth in the underlying industry has also been taken for the premium segment.

Two Wheeler

While the overall industry of two wheelers is expected to grow at a CAGR of 1.58% from 2023 to 2028, the premium two wheeler (motorcycle over 250 CC) is anticipated to progress at a CAGR of 9.6% during the forecast period, 2021-2027 (According to Gen Consulting Company)

Source: Global Premium Two Wheeler Market, 2021-2027 (marketresearch.com)

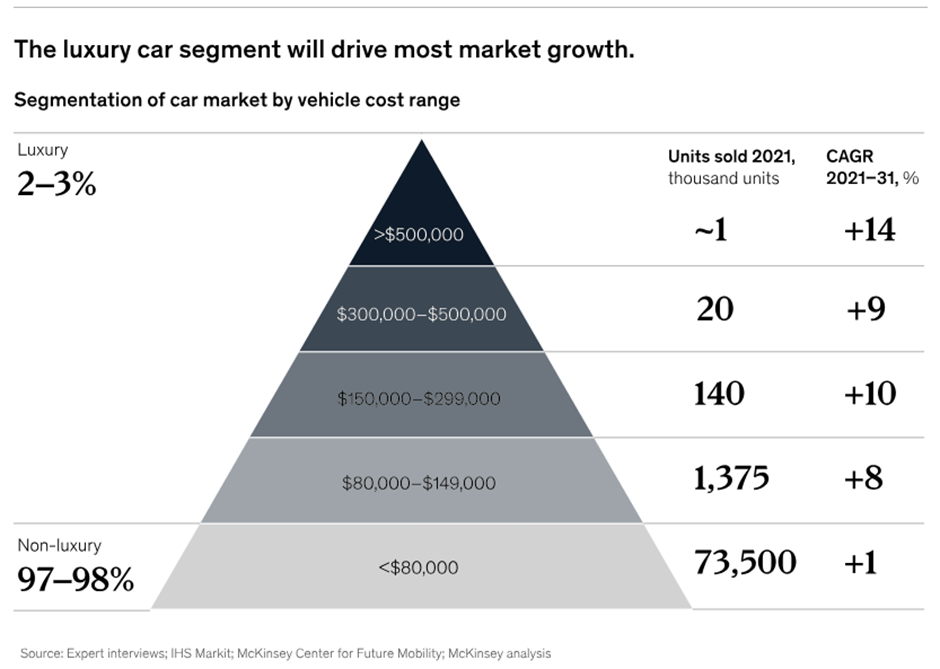

Four Wheeler

Similar trend of luxury sales outpacing the growth of overall industry is also present in the four wheeler market, with the luxury segment expected to grow between 8-14% while the mass market expected to grow at 1% till 2031.

Source: The luxury car market: Five new industry trends | McKinsey

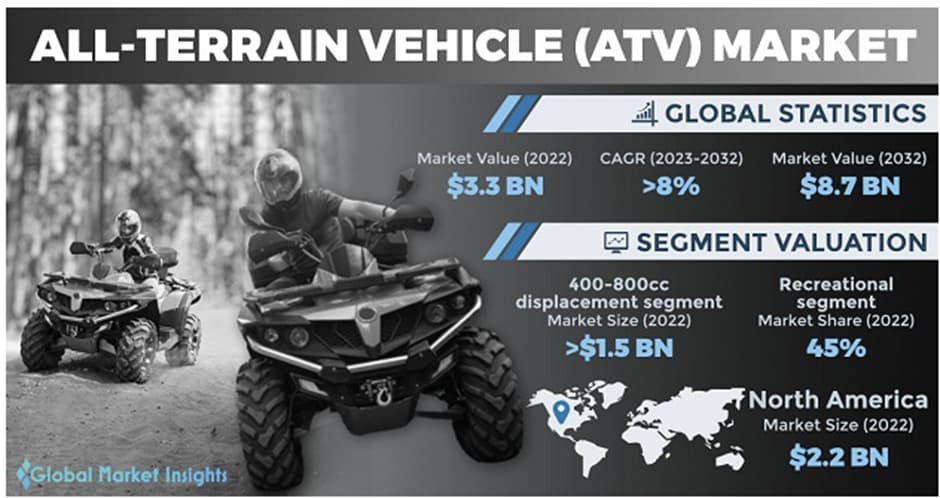

ATV

Source: All-Terrain Vehicle (ATV) Market Size, Growth Report 2032 (gminsights.com)

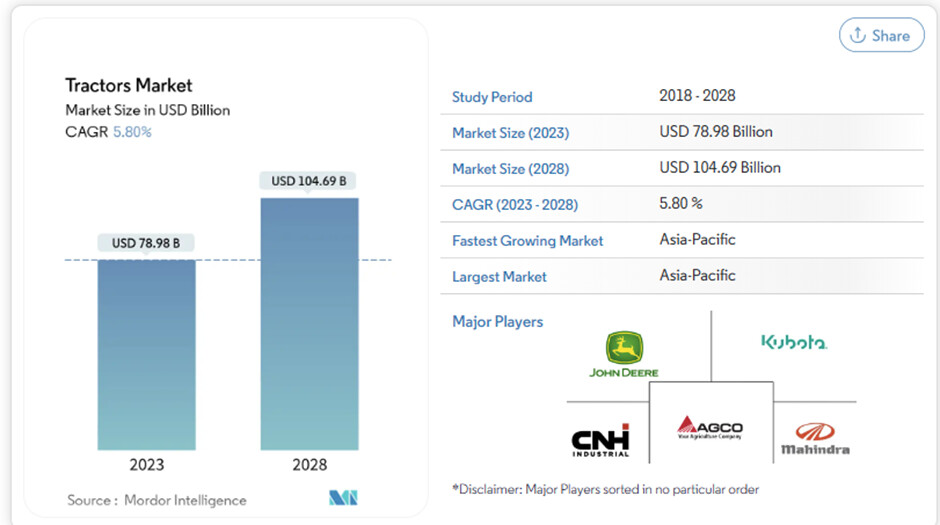

Tractors: Unlike vehicle segments where its clear on the segment that RACL is serving, in the tractor market the end client picture is not so clear. RACL currently services Kubota as well as Escorts and therefore might be present in both the premium and economy segment, and therefore the overall industry growth trends have been captured below.

Source: Tractor Market Share & Size (mordorintelligence.com)

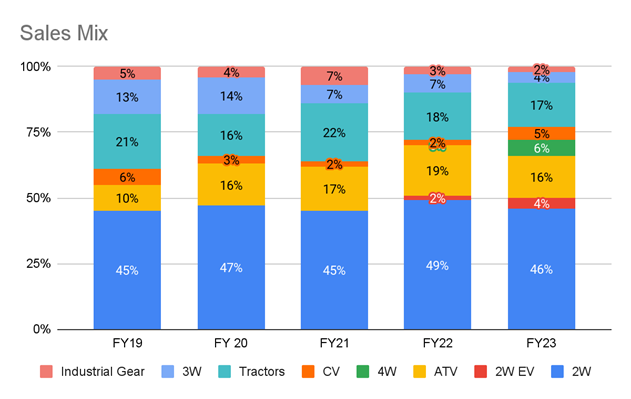

However, it is also important to note, that while the company initially focused on generating business through tractors, over the years it has diversified into 2W and 4W which now comprises >80% of sales; with sales growth also expected to come from non-tractor lines of businesses, e.g. ZF for luxury 4W and MAN trucks

In summary, the premium segment across the vehicle ranges are growing any where between 6-10% implying a fast expanding market for the company, which is also trying to enter into multiple other components to insulate it from the transition from ICE to EVs.

BARRIERS TO ENTRY

- Product quality in highly critical component → while customers have an acceptable tolerance rate of upto 100 PPM, the company has been able to consistently deliver within contamination rates of 25-50 PPM leading to quality reliability. This the company has been able to deliver by importing machines and operating the manufacturing locations in an air-conditioned environment (which reduces entry of dust particles).

- Long OEM approval cycles → Like for any auto OEM, part approval and design is a long drawn process and for any new product the process starts atleast a couple of years ahead of the launch. And therefore for any new player to make in-roads into RACL’s business will take time unless there are quality issues arising at RACL

- Process R&D → While the company doesn’t do any product R&D (i.e. creating new products), it invests in process R&D with 10-15% of employees working on the R&D to deliver reliable products probably on a more economical basis and higher quality.

Driven by the above factors, it becomes difficult for a new player to rapidly acquire new customer and gain wallet share, thus leading to customer stickiness.

BUSINESS MODEL

Product and Manufacturing:

-

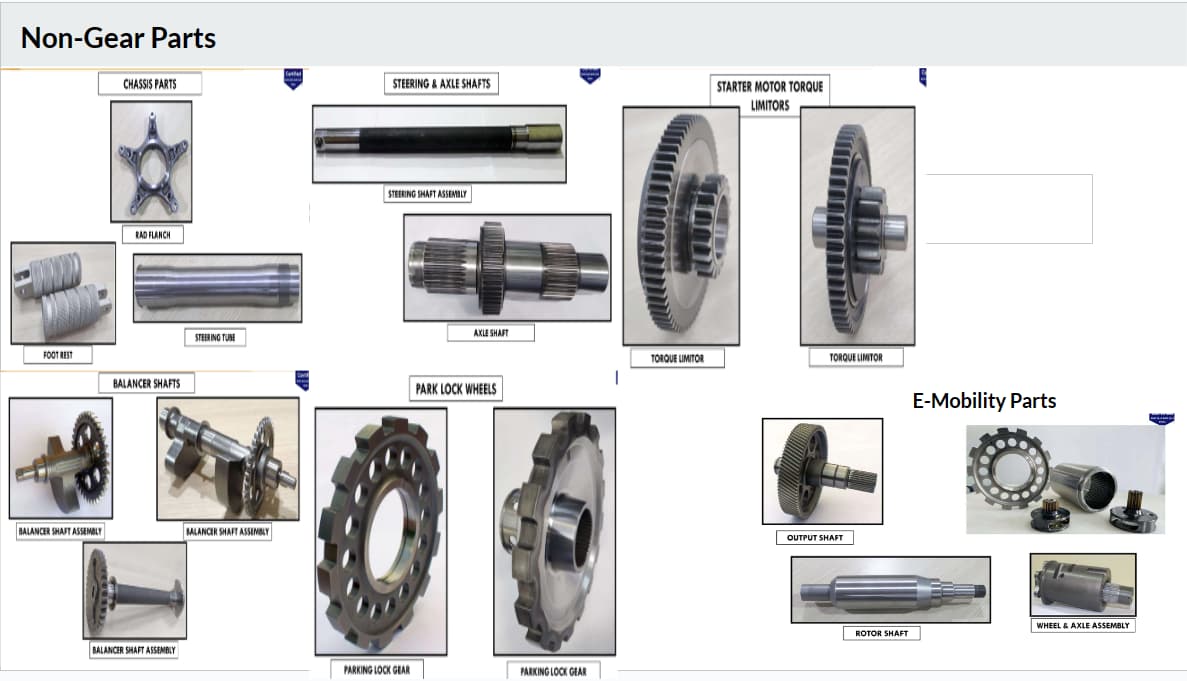

Company main business is of providing transmission gears, while also providing other components (Steering & suspension, chasis, e-mobility parts, axle shafts, torque motors, balancer etc.) as its offerings; refer to the product offerings below:

-

The products especially transmission gears, while not significant in the overall costs for the OEMs, is a critical component for the vehicles, and therefore the product goes through rigorous testing and quality check cycles before scale-up from any vendor; the products have a high quality requirements of less than 100 defective parts per millions, while RACL has been able to maintain standards of 25-50 PPM with no product recalls.

-

Customer provides long range plans with respect to product requirements, and RACL manufactures these products through mix of in-house manufacturing and job-works

-

The company’s major production happens through its plant in Gajraula, UP which has enough area available for expansion for the next 2-3 years; there is an additional plant in Noida which has been dedicated to producing for a single client (in Q3FY24 the company has expanded its Noida facility to manufacture for electric bicycle products, and this facility also becomes an exporting location)

-

Company’s IPs: The company is focused on doing process driven R&D work (and doesnt do product R&D i.e. developing new products), wherein the OEM comes with the product design and specs, and the company works with the OEMs to bring the product to realization (therefore it can be assumed doing it economically while maintaining quality requirements)

-

Company’s Gajraula plant is fully AC to prevent settling of any dust on the machines and avoid/reduce contamination levels

-

Company in collaboration with clients has been part of manufacturing of unique parts such as Yoke for rear tyre of bikes or steering shafts using actuator for rear steering (ZF product)

-

The company was earlier focused on Tractors, ATVs and 2Ws as their main lines of business, however in the recent years the company has also entered in the 4W and EV domain, with both of them combined having contributed 10% of sales of the company.

-

The products are low volume, in the nature of batch manufacturing, which is both +ve and -ve for the company;

+ve in the following sense:

- product volumes being low and batch produced therefore large manufacturer/auto ancillary may not enter

- given demand is low and there are peak cycles of demand, the company ends up manufacturing and keeping inventory upfront to service the projected demand, this leads to inventory build-up affecting cash-flows, which also makes it a bit challenging for new player to disrupt RACL.

-ve in the sense that the business will not be able to scale-up at a fast pace, and there would be challenges in working capital management, which is something that the management has also acknowledged

Customers and Competition:

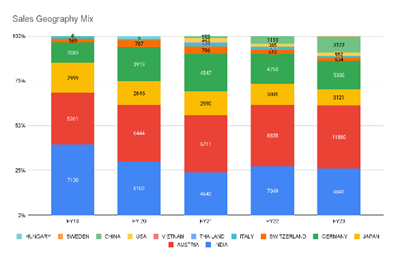

- India sales comprises about 24% of FY23 sales for the company, the dependency on the same has been continuously reducing driven by addition of international clients by the company

- The company typically operates on the principle of acquiring one big client in 2-3 years and then grow their wallet share/sales, stabilize the relationship and then add another client again. (This is something similar to establishing relationship with ZF in 2021, ramping up business over the next 2-3 years)

- The company believes in limiting excessive exposure from a single client, their top 5 customer contribute 67% of FY22 sales and top customer is 17% of sales; company as a practices prefers limiting any clients share to max 20-25%

- In India, there are other players who are manufacturing gears (e.g. Shanti Gears, Bharat Gears, Hi-Tech Gears etc.) but they are not operating in the same product range as RACL; in addition to this, players like Hero Motocorp have their own captive companies manufacturing gears for them, not allowing RACL to create a foothold among Indian OEMs

- Competition majorly is international coming from China, Japan (Musashi), Taiwan, Italy (Dana graziano transmissioni); In India competition may arise from players like Sona BLW (in EV domain), Musashi India (website)

Supply Chain and Working capital:

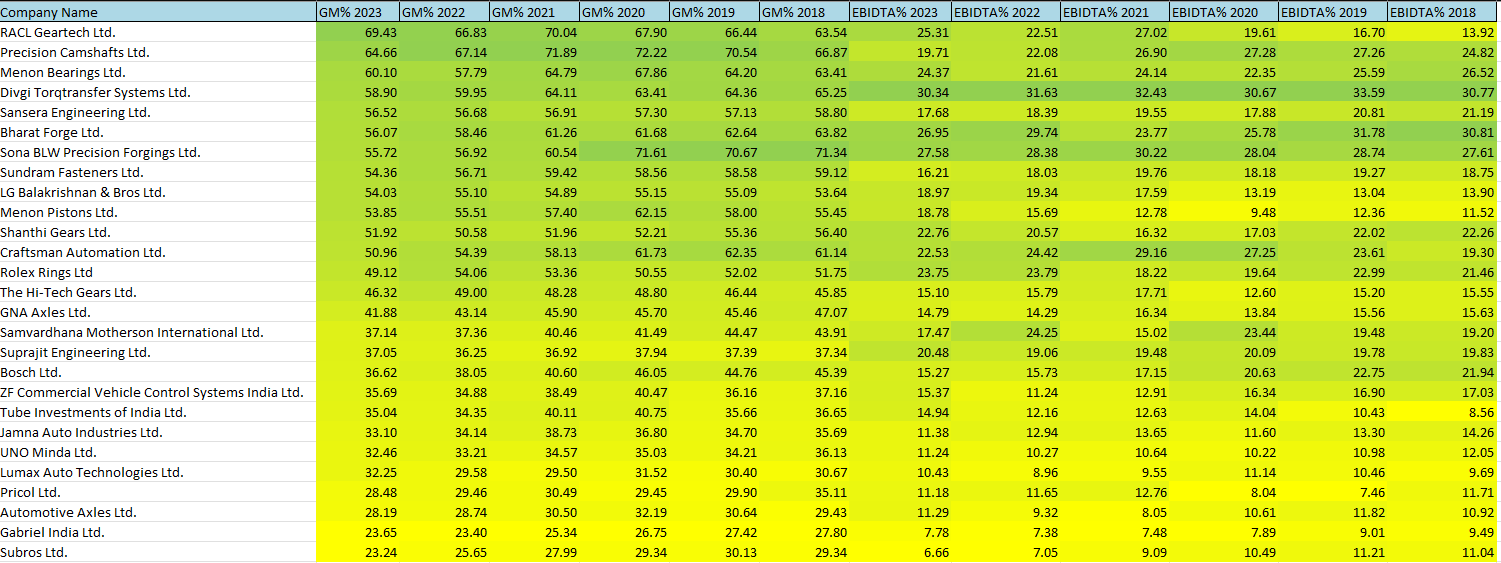

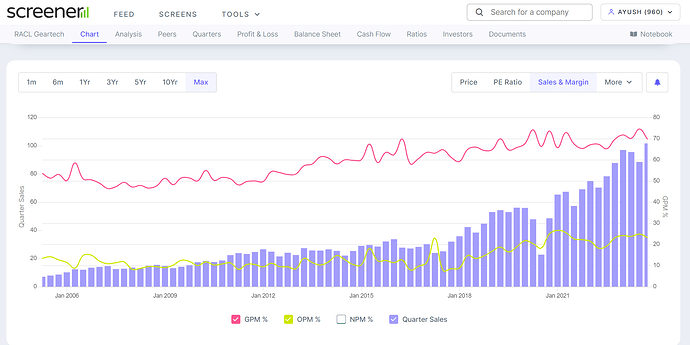

- The company has been able to maintain its gross margins (~65-70%) and EBITDA in the range of 17-20% reflecting company’s ability to pass on any RM volatility to its end-customers, reflecting value-addition and lower impact of raw material volatility

- While the gross margins and EBITDA are high compared to peers, the working capital cycle gets extended due to the nature of supply chain

- As most of the products are export oriented (~70% of revenues), the company ships out its equipment from Gajraula to ports via road-transit, which then gets transported to the customer, leading to elongated working capital requirements for the company (this causes the working capital to become at least 75-100 days on the exports side)

- ~53% of sales are made to European markets, which operates on a skewed production/ sales cycle, wherein 70% of demand is generated in a period of 4 months; in order to manage the overall capacity, the company ends-up stocking of raw-materials during the lean periods to service the peak demands, which ends-up increasing their working capital cycle.

Raw Material and Other costs:

- Steel is one of the most important raw-materials for the company to manufacture its products, on an overall basis, total raw-material costs have ranged between 30-35% of revenue

- Apart from the raw-materials, other major cost line items for the company includes job-works (10%), spares (7%), Power (6%) followed by Freight (3%)

- Machines bought for manufacturing: RACL competes with Chinese companies to procure the machines which are in-turn used by RACL to manufacture its products. The company in one of its concall had mentioned the fact that the machine supplier products are being taken away by the Chinese players and RACL is unable to procure its desired number of machines (refer transcript below).

Negotiation capability:

- Even though the company provides critical components to the OEMs, the company has limited negotiating capabilities given the size of the customers, and also the end-customers having alternate vendors to source from.

- However, ability to pass on price hikes has been demonstrated, implying pricing discipline and execution of contractual agreements

- Raw-materials: Given steel is the major raw-material, it is expected that it would be sourced from a mix of small and bigger players and thus the company may not have the strongest of negotiating power either on margins or payment terms; while the company also relies on smaller SMEs for the job-work, the regulations mandate payments to be made within a period of 45 days.

With the above context, applying porter five model on the company

- Customer Power: High

- Supplier Power: High

- Threat of Substitution: Med

- Competition intensity: Low

- Threat of new entrants: Low

INTERESTING VIEWPOINTS

-

Marquee Clients: As mentioned earlier, the company has been manufacturing for large international brands such as Kubota, Mercedes, BWMs (Car and Bikes), KTM and its not common to find a small company dealing as a single/main source supplier to such very large MNCs like BMW, Kubota, KTM, ZF etc. In many cases, RACL started with just one part to one of their parts and has been able to build trust and get more orders for more parts and multiple plants of those cos. Eg - KTM. When KTM went to China, they also brought RACL for CF Moto. Additionally, RACL supplies to both BMW and KTM, and its not common to see two competitors buying from the same supplier (entire gear solution is provided by RACL)

-

Ability to sustain high gross and EBITDA margins → RACL is among the few auto-ancillary companies which has been able to demonstrate gross margins in excess of 60% across an extended period of time while entering new verticals (implying no discounting led approach to grow business), and in addition to this being able to grow EBITDA margins clearly demonstrating the effect of operating leverage (single plant, with new installations and upgrades focused on automations)

Below are the historic Gross and EBITDA margin trajectory for the business

-

Sourcing Agreement with ZF → ZF has announced to double up its sourcing from India to 2 Bn USD; RACL had established a relationship with ZF during COVID period and since then has started providing parts to Mercedes, BMW, Lamborghini; RACL has also created its latest plant as a dedicated plant for ZF. Specifically with respect to the ZF partnership, it must be noted that when ZF gave the business to RACL, it was because of the superior engineering and innovation that RACL brought to the table. It’s one of those rare cases for a company like ZF to be outsourcing some critical component to Indian companies. They in fact closed their capacity and gave order to RACL. The company has also been able to deliver complex parts which exceeded their customer expectations pointing towards the process R&D capabilities of the company (for example, The complex 3-level gears which ZF used to make in 3 parts, RACL was able to make with single part (no welding) which leads to higher structural integrity & reliability.); Additionally RACL manufactures 7 products for ZF which are exclusive to RACL (i.e. no one else manufactures these parts)

-

10 year single supplier order for BMW 2W EV: The company was involved in the design process from the start to design the e-Axle and Kinematics for the 2W EV for BMW. While the company didn’t initially have the capabilities to deliver these products, over a period of 2-3 years, RACL was able to deliver the products, and was able to bag 10 year sole supplier vendor status for this prestigious 2 wheeler (New BMW CE4: Link)

-

Suppliers to Mahindra EVs (from Reva times): EV reduction gears is not something that is new to RACL, it has been a supplier to Mahindra REVA (one of the first commercial EV 4W in India) again demonstrating its ability to deliver on new technologies

-

Conservative Capex Investments → The company follows the process of creating capacity against confirmed orders/order book, implying conservative capacity expansion. The company is moving ahead with large capex cycle of 250 Cr which will be finished by FY26/27. This capex is eligible for UP government subsidy wherein 20% of capex (of 250 cr) to be refunded back over 12 years. Given the longstanding Capital investment track record this largest ever capex, implies large order pipelines/confirmed orders for full capacity utilization. Additionally, the company has enough land at its Gajraula plant that it can double up its revenue, implying lower capex intensity versus a greenfield set up

-

Ability to redeploy cashflows at scale with consistent ROCE:

As can be seen from the highlighted values, the company has been continuously deploying its cashflows into doing further capex to grow the business, however even though the capex has been happening, the company has been able to maintain/increase its ROCEs.

BULLISH VIEWPOINTS

-

Premiumization as a trend → Given the recent K-curve recovery or premium side of the economies continuing to do well, the demand for premium vehicles is expected to remain robust; any major economic recovery across the developed world should further boost the demand for the products. Additionally, the company has been able to enter and expand its offerings/wallet share among its customers through adding new product/segments

-

ZF Sourcing major growth driver → RACL has followed a pattern of acquiring new major clients once every 2-3 years and then growing the relationship. ZF account is one such premium account; given ZF’s focus on increasing sourcing from India (as part of China+1, or other reasons), The new plant built for ZF houses 7 products which exclusively RACL is doing. 100% supplies. RACL can also grow along with this increasing trend of India based sourcing e.g. it got orders for providing chassis components for BMW of 700K/year volumes, rear steering actuator for Porsche etc.

-

In-house Foundry->Till recently, the foundry work was outsourced, the company has subsequently started in-housing of foundry work which will aid margin expansion. Additionally, the company was approached by an OEM to provide foundry as a standalone service to them e.g. manufacture of Yoke component for BMW (supplier in France went bankrupt, and RACL was approached by BMW for manufacturing first in the world component). 50% in-house forging done by RACL, balance is to external vendors like MM Forging.

-

MAN Trucks Uptick in Orders-> While MAN Trucks has been a client for RACL and demand ramp-up is expected, there is an additional fillip as MAN trucks has closed its machining and forging unit for ICE in India, and RACL expects those orders may come to it in the next 2-3 years

-

T1 Supplier to European OEMs Optionality->Another optionality that exists is for RACL to become Tier-1 suppliers to the luxury brands over a period of time, as for BMW 2W side they are already supplying directly to them, this would aid in margin expansion. Something similar on this line has already happened, when in Q3FY24 the company announced that it received an order to manufacture a sub-system for parking lock mechanism for a European sports car manufacturer in a Tier-1 capacity.

-

Succession Planning in place → Small cap companies often face succession planning issues which leads to the business not scaling-up or withering away over a period of time. However in RACL’s case, the promotor’s son Prabh Mehar Singh has been leading Finance and Business Development functions of the company, thus potentially ticking off any succession planning issues down the line. Though it may be noted that Mr. Gursharan Singh is 61 years old and therefore can drive the company for the foreseeable future.

-

Euro+1 theme → Given the war in Europe, the manufacturing+power costs have shot up making the overall costs unviable for players operating in those geographies; this plays well for RACL as it can attract demand from European OEMs e.g. one of the vendors to BMW went bankrupt post war, and BMW asked RACL to manufacture an industry first part of yolks which allows the rear tyre of a 2W to move without chains.

In similar vein, due to increased energy costs, European companies are moving towards higher value add works of designing while moving out manufacturing to lower cost countries, which may be beneficial for RACL given the concurrent running China+1 theme.

BEARISH VIEWPOINTS

-

Transition to EV → As vehicles transition towards the EV drivetrains, the number of gears that are required reduce significantly. While the company is capable of producing EV reduction gears (which meet the lower noise level requirements), it also mentions that volume might get lowered, however the value add (and thus margins) is expected to be higher vis-à-vis gears for ICE due to higher technical requirements/specifications.

There remains a chance that the whole transition to EV may lead to idle capacities (as lower volumes) combined with new ancillary players emerging along with new OEMs -

Client Disruption Risks: RACL’s story is tightly linked with the fortunes of the premium OEMs, however the inevitable transition (ICE to EV) can lead to new players coming up with incumbents not nimble enough to stay on top of the curve. Though not like-to-like, Ola becoming the biggest EV scooter player in India, though Ather had a larger lead time on developing EV tech and ICE auto OEMs woke up later to the market demand (and Hero not being able to scale up Vida). Something like this is happening in Europe, where China is dumping EVs which is challenging the dominance of the European ICE as well as UE EV makers (Link)

-

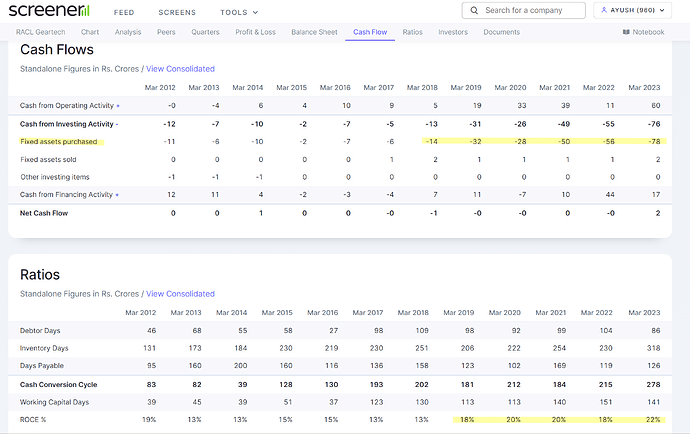

Free Cash Flows: Below is the historic cash flow statement for the company

-

High Working Capital: One can clearly see that while the company has been able to generate healthy operating cash flows, it has been able to have a positive free cash flow year only in 4 years out of 12, and in those years also the quantum of FCF has been very small, implying that the company is stuck with high working capital requirements and capex which will likely keep growing up as the business scales up (as it has limited bargaining power with its customers).

-

Increasing Leverage: Building on the free cash flow issue, with no/limited dilution, the company has been building up debt on its balance sheet to fund operations and capex. Any large slow-down among the customer demand can lead to the company facing issues with respect to its debt payments. The company has 20% of debt in USD, given increased interest rates in the US (expected to remain higher for longer) also impacts profitability negatively. The management when questioned about increasing leverage didn’t seem too concerned. This is coming from the fact that the debt is being raised to service business operation requirements of premium OEMs and thus debt servicing will not be an issue; however what happens in an economic downturn and how the OEMs behave is not certain and therefore increasing leverage remains an open point of concern.

-

Key Person Risk: Currently Mr. Gursharan Singh (61 yrs) is leading the overall business and it a manufacturing/production/technology focused leader in the company. His son comes from a finance and Business Development background, with nothing specific known on his ability to drive the R&D capabilities of the organization and there is no known second line of management in the R&D function. In any unfortunate event of Mr. Gursharan not being associated with the company, there is a question mark on who can lead the key differentiating function of the organization i.e. of the R&D. There have been several cases where in the OEMs/customers have asked RACL to design specific custom processes for them (e.g. Yolk for BMW bikes)

VALUATION MODEL

The company is targeting to grow revenues at a CAGR of 20-25% for the next three years with a capex of Rs. 250 Cr over the period of FY23 to FY 26, with the following assumptions:

- No equity fund raise and maintaining similar margins

- Asset Turnover to Gross Fixed Assets reaching 2x by FY27

- Working Capital days remaining at similar levels

- Cash Balance at the end of the year remaining close to 2-3 Cr

the profit and loss statement is as following:

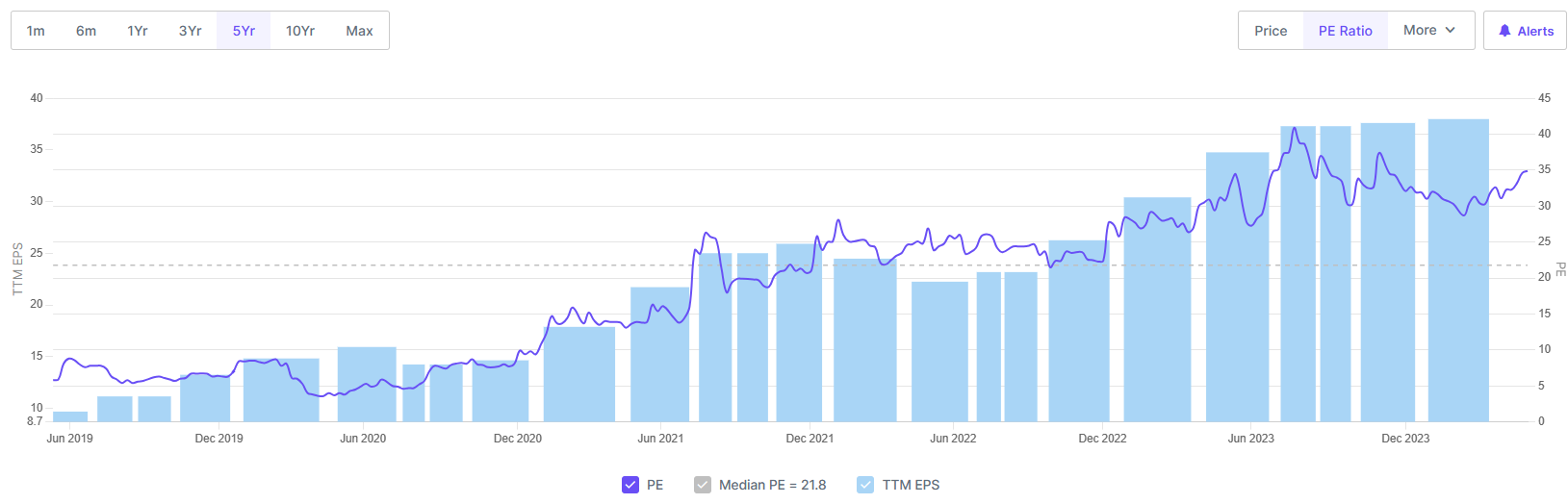

Currently the stock trades at a PE of 35, with the past five year median PE of 21.8 (refer below) the FY27 price would be 2600 giving an IRR of 22 (26% with 3yr median PE of 26)% that is incase everything positive that the management says comes to fruition.

One must note that the above IRR is the best case scenario returns, incase there is any difference arising due to slower growth, higher interest costs, lower margins or any economic slow-down the returns may be muted.

CORPORATE GOVERNANCE SCAN

Positives:

- While incidence of fund raises by the company have been limited, the promoters have infused capital subscribing to the new share issuances, reflecting promotor’s skin in the game/confidence in the business.

- No preference shares or related party transactions apart from compensation to the management

Negatives/Not so Positives:

- Wife of the CEO is on the board (not the only female board member, so MCA compliance isn’t the only driver) taking compensation of 25.95 lakhs

- Anil Sharma (RACL Non Executive, Non Independent Director) was a director on Jalpac India Ltd. which is a credit defaulter (started 30/9/2006), he was an employee of RACL for long time; exact relationship with Jalpac India is not known

RED FLAGS/FORENSIC SCAN

-

The method of preparation of cash flow statement was a bit different from industry (though nothing wrong per se), i.e. the company used to prepare the cash flow statement from PAT and then used to add back tax paid to arrive at the cash flow from operations. Post feedback from the investor community the company corrected the methodology from FY23.

-

Usage of bill-discounting to set-off debtor days: The company relies on using bill discounting to receive cash quicker (delay caused due to extended WC cycle). The outcome of this practice leads to debtor days appearing optically lower; therefore the working capital cycle is actually longer than what one sees in the statements.

-

SEBI violations w.r.t. insider trading: Order dated October 23, 2020, a penalty of ₹1,10,000/- (Rupees One Lakh Ten Thousand only) imposed on Arendra Kumar (who held 10.07% in the company) in the matter of RACL Geartech Ltd., for the violation of Regulation 29(2) r/w Regulation 29(3) of SAST Regulations; post that there hasn’t been any instances of SEBI violations

DISCLOSURE(s) OF STOCK STORY CONTRIBUTORS

- Divyansh Gupta: No position in the company, currently

- Sahil Sharma: No position in the company, currently

BACKGROUND

About the company: RACL is an auto-ancillary company which primarily focuses on manufacturing transmission gears for luxury OEMs. The company’s plants are based out of Gajraula and Noida and exports 70% of its sales to multiple countries. The company is run by a technocrat CEO who had turned around the company from BIFR status and has scaled it to a 350 Cr revenue company.

MAIN MARKETS/CUSTOMERS

RACL is supplying to top global OEMs like BMW Motorrad (Germany), Kubota Corporation (Japan, Thailand, and USA), IT Switzerland, KTM AG (Austria), Schneider Electric (Germany), Dana (Italy and China, etc.[1], with exports being ~70% of the revenues for the company.

Company supplies high precision gears to premium auto customers, and maintain a strong and resilient supply chain network. They have achieved defect free quality production with 100% On-Time deliveries.[2].

MAIN PRODUCTS/SEGMENTS

The company focuses on manufacturing transmission gears for all kind of automotive vehicles (entered 4W couple of years ago) and while this has been the bread and butter business for the company, RACL has also started to manufacture and supply new components such as steering and suspension, chasis products, forging services etc. and is supplying to same big premium OEMs as mentioned earlier. For details on the markets/geographies serviced, refer to the business model section.

SOURCES:

- Company Annual Reports, investor presentation and Transcripts

- ValuePickr Forum RACL thread

- Management posts on Twitter CEO and CFO

- RACL Plant Visit Note Oct 2023