May be, but than why to pay it out all in dividend?

Here are the notes from Q3 FY22 Concall.

-

Revenue guidance is 20% growth for next year as a conservative estimate

-

EBITDA guidance remains in 12-13%. This quarter it is 15% however CEO mentioned it is exceptional due to some projects on verge of completion

-

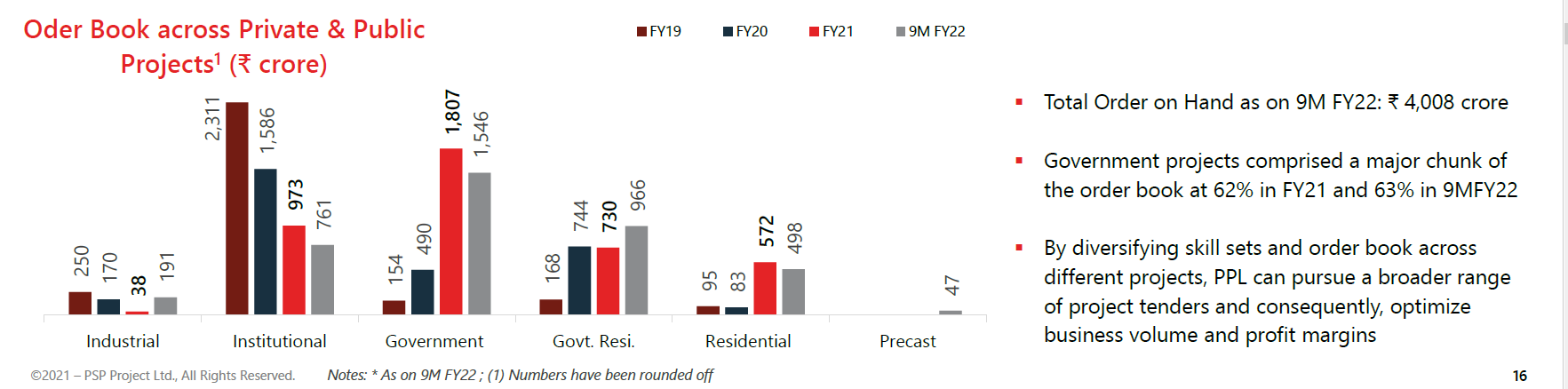

Existing Order book of ~3500 Cr which also includes 1171 Cr Central Vista project. The guidance given for order book is also 3500 Cr by Q4 FY22

-

CEO mentioned that starting from Feb 2022, once they complete Surat Diamond Bourse project (1775 Cr), they will be eligible for bigger projects i.e, more than 1000 Cr revenue

-

CEO hinted that they are looking for a project of expansion of Kashi Viswanadh dham project to other parts of India which will be more than 1000 Cr

-

The capex for the precast was 109 Cr and expected to recover the cost in 4 to 5 years. L&T has awarded the first order worth 46.5 Cr. The maximum revenue estimate for precast facility is 300 Cr per year.

-

Pandharpur project which is of order 150 Cr is right now at a halt. 20 Cr receivable amount is pending and the client is having financial issue

-

EWS Housing Bhiwandi is stopped as PSP did not find it profitable to proceed further as mentioned in Q1 FY22 concall

-

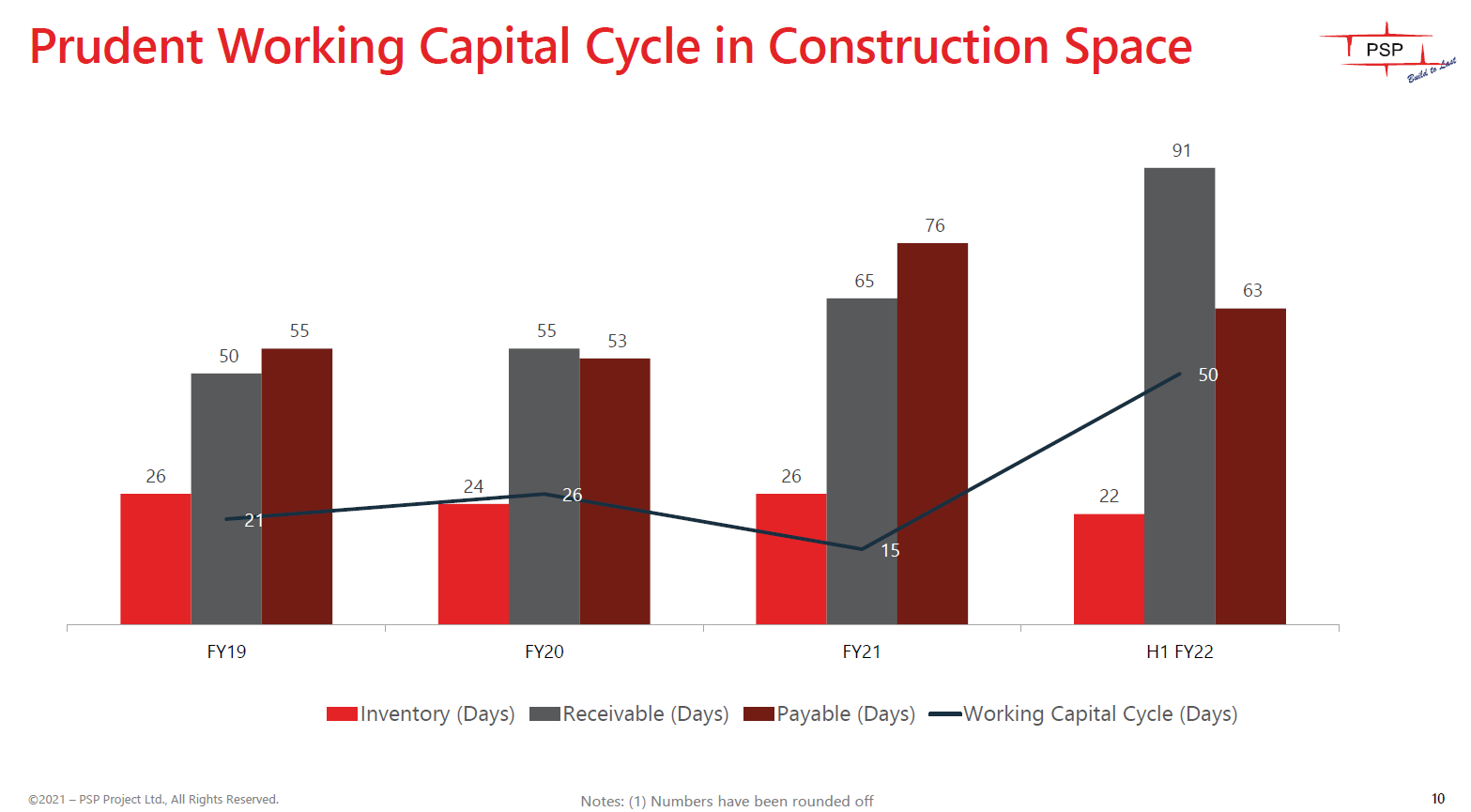

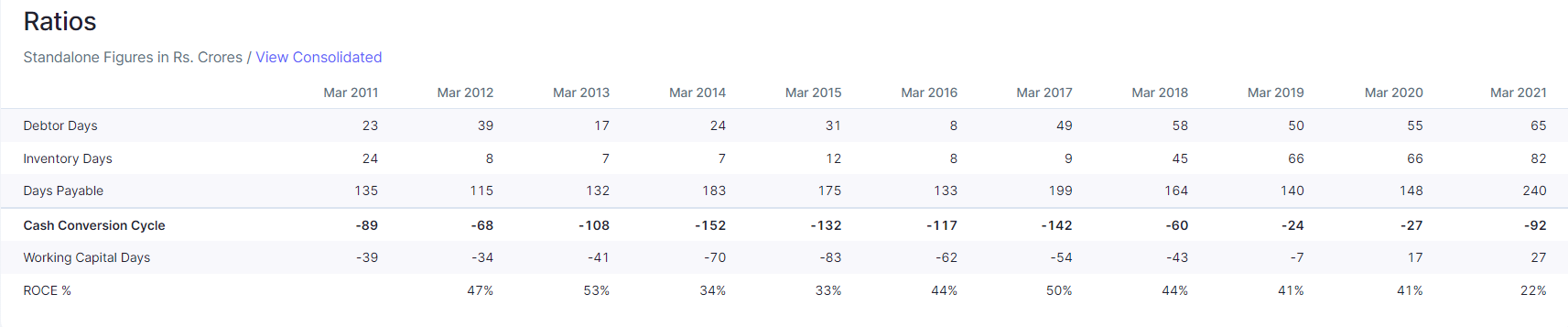

Gross Debt is 185 Cr and Cash Balance in bank is 215 Cr

-

US subsidiary is successfully divested for USD 10,000

-

The FY22 revenue guidance of 1600-1700 Cr provided in earlier con calls seems to be on track and management confirmed the same.

Valuation -

TTM EPS is 41.46 Rs

CMP 575.35

P/E ~14

D/E 0.32

CEO’s vision especially he is not interested to venture into any PPP projects and stopping projects wherever there is a finance default is commendable.

Overall, the execution seems to be good and the company’s growth trajectory seems intact. The central vista has around 15,000 Cr worth projects which are yet to be allocated. With Surat Diamond Bourse almost getting completed, the company will be eligible for projects worth more than 2000 Cr from Feb 2022. As the company recently completed the Kashi Viswanadh Dham corridor project in Varanasi and based on the concall, there is a high chance the company will be a strong contender for the subsequent roll out project which is meant to other parts of India.

With a strong balance sheet and diversified order book, CEO delivering as per the estimates, I believe the stock price will move further up. The only key risk I see is 63% of the projects are from government but CEO clarified that unless they see strong funding available, they are not planning to proceed. So far, only the Bhiwandi and Pandharpur projects from government did not turn out for better.

Discl - Invested 4% of PF.

4 Likes

Please listen to the concall starting from 53:10 about the question on receivables

The CFO has mentioned, they usually get 70-75% of money during the project and the rest within 2 months after the completion certificate. So, she mentioned that they will receive around 380 crores for the finished projects in next 2 months which will reduce the receivable days from 91 to around ~65 again.

My understanding is, it will then put the working capital days back to negative. Is there something else which you think is a risk here?

4 Likes

The problem is in the operating cash flow every time the current liabilities has to be increased to support cash flow

Even in the con call they are clear on long-term they can only maintain a npm of 7 to 8.5 margin

Iam not able to understand but is it a fact that generally the OCF is low for epc companies

Can some seniors please explain the low Ocf

Disl sold at high because of not able to understand the OCF

2 Likes

Axis securities initiate coverage on PSP Projects Limited (PSPPL) with a BUY recommendation and aTarget Price (TP) of Rs 620/share

89887357.pdf (974.1 KB)

Disc: Invested. this is Not a buy or sell recommendation

2 Likes

Declared L1 bidder

4 Likes

Hello members any confermation about completion latter of sdb projects… and how much impact due to raw materials price hike on psp projects…

PS Patel Of PSP Projects Speaks On The Firm’s New Orders

Co. target 20-25% growth p.a

Co. is virtually debt free and no further requirement of debt for this new projects allotted.

management haven’t given any indication on the completion of sdb project

Disc: Invested. this is Not a buy or sell recommendation

4 Likes

Very vaild question.

Least they can do is to save some hard cash rather than paying pennies in dividend to shareholders.

More stress can be in the path going forward, since they are just starting manufacturing added by high input cost cash is really they need unless they will end up increasing debt. Which should be the last resort for any contractor.

1 Like

https://www.bqprime.com/amp/research-reports/psp-projects-set-to-enter-the-big-league-icici-direct.

ICICI_Direct_PSP_Projects_Nano_Nivesh.pdf (974.2 KB)

3 Likes

Promoters continue to buy from open market. The order book pipeline also looks healthy.

4 Likes

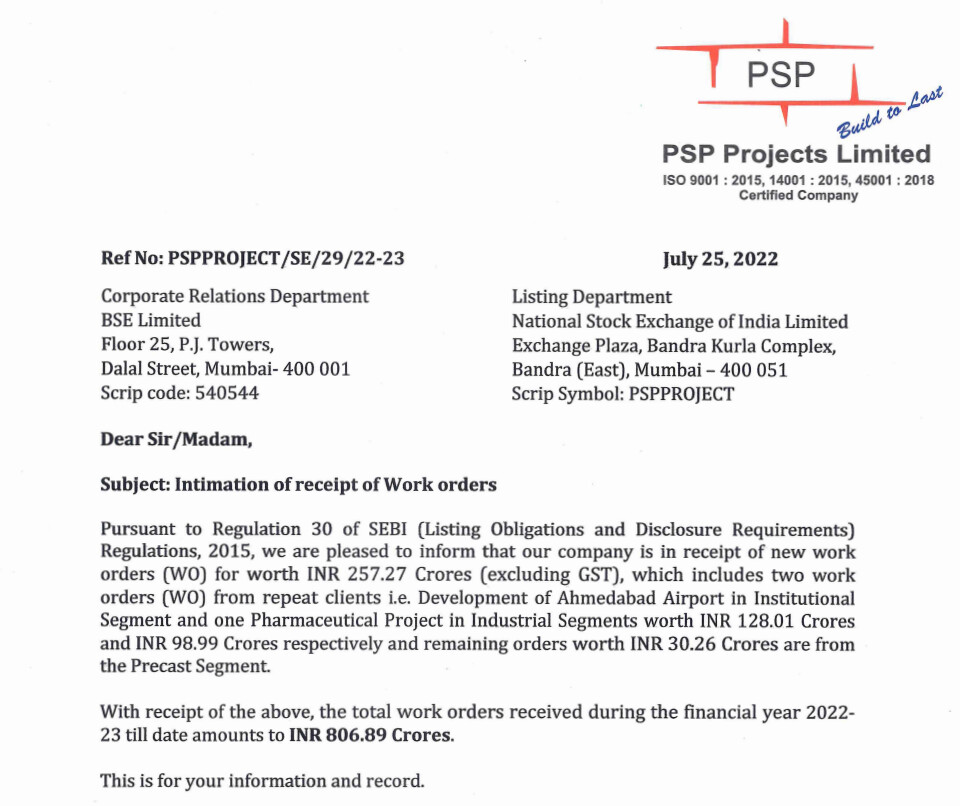

Communication on new order receipt and award of contracts

Pursuant to Regulation 30 of SEBI (Listing Obligations and Disclosure Requirements)

Regulations, 2015, we are pleased to inform that the company has been awarded the

contracts worth INR 247.35 Crores (excluding GST) from Precast and Government

segments.

With receipt of the above, the total order inflow for the financial year 2022-23 till date

amounts to INR 1,344.24 Crores.

2 Likes

This order is solely for precast facility or mix some construction work?

Disc: invested. this is Not a buy or sell recommendation

@ValueSeeker234 cant be sure from the disclosure, but in concall, prahaladji mentioned about expected Precast Duct order of about INR200 crore in Rs.4000 cr bid pipeline

2 Likes

If the whole order is from precast facility than it is good that this segment is picking up and people are recognizing this precast technology.

Hope for better orders in this segment in future

Q1FY23 Concall snippets

Major highlights

- Financial Performance

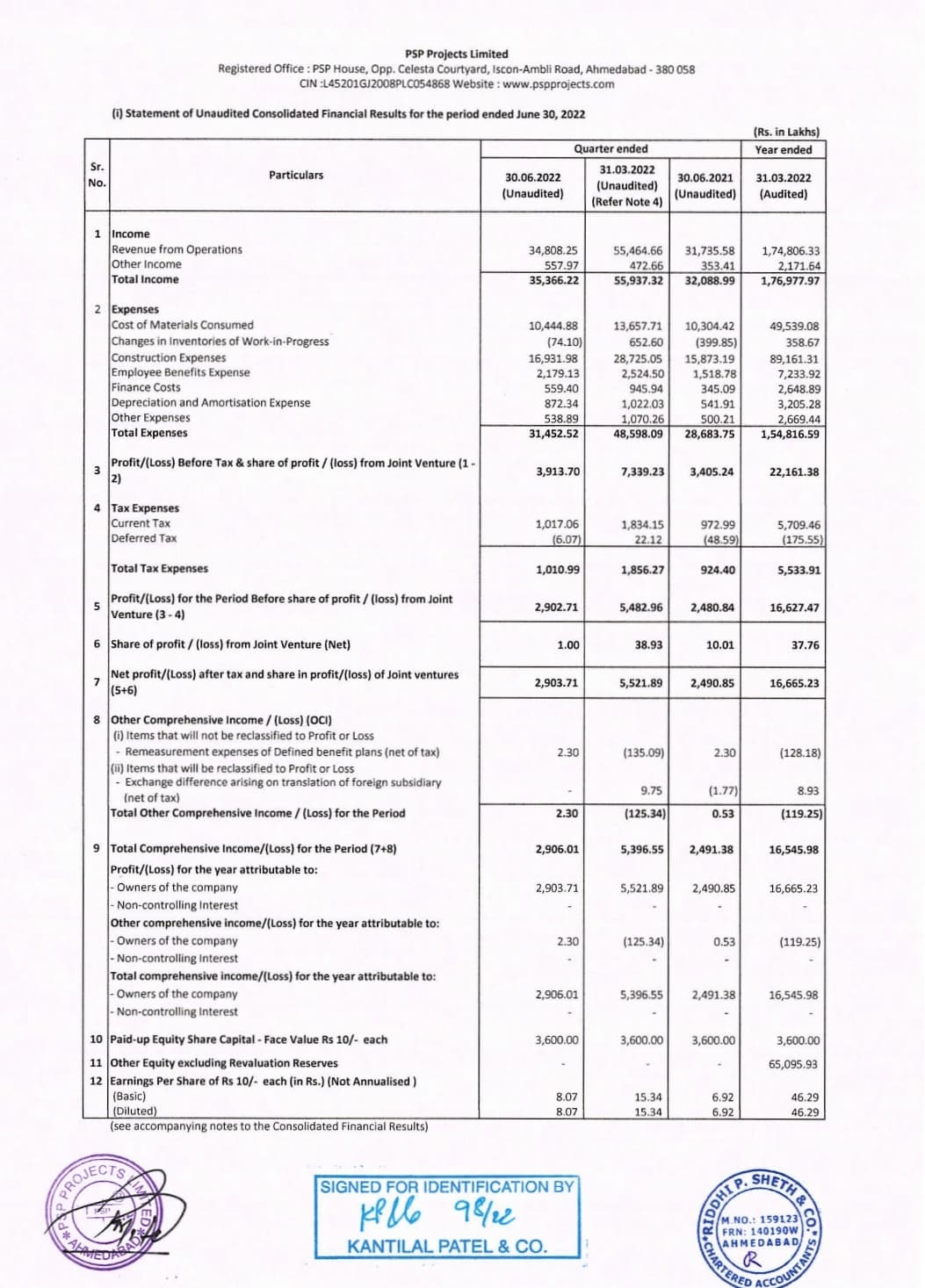

a. Revenue from quarterly operations is at INR345 crore, higher by 8.8% on Y-o-Y basis.

b. EBITDA for quarter is at INR47 crore higher by 19.6% on by Y-o-Y basis.

c. Net profit for the quarter is at INR28.51 crore, which is higher by 13.5% on Y-o-Y basis.

d. PAT margin is at 8.13% vs 7.8% (Q1 FY22) - Q1 FY23 order inflow is Rs. 550 Cr

- Post receipt of 24/08/2022 order, total order book is ~Rs.4850 Cr & FY 22-23 order book till 24/08/2022 is Rs.1344 Cr

- Utilized credit limits are Rs. 579 crore, of which Rs. 53 crore are fund-based utilization and Rs. 526 crore is non-fund based utilization. Total Fixed deposit by company is Rs.317 Cr.

- Total net working capital days are 35

Project Concentration

- 63% of the projects as on 30/06/2022 are government projects

- In the total order book 45% projects from UP, 39% from Gujarat. 45% of the projects doesn’t have price pass through mechanism

Headwinds/Margin compression

- Headwinds faced in Q1 FY23 in UP projects due to labour shortage

- As per top management, Employee expense has increased by 43.5% on Y-o-Y basis, the increase is mainly due to annual appraisals and increments during the April '22 and increase in managerial remuneration.

Growth/order inflow expectations for FY 22-23

- 25% growth in revenue expected this year

- Expected order inflow for full FY 22-23 is Rs.2200 Cr

9 Likes