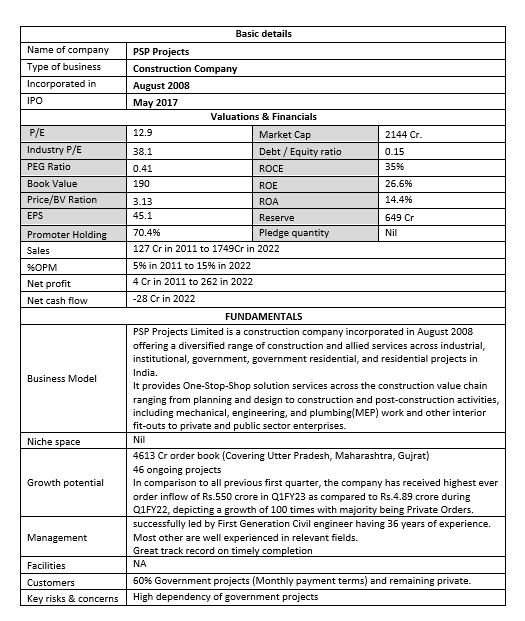

PSP Projects promoter bought 25000 shares from open market

Was just checking the FY22 annual report, and found this:

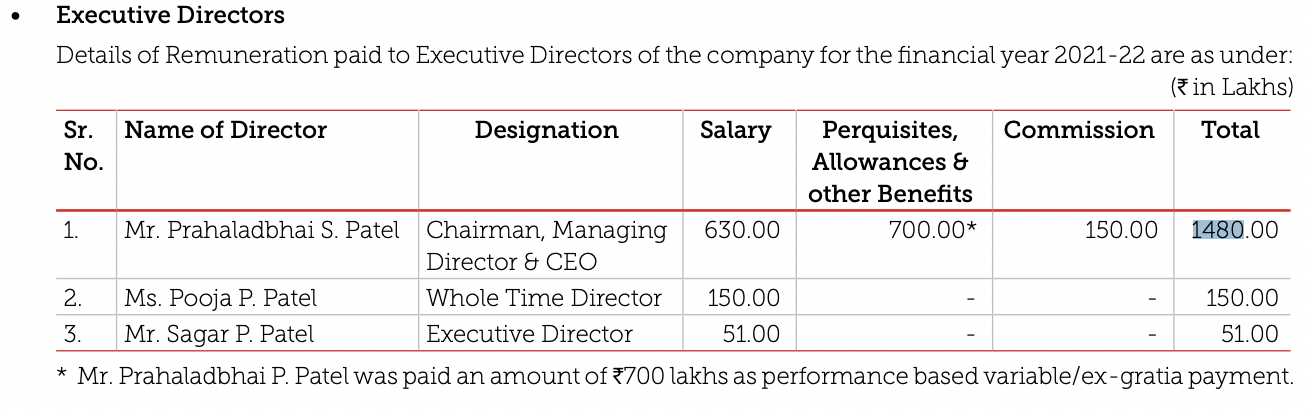

Chairman compensation is 14.8cr! While the companies profits for FY22 was 160cr. This implies chairman’s componsation is 9% of profit.

How shoud I as a retail investor interpret this, considering the chairman is the promotor.

It shouldn’t be a concern, IMO. Sec 197 of companies act prescribe upper limit of 11%. This too can be increased with shareholder resolution.

In last year (FY22), sales have grown by 40% and profits have doubled. So variable pay of Rs. 7 cr is tenable. It is better that the promoter of infra company is taking money in a rightful manner instead of doing some hera-pheri. So long as there are full disclosures, I am comfortable with the company.

Key monitorable is Q2 was a washout due to heavy rains in Gujarat and UP. Lets see how it pans out in Q3. I am also looking for company to win some part of central vista project. With SDB completion, they are eyeing for big ticket projects in Gujarat and Mumbai.

Disclosure: Invested and added on steep correction during result day. I may be biased ![]()

7 Cr performance bonus per 2022 year.

Is it normal or questionable??

But issue here is not promoters pay. In my opinion issue should be industry trend. We should compare position in peer group companies. I have verified IRB Infra, NCC, PNC Infra, KNR Const, HG Infra etc. Nowhere I found such big pay outs.

Agree with your point.

The big point here the company is not able to convert the profits into enough free cash flows.

All aspects of the business are looking good. But there are two points I have trouble imagining the company’s sustainability.

- Free Cash Flow: For a growing company, free cash flow can be somewhat on the lower side. Free cash flow of Rs. 58.05CR vs PAT of Rs. 620.08CR in 9 years is not good. Around 10% of the PAT has been converted into free cash flow.

- Expansion of the business: For the growth of the company, they have to bid on big orders. I don’t find any big construction business efficiently growing. They have to enter into competitive bidding subsequently. The bidding market seems like many suppliers and low demand. The company depends on the CAPEX plans of the other industries and the government infrastructure. This seems like a terrible industry to me.

-

Key Man Risk: P Patel is a great person. For the growth of the company, the company needs to employ talented people like P Patel.

Disclosure. Invested but am now uncertain about holding further.

Need counter-arguments.

- About the concern regarding FCF: The construction industry is a FCF-deficit industry where money circulate in cycles. It involves an intensive working capital. The contract sum received in one project goes into repayment of liabilities involved with that project to the vendors, lenders and outsourcing partners. A major chunk of the remaining money goes into Security Deposit, Earnest Money Deposits, procurements, etc. concerning the next project in pipeline. As such, not lot of cash is left free.

In simple words , FCF is the cash readily available after the company has paid for its OPEX and CAPEX. So, This is what I tried explaining in the paragraph above. The cash freely available is less in the construction industry. Hence, FCF for PSP being on the lower side is justifiable and not a point of concern.

-

Taking support of the previous point, it is evident that the CAPEX and OPEX are happening and the growth is visible in the topline and bottomline of the company. Also, the company is having a rock-solid order book of 5081 Cr. This is because of their aggressive bidding strategy. “The bidding market seems like many suppliers and low demand.”. I love this statement. Its 100% true. The cherry on the cake here is that PSP is one of Govt.'s most eligible supplier.

-

Mr. Patel is a revolutionary leader. Agree with you here.

Disc: I am in the Construction Industry and have very carefully felt and observed the FCF pattern in the entire industry. Also, Invested.

If value of the business is total free cashflow discounted to present value, then PSP seems expensive. Its price to free cash flow is 289, which twice as high as likes of Asian paints of the world. With opportunities like those, why would you invest in a company like PSP projects? If you are making a case for why construction industry is notorious for poor FCF, why would you choose this industry among many other available to choose from?

Just curious.

The company is in a super growth phase with rapid projects undertaking. This involves taking on multiple projects and overshooting cash capacity. As such, for this super growth momentum, the company needs to compromise on Free Cash Flows. This compromise is not hampering their solvency and liquidity but is strengthening it’s operations. As soon as the company is out of its super growth phase, the FCF will be seen in a rising trend.

I am a value investor and prefer to invest in companies in their super growth phase more than in their sustainable/stable growth phase. Hence, I am ready to invest in the company. One needs to invest in construction industry as infrastructure push is live and now.

P. S. FCF pattern in construction business is different than other business and comparison with other Industries like that of Asian Paints cannot be treated as an Apple to Apple comparison. Construction is a business of delayed cashflows plus taking multiple projects and overshooting cashflows. If we check the growth stories of other construction companies, we can find resemblance in these patterns.

One key risk in PSP projects which dampens my conviction is its dependency on Government projects.

Good points.

Also, to chip in, while the company usually spends about 3-4% of sales on capex, last couple of years the capex has been elevated due to the precast project to the tune of 75-100 cr, which affects the free cash flow numbers.

Further, the cashflow numbers pre 2017 are meaningless as the business model itself was different and focussed more on civil contractor work, the nature of the work itself was such that it was not fixed asset intensive, more labor intensive and focussed more on quick turnover of projects at negative working capital cycles. Post 2017, the nature of the work has changed for the company due to full EPC, MEP, interiors and end to end ownership of the project. Which changes the structure of debtor days, payable days and inventory days, all of which affects the cashflow from operations. Makes sense to keep these points in mind while looking at cash generation potential in the company.

On the point about competition, it’s important to look at different buckets of orders. The competition is more pronounced in the 100-300 cr government projects, where multiple companies qualify and are empanelled. In private projects, there are other variables in play and not just the cost factor like trust in company, quality of construction, speed to finish the project, etc. And in the case of government tenders of higher size than 500 cr, the competition significantly diminishes between just the top 4-5 players. As can be seen in the Kashi, central vista projects, etc. If the govt begins approving precast use in construction, this opens up another variable to differentiate for PSP.

Key man risk is there, but both the son and daughter of the promoter have been involved in the company since past few years and are involved in day to day ops of the company. Also, at age 59, PS Patel is not yet at the higher end of the age where succession is too much of a concern. And can probably make the case as well that promoter involvement helps their case in key projects vs dealing with business managers or project directors in a L&T or Shapoorji.

Having said all that, don’t want to gloss over the fact that any construction company’s business quality and metrics is inherently inferior. The value appreciation here is more around where the capex cycle is in India, how the company fares with respect to competition, order book mix, quality of promoter.

Disc: invested. Pls do your own due diligence before investing.

Agree with Tanay_Malpani and beg to differ with Sumit11. There are different ways to value companies. It is not kind of one size fit for all scenario. If free cash flow is the only parameter, then everybody would be investing in Asian paints and there would not be thousands of good companies.

Having said that, I have my reservations about PSP. More Govt projects means more red tape, inefficiency, long receivable period, and above all bribery and corruption. It creates a red flag. Private projects mean efficiency, quality and technological efficiency. I did not find any Mojos in PSP. See HCC. Inspite of their blunders at Lavasa, nobody can take away their quality of construction and technological superiority. It can only be compared to L&T.

Another negative is the payout. Agree that Mr Patel is a visionary. But it is also true that he is greedy. Any good work done by him is amply rewarded to him by his ownership and investment in the company. Otherwise he should resign and appoint a professional CEO.

In today’s world yhere hardly anyone who doesn’t misuse the power. Some do in a big way some in small fractions.

PSP emerged lowest bidder for ~1300 Cr Surat Municipality building

So total order book for FY’23 is how much, 3313crs?

PSP Projects has emerged as Lowest Bidder (L1) for a Government project worth INR 1,364.47 Crores

Overall a good company. It is growing fast. Good roe, profitable. Valuations seem fairly valued at 600-700levels.

But promoter holding is decreasing. This is a bit strange