Hi Deb,

I’m also very new to the industry, and from whatever I’ve gathered from the net, let me try to answer your queries

Precast concrete vs Cast in place concrete:

Method- Precast concrete is prepared in factories and then transported to the site whereas the latter is prepared on site (casted and cured both)

Casting- For precast concrete, casting can be done in advance, thus saving time which is not possible for the latter case

Quality- For precast, quality can be maintained and controlled (since it is prepared in a factory) and durability and reliability is better

Labour- For precast, less number of labour is required and also less skilled, thus saving costs

Speed- Precast requires no waiting time whereas the latter requires 28 days to gain 99% strength

Curing (the process of keeping the hardened concrete moist so that it can continue to gain strength)- In precast concrete, curing conditions can be controlled because of ideal conditions in a factory

Cost- For large scale construction, precast concrete is cheaper but maintenance cost is more and for small scale, the latter is cheaper

As per PSP Management, points #4 and #5 seem to be of more importance (even if it means adding a bit to the costs)

Now, the obvious question on why precast concrete isn’t used everywhere when it has so many benefits:

Requires technical expertise and very few contractors are available in India (this was voiced by Mr. Patel in the latest concall where he says that he’s putting efforts in trying to convince the clients on why PSP Projects is a superior construction firm)

Expensive to hire cranes

Difficulty in logistics and increase in transportation costs for long distances from factors (for PSP, considering that even in medium-long term they aim to derive majority of revenue from Gujarat, this should play well for them)

BTW, PSP is out of qualification stage for Parliament building project, as they were deemed to be not big enough to qualify for this project… some criteria around net worth… I think Tata projects, Shapoorji Pallonji and L&T made the cut

Hi all,

A lot has already been said about the company in the thread.

Here are some points which I want to add:

Bigger theme for investing in PSP is that the company seems to be in a good position to capture the private industry’s growth, especially in Gujarat which is home to many chemical and pharma companies (both of which have tailwinds as of now). Smart city initiative has also benefitted the company and might play a good role going forward too.

Opportunity size is huge, if the company can successfully deliver results pan-India coupled with the above factors.

Some positives for PSP:

Healthy return ratios driven by asset-light business model and better utilization of resources (ROIC in the mid 20 range drives by less invested capital and Consistent 20%+ ROE driven by better asset turns, which again is something that needs to be observed)

Use of superior technology like SAP, CANDY, and now precast concrete (in an industry like construction, this plays an important role according to me)

Healthy order book ~3000cr creates visibility of revenue for the next 1.5-2 years and similar sized bid book also gives some confidence

On P/E basis, PSP is available at its 1 year Median P/E of ~15, compared to 3 year Median P/E of ~20, seems to be fairly valued if not a bit undervalued

Key Monitorables for me are:

Ability of management to get higher value orders like SDB

Management bandwidth to execute many projects in parallel

In the short-term, how fast is the company able to increase its labour strength to pre-covid levels also remains to be seen

Annual Report FY20 notes:

(Some points might be repetitive)

Reported highest ever revenue of 1500cr, an increase by 44% on YoY basis. Also reported highest ever EBITDA and PAT

During the period, PSP Projects INC (foreign subsidiary) formed a California limited liability company, PSP Fremont LLC with 50% partnership; engaged in the same line of business of making investment in development and construction of residential and commercial properties.

Tech-Deployment of ERP solutions has enabled the company to optimize inventory levels, ensure transparency in operations, and preserve a solid financial structure.

CANDY technology has facilitated accurate cost estimation, budgeting, planning, and monitoring, leading to a phase-wise understanding of resource requirements and consumed a third of the time taken through manual intervention.

As a project crosses 60% completion, it will make the company eligible to bid for larger and more complex single projects (SBD has crossed 61% in FY20)

We are one of the rare contractors who also undertake large scale interior fitouts, as demonstrated for the renovation of the Vidhansabha building in Gujarat.

Every new joiner is given the opportunity to work under an experienced manager to develop deeper skill sets before taking on challenging roles

Company receives upfront mobilization advance from clients. This advance is used for purchasing raw materials and some initial equipment, if required. On the other hand, the upfront margin money given to banks to get performance bank guarantees is generated from internal funds

Promising opportunities in Gujarat on which the management is bullish:

a) Delhi-Mumbai Industrial Corridor (DMIC)

b) GIFT City (Gandhinagar)

c) DREAM City (Surat) [SDB is also a part of DREAM City]

Going forward, company intends to diversify to airport building vertical. In this regard, the announcement of development of 400 regional airports under the ‘UDAAN’ (Ude Desh Ke Aam Naagarik) scheme offers promising prospects for construction companies. Also keen to enter the pre-cast and pre-engineered building segment

The Jan-March period is most crucial for construction companies as most of their orders fructify. June onwards, the monsoon hinders building activities.

In 2020, this most productive season for construction has been severely affected by the contagion and the lockdown.

The construction industry, next in line after agriculture, contributes about 9% to the national GDP and is the 2nd largest employment provider

The Indian construction industry is predicted to grow at an average rate of 6.4% between 2018 and 2023, according to Global Data, and have a value of approximately USD690 Bn.

As per the India Brand Equity Foundation (IBEF), the institutional construction demand from the healthcare sector is also on the rise .

The hospital industry in India is forecasted to expand at a CAGR of 16-17% to USD 132.84 Bn by FY2022 from USD 61.79 Bn in FY2017.

During the year, the Company deployed the SAP HANA database management system developed by SAP SE. This in-memory database technology allows real-time data processing to analyse business operations. Leveraging this technology enables the Company to enhance its capabilities and decision-making.

Company declared and paid an interim dividend of 5/- per equity share of the face value of 10/- each

Recent announcement by the company for a small order worth ~80cr in Gujarat

One interesting thing is they’re setting up a manufacturing unit for pre-cast slabs. Construction company getting into manufacturing is uncommon. Need to see how would the management bandwidth support in maintaining it profitably…!!

but when construction technology is changing to pre-cast column, beams and walls,

It probably make sense to have control on margin, schedule, quality etc …

PSP Projects consolidated net profit declines 56.73% in the September 2020 quarter. Net profit of PSP Projects declined 56.73% to Rs 14.07 crore in the quarter ended September 2020 as against Rs 32.52 crore during the previous quarter ended September 2019. Sales declined 22.11% to Rs 243.09 crore in the quarter ended September 2020 as against Rs 312.11 crore during the previous quarter ended September 2019.

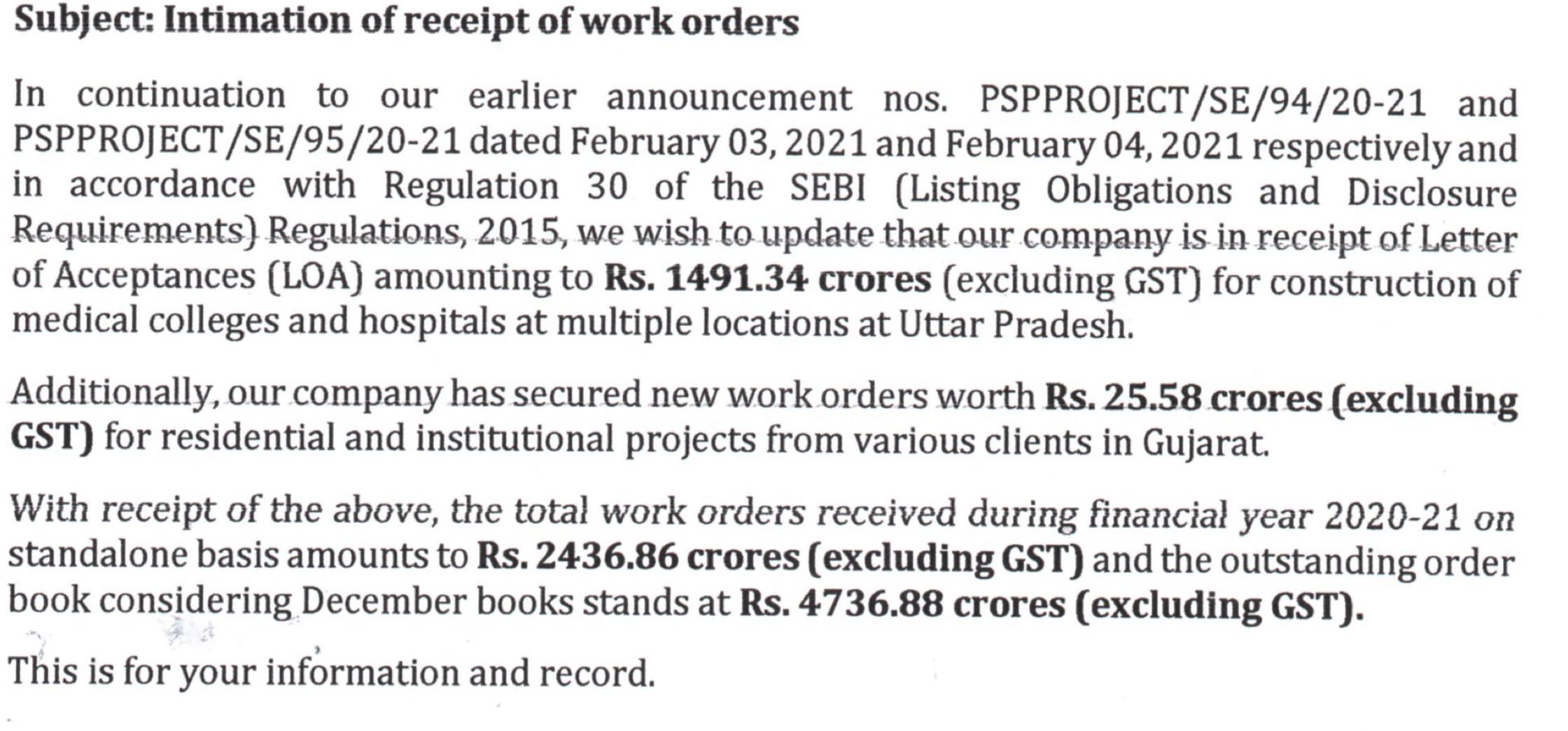

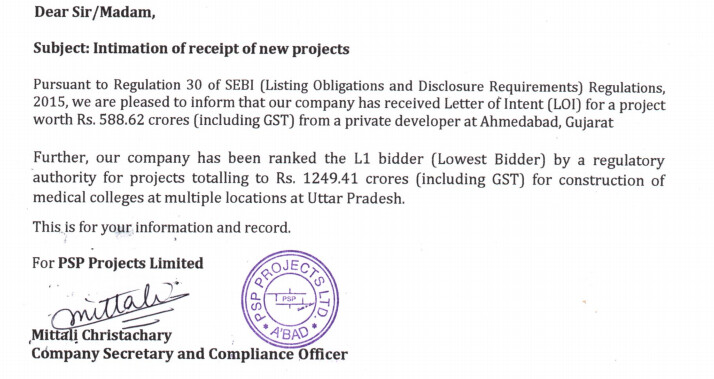

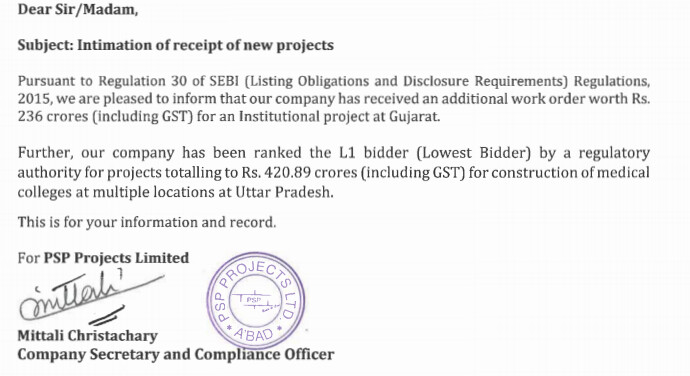

If one adds 1250 and 420 it comes to ~1670 but they are showing ~1491 crs. Anything I am missing or despite being L1, were they not alloted full w.r.t. 420 crs?

I’ve been tracking this business since past 2 years. Being form Ahmedabad, I’ve seen the kind of work this contractor has executed be it beautification of CG Road or construction of Zydus- Cadila Head Office. The contractor is actually good at their work. They know construction very well.

Around 74% share holding is with promoters, FII ~ 1%, DII ~ 3%, (Big Investors hold around 8%) not much of the stock is in the hands of retail traders/investors.

Even the script is covered by many Brokers and the script has become a favorite amongst many Youtubers.

So should we invest in the company?

Lets have a look at some fundamentals -

Revenue Growth is stable at around 23% CAGR for 5 years.

PAT growth of 15% CAGR over 5 years period.

Company has maintained a good NPM above 8% year on year except FY 21.

Pipeline Book of around 3000 Crs

TTM PE of around 14.

Positive Operating cash flow, Cash outflow for each Investing activity and Financing activity.

Company is setting up precast concrete manufacturing plant, they are diversifying the business which will also help them in reducing the input cost and they can sell the product in the market as well.

All of the above fundamentals coupled with positive outlook by visionaries makes us feel that ignoring this stock can be a mistake. It tempts us to be part of this business and ride in its growth story.

I had invested in the company after looking at its work quality. After 2 years of investing, when the market is in a bull run, investors and traders are finding quality in every other business, I was quite surprised as to why this business has not created wealth for its investors.

I was curious, after digging up some data from the Annual reports and peer’s data following are my observations -

Company has a unique standing in construction business - it is involved in beautification work of roads, river front, construction of gorgeous architectural buildings/offices, interior outfits etc. whereas most of the listed contractors are either into construction of infra projects such as road, bridges etc. some contractors are into / constructing and selling/ renting of properties. This business has different business operations unlike most of its peers.

Cash flows - Choking cash flows, operating cash flow is significantly small. In the past 5 years, the company has sourced around INR 400 Crs PAT, whereas operating cash flow is INR 80 Crs.

Dividends - Company has distributed around INR 77 Crs of dividend in the past 5 years.

With these observations now I am clear why this business has not created wealth for its investors.

Order book as on March 31, 2021 is 4121 cr. (highest ever). It was 729 cr in 2017.

23 projects completed in fy 2021.

The company is diversifying geographically. 61% of order book for market other than Gujarat.

The company aims and is moving towards ‘One stop solution’.

Order book break up(%) :

Fy20 vs Fy21

Pure play civil construction 13.7 vs 5.4

Turnkey (Civil, MEP, Interiors & O&M) 68.5 vs 38.3

EPC Projects (Design, Construction,

MEP, Interiors & O&M) 17.8 vs 56.3

SDB project which on verge of completion will enable the company to bid for projects worth over 2000 crore.

The union govt’s push for infra development is a good news.

The annual production capacity of the precast plant is expected to be 3 million sq ft once fully operational. Initially, the plant is expected to deliver 1 million sq ft as Phase 1.

The company believes that setting up precast plant will increase operational efficiency and margins, eliminate the dependence on laborers over time, reduce the safety concerns, allow faster delivery and better quality of work.

The construction of medical colleges and hospitals has started at multiple locations in UP.

A nice management interaction, one key missing question was why company is unable to convert accrual earnings into operating cashflows since FY17. One structural change in the business model since listing (2017) has been increase in inventory days from 5 days to 25-30 days. After the delivery of Surat project, it will be interesting to see if operating cashflows are much higher in FY22 and make up for poor cashflow conversion since FY17.

Can some one please comment on following part from video(time line roughly at 1:00:00 hour?

promoter selling PSP shares in listed entity

putting this money in US entity

US entity will pay back this money to listed entity

US entity will become completely owned by promoter?

This is actually appreciated by Varinder ji in 1:08:00. But still question lingers in my mind isn’t promotor holding company in same business area considered as conflict of interest?

Could it be because they have cash inflows from the past projects that have been completed and cash outflows from the present which would be larger as they have grown ?

The promoter wants to increase free float of shares. He understands that unless there is some more shares available for trading in market, the chance of better discovery of share price is difficult. At the same time, promoter selling stake is a negative sign. The company has a subsidiary in US which is worth 34 crores. In Indian stock market, there are many shoddy promoters who siphon off funds using foreign subsidiary. Hence, promoter thought ,he can negate the stake sale with removing the foreign subsidiary, which is anyway not generating revenue after listing. This action reflected immediately on the stock price, moving from 450 to 530 within a week. The promoter sold 4% and he mentioned he actually doesn’t have any need to sell.

Apart from this, promoter gave an optimistic opinion about chance of getting a project in central vista redevelopment projects - 13000 crs. With Surat Diamond Bourse project (1850 crores) to be completed in next 3 months, the company will be eligible for bidding projects around 2000 cr.

Hi

My understanding is as follows:

PSP at given loan of around 35 Crores to US subsidiary, which apparently isnt doing well and cannot pay back to PSP. so it would be result in to bad debt. in order to avoid this situation prahladbhai ( MD) is selling is own stake and will provide this money to PSP US subsidiary which inturn will pay back to PSP India. So PSP shareholders donot suffer.

Can anyone throw some light on how to read Cash flows from the Operations of a construction company?

If we see in the case of PSP projects, last 4 years CFO has been 180 Cr. while EBITDA has been 580 Cr and PAT 365 Cr. So, in the last 4 years, only 50% of PAT is converted to cash and this number is only 31% if we see EBITDA to cash conversion. Whereas, in the case of companies like NCC, avg. CFO/EBITDA for the last 4 years is around 67%.

If we see KNR construction, avg. CFO/EBITDA of last 4 years is approx. 27% which is somewhat similar to PSP. So how should one read this metric?

As per my understanding, in construction companies, EBITDA to CFO conversion would be on the lower side due to working capital stuck in receivables, Bank Guarantees, and Retention money. Anyone with the knowledge on this aspect please throw some light