Happy New Year !!

Here is the latest portfolio

| Sr. No | Company | Sector | Capitalisation | Allocation % | Rationale |

|---|---|---|---|---|---|

| 1 | HDFC ASSET MANAGEMENT COMPANY LIMITED (XNSE:HDFCAMC) | Financial | Large Cap | 11% | Financialization theme |

| 2 | BSE Limited (XNSE:BSE) | Financial | Small Cap | 10% | Financialization theme |

| 3 | AVENUE SUPERMARTS LIMITED (XNSE:DMART) | Services | Large Cap | 9% | Longterm retail play, debt free |

| 4 | HCL TECHNOLOGIES LIMITED (XNSE:HCLTECH) | Technology | Large Cap | 9% | Coffee Can |

| 5 | LAURUS LABS LIMITED (XNSE:LAURUSLABS) | Healthcare | Mid Cap | 7% | Growth |

| 6 | DEEPAK NITRITE LIMITED (XNSE:DEEPAKNTR) | Chemicals | Mid Cap | 7% | Growth |

| 7 | ASTRAL LIMITED (XNSE:ASTRAL) | Chemicals | Mid Cap | 5% | Coffee Can |

| 8 | OLECTRA GREENTECH LIMITED (XNSE:OLECTRA) | Engineering | Small Cap | 5% | Promising sector for future |

| 9 | ABBOTT INDIA LIMITED (XNSE:ABBOTINDIA) | Healthcare | Mid Cap | 5% | Coffee Can |

| 10 | DR. LAL PATHLABS Limited (XNSE:LALPATHLAB) | Healthcare | Mid Cap | 5% | Coffee Can |

| 11 | NAZARA TECHNOLOGIES LIMITED (XNSE:NAZARA) | Technology | Small Cap | 4% | Promising sector for future |

| 12 | TITAN COMPANY LIMITED (XNSE:TITAN) | Cons Durable | Large Cap | 4% | Longterm retail play, debt free |

| 13 | GATEWAY DISTRIPARKS LTD. (XNSE:GDL) | Services | Small Cap | 3% | Promising sector for future |

| 14 | PSP PROJECTS LIMITED (XNSE:PSPPROJECT) | Construction | Small Cap | 3% | Asset Light business in construction |

| 15 | PAGE INDUSTRIES LIMITED (XNSE:PAGEIND) | Textiles | Mid Cap | 2% | Coffee Can |

| 16 | INDIAN ENERGY EXCHANGE LIMITED (XNSE:IEX) | Services | Mid Cap | 2% | Growth |

| 17 | HDFC BANK LIMITED (XNSE:HDFCBANK) | Financial | Large Cap | 2% | Coffee Can |

| 18 | AMBIKA COTTON MILLS LIMITED (XBOM:531978) | Textiles | Small Cap | 1% | Tracking |

| 19 | KOVAI MEDICAL CENTER AND HOSPITAL LIMITED (XBOM:523323) | Healthcare | Small Cap | 1% | Tracking |

| 20 | LUPIN LIMITED (XNSE:LUPIN) | Healthcare | Mid Cap | 1% | Coffee Can |

| Stocks | |

|---|---|

| Top 5 | 46% |

| Top 10 | 74% |

| Top 15 | 91% |

| Top 20 | 97% |

| Market Cap | |

|---|---|

| Large Cap | 35% |

| Mid Cap | 36% |

| Small Cap | 30% |

| Sector Split | |

|---|---|

| Financial | 23% |

| Healthcare | 20% |

| Services | 15% |

| Technology | 14% |

| Chemicals | 13% |

| Engineering | 6% |

| Cons Durable | 4% |

| Textiles | 3% |

| Construction | 3% |

Investing Objectives –

Return of Capital - ![]()

Beat BSE Sensex in terms of CAGR ![]()

Beat FD returns ![]()

Reach 15% CAGR ![]()

Beat MF(direct) returns (26.9% CAGR so far) ![]()

Changes –

- Increased allocation to Dr. Lalpath labs and a little to Astral when the market was down

- Sold Off Quantum Long-Term Equity MF. With this, beating MF returns becomes even more difficult. Especially, I am no longer buying any SIP or lumpsum while I am doing some investments in direct equity

Notes –

- The allocation to defensives(Pharma.Tech) is 33% now and New Age(Nykaa, Nazara, Olectra) at 10%

- Samit Vartak’s words on superior portfolio construction(how to make 10x in 10 years) and always looking at future market cap of the stock while investing has made a profound impact on my current investing thought process

- The portfolio is evenly balanced across market cap sizes

- The top 10 allocations are now filled with high conviction ones and in most cases has a history about their narratives and numbers. To break into the top 10 now, is very difficult. The only rookie stocks I see are

-

BSE Limited which I think can hold the place for it is a duopoly and will remain as long as stock markets are present in India. The optionality of 20% stake in CDSL and monetisation of BSE Star MF and India Inx(GIFT City) along with Cash Balance of 2200 Cr makes it more safer.

-

Olectra Greentech is aggressively capturing the market share in Electric Bus segment. Its order growth and execution seems to be impressive. The way they are operating intercity buses between Pune to Mumbai only shows the intention that they are not just looking at State Road Transport Units. Its foray into EV 3-Wheelers and Electric Trucks will increase the opportunity size.

- 2021 has been a great year in terms of learning as well as returns in direct equity. The portfolio 1 Year returns are 62.2% and overall CAGR is 25.5

Outlook for CY 2022

- Based on the HDFC MF November 2021 Factsheet,

Source - https://www.hdfcfund.com/investor-desk/downloads/downloads

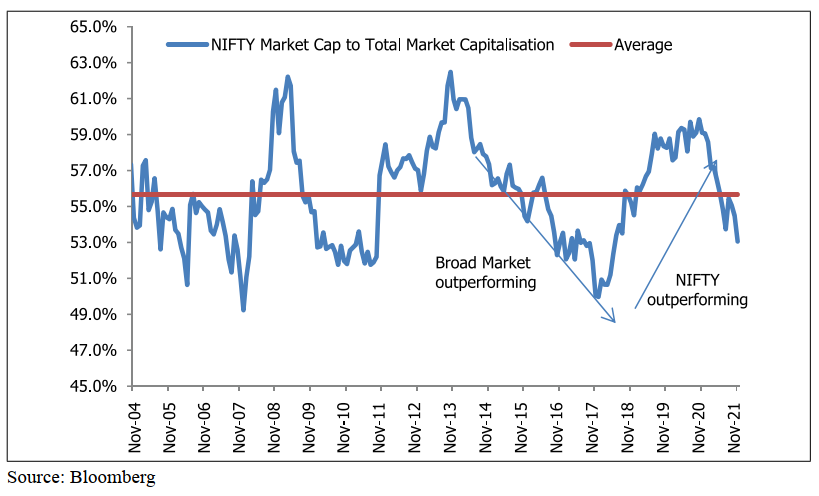

As per the below text, it is clear that ETFs may not be outperforming the Active Mutual Funds due to the fact that the rally is broad-based across sectors/companies in Nifty. Corporate India is at one of the lowest profit to GDP ratio and having very much de-leveraged(debt/equity ~ 1.6) with balance sheets displaying strength just like start of a bull run in 2003.

the below image gives us the direction that Nifty most probably will underperform the broader market(Mid and Small Caps)

Government of India along with RBI has been coming up with supportive fiscal and monetary policies, and hopefully will continue to keep the corporate tax lower at 25%. PLI schemes,China+1 in selective spaces like chemicals will also aid further growth in earnings.

With Covid-19 hitting much of MSME industries, I believe the organised players will aggressively increase their market share. It will be much more prevalent in Small Caps.

The key risks I see is the inflation which can spoil the party. Also, never in last 10 years, one asset class has been dominant for three years in a row. In fact, not even two years in a row. However, Covid itself is an exception.

https://twitter.com/gvkreddi/status/1476240907657646081

Based on the above rationale, I am continuing with 70% Equity( and 30% Debt) and having defensives as 33% within equity to give some comfort in case market turns bearish. I see the signs that in the near term, it does.

Interesting Videos -

- Ashwath Damodaran is hitting a nail in my head that I should firmly understand valuation. Our assumptions for valuation can go wrong but without valuation it is akin to shooting in the dark. This remains one of my key learning areas for 2022. Professor is so much for disruption in education that he has kept his entire valuation class recordings in YouTube.

- @basumallick in the below podcast has explained very well about how to become financially independent with calculations from 1:08:24 to 1:10:45. The entire podcast is very good - Thanks @vivek_mashrani and @basumallick for this. Now, if we can identify one 100x company in 15 years where we allocate say 10% of portfolio, our portfolio returns will itself becomes 10x with this one great choice. However, the catch as mentioned in the video, in India, generally, the 20+ CAGR growth may not sustain after 5 years for most companies. This is where some of the 100x companies of the past like Astral are expanding to other adjacencies(Adhesives, Tanks, Faucets etc) whenever they see limited scope for margin expansion with existing verticals. This theme is visible in other such multi-baggers like Page Industries, Deepak Nitrite and Pidilite Industries. Laurus Labs seems to exhibit these characteristics but we don’t have too much of history to ascertain. Now, the most important question is - Can I identify one such company in next 2 years and stay through it in thick and thin like Rakesh Jhunjhunwala stayed put with Titan? There will be long stagnations and also significant drawdowns resulting in short term opportunity costs. If I identify one and has the vision to stay long, the incentive is - I will be financially independent in 15-17 years.

- As usual, Motilal Oswal’s wealth creation study gave good insights on what worked and what did not work in last few years. The enthusiasm with which Raamdeo Agrawal presents the study makes it inquisitive to watch.