PSP Projects is a construction company offering construction services across industrial, institutional, government, government residential and residential projects in India primarily in Gujarat. Activities of the company include planning and design to construction and post-construction activities to private and public sector enterprises.

Incorporated in 2008, Company started major construction activities in June 2012 with construction of GCS Medical College, Hospital and Research Centre in Ah medabad. Since then company has completed about 71 projects until Nov 2016.

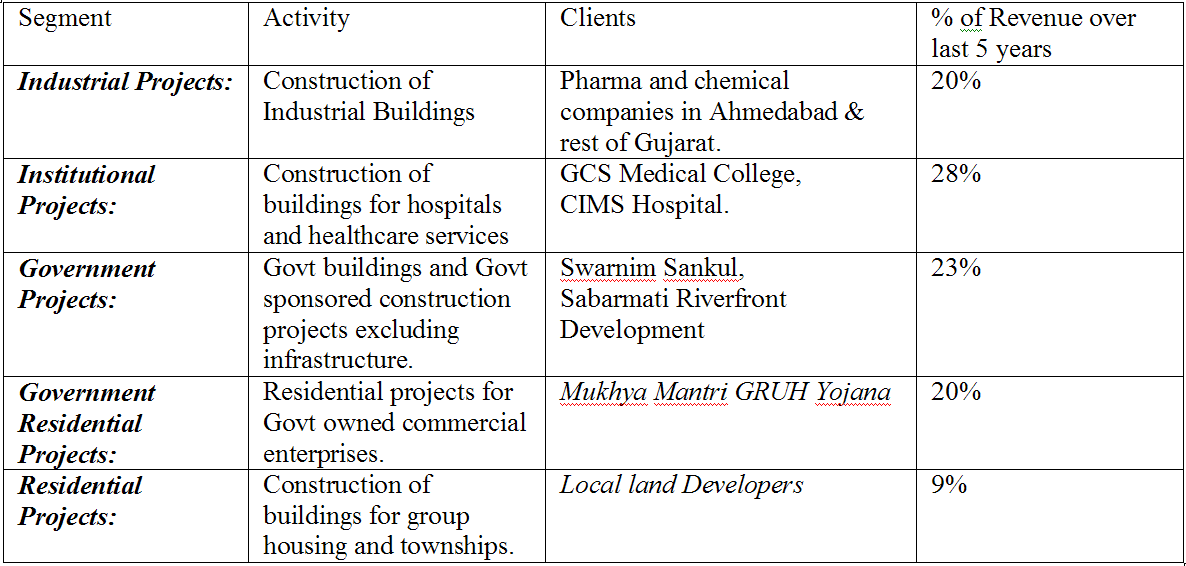

Following table provides construction activities of the company.

Source IPO Prospectus

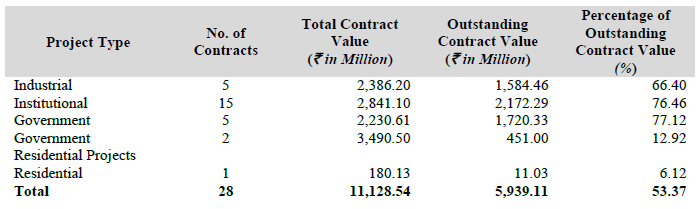

Order Book

The following table sets forth a breakdown of the Company’s total order book as of November 30, 2016, by type

of project:

Source IPO Prospectus

Company’s activities are mainly concentrated in Ahmadabad and rest of Gujarat. It is bidding for projects in Surat and GIFT City. The following table sets forth a breakdown of the Company’s total order book as of November 30, 2016, by

geography:

Source IPO Prospectus

The Company’s order book is not audited and does not necessarily indicate our future earnings. Book-to-bill ratio is about 1.3 which is low compared to infrastructure construction companies but PSP Projects executes mainly small ticket construction projects which are not awarded in advance like infrastructure projects.

In a recent chat with ET, company MD PS Patel said that order book for FY2018 is about 729 Cr and about Rs 600 crore turnover is going to come from this present order book for FY2018.

In yet another interview with a TV news channel, company MD PS Patel said that revenue for FY2018 will be 650 Cr and bottomline will be 70-90 Cr.

In the long term, company expects revenues to reach 1500 Cr by 2020.

IPO

Company issued approximately 10,080,000 Equity Shares of Rs 10 for Rs 210 per share raising around Rs 200 Cr. Out of these 10 million shares, 7.2 million shares are issued by the company as a fresh issue and 2.8 million shares are sold by company promoter family. Post issue, promoter family owns about 72% of post issue capital of the company. Of the 10 million shares offered, 4.5 million shares are offered to anchor investors including Reliance Mutual Fund, SBI MF, Axis MF, Sundaram MF and Birla Sun Life Insurance – at Rs 210 apiece, aggregating to Rs 95.25 crore. Remaining 5.5 million shares are offered to public though book-building issue.

Company will receive Approximately 144 Cr from IPO proceeds. IPO listed at a discounted to issue price.

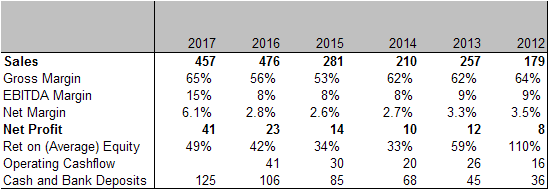

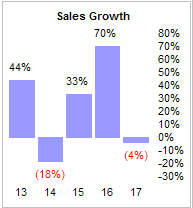

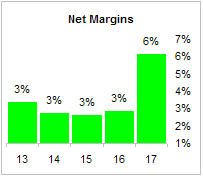

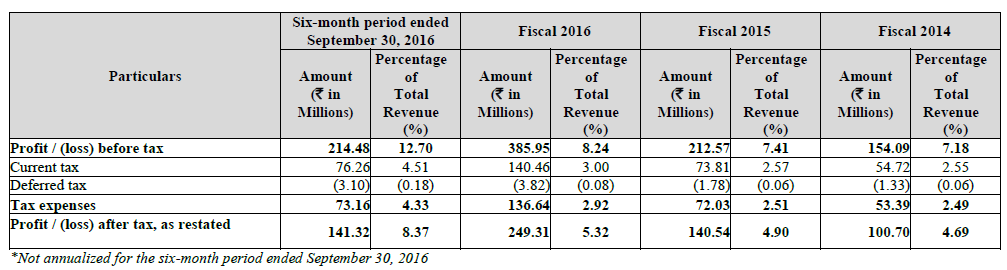

Financials

Rs Cr.

Source IPO Prospectus, 2017 Earnings Release

company’s sales growth is lumpy which is typical of construction companies. Some private clients provide construction materials free of cost to the contractor so revenue will be low for such contracts but margins will be higher.

Margins have improved in FY17 and company expects to maintain these margins going forward. company is mainly a labor contractor at the moment but with IPO proceeds it will purchase construction machinery and will be participating in value added projects.

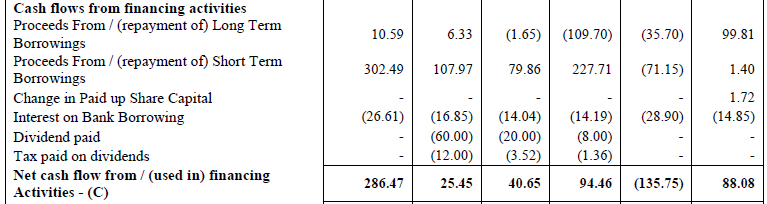

Company has managed to maintain good working capital mainly by keeping receivables and investory low. This has enabled company to remain debt free (on a net debt basis). It has short term borrowings of 62 Cr against bank deposits of 125 Cr. Usually companies with both debt and cash is a read flag. However, construction is a cash-heavy industry and PSP project is keeping cash as bank deposits and taking out short term loans from the bank which is secured by the deposits and interest rate on the loan is 1% above the deposit rate. Essentially short term debt costs company about 1% as interest expense on loans is offset of interest income from deposits.

Unlike infrastructure construction companies, PSP projects executes small ticket projects that are completed in few months so it recovers cash quickly. Company’s cash and deposits have steadily gone up over the years indicating that company is able to recover receivables quickly.

company is cashflow positive and does not really need funds from IPO for its ongoing operations. IPO is for benefit of listing and buying construction machinery which will enable company to take on bigger projects.

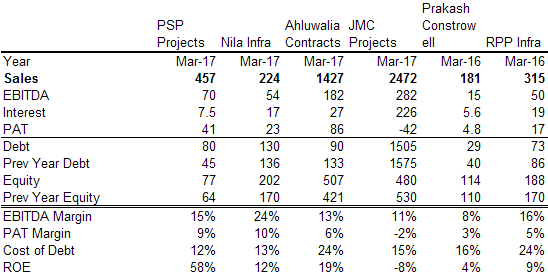

Peer Analysis

Companies margins debt levels and ROE is much better than peers.

Promoter

Company is promoted by PS Patel. He is 53 years old and so far this appears to be a one man show. He has over 30 years of experience in the business of construction. He holds a Bachelor’s degree in civil engineering. He has also been featured in the book titled “Business Game Changer: Shoonya se Shikhar” authored by Prakash Biyani and Kamlesh Maheshwari for completing government’s infrastructure project before the scheduled time for which he received appreciation of Prime Minister, Mr. Narendra Modi.

Corporate Governance

- Executive Compensation

Company paying a total salary of Rs 3 Cr to promoter family. This works out to be 8% of FY17 profits, close to upper limit of 10% set in Company Act. As a percentage of net profits of the company salary appears to be on the higher side but in absolute terms this amount is reasonable given the high profitability generated by the company.

- Dividend Policy

Company has paid dividends in the past. However, until IPO, promoter family wholly owned company.

- Taxes

Company is paying taxes. Its tax rate is about 30%.

- Debt Repayment

company is a net borrower and only occasionally repaid loans. However looking at the growth rate of the company and its cash & deposits, this is not a warning sign.

Valuation

Based on TTM earnings, company is selling for about 26 times TTm earnings. Based on management’s projections, net profits for FY2018 is expected to be about 70-90 cr against a current market cap of 1051 Cr. forward PE works out to be 13. However, this assumes near doubling of profits in FY2018 which appears optimistic.

Risk Factors

- Activities of the company are largely concentrated in Gujarat.

- company is heavily dependent on promoter Mr. PS Patel.

- company may face increased competition when it bid for big ticket projects

- Executive compensation is high.

- Activities are cash dependent.

Disclosure: Invested in IPO and thereafter.