Dear Friends,

I didnt see any thread on this wonderful company and thought of starting a new one to discuss. I tried to analyse the company myself in my own way but I invite comments from some of the more senior investors.

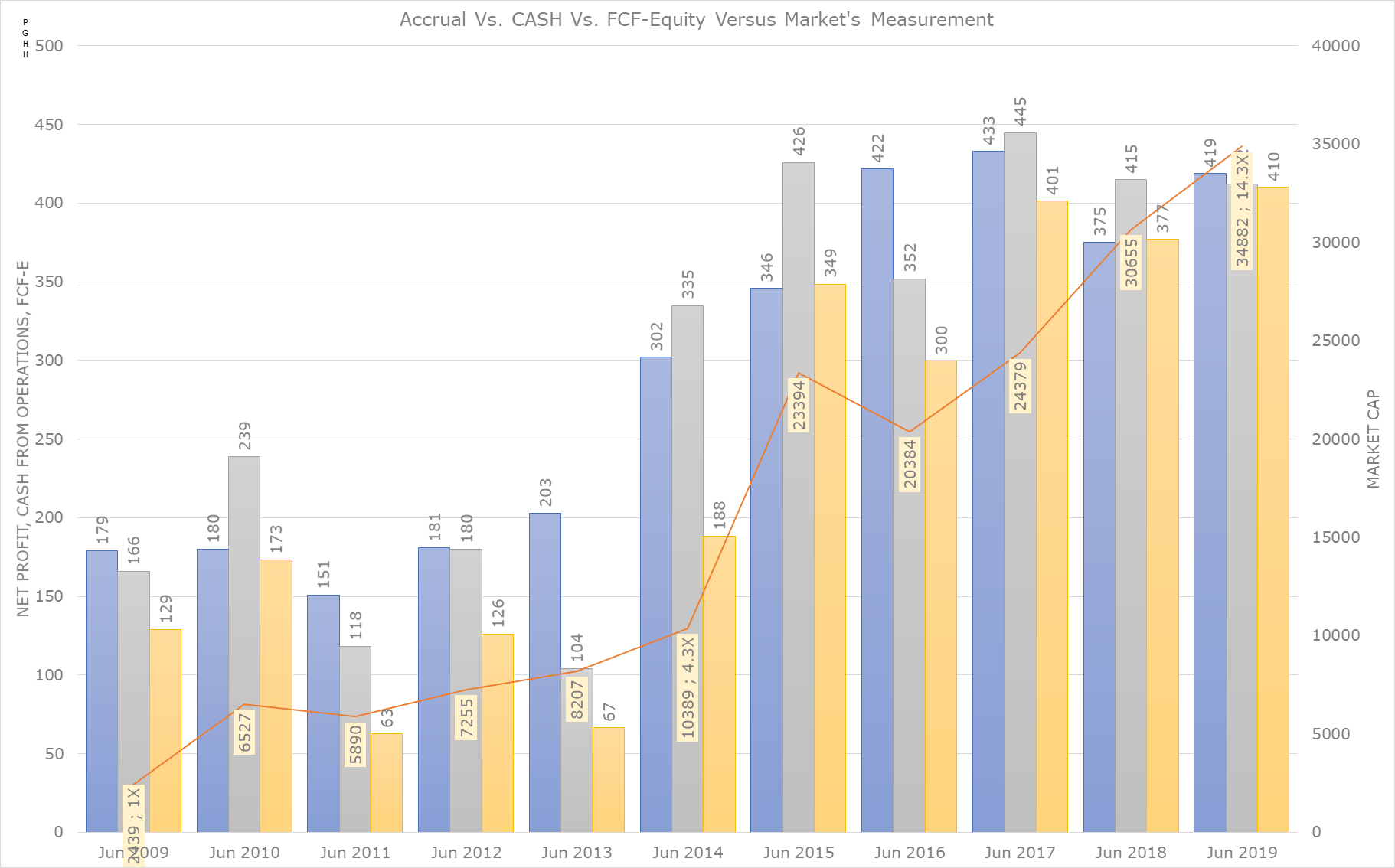

I though P&G stands at the top of the consumption story of India and after analysing a few companies in this space thought this is most close to a WB type investment. (In fact I found out he has actually invested in the global company later!)

| 2013 | 2012 | 2011 | 2010 | 2009 | Sep-13 | Jun-13 | |

| COGS % | 44.2 | 42.2 | 39.5 | 31.4 | 31.0 | ||

| Employee cost % | 5.9 | 5.0 | 5.0 | 8.0 | 7.7 | ||

| Advertising % | 9.5 | 10.6 | 11.7 | 12.5 | 11.6 | ||

| Trade Incentives % | 7.5 | 7.4 | 6.7 | 5.4 | 4.4 | ||

| Royalties % | 4.7 | 4.9 | 5.1 | 6.4 | 5.3 | ||

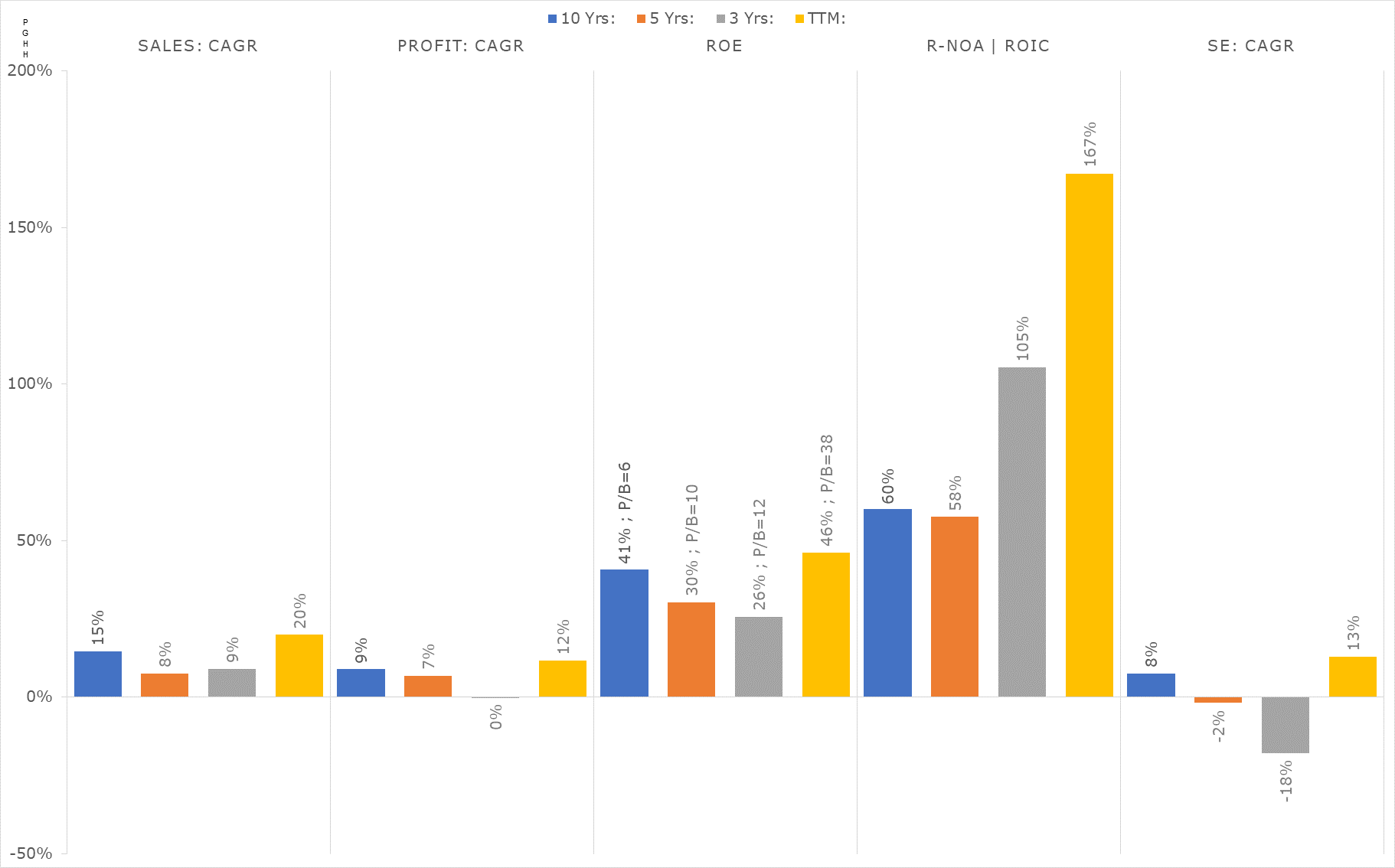

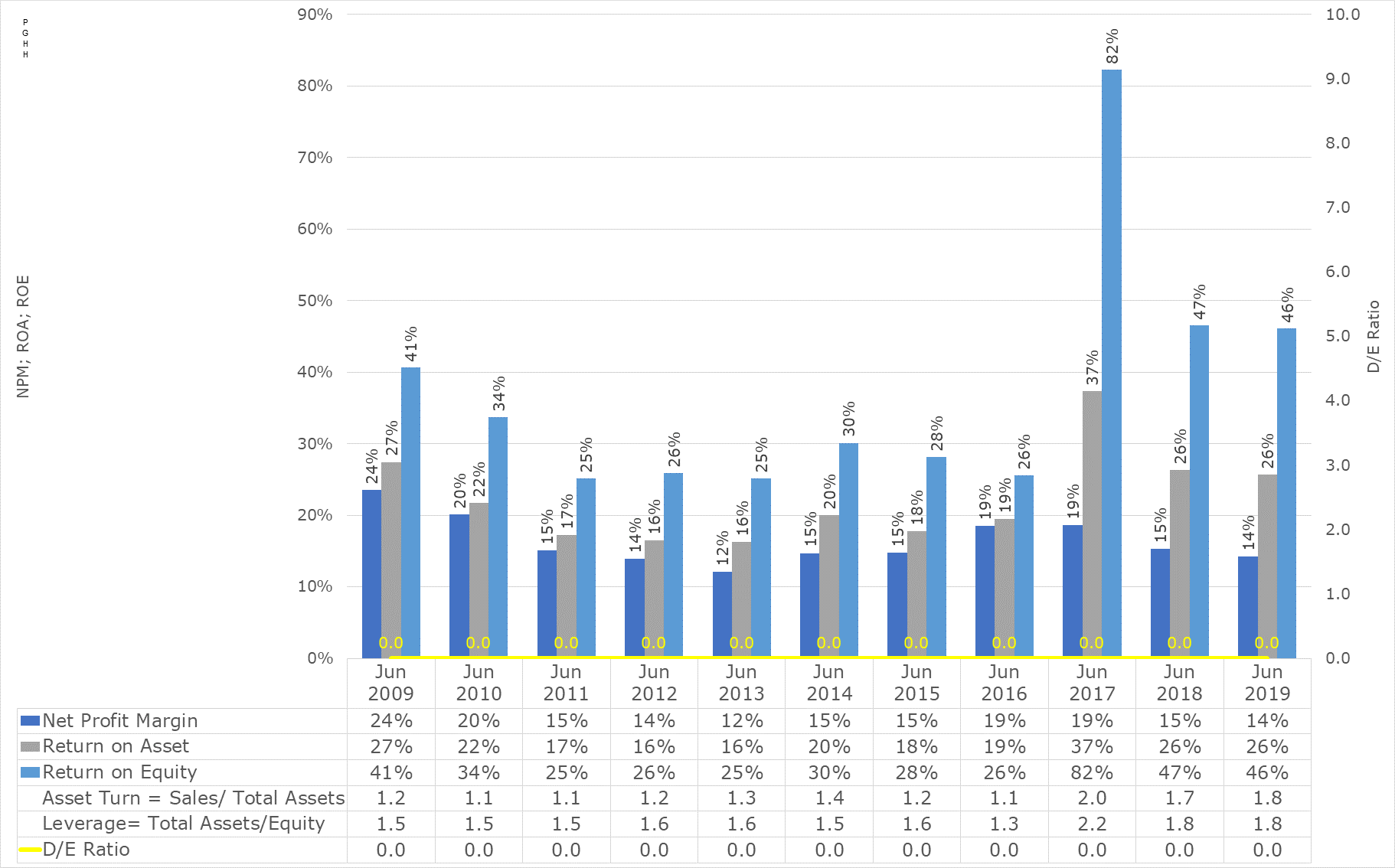

| PBT % | 17.0 | 17.2 | 17.9 | 26.2 | 30.0 | 17.7 | 18.2 |

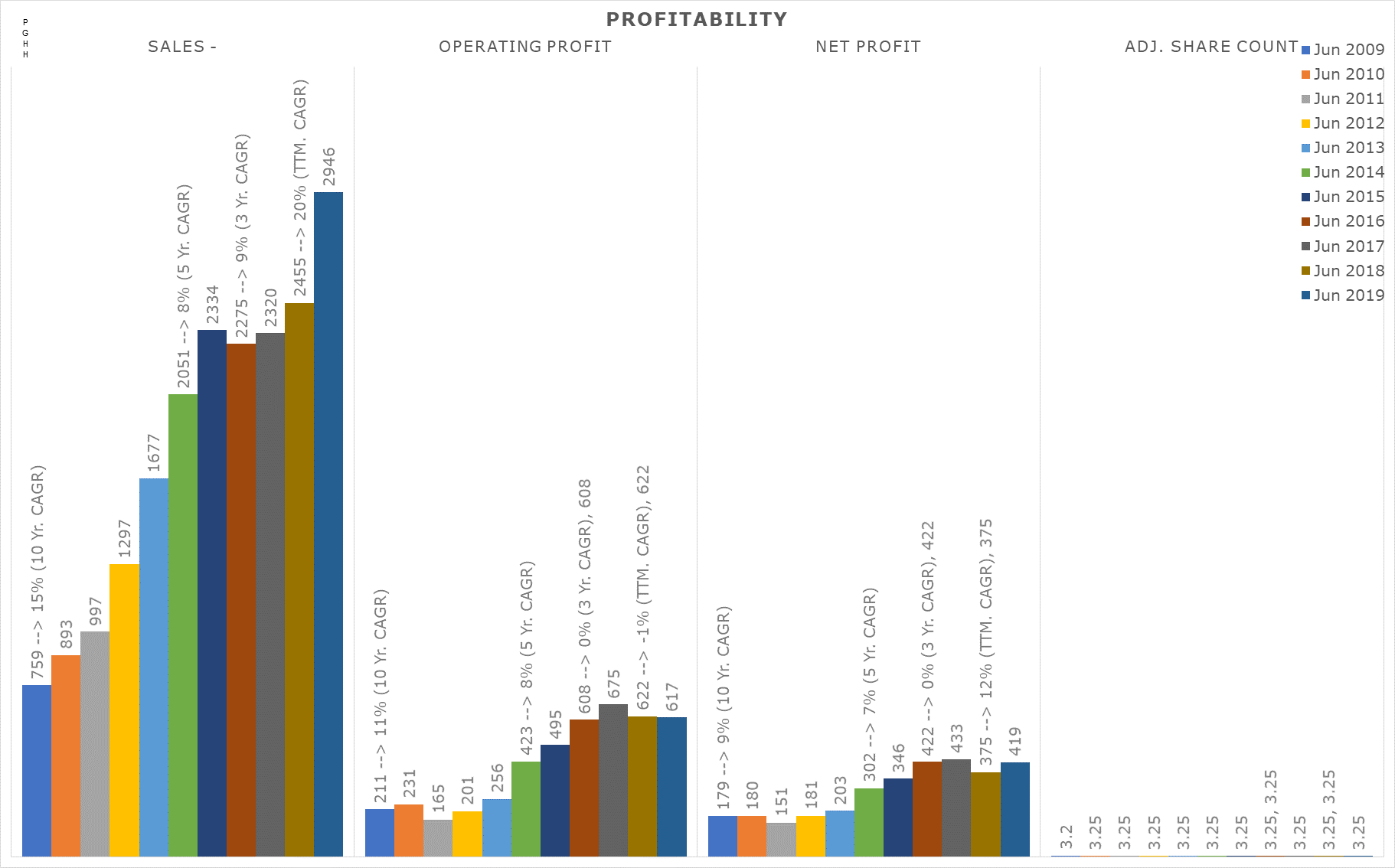

| Sales growth % | 30.0 | 29.6 | 11.1 | 16.6 |

| INVESTMENT ARGUMENTS |

| Price cuts till year end of 2011 have caused COGS to increase

from 31% to 44% however volume growth in last 2 quarters suggest no further

need to cut prices |

| Last 2 quarters have yielded an above average PBT of 17.5%+

corroborating the above fact |

| P&G is in the business of Sanitary Napkin which is the most

under-penetrated FMCG (only 15-20% penetration) item - implying that the market can scale up considerably |

| At an overall penetration level of 80% the sales can increase 5

times plus the benefit of higher end products such as ultra thin adding to

margins |

| Adding to this usage in tier 1 is likely to increase as women

use the products between 2-3 times a day as in Western Developed markets |

| Sales growth in the last 2 years despite no price cuts have

been 25% +.Volumes have increased by over 25% in the last 5 years CAGR |

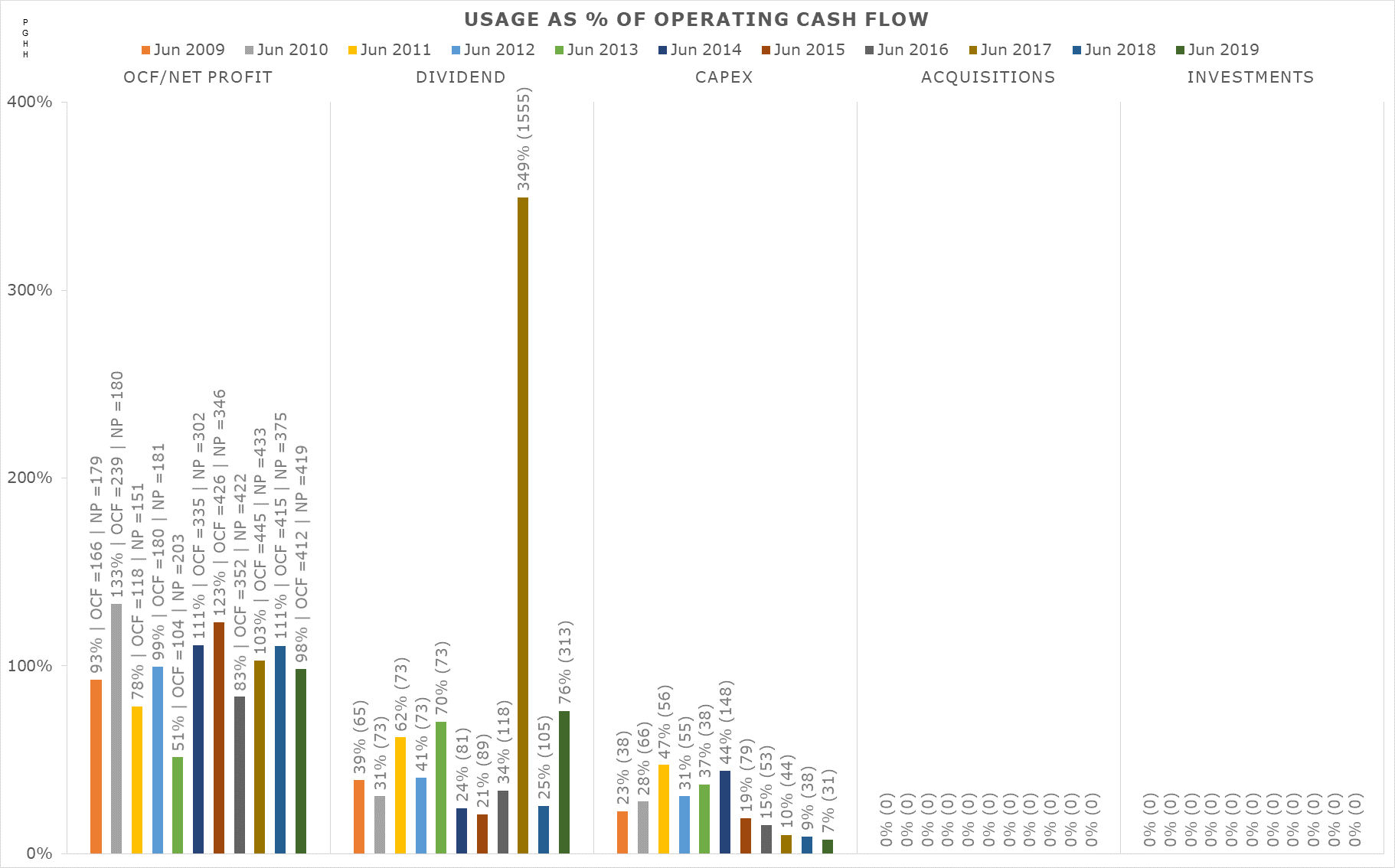

| Net debt of the company is 0 |

| Management quality is better than any other company - completely professionally managed |

| Company is the leading player in the sanitary napkin space with

almost 60% market share and hence is in a better position to control prices |

| Company has already developed a pipeline of products in the international markets which it can launch in the Indian market as the market develops. |

| R&D expense is likely to be low due to this reason |

| ROCE is 30% + and is likely to improve as the business model is

very asset light |

| Healthy growth is going to enable a spread of fixed expenses

such as marketing and distribution thereby improving margins |

| India will have one of the youngest working age population by

the year 2021 after which it will start reclining - currently menstruating

population is 355m which will increase till the year 2021 |

| WC cycle is extremely efficiently managed. If cash and loans to

group companies are excluded, the company is net negative working capital |

| Extremely strong brand recall making it difficult for new

players to make an impact unless they are willing to spend heavily on

advertising |

| Product is a necessity and during times of recession, a woman

who has started using these products is less likely to switch back to

traditional methods |

| The market share of the brand is said to be expanding over the

last few years |

| Governent trying to increase awareness and raise consumption by

offering free samples of products |

| RISKS |

| A lot of new entrants and competition from the likes of

Unicharm and SCA is only going to intensify thereby putting pressure on

margins (however none have the reach or distribution capacity |

| The company can decide to raise royalties on an ad hoc basis

which will affect margins (royalty in 2005 - 2.5% in 2013 is 5%) |

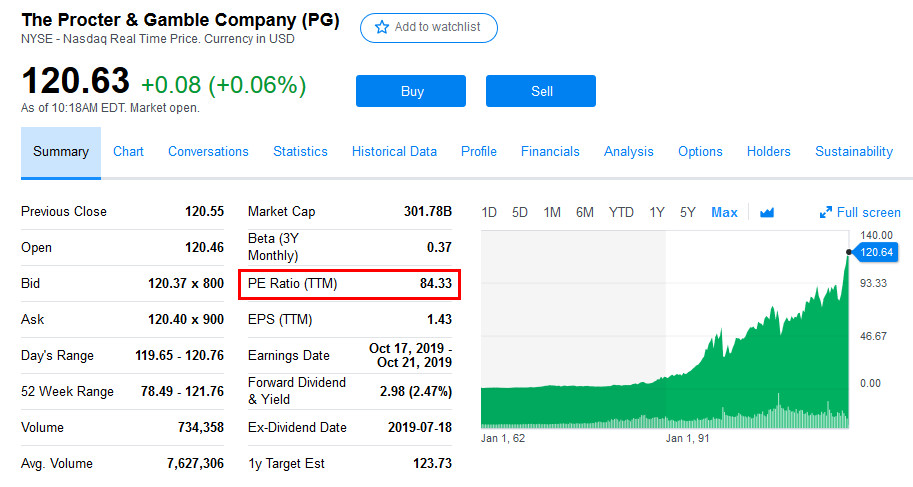

| PE ratio of 46 means that the growth is fully priced in - PEG > 2 |

| Government may decide to levy excise duty on sanitary napkins

again in the future which will impact the sales growth and margins |

| The male female ratio continues to decline in our country |

| Relaunch of Old spice brand could drain the profitability of

the company in the short term |

| Usage of unorganized unbranded products pushing prices down |

| VERDICT |

| Buy but at a PE ratio of between 35 and 40 times |

| Target price to buy should be approx 2400-2700 |