P&G listed arms are - P&G HH, P&G Health, Gillette…which is the 4th one?

I agree with you on all points…infact Gillete is also a hygiene theme product. It is amusing what is battery doing inside a Gillette

Having said that, many years I had shunned these MNCs because of this very reason of unlisted subsidiaries etc. only to see them create wealth for others

It is confusing as minority Indian investor, what should we do…

Additional product launch: India business contributes 2%+ in revenue for the parent company. When one looks at the ARs of PGHH and Gillette, it becomes evident that the parent treats all India businesses as one unit. The above inference comes from the observations such as sharing of management & admin expenses, lending money across companies and writing content of the chairman or MDs letter. On a lighter note, Chairman’s letter in the ARs of Gillette and PGHH are Ditto for FY 19 except the photo and signature whereas MD’s letter is almost identical except the change in product names and company specific initiatives, which match in spirit as the same talk about initiatives that have ‘Women’ independence at core.

On the launch of additional products or look in to the business strategy, ARs hardly provide any clue in either companies case. The ARs of Gillette and PGHH flow like a standard template.

On hearing/ reading at few places beyond the ARs, the current MD-who has been elevated in FY18 - does talk about their relentless focus on:

1- Expanding the existing categories reach with improvement in network for point of sales, Supply chain efficiency and products by innovation to make them affordable for masses.

2- Sustainable and Balanced growth in Top and Bottom line with real CASH profits.

3- Customer at core of all activities while better results will be a net outcome.

4- Providing better solutions to existing alternatives, ensuring attractive packaging, communication and availability for the product.

In my understanding, it’s a simple business that generates real cash and can be understood by immortals like me. The business belongs to a solid parent and is run by professionals. Indian opportunity is HUGE and expanding even if one considers only the existing product categories. In case the company keeps executing well on point 1 to 4 mentioned above, parent should be more than inclined to harness the Indian opportunity.

The bigger question that one should work upon is to find the ‘RIGHT’ range for one to swing his bat to become a partner in the ride.

In short: I do not know.

Why huge Dividend?

Same as above. But it does seem that it was done for both the listed companies,Gillette and PGHH, in order to celebrate the 30 Yrs.

I see you have read beautifully between the lines…this is simple yet significant insight. Thanks…

From your experience on MNCs have you figured out exactly what benefits they get to have some listed and some unlisted subsidiaries in India? It cannot be a coincidence with so many such examples like P&G, Abbott, Honeywell etc…and all from excellent parents… Thanks

There are mainly two kinds of benefits of having unlisted subsidiaries.

Financial Benefits

In India, the MNCs can’t have more than 75% ownership in a listed subsidiary, so they can get only 75% of total dividends. In unlisted subsidiaries they get 100% of dividends.

Also, 100% ownership means complete benefits of capital gain. However, this will help them if they ever decide to raise money from private investors.

Royalty & Technical Know-how fees don’t depend on shareholding %. However, the companies can’t charge any arbitrary amounts. In India royalty payments linked to brand usage or such matter will require shareholder approval if it crosses 5% of annual consolidated turnover.

Strategic Benefits

Listed companies have many compliance norms.

Without full ownership management / promoter won’t have full voting rights to make some urgent resolution.

Previously MNCs had around 90% ownership in listed subsidiaries, and so when the rule came out for ownership % reduction many went for delisting. This caused the market participants to shore up the share price of those companies much above their intrinsic values, which ultimately put off many of those MNCs’ delisting plans. IMO, therefore, most of them opted for unlisted subsidiaries to launch newer products in India.

It may be a way to avoid ‘PUBLIC’ disclosure of your strategies while taking tough decisions to make the business work in situations where the market is hyper-competitive and price sensitive… Just an opinion and no facts to back it up.

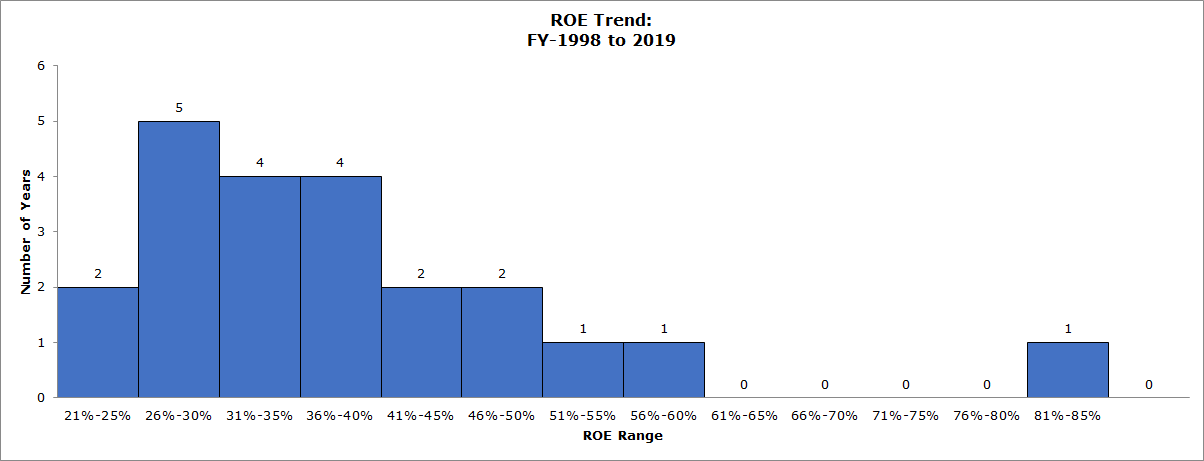

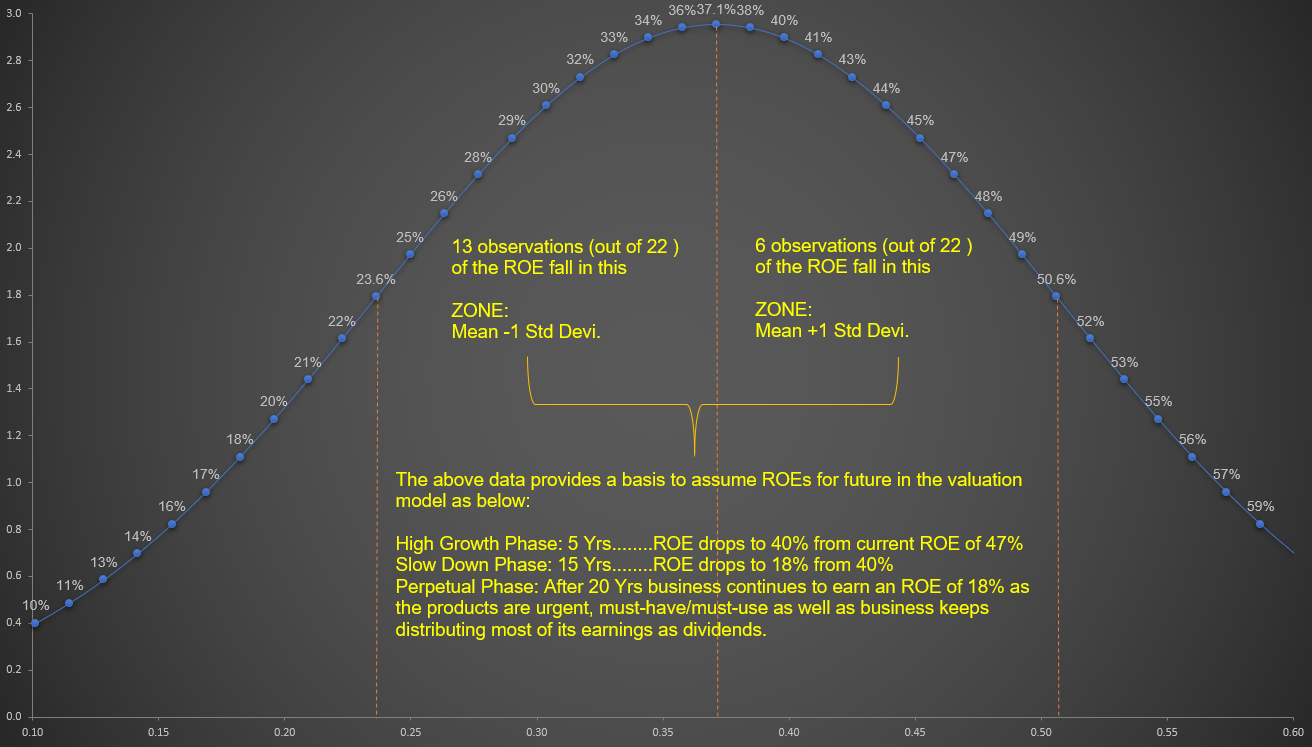

Let’s see what’s evident in numbers. Here is the snapshot for the ROE trend, which might help us to plug in the valuation model to arrive at elusive IV, for data from FY1998 till FY2019 (22 Years). The business has a sweet spot to earn ROEs of 26% to 40%.

@Surender@sujay85 thanks for your replies…while I fully understand benefits of having unlisted entity alone…my question was why many excellent parents have a combination of listed and unlisted entities…why list them in first place if they greed for unlisted benefits…one reason could be they got these listed businesses as legacies by buyouts, any restructuring etc. Or maybe because of old government rules for compulsory listing…I am not sure…and that’s what I need to understand that why list at all… thanks

I further analyzed the 22 Years ROE data using ubiquitous ‘BELL-CURVE’.

Do help by questioning or providing feedback on the sanity of the thought process as the same will provide me to think and understand better. Here is the gist:

As far as I know , these didnt want to be listed but thanks to regulatory requirements got listed. And thanks to regulation public got the opportunity to invest in them . These are opposite to those cases who come to market for capital while these dont need any capital as is evident from their stellar roc and healthy cash flow . While listed and unlisted in a way is unethical and I wouldnt have wished it that way, ultimately these companies arent wrong as they are responsible for their parent roc . Hence I exited p&g and gillette long back and am invested in companies like Nestle etc which are very fair. Even HUL doesn’t have unlisted subsidiary to my knowledge

Ok, what about others , i mean Pampers, Ariel , Tide, Ambi Pur, Head & Shoulders, Pantene , Olay are these under P & G Hygiene and Health ? Or are they not part of the listed company.

Procter & Gamble Hygiene and Health Care Limited (PGHH): The Company is engaged in the manufacturing and selling of branded packaged fast-moving consumer goods in the femcare and healthcare businesses. The Company’s products are sold through retail operations including mass merchandisers, grocery stores, membership club stores, drug stores, department stores, and high-frequency stores. The Company has its manufacturing locations at Goa and Baddi in Himachal Pradesh, apart from third-party manufacturing locations spread across India. Company’s operating segments are:

Health care products - Comprising of Ointment and Creams, Cough Drops and Tablets.

Key Brand: VICKS

Hygiene products - Comprising of Feminine Hygiene products and other skincare hygiene products.

Key Brand: WHISPER. The Company claims to command a market share of 50%+ in this category

Key Brand: Old Spice – As of now, it’s in the sunset phase for new investments due to lack of anticipated sales in the market.

In FY19, Hygiene products contributed 70% of the Company’s revenue while the Health care products contributed the rest in overall sales of 2946 Cr. The company’s ARs from FY07 onwards mention the companies focussed efforts to expand the market size of Hygiene products using the following approaches:

Distribution of Trial Samples by various channels such as Public-Private partnership with state governments for Door to Door Marketing, and visiting schools.

Go to Market Entry initiative: A school level program, which covers 4.5million potential consumers, at to educate the females about the sanitary aspects of menstruation phase.

Innovative Product launches that cater to different price points to enable affordability for the majority of consumer segments. In FY18, Company did Whisper portfolio expansion by extending it from ‘Period protection’ to overall ‘Feminine wellness’ via product named as Whisper daily liner.

Distribution expansion for wider availability

Substantial advertising

What’s likable?

Strong Balance Sheet: No Debt, No Equity Dilution (Checked from FY08 onwards).

Continuous wealth sharing as dividends.

Company’s Hygiene products have grown at a rate of 18% over the last 13 years. This category has a long runway considering India’s demographics, lower penetration of sanitary products, urbanization trend where females ratio in various jobs is bound to improve.

Best suited for an equity investment as the company can be valued using DDM.

Strong Parent with a rich legacy.

High Promoter holding (70%+)

Recessions proof product that is must-have, has a repetitive demand and is a small expense in the overall monthly budget.

Low Capex needs. Depreciation is higher than CAPEX over the years. However, Advertising expense, 10% of sales on a consistent basis, is the real CAPEX for this business to maintain the brand pull among consumers.

Reputed Auditors.

Negative Cash Conversion Cycle

20%+ ROE over the last 22 years. See my earlier notes.

Risks:

Rich Valuations with inconsistent dividend pattern.

Products cater to only two categories.

Potential candidate for delisting in the future.

Negative/Negligible growth in FY16, FY17, and FY18. I assume that it was primarily due to a major cut in trade incentives from FY17 (see Addendum Data). Also, GST came into existence in FY18. It seems that to overcome the slow growth, the Company scaled up Advertising expense from FY18.

Hi the company was averaging between 30-40 EPS/qtr before and now that has shot up to 75-80 range, I am unable to understand why this is happening? There does not seem to be an increase in CAPEX or fixed assets and the growth seems very high for organic growth?

You may want to read the coverage of MOSL on the stock or download the company’s result releases to get an answer to your question. In brief, they’ve had some one-off gains over the last two quarters that has led to significant jump in the bottom line. Adjusting for the one-off gains the sales are up ~18-19% and bottom line ~30% or so in 1HFY21.

Ever since the new MD and CEO (Madhusudan Gopalan) has come in, sales have started growing nicely.