Background

Goldstone Infratech Limited is registered in the year 2000 with their only product segment as electric insulators. The company got listed in the stock exchanges in the year 2002.The promoter group is Trinity Infraventures limited who are also promoters of Goldstone Technologies which is another listed company in India.

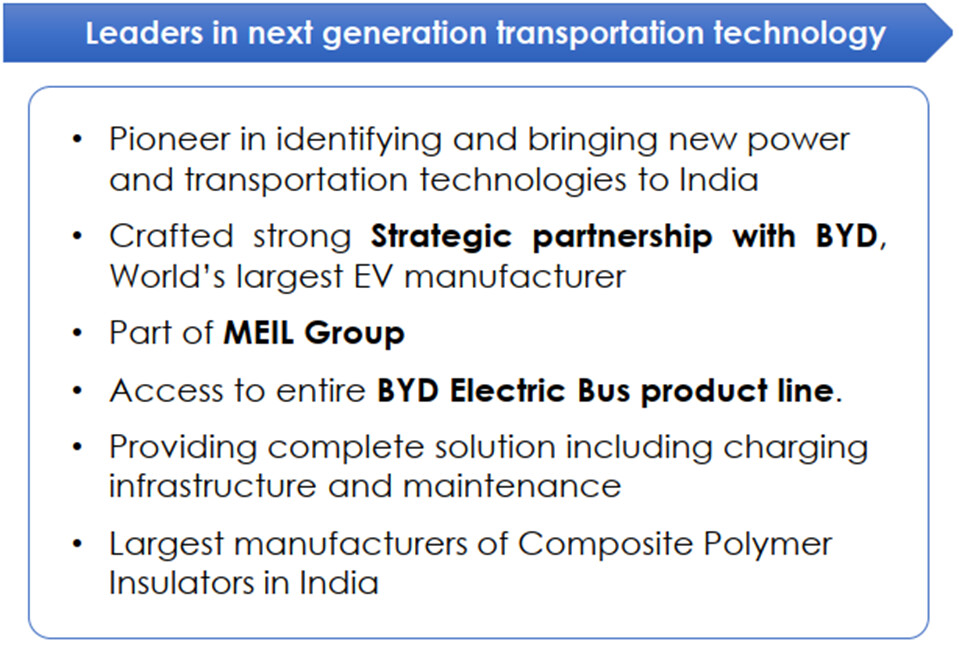

The company started electric buses division in 2015 having a strong partnership tie-up in India with Warren Buffet backed BYD Auto from China.BYD is a pioneer in EV battery space and has a significant presence in EV ecosystem right from rechargeable batteries to electric buses, trucks, cars etc.As per Wikipedia BYD page - As of 2021, BYD Auto is the world’s second largest New Energy Vehicles carmaker in the world, with 329,408 units sold in January-September 2021

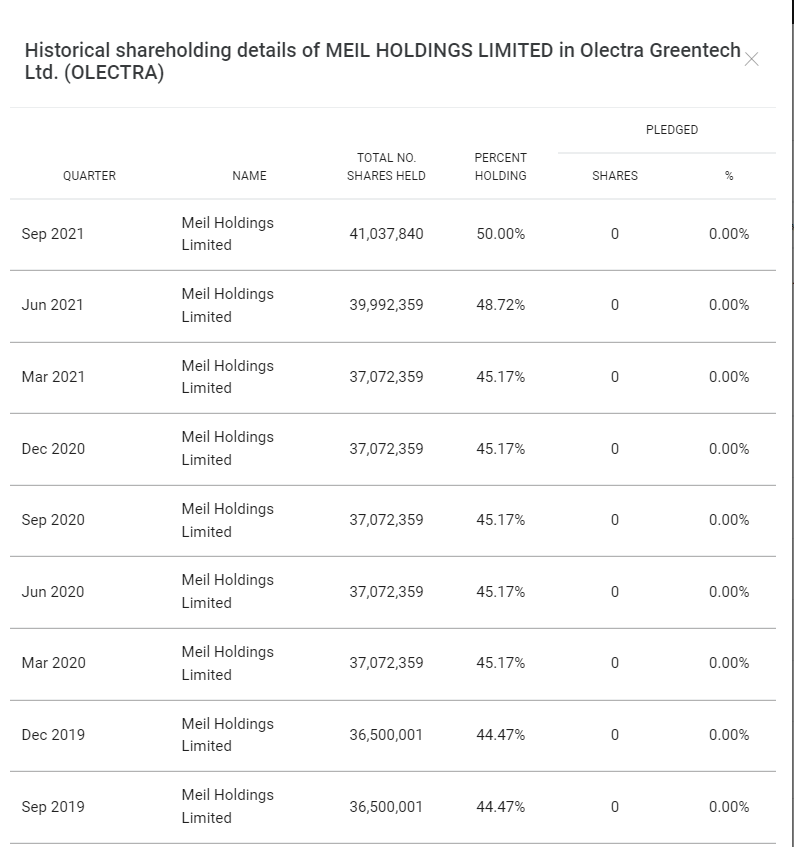

In the year 2018, the company’s name is changed to Olectra Greentech, and MEIL Holdings, which is a subsidiary of MEIL(Megha Engineering and Infrastructure Limited) company came up with open offer and increased stake in Olectra. At the moment, MEIL Holdings hold more than 50% stake in Olectra making it a subsidiary and all the previous promoter group entities have reduced their stake.

My understanding is, there was an unwritten agreement between the old and new promoters that the old promoters have to completely exit Olectra once new management takes over.

The new promoter group(MEIL) is one of the biggest and successful infra player in India and have been regularly featuring in the top 100 of Hurun India Rich list.

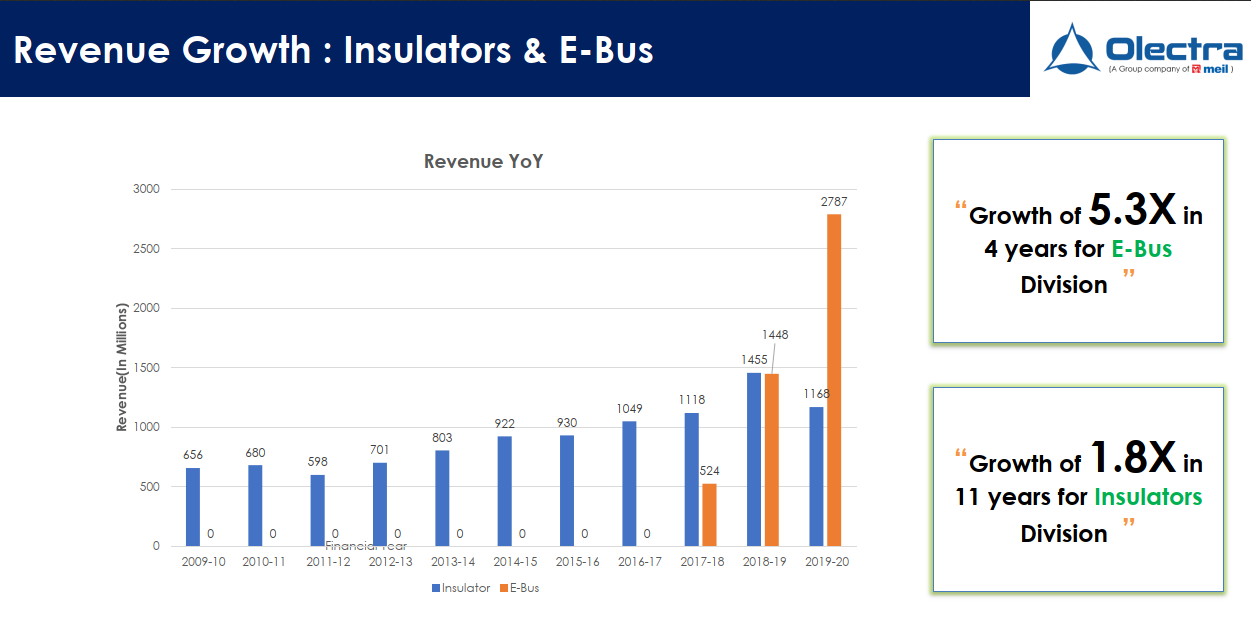

The bet on Olectra is primarily a bet on the E-Bus segment which has huge opportunity. The revenue growth in insular division is minimal from past 10 years.

Electric Bus

Industry Structure and Development:

The oath taken for Faster Adoption and Manufacturing of Electric Buses in India by NITI Aayog in 2017-18 through Department of Heavy Industries (DHI) has initially launched, FAME I scheme, facilitating “Capital Subsides” for 560 of Electric Buses has given encouragement to State Transport Undertakings (STUs) in 11 Indian cities, to own the EV Buses in their fleet, and their long awaited desire to operate and witness the performance of Electric Buses became a reality in India with the subsidy support provided .The Succeeding FAME II scheme notified in 2019-20 was initially aimed to deploy 5595 no. of E Buses in various STUs under Gross Cost Contract (GCC) Operational model, which has attracted attention of 64 cities to deploy Electric Buses without any investment from STUs. In 2020-21, DHI has sanctioned subsidies for additional 670 Buses. GCC model has enabled Private investments in this sector and STUs thus need not facilitate any finance arrangements for the After-subsidy costs of Electric Buses.

Since the deployment of Electric Buses under GCC Operational model is for the first time in India, STUs have taken some time to understand the technical feasibility, financial viability, economic feasibility and Operational compatibility of E-Buses, including Routes and Schedules management. Early deployment of E Buses under Operational Model in cities like Pune has given tremendous insights, analysis and study practices to all the other STUs in India. Delay in understanding the EV technology and viability factors has led to conclude projects in snail pace. The successful deployment of Electric Buses in GCC model has ignited the momentum in EV Bus adoption in India. Despite non-operation of Public Transport during COVID Wave I & II, Department of Heavy Industries – DHI along with State Transport Undertakings - STUs, and Urban Local Bodies (ULBs) have successfully implemented FAME II.

More than 1000 electric buses are running across the country with an additional 2600 electric bus orders are in execution stage under FAME -2 scheme. Accordingly, DHI has extended the FAME II scheme validity till 31st March 2024 for a period of additional 3 Years from 1st April 2021 It is also understood that in India that STUs having deployed Electric Buses with Longer Range have been be progressive in their next set of deployment. The COVID-19 crisis will create many new challenges for this sector, especially in urban areas and intercity segments with high travel demand. Finally, the vision of NITI Aayog that only electric vehicles should be sold in India after 2030 would result in a reduction of 156 million tons in Diesel and Petrol consumption with net saving of roughly Rs. 3.9 Lakh Crore by 2030 at present oil prices.

Source – Company’s 2021 Annual Report

The management discussion and analysis section starting from page 90 to 95 in the 2021 annual report is worth reading to understand the complete context

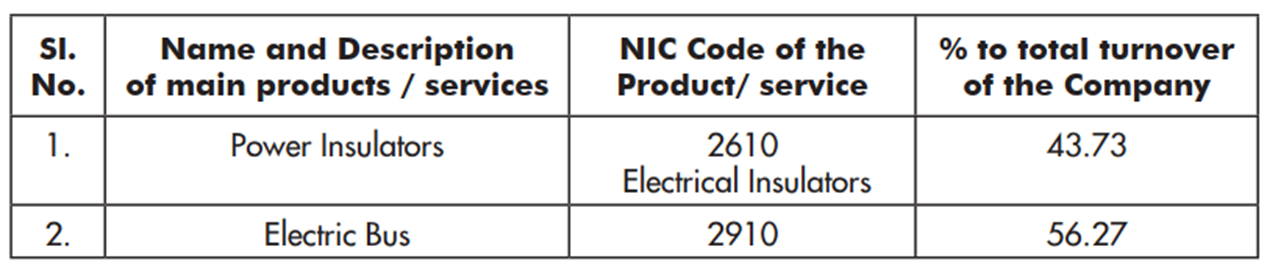

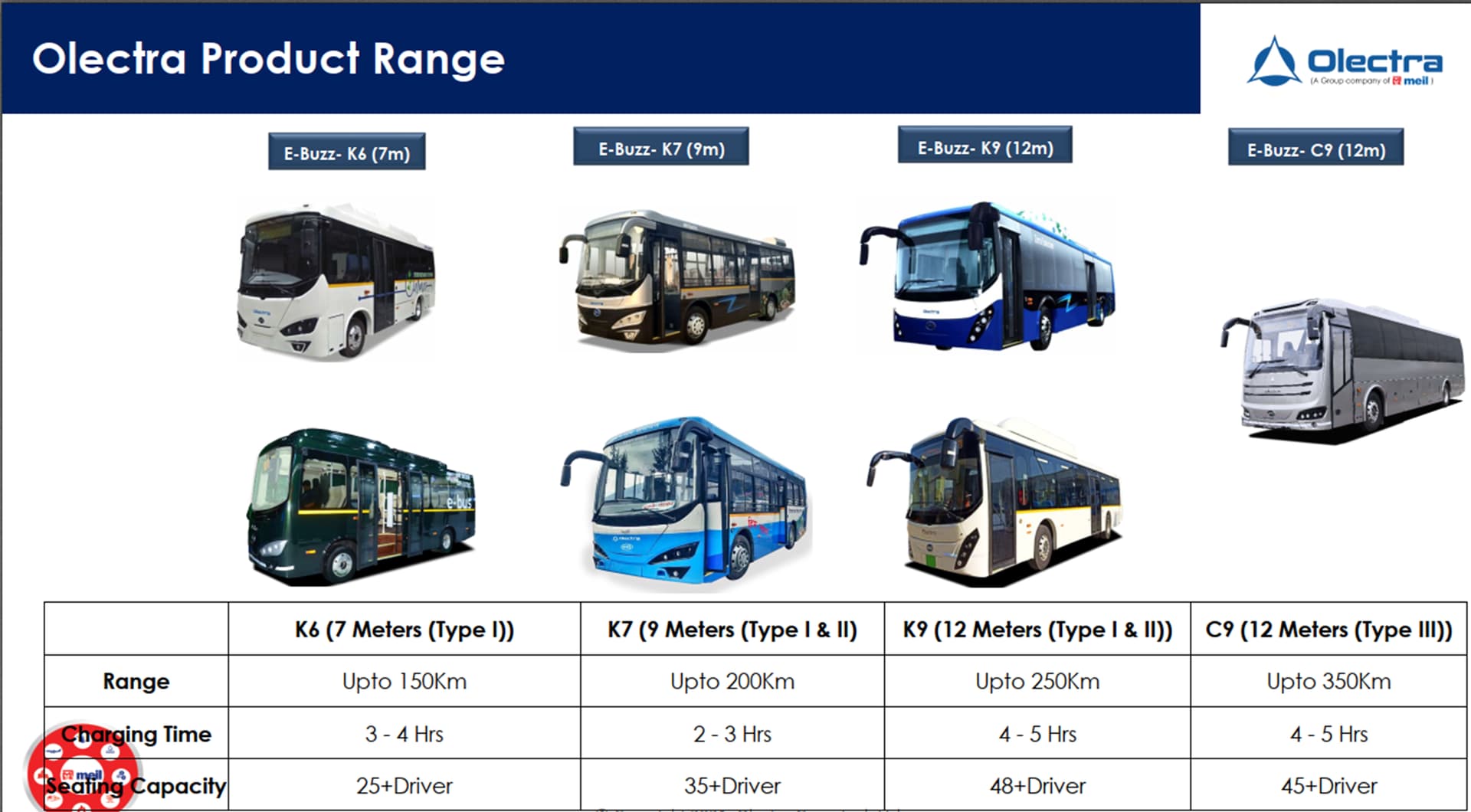

Main Products/Segments

Source – Company’s 2021 Annual Report

Source for the images above – Company’s Investor presentation dated 09.11.2021

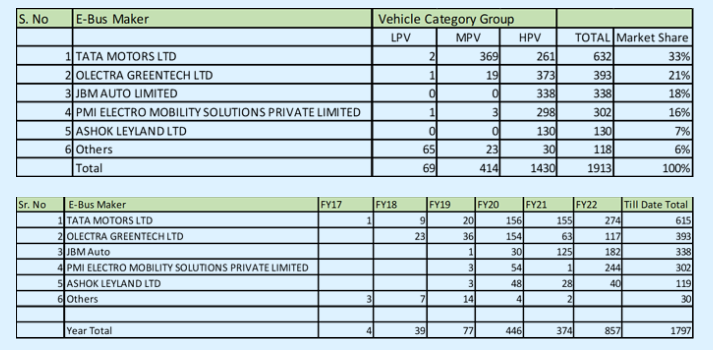

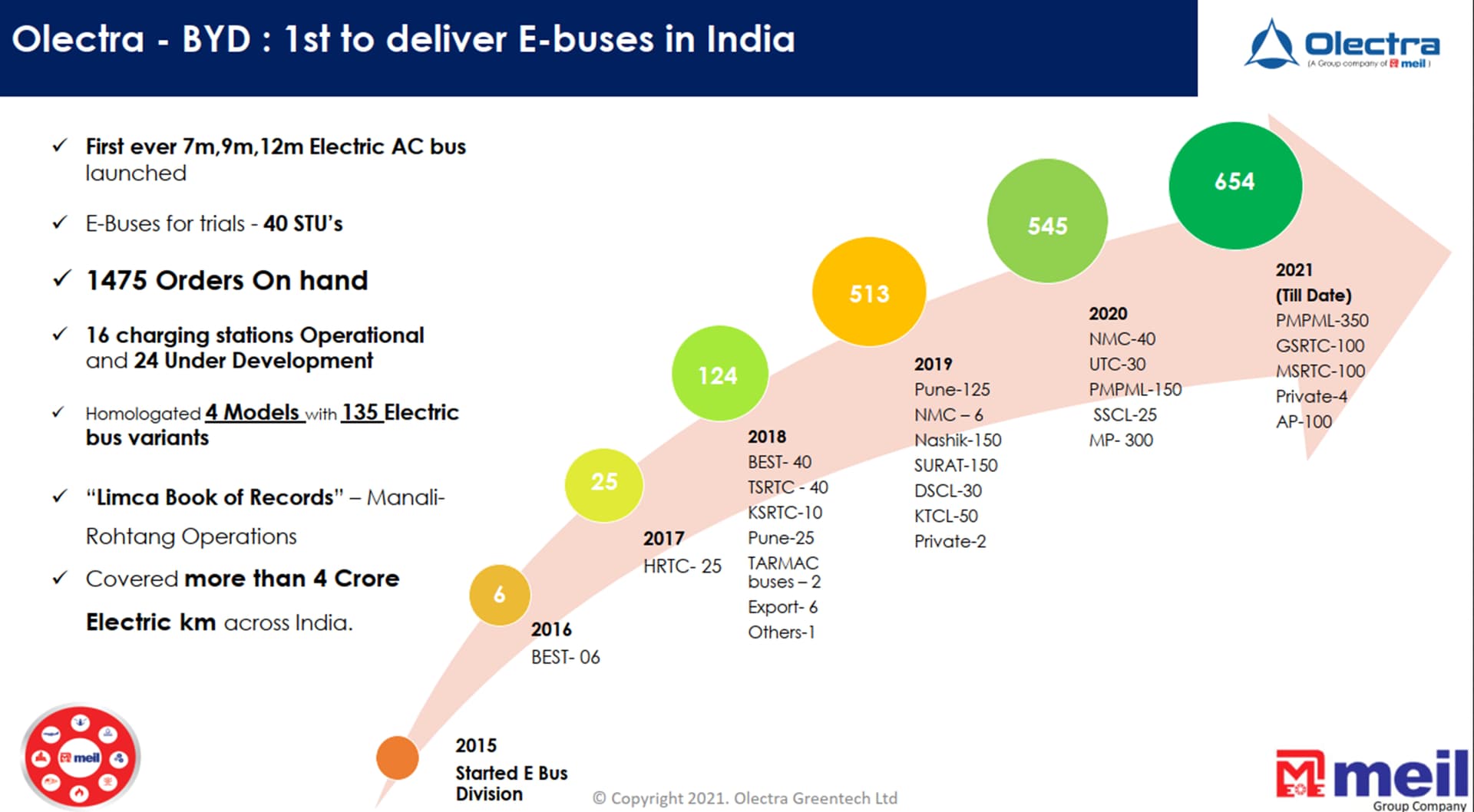

Main Markets/Customers

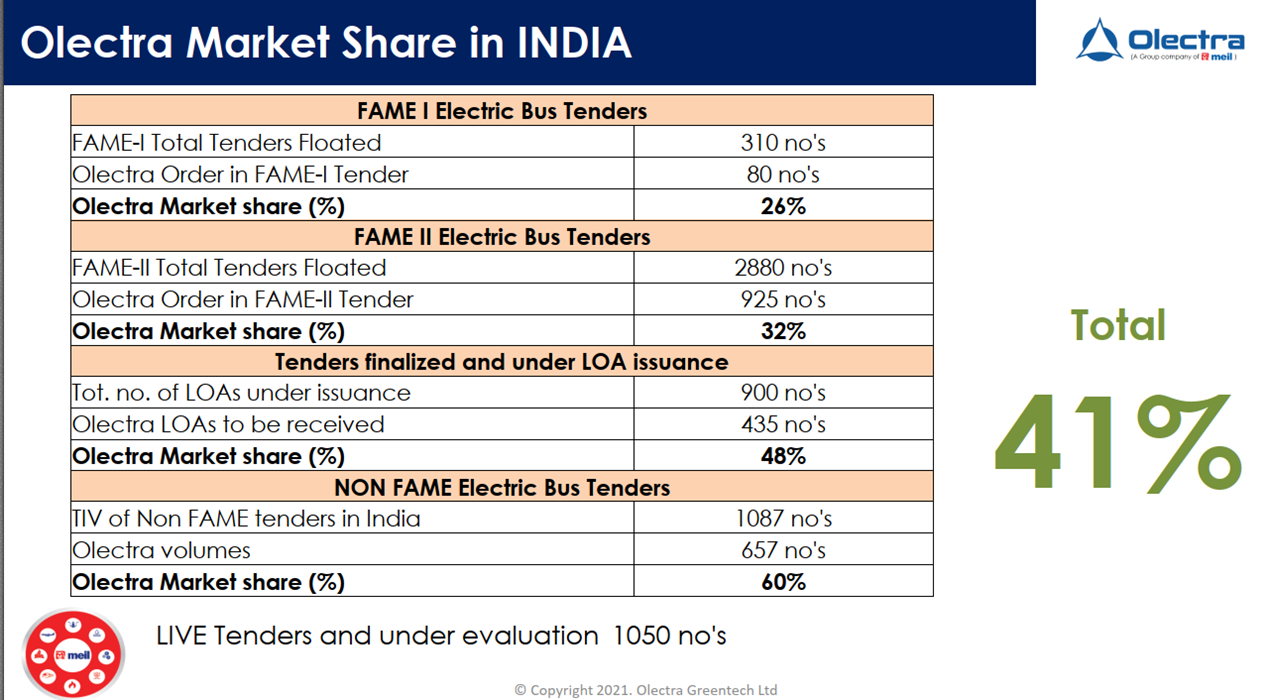

The State Transport Corporations(SRTUs) are the main customers for Olectra. Olectra is the market leader in electric buses in India.

Source for the image above – Company’s Investor presentation dated 15.09.2021

Current Market/Industry Trends

Outlook

Electric Bus market is expected to grow rapidly in India considering various factors like hikes in Diesel prices, Diesel fleet purchase holiday during COVID-19 impact, EV Policies across country, State Government commitment to EV adoption,Grid balancing factors and Power surplus States, Lesser Bus ratio vs 1000 Population, etc., NITI Aayog has mandated aggregation of demand for 5,500 Electric Buses in India through Convergence Energy Services Limited (CESL) and World Resources Institute(WRI) , for which the process has already begun by CESL.

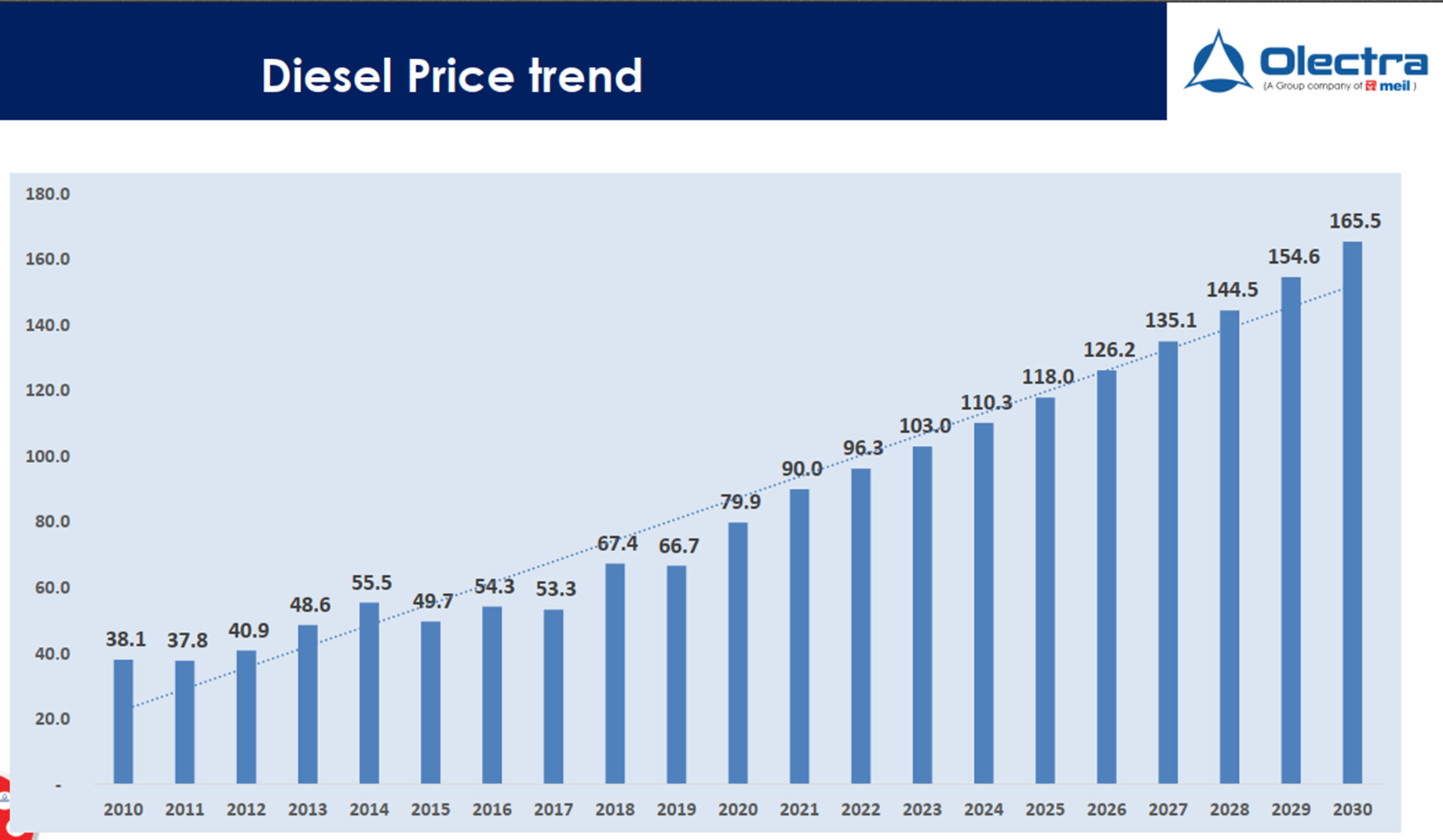

Diesel prices in India have been hiked 69 times in this Year, which is expected to be further increased. Huge financial impact is seen on the Public Transport Undertakings fleet operations with the increased diesel prices. Hikes in Fuel costs are one major factor that been shift Diesel to Electric. The said hikes are also impacting the Total Cost of Ownership for Diesel fueled Buses. The current Climate Policy in India is rightly addressing the challenges of electric buses and providing an environment to accelerate their adoption and implementation.

This current trend of increase in Diesel prices, seems consistent and expected to continue. Diesel Fuel cost is contributing to 40% of CPK in Mofussil NonAC Buses and 50% in AC Intercity Buses. Public and Private Transport fleet expected an early adoption with faster growth compared to previous Years adoption.

CESL entry into E Bus aggregation in India will further improve the Market opportunities as CESL will be acting as Aggregator between STUs, Operators and OEMs. CESL main focus is to aggregate the demand in 9 cities taking into consideration Public Transport, Last Mile connectivity for Metro, Airport Tarmac Electric fleet, etc., In the FAME II Phase I Scheme, a New Segments like Intercity deployment has successfully taken off in form of concluding contracts by MSRTC, KSRTC and APSRTC.

Last Mile connectivity Project has also been initiated by Delhi Metro Rail Corporation – DMRC under FAME II Scheme. Opportunities in the form of Metro Neo projects in India will further open a new segment for Electric Buses. Few Green fund agencies are also aggressively preparing their strategies to deploy Electric Buses in India for Private Sector deployment.

Source – Company’s 2021 Annual Report

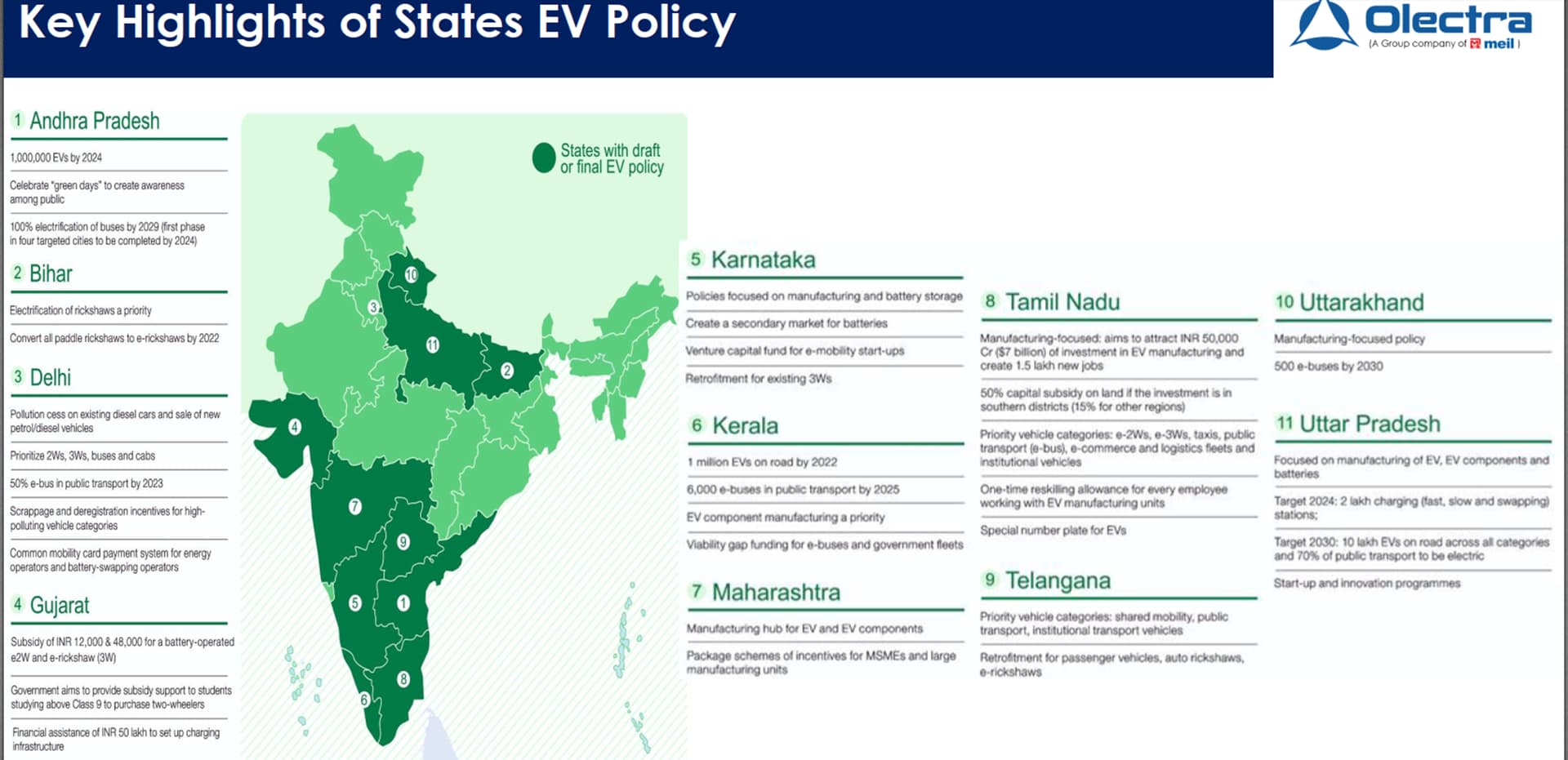

Many states have got their EV policy draft ready.

Source – Company’s investor presentation dated 15.09.2021

Bullish Viewpoints

- Gross Cost Contract model will solve the biggest problem of SRTUs - huge Capex front load is no longer a viable option especially with many years of losses

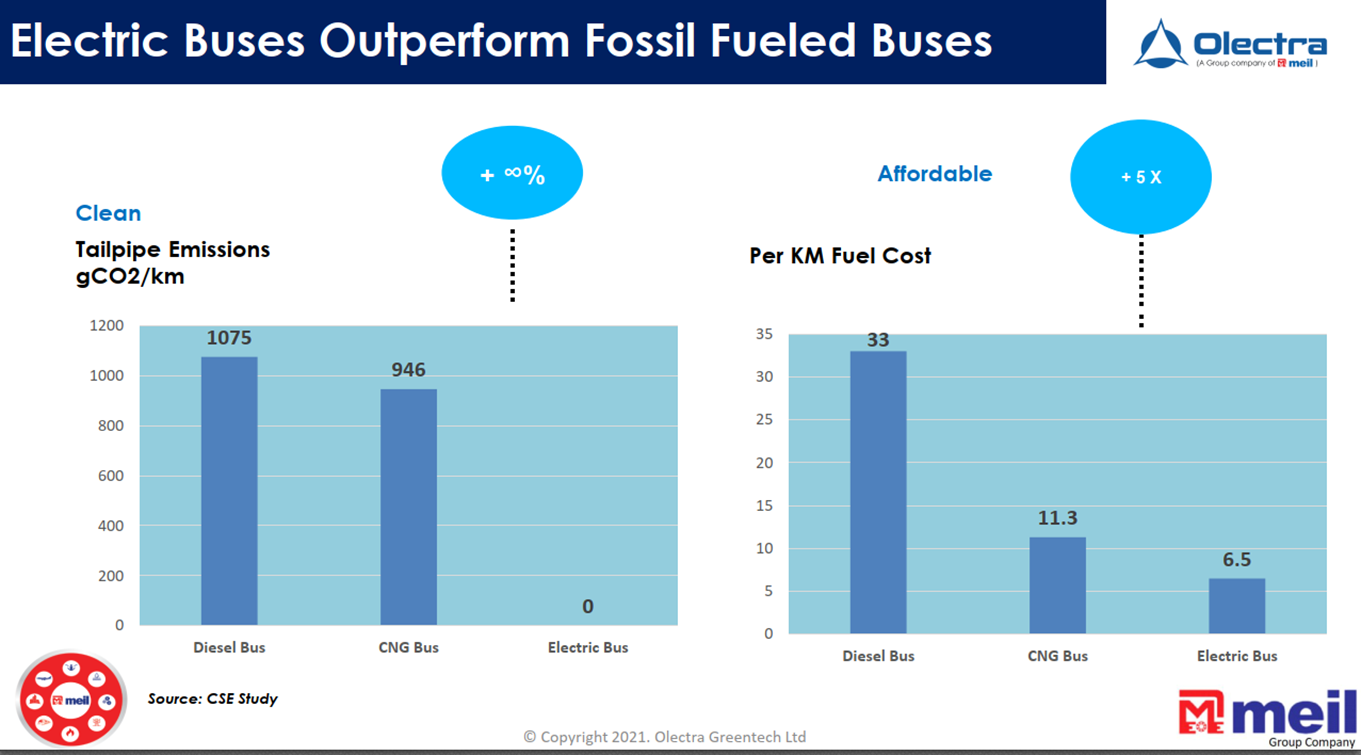

- The cost of operational costs and maintenance of electric buses is very less compared to diesel and CNGs

- The cost of operational costs and maintenance of electric buses is very less compared to diesel and CNGs

Source – Company’s investor presentation dated 09.11.2021

- Well placed to attract ESG investors and Green funds

- Government of India wants to reduce dependency on Oil and so pushing EVs, eventually pushing for only EVs after 2030

- Leader in securing the orders and first mover advantage having operations from 2017. At the moment, they have a market share of ~40% of electric bus orders in India

- The opportunity size is huge as the bet is not just on the Electric Bus alone as its future plans include manufacture of Trucks, LCVs, 3 wheeler’s etc

Source – Company’s investor presentation dated 15.09.2021

Bearish Viewpoints

- Technology rests with BYD and BYD can start its operations in India on its own. They already have their plant in Chennai and were planning to venture into categories other than Electric buses on their own previously.

- The mitigation to this is to have an exclusive partnership similar to Maruti-Suzuki model. At the moment, BYD Auto has zero stake in Olectra shares.

- BYD being from China can affect company’s prospects adversely due to sentiments at border

- Inherent risk of damages to public property (incl buses) in exceptional situations likes riots

- Regulatory risk as government can enforce new policy unfavourable to EVs or delay EV adoption to save existing industry like postponing scrappage policy

- The target customer market segment is government backed State Road Transport Undertakings(SRTUs) and B2G segment is very tough nut to crack

- The new promoters (MEIL) are well known for executing government projects(50% of order book) and have a successful track record of completing big projects

- Electric Bus technology is relatively new and we don’t know all the risks associated with it

- Promoter is new to bus industry and the other competitors like Tata Motors, Ashok Leyland, JBM Auto are well entrenched in this industry from long

- Currently, government is supporting EV push by giving subsidies in the form of FAME-I and FAME-2, no idea whether they will continue to support

- However, with Gross Cost Contract(GCC) model, there is no CAPEX load on SRTUs

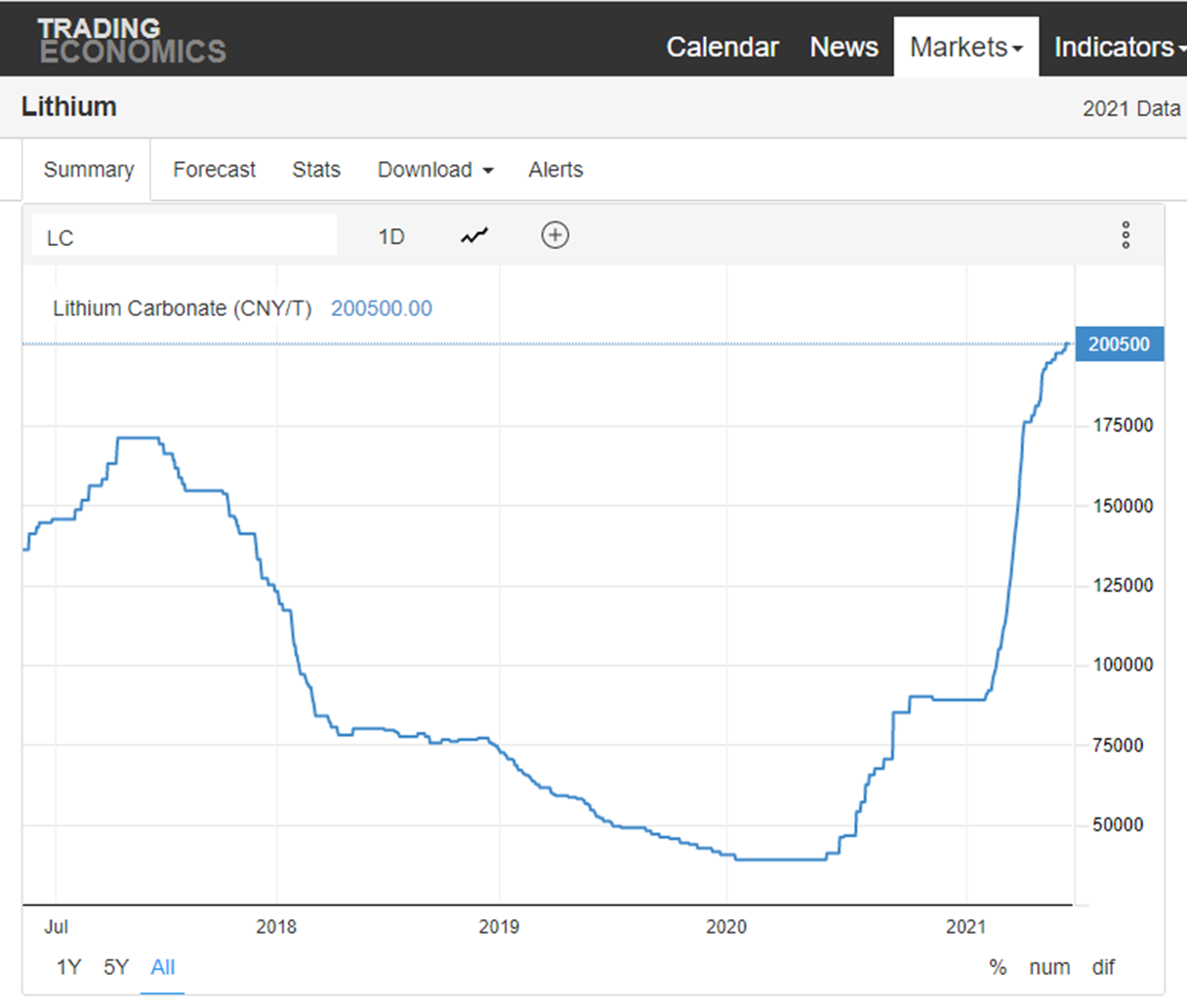

- The cost of battery(Lithium Ion) is around 40 to 50% of the overall cost of the electric bus. Any significant increase in the price of Lithium will adversely impact the sustainability of the business model

- China has 12.2% of world’s lithium production in 2020

Source – Trading Economics

- Elon Musk. No idea, what are his plans in electric bus space or even new battery technology

Interesting Viewpoints

-

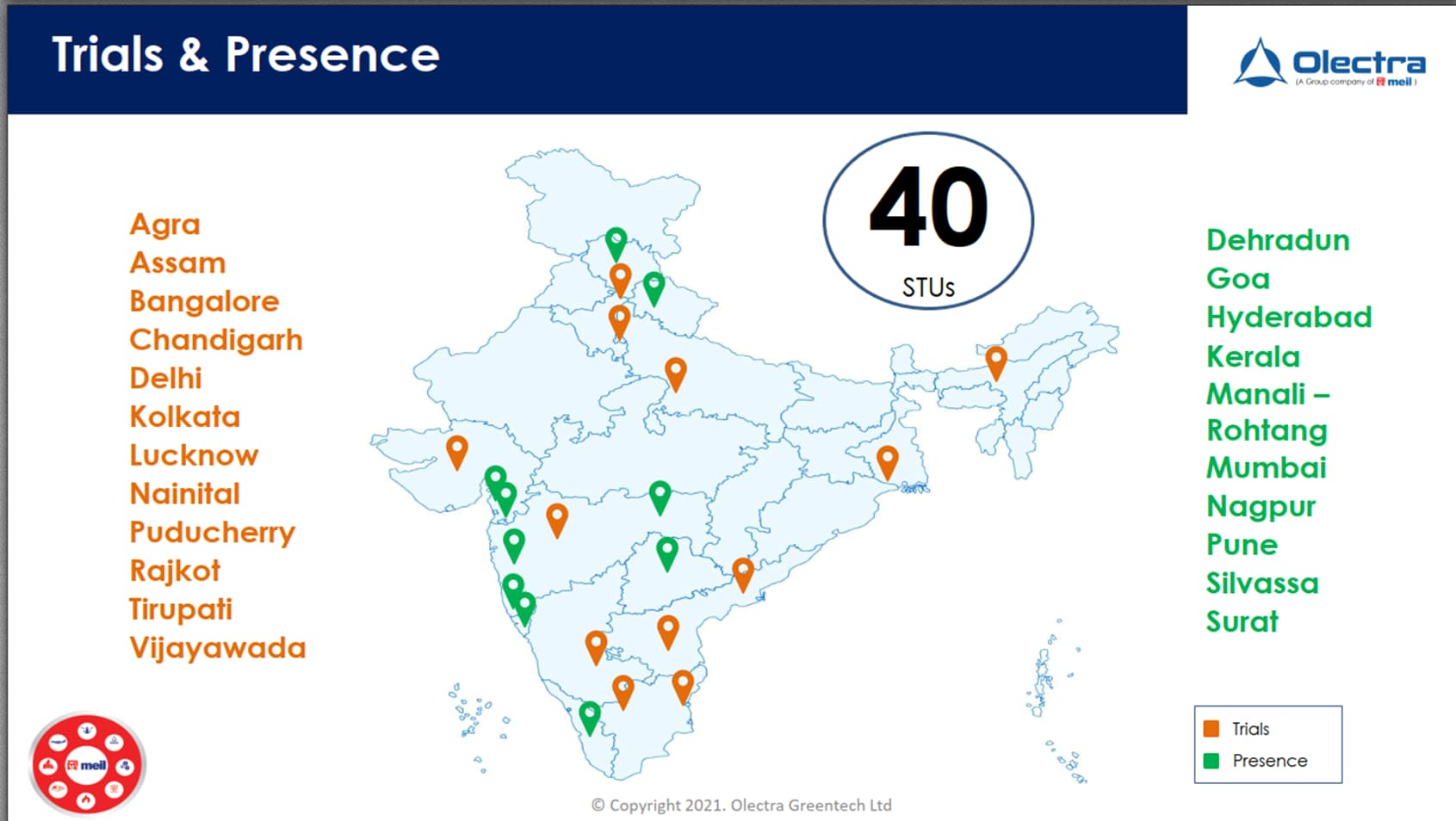

Olectra is either in trails or presence in 40 STUs

Source – Company’s investor presentation dated 15.09.2021 -

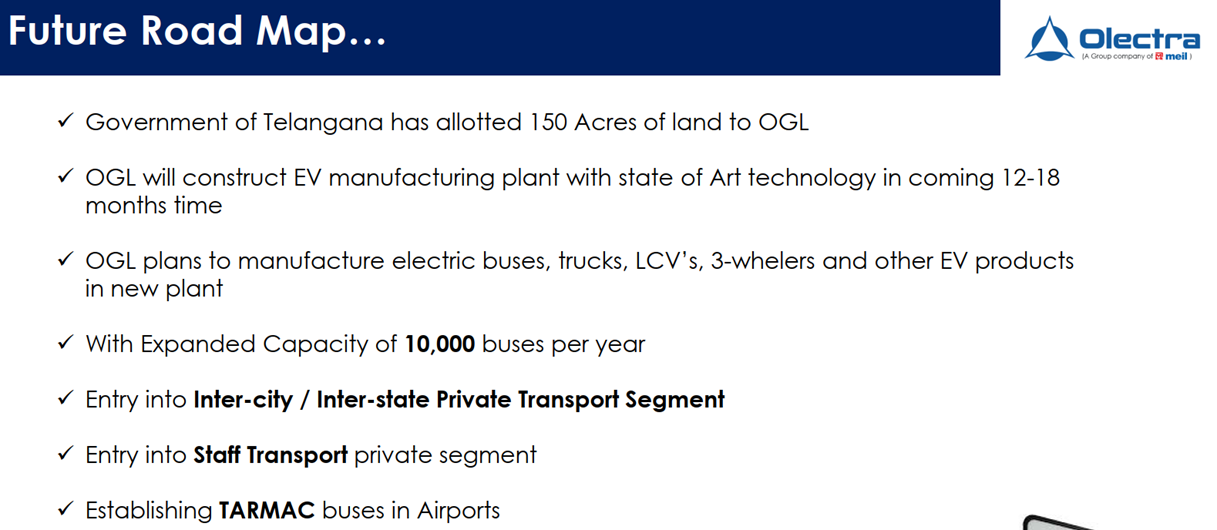

Promoter is not just looking at Public Transport but other adjacencies like inter-city/inter-state, private transport segment and also into TARMAC buses in Airport

Source – Company’s investor presentation dated 09.11.2021

Barriers to Entry

- There are almost no barriers to entry

- The target customer segment is State Road Transport Undertakings and dealing with government organisations is very difficult

- Olectra is the only company giving more than 250 kms for single charge. This is a great barrier especially if one is interested to run inter-city buses

- If I remember correctly, Ashok Leyland uses replaceable batteries to mitigate this risk

- To execute GCC contracts of bigger scale and long payback periods, you need to have very good money muscle and so smaller players may not be able to compete

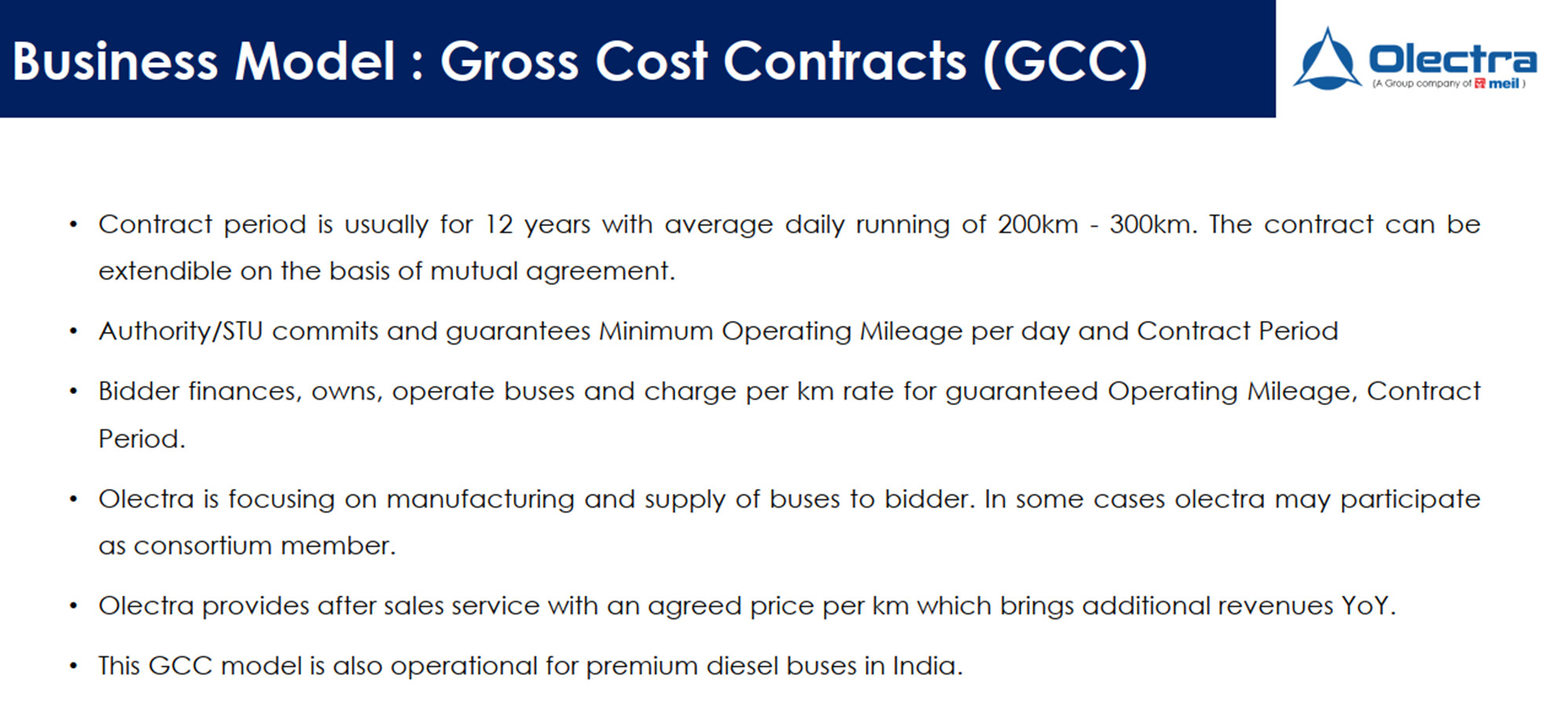

Business Model

Olectra has BYD as the technology partner which basically provides the most important components of electric bus like battery and technology.

Olectra mostly does the assembling of parts. Usually, the cost of electric bus will be in the range of 1 to 2.5 crores.

The most important target customer segment for electric bus is SRTUs and they are all usually running in operational losses.

This is where Gross Cost Contract model will help as SRTUs don’t need to do Capex but agree on paying bus operators with price per km.

This model is already operational in some diesel buses and compared to diesel buses, the cost per km is very less for electric buses.

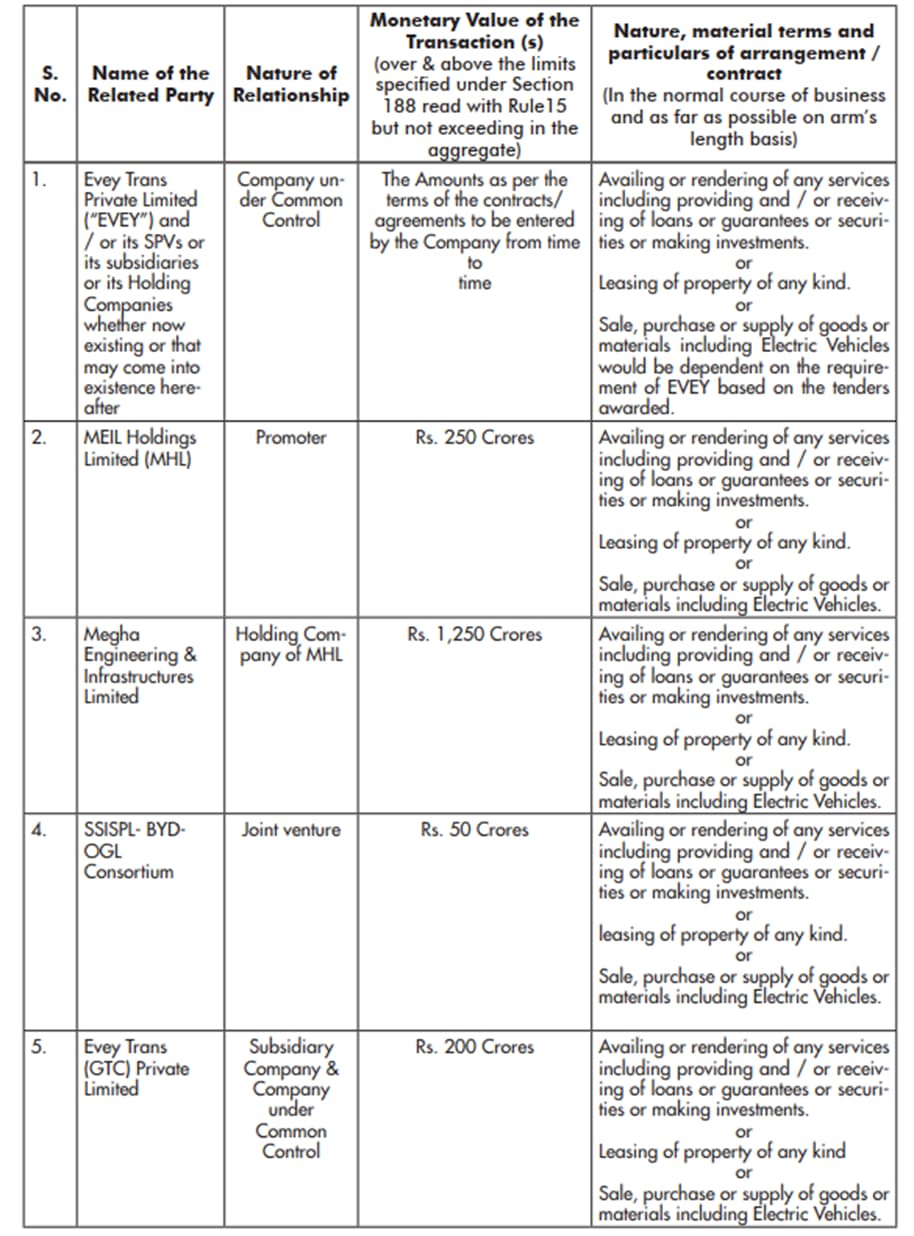

Holding Structure

Evey Trans which is a subsidiary of MEIL Holdings, buys electric buses from Olectra and creates Special Purpose Vehicles(SPV) for each Gross Cost Contract(GCC).

Hence, you see many related party transactions. I just mentioned only two in the above structure

Source – Company’s investor presentation dated 09.11.2021

Source – Company’s investor presentation dated 15.09.2021

Valuation Model

The bet on Olectra is basically a bet on the number of E-buses it sells.

Source – Company’s investor presentation dated 09.11.2021

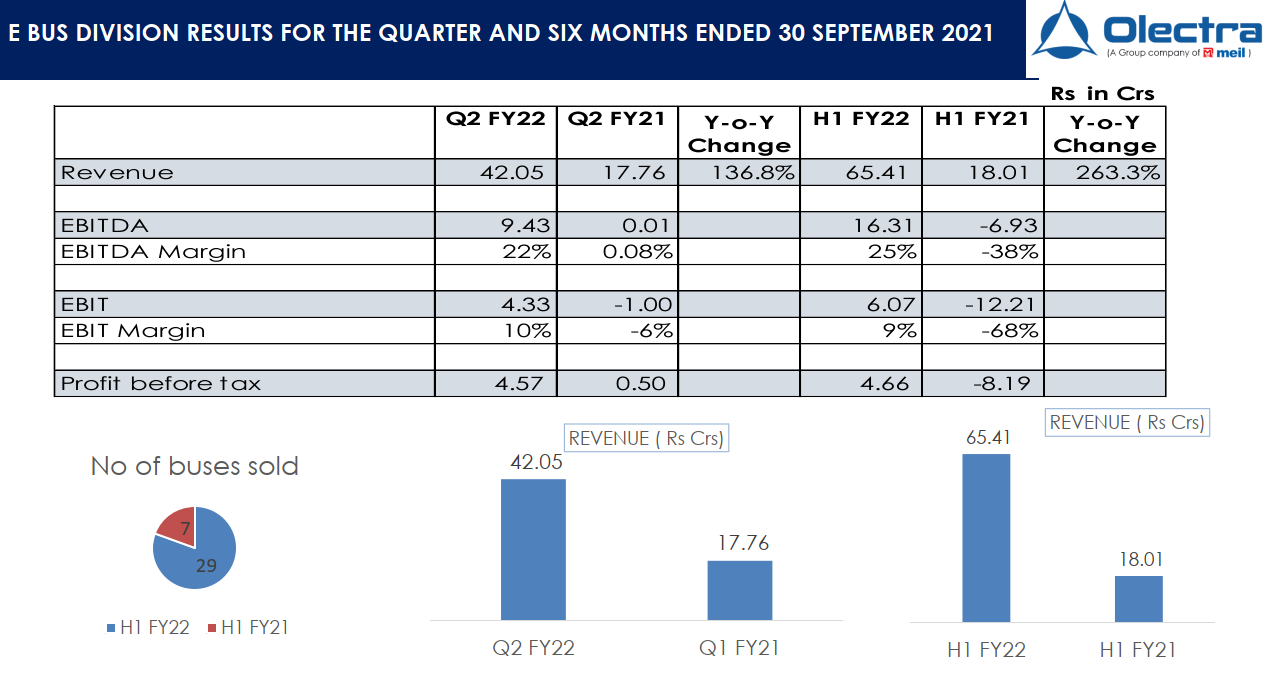

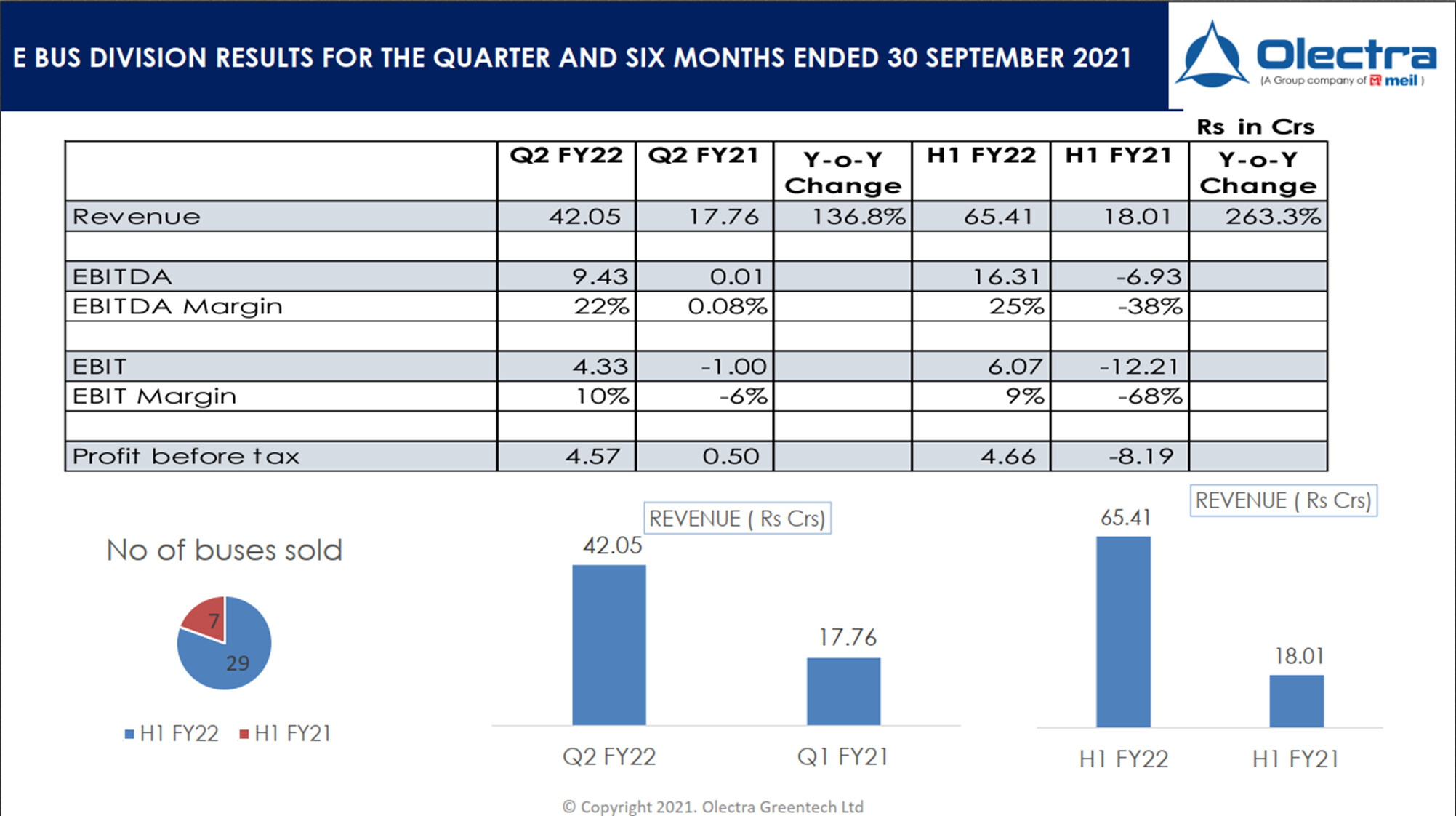

Based on my back of the envelope calculations – Olectra delivered 120 E-buses in Q3 FY22 so far

- Order Book on 08.11 – 1450

- Order Book on 09.11 – 1550

- Fresh Order on – 01.12 – 100

- Order Book on 01.12 – (1550+100) – 1650

- Order Book after deliveries made on – 01.12 – 1530

So, 120(1650-1530) E-buses have been delivered in Q3 FY22 so far. This itself generates revenue far greater than H1 FY22(29 buses) ~ 234 crores(1.95 Cr as average bus price)

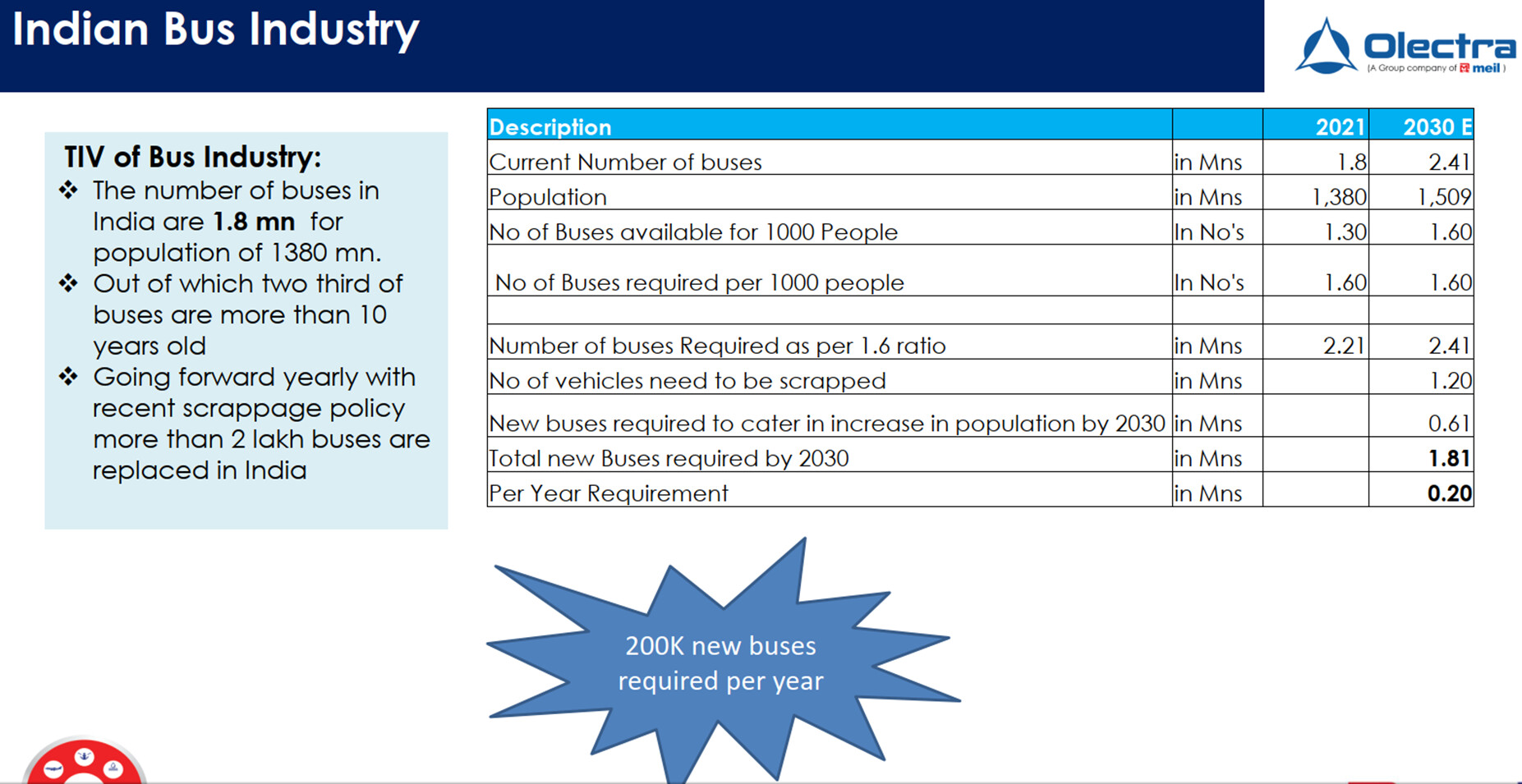

Olectra is a growing company and we are currently at the start of EV bus adoption. The below analysis shows the opportunity ahead.

Source – Company’s investor presentation dated 09.11.2021

Considering that Olectra is able to get 5% of 200,000 buses – it will translate to 10,000 buses per year. Let’s say, we consider the average price of Olectra bus as 1 crore, it will translate to 10,000 crores.

Olectra is currently having a market cap of ~7,000 crores. It will translate to Price/Sales of less than 1. The estimates provided do not include other adjacencies like Trucks, LCVs and 3-Wheelers etc

If the question is whether the company is really prepared for manufacture of 10,000 buses per year, I think yes. I have been hearing about this number from at least 2 years.

The recent land acquisition of 150 acres in Telangana substantiates the conviction that company is moving in the same direction.

Corporate Governance Scan

- Promoter cancelled 91,00,000 convertible Warrants on 10.04.2020 during peak of covid which were allotted on 10.10.2018. The subscription amount received at the time of allotment of warrants was forfeited

- The main reason is due to the fact that the share price was way below compared to the warrants price of 175 rupees per share

- However, they increased the stake in multiple tranches recently at around 400

- The previous promoter was not known for best corporate governance practices

- The new Promoter is now having more than 50% stake in Olectra and the earlier promoter sold most of their stake

- MEIL itself wants to list their company in next 1 or 2 years. After they taken over Olectra, there is a significant improvement in their disclosures and investor relations

- Olectra website is showing all kinds of transparency in disclosures.

- I believe, they will stick to their highest corporate governance standards at least till the IPO of their flagship company

Forensic Scan/Red Flags

- MD Salary ~2 Crores. PBT ~8.44 for H1 FY22. Annualizing it to 16.88 which means ~11%

- As it is a growing company with much growth expected in future, the salary doesn’t seem to be a red flag

- No Stock options offered to MD which means no “Skin in the game”

- Subsidiary Evey Trans was sold to parent company MEIL Holdings. The reason for this transfer is to ensure that the promoter will shell out the money to buy buses from Olectra and in the process, de-risk the financial liability

- There is a risk of related party amounts between the promoter entities. This will be majorly with Evey Trans which buys the buses from Olectra. Having a tab on Cashflow will help in identifying in any lapses of payment

Source – Company’s 2021 Annual Report

Resources –

- Annual Report - Annual Reports | olectra

- Quarterly Results - https://olectra.com/quarterly-reports/

- Investor Presentations - Stock Share Price | Get Quote | BSE

The opportunity is similar to how Jio disrupted telecom. There is neither past baggage nor debt and incumbents have debt and incumbents will also need to work on their existing services.

The other advantage is Olectra has the edge in technology in terms of electric bus among the existing competitors.

The promoter has the money muscle, best technology partner(BYD) and all he needs to do is hire/nurture best talent.

Can Olectra disrupt the bus industry like how its promoter MEIL did in infra? Only time will tell.

Looking forward to the views of other investors.

Disclosure(s) – Invested 6% of PF and biased. Actively tracking from 2018.