The competition in the electric bus industry is increasing all of a sudden. Tata Motors is a huge giant which has the capacity to win big tenders even at a loss to capture market share.

Also the huge Fame 2 subsidy which is almost Rs 50 to Rs 60 lakhs on a 2 crore bus (25% to 30% discount) is going to end around March 2024. There might be slower growth for the next 2 to 3 years, after which due to economies of scale and reduction in prices of lithium on batteries, there might be pickup in sales again from 2026 or 2027 onwards.

Also in cities especially like Delhi where Metro trains are growing at breakneck speed, I can already some slowdown in the number of buses deployed on various routes. In future, many more cities will be covered by metro trains, hence the demand of electric buses although robust will not be skyrocketing.

Most big electric bus tenders are very competitive and will offer maximum 5%-10% PAT margins for manufacturers due to high competition. Also under the per KM operation scheme, there is a risk of late payments from government owned STUs to the electric bus manufacturers.

Taking into consideration the above factors, I would be very cautious paying 100-200 PE price for any electric bus manufacturers like Olectra Greentech. Remember the promoters didn’t covert their warrants into shares at a price of just Rs 175 and forfeited the 25% prepaid price.

I might look at this company as an investment at a more realistic PE band of around 30-40 or even less.

Hi everyone, I must admit that I have been spectacularly wrong on Olectra Greentech. But my logical mind cannot understand these fundamental issues:-

How can a company which just made 500-600 buses in the previous year, start making more than 2,500 buses (5X) from this year as they have to provide 5,150 buses to Maharashtra State Road Transport Corporation (MSRTC) in 24 months.

This is just a Letter of Intent and not a Definitive Agreement. There is a huge difference between these two things. Also how can some company be awarded a Rs 10,000 crore order without any competitive bidding or tender. I didn’t find any big company losing this contract or Olectra being declared L1 in competition. This order might face some legal issues in near future.

Also if you see carefully the State undertaking will pay them over 12 years. Now whatever financial engineering is or is not being done by the company Olectra or its subsidiary Evey (I hope it’s a subsidiary and I might be wrong). The fact is that 10,000 crores will actually accrue to the company over 12 years which is around just 833 crores per year.

I have definitely missed this opportunity partially as I have exited the company in 2021 with a very handsome multibagger profit but far short of what I could have actually made. Good luck to all those investors who have made money in this company. But with a market cap of Rs 10,000 crore already as on 7 July 2023 and a PE of around 150, I think we should be a little careful in this stock. At a correct price (I think not possible now as it will have to correct by atleast a huge 60 to 70 percent), I might be tempted to buy this stock once again.

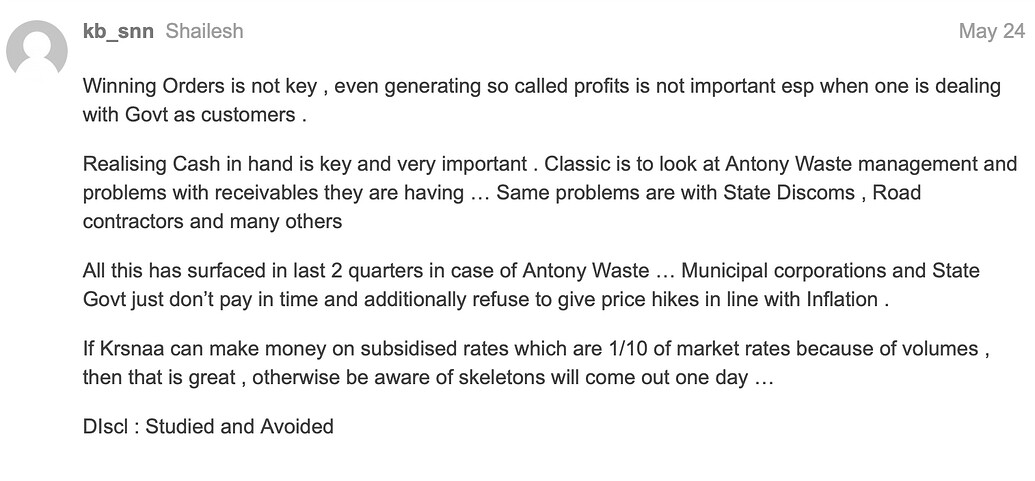

@kb_snn

Hope you don’t mind me sharing this image.

This comment screenshot was shared under Krsnaa’s forum.

We saw what happened today.

It is tricky dealing w govts and long term contracts increase the risk even more.

These are not private entities who you can fight on equal footing in the court of law. Its fighting the referee.

The Buses order is frought w risks. Risks that could be easy to forget in the recent run up.

Govt contract + for a decade if im not mistaken.

Chinese enterprise, which is also looking to grow its presence

TATAs and their connections

The Free Schemes being ran for winning elections impacting Budgets

Owning Cars as a status symbol

Building of hyper connected metros (you rarely need to use buses in cities like Delhi anymore).

there might be more, please be cautious.

On the other side of a table, I understood that Olectra has a contract with BYD for batteries until January 24, and it is interesting to see whether the company is able to renew the contract in battery technology with this impact in place. If this fails to renew, it would be a very bad sign. As BYD is superior in supplying batteries for EVs and the only lead player in supplying EV batteries with reliable technology, it would definitely be difficult to find a partner with similar technical capabilities. As far as EVs are concerned, batteries play a key role, and we need to carefully watch and observe this development.

I will try to answer few things as per my understanding about the company.

They have started construction activities of a new facility with a capacity of 5000 buses/ years on single shift basis, this will be ready in this month. This facility can help them to clear the backlogs.

Regarding 12 years contracts, they are selling buses to the operator not ST’s, operator will clear the due amounts to olectra (As per some concall discussions ) as per the payment cycle. This 12years staggered payment may not be applicable to olectra.

Now in 1 more tender (BEST) they are L1 (told by management in previous call) and price negotiations are underway. Order book will be 11000 buses now.

Order book can grow from here onwards due to PM e-Sewa EV bus tenders, 3600 buses tender is already floated and about to close in the Jan’24.

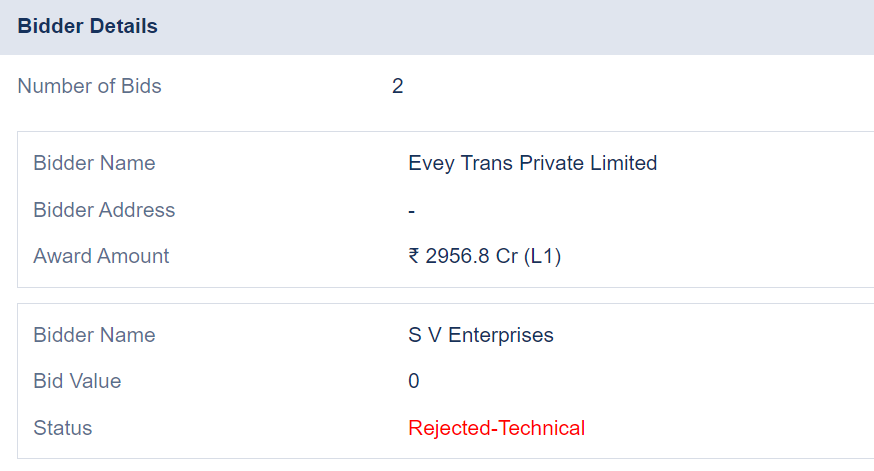

The tender floated by BEST for 2400 ebuses had ONLY 2 participants, out of which the second participant didn’t even name the bus they will provide. Ultimately the second participant was rejected on technical grounds. Makes me wonder why wouldn’t companies like Switch, JBM, Tata didn’t even participate.

Disc- invested

Could you please share the source link. I would like to track upcoming tenders as well.

Management already told about this L1 in the last conference call, it’s almost 3000 buses after considering the +ve tolerances.

Recent media interaction they have confirmed that they are L1 in some other 500 buses tender.

I am concerned about the execution of these orders, Earlier they had a target of 1200 buses later its come down to 1000 buses and now they said 700-800 buses will be delivered in FY24.

Source is bidassist, it is a paid service I use for my business.

BEST cancelled an order of 700 ebuses in 2023 when the bidding company was not able to fulfil the order on time. Will dig deeper and get back on the timelines of this tender.

i) 25% of the buses should be delivered within 4 months of date of issue of LOA,

ii) Additional 50% of the buses should be delivered within 7 months of date of

issue of LOA

iii) Balance 25% buses should be delivered within 10 months of date of issue of

LOA.

The LOA will specify the depot where the Buses are to be delivered and the same

shall be subject to inspection & acceptance of BEST.

Once LOA is issued,

600 buses should be delivered within 4 months

1200 buses should be delivered within 7 months

600 remaining buses should be delivered within 10 months.

Olectra Greentech is trading at a P/E of 177 times at a market capitalization of INR 13,902 CRORE as at 29 January 2024. At this price point, if you’re entering the stock – it’s hard to see any major upside unless the company can expand earnings substantially over the next few years. Can it do that?

I’ve written a detailed blog on ^. I cannot include the link to that blog here, in case you’re interested, check out the link in my profile bio or DM me for the link.

Here’s my summary on the brief reading of the Q2FY24 investor con call:

Pros

Won order of 5,150 buses from MSRTC – which is the largest single order in the EV bus category in India. At the L1 stage for its order from BEST for 3K e-buses. Anticipating a tender of 10K e-buses from PM e-Seva, although how much share Olectra could get out of this 10K is unknown at this point.

Expecting good order inflows for e-tippers in the next 6-12 months. But, no major order book for e-tippers at this point. Would need to watch out next few quarters to see if there’s any development here.

Execution of the above order book as follows – (i) 2500-3000 e-buses in FY25 (ii) 4000-5000 buses in FY26.

To achieve these volumes, company is expanding capacity. New factory being set up which should be able to commence production from Q4 with output of 3.5K units per year.

Insulator segment is a [relatively] high margins segment. Olectra has market share of 45-50% with market size of 350-400 crore. Expecting revenue of INR 150-160 crore in FY24 from insulator segment.

Invested in 50+ R&D personnel to bring in new designs + new models

Cons

Delivered only approx. 240 e-buses in H1FY24. Targeting to deliver 1000 e-buses in FY24 due to disruption in production of 3-4 months. It has to complete certain testing / obtain certifications to comply with new battery norms. R&D costs have gone up due to extensive testing of products.

Guidance initially was given to deliver 1200-1500 e-buses in FY24. Guidance has been lowered to 1,000 buses now. Gross margins decreased in Q2 due to change in product mix.

Not going for equity fundraise but a debt fundraise to fund the capex expansion plans. 70% of requirement will be met with debt options and the rest through internal accruals.

Some general points

Management expects partnership with BYD to continue beyond 2025. Olectra has been slowly acquiring technology + knowledge transfer from BYD. Sources battery cells + certain child parts for the power train from BYD which constitute around 25-40% of total components procured. The rest are sourced from local vendors.

Hydrogen bus (partnership with reliance) is still in progress. Will take another year to get clarity on the potential of this project. Very early days.

The management doesn’t have any plan to enter into 3 wheelers / passenger vehicle segment in the foreseeable future. Obviously, since they don’t have capacity to fulfil existing demand at this point.

EBITDA margins on sale of e-tipper would be around 10-12%

Concluding thoughts: Olectra is a good business. Good potential. Robust order book. However, valuation plays a very critical role when investing in a company & unless Olectra can grow their profits 2X every year from here – the valuations look lofty with little margin of safety at this point.

Disclosure: Invested, looking to add if there is a good correction in the stock.

In the August 10th, 2023 Conference Call the management guided for 1200-1500 e-buses & e-tippers for FY23-24. The management then reduced that guidance to 1000 in the November 7th, 2023 Conference Call. The management again reduced the guidance to 700 in the February 1st, 2024 Conference Call

The management is guiding for 5000+ e-buses & e-tippers in FY25-26 and is currently struggling to reach 1000 in FY23-24. I have my doubts about the management’s ability to scale up so quickly for FY25-26.

Even with the 8088 e-bus order book on hand, I am not able to understand the management’s reluctance to work in multiple shifts instead of the current one-shift structure of production.

My second biggest concern stems from their strong technology partnership with BYD (a Chinese Company). The partnership started in 2015 and as per the management, it is likely to go beyond 2025. Olectra Greentech Ltd. is dependent on BYD for the battery cells and some of the child parts relating to the powertrain. Apart from this, all the other components, are sourced locally in India. As per the management, 25-40% of e-bus components come from BYD. This heavy dependency on a Chinese company is concerning. Considering the current geo-political tensions between India and China, it is very likely that the government of India would not view relations with a Chinese company favorably.

With 163 PE , stock price run up 3 times in last one year and connection with Megha Engineering (Electoral bond case), only time will tell how the stock price would react as election campaigning starts getting heated. Can become major campaign issue thereby pulling down company’s fortunes. Just trying to become devils advocate here

JBM won 1390 bus orders in the first tender of PM E-sewa (3600 buses), there is no update from the Olectra regarding this tender. any body know who won the balance bus orders?

CESL released another tender for another 3132 buses in PM E-Sewa program.

Only JBM is leading in bus category.

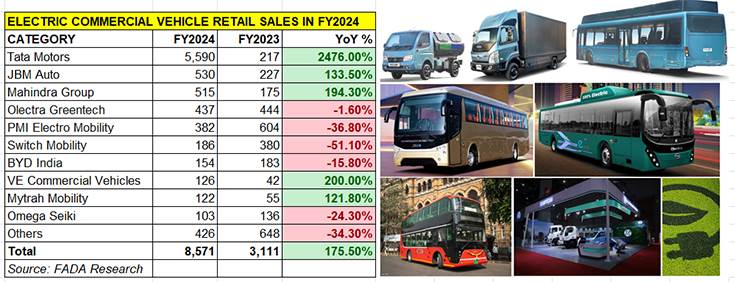

Interestingly PMI numbers also down by 37%.

I hope this year Olectra numbers will be good as 1st phase of expansion is about to complete and 2nd phase will also get completed in the Q2FY25