There are some notions people have about CDMO businesses. Let me list them all and then we will explore each of them into the mechanics of what causes it and if they are actual universal truths.

- CDMO business is lumpy

- Innovator sticks to CDMO partner from trial phase for production after FDA approval

- $1b drug for Innovator would translate to big earnings for API/Intermediate maker

- High value APIs (say 12 lakhs/kg) would mean big margins

- Frequency of oftake (lumpiness) doesn’t matter as long as you compare YoY and see growth in sales

- A company with 20 drugs is better than a company with 5 drugs

It is important to understand the mechanics of all these because now there are several interesting opportunities for Indian CDMOs - from Nubeqa (Ami), Elinzanetant (Aarti), Cobenfy (Neuland), Bempedoic Acid (BlueJet/Neuland) and so on. All these may go on to do well in end markets and become blockbuster drugs - but are all these same from the perspective of an API/Intermediate maker? Its not an easy question to answer but lets try to.

Although lot of stuff in this post are general, am writing in this thread because lot of the learnings in this post come from analysing Austedo for which Neuland has been supplying since trial phase (2017 FDA approved)

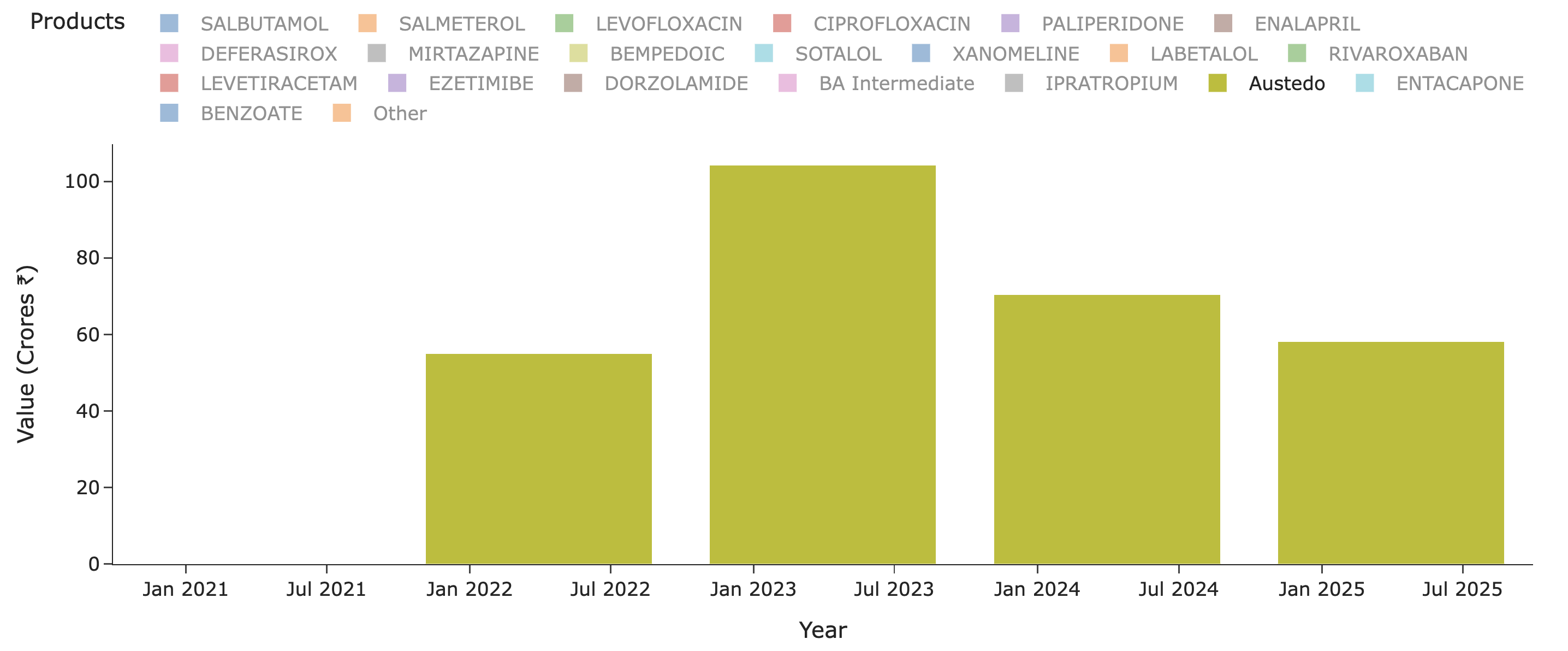

I have really been stuck on the anamoly that is Austedo. People who remember the fanfare this molecule had in '20 on Twitter know why its important. People used to celebrate its sales and assumed it would flow down to Neuland but it never did (Highly recommend reading all posts from this point until about Mar '22 for context). Austedo sales today is $1.6b. It crossed $1b 2 yrs back or so.

Lets see what Neuland exports of the molecule in recent years look like - for Austedo in specific. Peak sales for Neuland was a mere ~100 Cr for a $1b drug. Thats just ~1% or less on most years. Why is this? Why didn’t we see 5-10% of sales of value of drug and thus reaching 1000-1200 Cr levels? (In recent times, Bempedoic Acid sales is probably ~10% of sales for eg. - why didn’t Austedo ever even cross 1% of Austedo sales by value in any year?)

The reason for this as per my hypothesis was that all drugs are not created the same. To understand this discrepancy, one has to understand nature of drug - is it mass-market (statins, glp-1, alzheimer’s) / lifestyle elective medications (erectile dysfunction stuff, wegovy) > chronic niche (RA, parkinsons, schizophrenia, opiods etc.) > acute mass-market (broad-spectrum antibiotics, NSAIDs, painkillers) > acute high-cost (resistant infections, cancer, stroke drugs) > orphan drugs (metabolic disorders, cystic fibrosis).

It requires us to understand dosage - how many milligrams of drug is given per day and for how many days? How is it titrated up and down? (low dose to high dose and vice versa). How is the prescription uptake for the drug? How is the insurance coverage? What’s the drug’s stoichiometry and actual yields like i.e What proportion of raw materials are needed to make the drug theoretically and what are the actual yields in production. Without understand the nuts and bolts of all these, we will be given to platitudes like xyz is supplying solely to blockbuster drug.

So what went wrong in Austedo? Austedo is a drug for Huntington’s chorea and Tardive dyskinesia - these aren’t big market but are very, very high value and niche. It costs almost $60k-90k per patient per year. That also implies the market for this isn’t going to be very large (~30-50k active patients as per quarterly prescriptions above). The patients starts taking 12mg/day and is titrated up at 6mg every week until a max of 48mg/day. So on avg. each patient likely takes around 24-30mg/day of the drug.

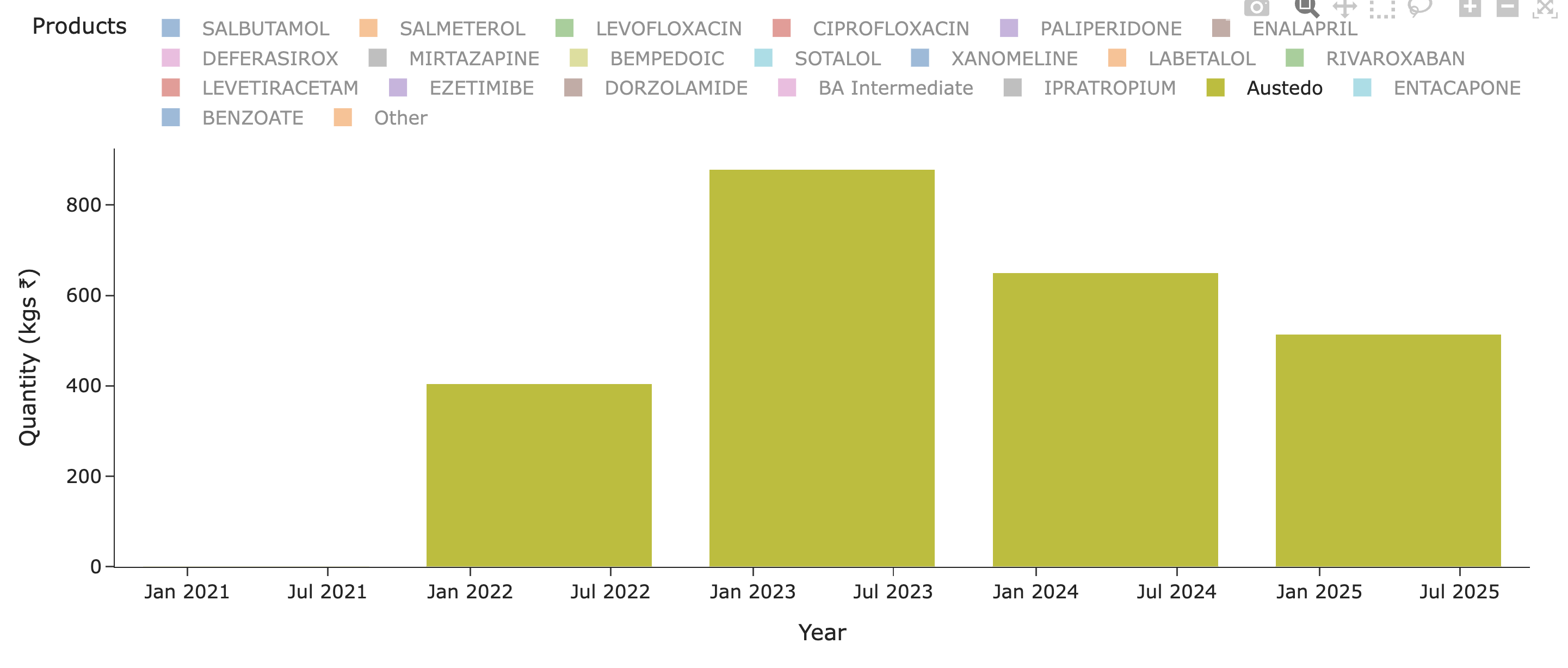

What does that translate to, in terms of per year consumption per patients? 30mgx365 = ~10gms/yr/patient. So a 1 MTPA capacity should cater to 1000000/10 = 100k patients (If you remember in BlueJet’s intermediate’s case, 1MTPA capacity could only cater to 7500 patients for context - that’s a pretty wide variation we need to pay attention to - and thats because 180mg/day of drug in BA’s case and intermediate to BA API conversion yields being poor. Even BA API 1 MTPA would translate only to 15k patients - unlike the 100k we see in Austedo’s case). So considering Austedo has only now reached ~40-50k patients in US (100k quarterly TRx), we should see much less than 1 MTPA in exports for Neuland.

The quantity of exports supports this hypothesis. At peak it was 0.8 MTPA and since then lower - so overall uptake of drug is limited by dosage, prescriptions and margins by stoichiometry and yields.

It should be pretty clear by now that a mass market drug, at higher dosage and dosing frequency should do very well and way better than all other categories because of higher MTPA requirement and that means physical constraints would force multiple batches or a continuous process throughout the year (always higher margins from operating leverage) and consequently an uptake that’s not very lumpy (supply-chain stocking level lumpy will always be there).

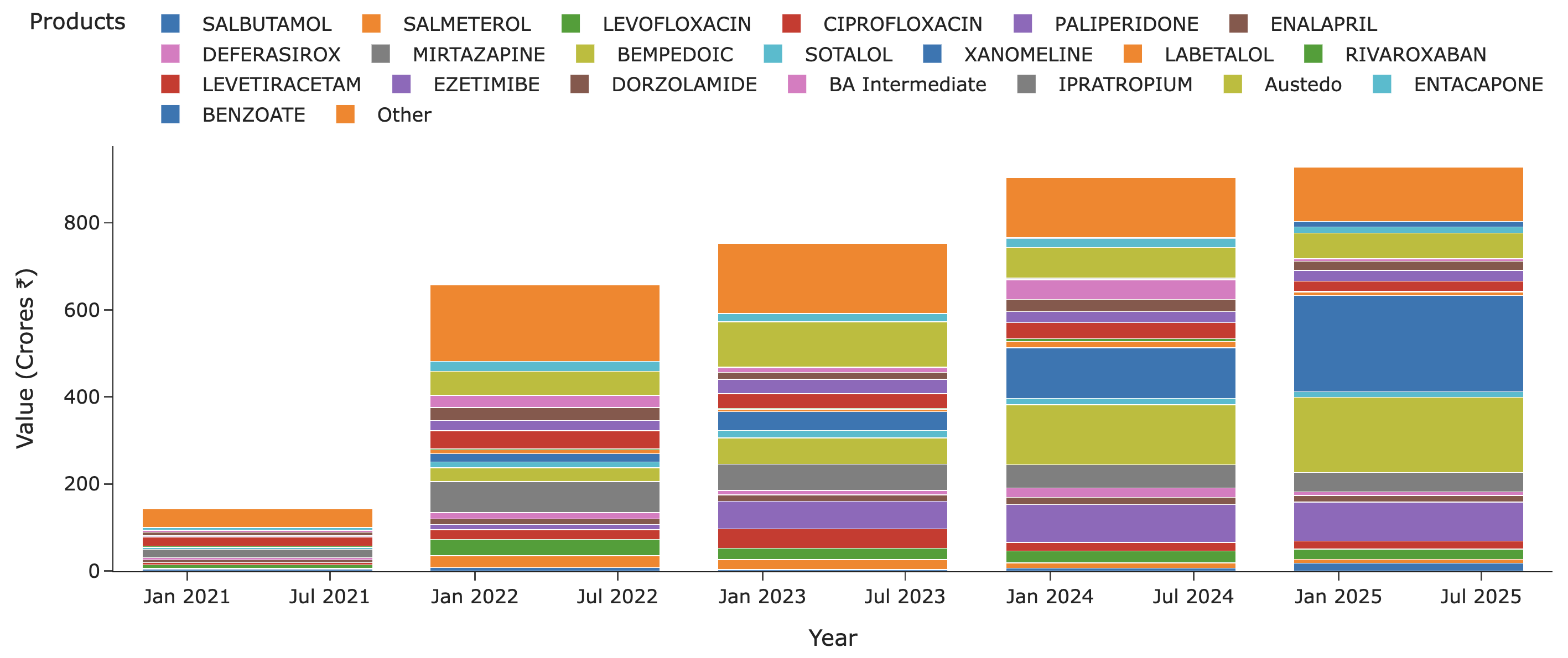

A look at overall Neuland molecules also sheds further light. There are over 20 molecules in exports but of these, only Austedo, Cobenfy and Bempedoic Acid are NCEs of value. There’s a crowd of generics here from across the spectrum.

And a lot of these generics are degrowing as well (for that matter, even Austedo has degrown as we saw above) - like Mirtazapine and Levetiracetam. You put all these in context and we can see why Neuland’s margins have been under pressure. This is why I feel a company with fewer molecules but molecules with moat - either because they are patented or because of unbeatable high volume/low-cost production or because of limtied suppliers (technical limitation or contracts) will always have higher NFAT and Margins (As we see in BlueJet’s case all these at 5x NFAT and 40% margins!). I would even go to the extent of saying a company with 20 molecules where bulk of them are generic isn’t less risky than one with 5 molecules but with serious moats.

So going back to our initial notions, most of them aren’t universal truths. Lumpiness comes from trial batches and also from post-approval production supply if its to a limited market (which most drugs are but a high dose mass market drug can be non-lumpy). An innovator doesn’t always stick to the CDMO that did trial batches and often establishes secondary and tertiary supplies for high volume drugs (As has happened in BlueJet’s case even though Esperion was engaged with Neuland).

A $1b drug doesn’t have to necessarily make a lot of money for API/Intermediate guys and might be limited to 80-100 Cr/yr if its limited batches. A high value doesn’t translate to high margins - I am yet to work out what margins Austedo would have made for Neuland - it could be high but since sales itself is low, that’s the reason Neuland didn’t make money from Austedo (and not necessarily due to margins as I initially suspected). But in case of BA, there’s a clear case of high value not meaning high value add (2kg of Intermediate is $900/kg and 1kg of API is $950/kg in BA’s case is a case in point at least for this).

Frequency of uptake matters a lot since running small batches few times a year possesses zero operating leverage. Continuous operations or high frequency of batches over several months can give a big fillip to margins from operating leverage. Lot of molecules in phase 3 in a company’s roster doesn’t mean we should automatically get excited before guaging the market size in terms of patients and prescriptions, the competetion, the insurance coverage (post launch), doctor’s opinion on the drug’s standing (some will be reluctant to prescribe for various reasons), volume and frequency of uptake, possible margins, primary/secondary supplier etc.

Disc: Interested in Neuland. Invested in BlueJet as disclosed earlier and no recent transactions. I have been studying the CDMO space in some depth over last 2 months across companies and these posts are my attempts at understanding the nuts and bolts of a sector I am new to. I am not professionally qualified in this field and by no means an expert - so I am bound to have made lot of mistakes.