Neuland Laboratories Ltd a 30 year old pharma company is a predominantly API manufacturer (85% ) with some presence in CRAMS (15%) derives 73% of its revenues from US, Europe & Japan.

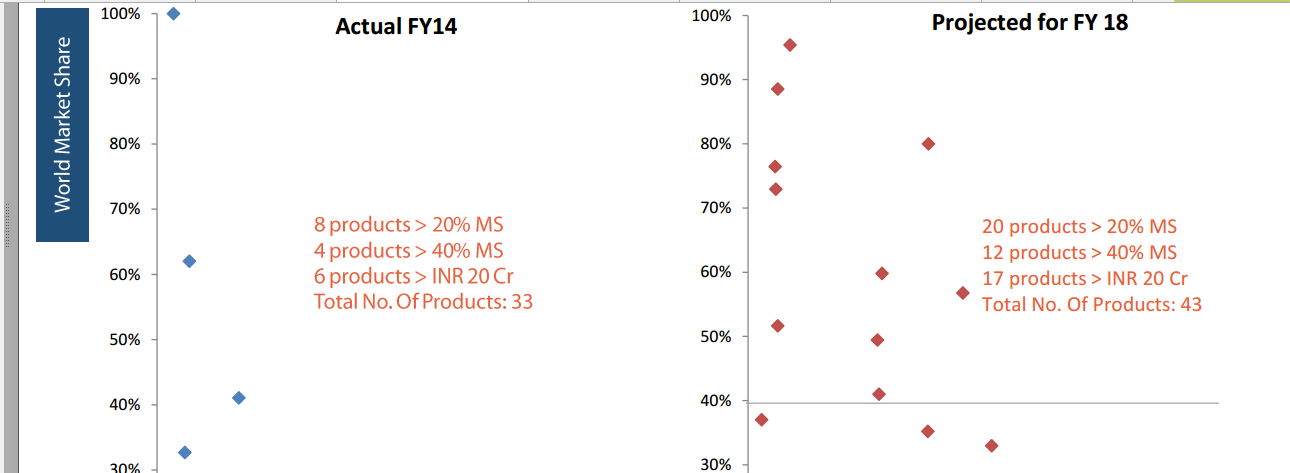

Neuland claims to have to transformed itself from manufacturing commodity APIs towards having capability to develop complex molecules in niche segments – Opthalmic, Schizophrenia, anti-asthma, anti-fungal. → This is verifiable easily. We will see in the subsequent sections.

Their top five products contribute to ~4% of the topline while top 5 customers contribute ~40% of the topline.

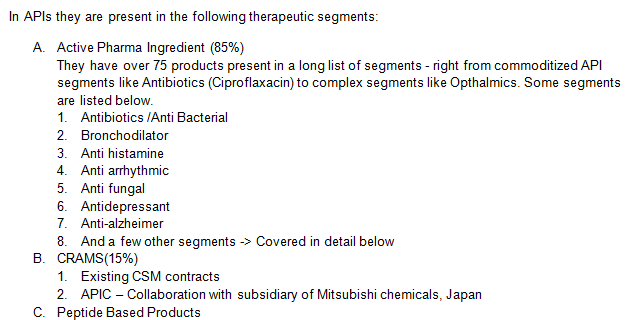

Active Pharma Ingredient (85%)

In API manufacturing, the competitiveness of a manufacturing company is determined by one of the following ways:

- Build massive scale, cost advantage in commoditized APIs – A new competitor won’t be able match you (or)

- Identify niche APIs which has complex chemistry so that competitors will find it difficult to imitate. → How to verify this? Look at the molecule, find out the # of DMF filers for that molecule(may give a hint).

Neuland claims(or HAS IT?) to have graduated from #1 (above) towards building capabilities in developing niche complex APIs in segments like Opthalmics, Anti-asthma & Bronchodilator segments.

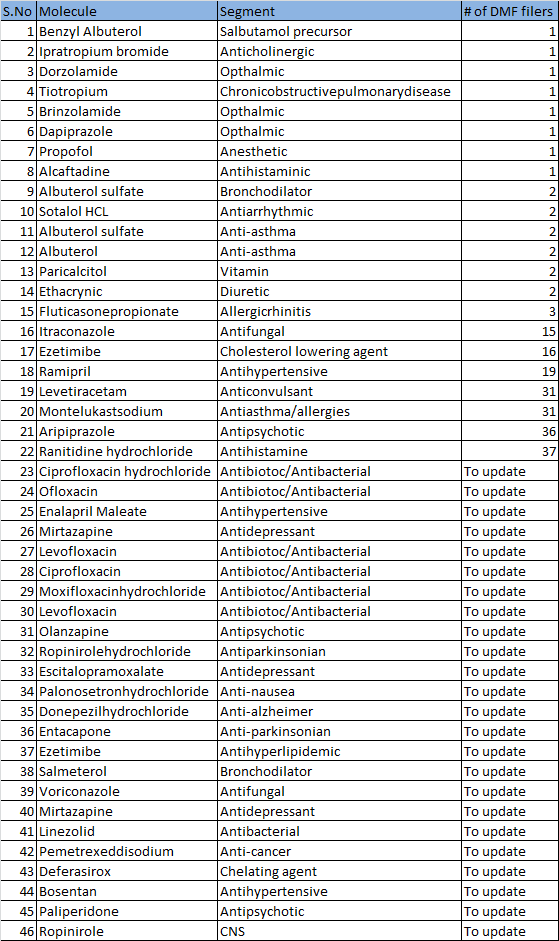

Here is the current list of Products from Neuland’s with the # of DMF filers:

To update - I am working on identifying the # of competitors for these molecules. Will update after I complete. All these molecules have more than 1 competitor.

Some observations:

-

In about 15 molecules, Neuland is either the only player/ has only one another competitor. - This is quite significant because the generic company will have limited options when it looks at identifying a DMF partner. Lesser the available options, bargaining power of the API company increases.

-

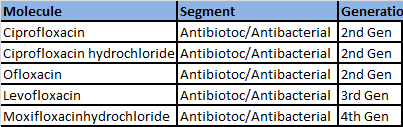

In antibiotics:

a. Higher the generation the molecule is present in, higher the margin for the company. The company’s presence in 3rd and 4th Gen molecules indicates R&D capability of the company.(check the table below)

b. In Antibiotics, Ciproflaxacin is a commoditized API. Neuland is moving away from this molecule. A few years back, 65% of their revenues were from this molecule vs 15% of their revenues from Ciproflaxacin now ->Aarti Drugs is the global leader here.

3.For commoditized APIs, Neuland’s claims to play the volume game. – this contradicts in case of Ciproflaxacin – Aarti has taken away significant market share in the last 3 years from Neuland.

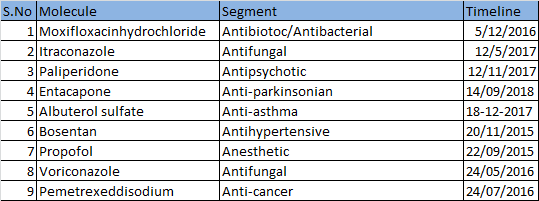

4.Visibility of earnings : About 10-11 APIs for which DMFs have been filed, are expected to go off-patent in the next 3 years. Timeline column indicates the expiry date for the patented version of the molecule in US market.

CRAMS:

Contract Manufacturing involves manufacturing APIs based on custom specifications of the customer.

- Their Contract Manufacturing segment has grown at a CAGR of ~70% in the last three years.

- They have non-exclusive agreement to manufacture custom products with leading Europe & US customers.

- Recently a large US customer has filed an NDA for the US market which is said to throw up an interesting opportunity – have to verify this claim

Pact with Mitsubishi Chemicals:

Neuland has entered into a pact with API Corporation (subsidiary of Mitsubishi chemicals ) to manufacture custom products for APIC.

APIC has invested 15 crores in their existing Pashamylaram facility to create the manufacturing infrastructure.

Neuland gets reimbursement of the operating expenses incurred at this facility – Don’t understand the revenue model here. Need to research more.

Neuland has developed some expertise on Peptide based products which are considered very complex in chemistry field.

Questions/Summary:

The company definitely looks decent because of the following reasons:

a. it looks like it is trading at 12 PE based on FY17 earnings

b. # of molecules where they have limited competition.

c. Added Revenue visibility from APIC contract with Mitsubishi

But the following questions are key before one considers investment here. The management seems very transparent as they have disclosed most of what is required in every concall.

- Imitability: The above pipeline of molecules going off-patent in the next few years looks interesting. But how difficult is it for a new API manufacturer to develop these molecules?

-

Debt: API manufacturing companies go down when they take the path of debt – Wanbury (global leader in Metformin), Parabolic(Cephalosporin), Indswift labs all failed because of financial distress and not because of lack of demand for their products.

As of now their D/E ratio at ~1 looks decent for an API manufacturing company especially considering the future growth possibilities. What is their approach towards debt? - What is their revenue model with API Corporation?

I wanted to look at some pharma names outside our comfort zone - i.e. Torrent, Shilpa, Ajanta etc. That’s when I zeroed in on Neuland after researching other API manufacturers like Aarti, SMS, etc.

I am still researching on this idea. Will update this thread as and when I find out more.

Thanks,

Ravi S

Disclosure: I have no positions in Neuland as of today. I may initiate a position in the next few days in this company based on further analysis.