Adding to Bharani’s masterclass on CDMOs:

I had a certain understanding of CDMO businesses:

- Treadmill business if you are very early in the CDMO journey. You have to keep finding new molecules frequently as supply to innovator is lumpy and your pipeline is small.

- Thumb rule – API will get 10% of the innovator sales. Intermediate will probably get 5% of the 10%. If you are doing end to end including formulation, you might get 12-15% including milestone payment. So, the innovator might make 85% gross margin.

- Valuation multiple for Innovator >>> CDMO

While Bharani has explained most of it using Neuland’s example, I felt Aarti Pharma is a live case study in the making.

Aarti Pharma has exported 2 intermediates for Bayer’s new drug Elinzanetant. Elinzanetant, formerly known as NT-814, is a dual neurokinin-1 and neurokinin-3 receptor antagonist under development for treating menopausal symptoms, particularly vasomotor symptoms such as hot flashes.

Note – Aarti Pharma mgmt. has not mentioned about this anywhere. It is my understanding that the 2 intermediates they exported in Q4 FY25 could be for Bayer’s drug. I could be wrong.

Bayer is a global leader in women’s healthcare. It acquired British biotech Kandy Therapeutics Ltd which developed NT-814. KaNDy was spun out of NeRRe Therapeutics, a GlaxoSmithKline spinout, in 2017. NeRRe filed the original patent for NT-814 / Elinzanetant:

Under the terms of the agreement, Bayer will pay an upfront consideration of USD 425 million, potential milestone payments of up to USD 450 million (for Phase-3 and regulatory expenses) until launch followed by potential additional triple digit million sales milestone payments.

The Phase III clinical trial is over and US FDA action date is July 2025. Once approved, the compound could generate peak sales potential of more than $1 billion globally.

https://www.bayer.com/en/ca/news/canada-bayer-to-acquire-uk-based-biotech-kandy-therapeutics-ltd

Note (for Wockhardt investors) – 425 Mn for a Phase-2 drug with a peak sales potential of >$1 Bn!

(Elinzanetant’s competitor drug Veozah was acquired for $588 Mn - https://www.fiercebiotech.com/biotech/bayer-inks-425m-upfront-kandy-buyout-to-challenge-astellas-for-menopause-market)

To understand the molecule, you have to read the patent fully. Or upload it to ChatGPT and ask the right prompts.

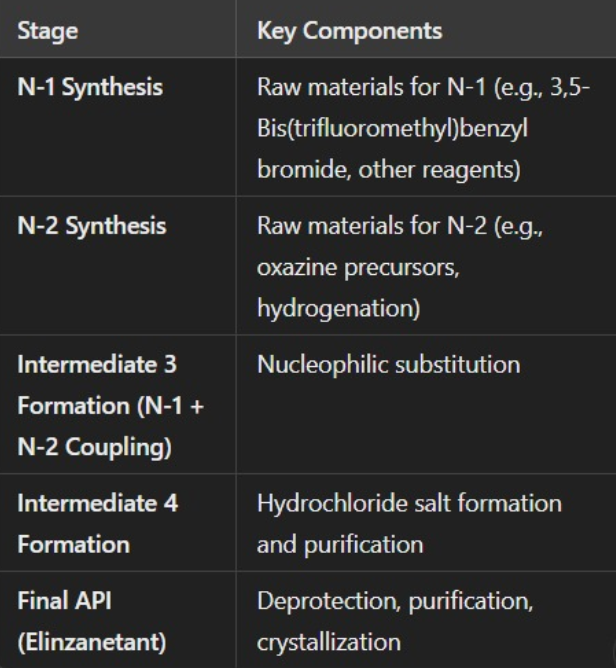

To put it in simple terms, there are 2 key intermediates to make Elinzanetant. Lets call them N-1 and N-2. The N-1 and N-2 intermediates are coupled together to form the API.

To calculate how much quantity of N-1 and N-2 are needed for 1 KG of API, we have to understand the Reaction Stoichiometry. The Elinzanetant synthesis follows a 1:1 coupling ratio. Each mole of N-1 reacts with 1 mole of N-2 to form 1 mole of Elinzanetant.

Given the molecular weights:

- N-1: 532.89 g/mol

- N-2: 262.35 g/mol

- Elinzanetant: 668.65 g/mol

In an ideal scenario with 100% yield, the mass balance would be straightforward:

- Combined Mass of N-1 + N-2: 795.24 g

- Mass of Product (Elinzanetant API): 668.65 g

This indicates that, theoretically, 668.65 g of Elinzanetant can be produced from 795.24 g of combined intermediates. The difference accounts for the loss of by-products such as water or other small molecules during the reaction.

However, actual industrial processes rarely achieve 100% yield due to side reactions, incomplete conversions, and losses during purification. Assuming an 85% overall yield, the expected recovery would be:

- Actual Yield**:** 668.65 g × 0.85 = 568.35 g of Elinzanetant.

Based on export data, Aarti Pharma has sent:

- N-1: 2,371 kg

- N-2: 2,142 kg

First, determine the limiting reagent by comparing the molar amounts:

- Moles of N-1**:** 2,371,000 g / 532.89 g/mol ≈ 4,451.6 mol

- Moles of N-2**:** 2,142,000 g / 262.35 g/mol ≈ 8,165.2 mol

Since N-1 has fewer moles, it is the limiting reagent. The theoretical amount of Elinzanetant produced is based on the moles of N-1:

- Mass of Elinzanetant API**:** 4,451.6 mol × 668.65 g/mol ≈ 2,976,000 g or 2,976 kg

Considering an 85% yield:

- Actual Mass of Elinzanetant API**:** 2,976 kg × 0.85 ≈ 2,529.6 kg

Therefore, approximately 2,529.6 kg of Elinzanetant API can be produced from 2,371 kg of N-1 and 2,142 kg of N-2. Yield = 2530/4513 = 56%.

Note – These estimates are based on online references and can be completely wrong as real world is very different and we are working with lot of assumptions.

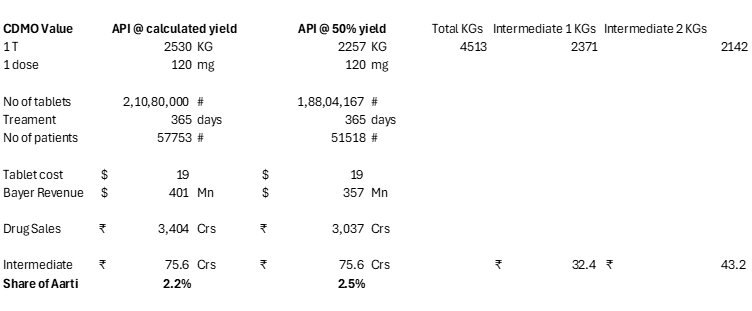

So how many tablets can be made from 2530 KGs of API?

One dose is 120 mg based on clinical trials done by Bayer.

2350 KGs / 120 mg = 21 Mn tablets.

Elinzanetant’s competitor drug Veozah sells at roughly ~19$ per tablet. It is the list price that a patient without prescription insurance pays:

So Bayer’s sales from this drug will be = 21 Mn * 19$ = $400 Mn or 3400 Crs.

Aarti’s 2 intermediates were sold for 75 Crs.

So Aarti gets only 2.2% of the end drug sales.

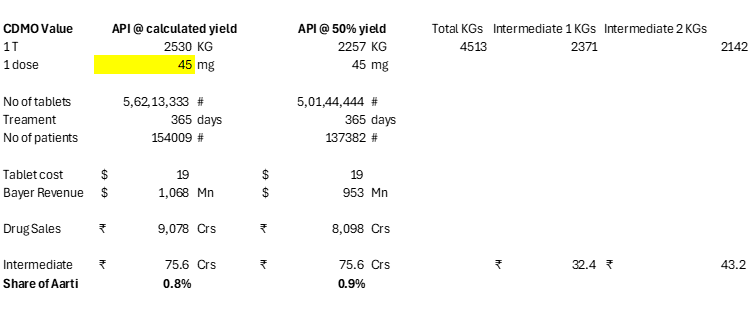

As Bharani indicated, the dosage is one of the important drivers for the CDMO company’s value from the drug.

If I reduce the dosage from 120mg to 45mg which is Veozah’s prescribed dose, Aarti’s value falls to <1% as now Bayer will have to sell more tablets and hence more patients:

One positive for Aarti could be the yield. If the recovery of API during the final stage is lower than our assumption, Aarti’s value capture can be higher.

How many tablets does a patient take every day and for how long?

While the minimum period for Veozah is 3 months, the average can be upto 1 year. So a patient will need 365 tablets. 21 Mn tablets will be consumed by 58k patients.

Which means, Aarti might not supply more intermediates till Bayer sells to 58k patients. If you consider the consumption period to be lower than 365 days, say 250 days then Bayer has to sell to 84k patients. Because of this issue, it is better to track and benchmark absolute sales.

How has Astellas scaled with Veozah so far? Veozah was approved by US FDA in May 2023 and EU in Dec 2023.

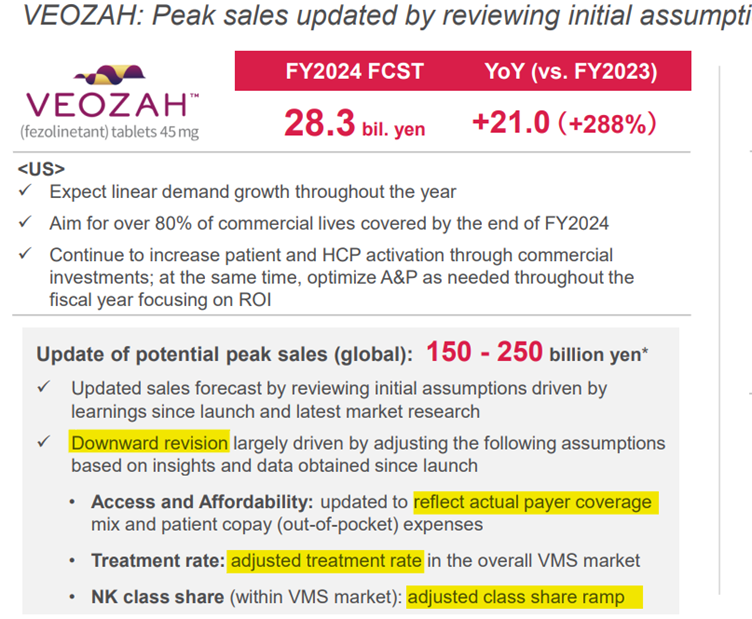

Veozah has reached a quarterly sale of $64 Mn in the 6th full quarter since launch! It was not a clear path to it.

When they launched, they had forecasted 49 Bn JPY or 325 Mn USD for FY23 but actual in FY23 was only 7.3 Bn JPY or 50 Mn USD!

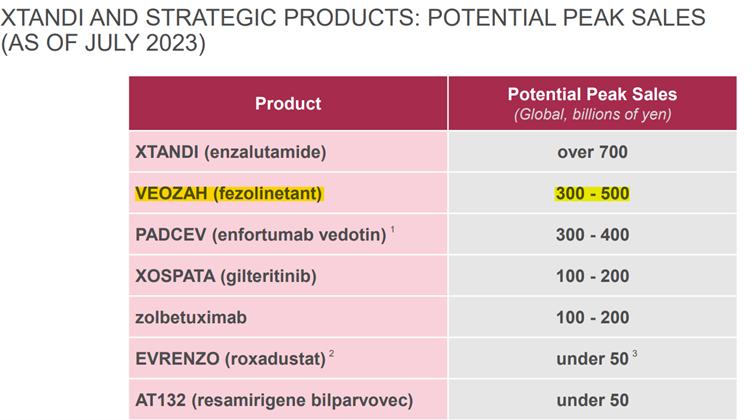

Initial projection of peak sales potential of 300-500 Bn JPY or 2-3.33 Bn USD! ![]()

But within few quarters, they had to revise it downwards to 150 – 250 Bn JPY or 1-1.66 Bn USD.

Reasons for downward revision:

- Insurance – payer coverage / out of pocket expenses – During launch, Veozah was eligible for only 15% commercial lives.

- Treatment rate

- Class share – within the treatment options, rank of drug.

Late last year, Veozah hit a small roadblock. In Sep 2024, US FDA issued a warning that Veozah can cause rare but serious liver injury. In Dec 2024, FDA added a Box Warning:

Coming back to calculating time taken by Bayer to utilize the intermediates sent by Aarti:

Astellas did 220 Mn in 6 quarters. Bayer being a global leader in women healthcare can do it in 3-4 quarters? But the API potential based on our assumptions is 400 Mn! If we assume Bayer to consume 400 Mn by 6th quarter from launch (Q2 FY26, our FY), then they don’t need more API till Q4 FY FY27. If Bayer buys intermediates 6 months before next batch of API needed, then Aarti will supply its 2nd batch only in Q1 or Q2 of FY27.

Best case for Aarti Pharma in my opinion assuming 1) insurance coverage increases significantly, 2) additional indication for breast cancer hot flashes, and 3) Veozah loses market share, Bayer will not need intermediates till Q4 FY26 at least.

Very good article on all issues regarding Veozah ramp up:

- Payer reluctance / stringent requirements (like it has to be prescribed by ob/gyn and patient has to try other non-hormonal treatments first) - https://healthy.kaiserpermanente.org/content/dam/kporg/final/documents/formularies/nw/kp-veozah-nw-en.pdf

- General awareness (menopause symptoms are not considered a disease)

- Patient and doctor acceptance (which is mostly side effects and insurance cover)

Hopefully, awareness and acceptance only increase from here on. And Bayer will have a second mover advantage from all the spending that Astellas has done so far (Example - https://www.youtube.com/watch?v=e-H2BF0GZik) in market creation. Bayer might also have a higher insurance coverage for its drug compared to Veozah during launch.

Summary:

- Treadmill business. Yes, Aarti Pharma even in the best case will not supply intermediates to Bayer till Q4 FY26 at least. Has this happened before? Yes, Yes, Aarti had supplied 4500 KGs of an intermediate for the drug Osimertinib in FY24. In FY25 so far, they have supplied only 2250 KGs. Similarly, intermediate for Afoxolaner supplied in FY24 was 23500 KGs but only 9900 KGs in FY25.

- Value for CDMO. Aarti Pharma might get 2-2.5% of the drug sales. So even if Bayer hits $1 Bn in Elinza, Aarti Pharma from the current 75 Crs will move to ~200 Crs supply. By when can it happen? Best case - Maybe 2-3 years from launch, so FY28 with the risk that in FY26 there can be no further supplies? Despite the lumpiness, potential of ~2.5x in 3-4 years is very good. Have to keep tracking the data.

- Initially, I was of the view that innovator will have only 85% gross margins. With the current understanding, it is possible that the innovator can have 95% gross margins too especially in acute therapies. 2% Intermediates, 2% API (can be higher too?!), 1% formulation = 5% COGS. So, the incremental 10% has to go to the innovator? What does it mean for an Indian innovator who is looking to out license the drug? In this Wockhardt post - Wockhardt: an NiCE story - #25 by Sanjay_Kumar_E – I had assumed only a 15% royalty for Wockhardt and 20% PAT margin for the buyer. Both can be significantly higher. Wockhardt can get 20% royalty and if they are lucky, 25% too. And Wockhardt’s royalty will be consistent because it is not linked to drug manufacturing but the actual sales.

Going through the patent and the manufacturing process also gives some indication of the capabilities that these CDMO companies have to make the intermediates or APIs.

In this case, ChatGPT says N-1 involves Fluorination (I don’t know if Aarti imports RM post fluorination or if it does it) and N-2 involves Cyclization & Hydrogenation. API process involves Nucleophilic substitution, Hydrochloride salt formation and Deprotection. I am not sure if the API has more value addition (ChatGPT says yes) than the 2 intermediates (was trying to see if this molecule is also similar to Bempedoic Acid where Bluejet which makes intermediates adds more value than Neuland which makes API) but more importantly @aga.ayush11 says that CDMO companies win certain molecules based on their chemistry and process capabilities.

Disclaimer:

I am a rookie analyst. I have been studying the CDMO space in some depth only over the last few months across companies. I am not professionally qualified in this field and by no means an expert - so I am bound to have made lot of mistakes. ChatGPT could be wrong too. This post is a case study to understand CDMO value chain with a live example.