Nagarjuna Construction Company (NCC)

Two-line summary: NCC Ltd is engaged in the infrastructure sector, primarily in the construction of industrial and commercial buildings, housing, roads, bridges and flyovers, water supply and environment projects, railways, mining, power transmission lines, irrigation and hydrothermal power projects, real estate development, etc 1.

Business Summary 2 (May 2020)

-

Scale: Second largest Listed construction company in terms of revenues in India.

-

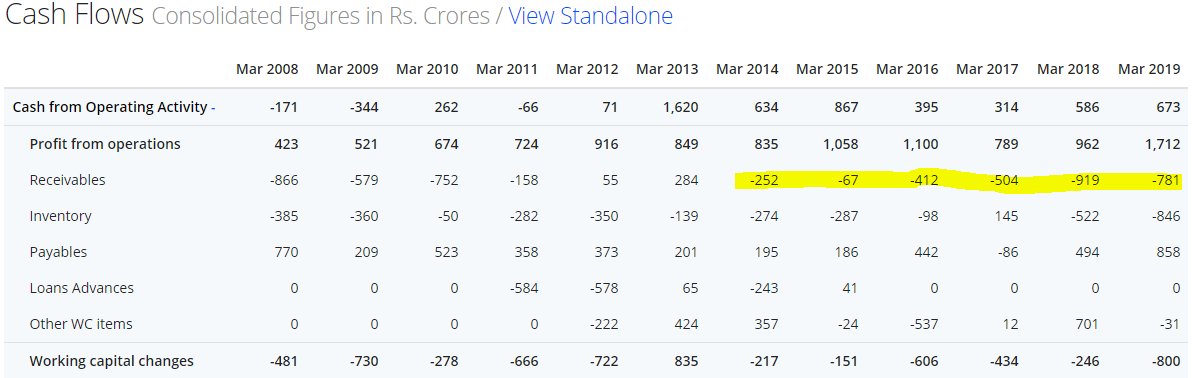

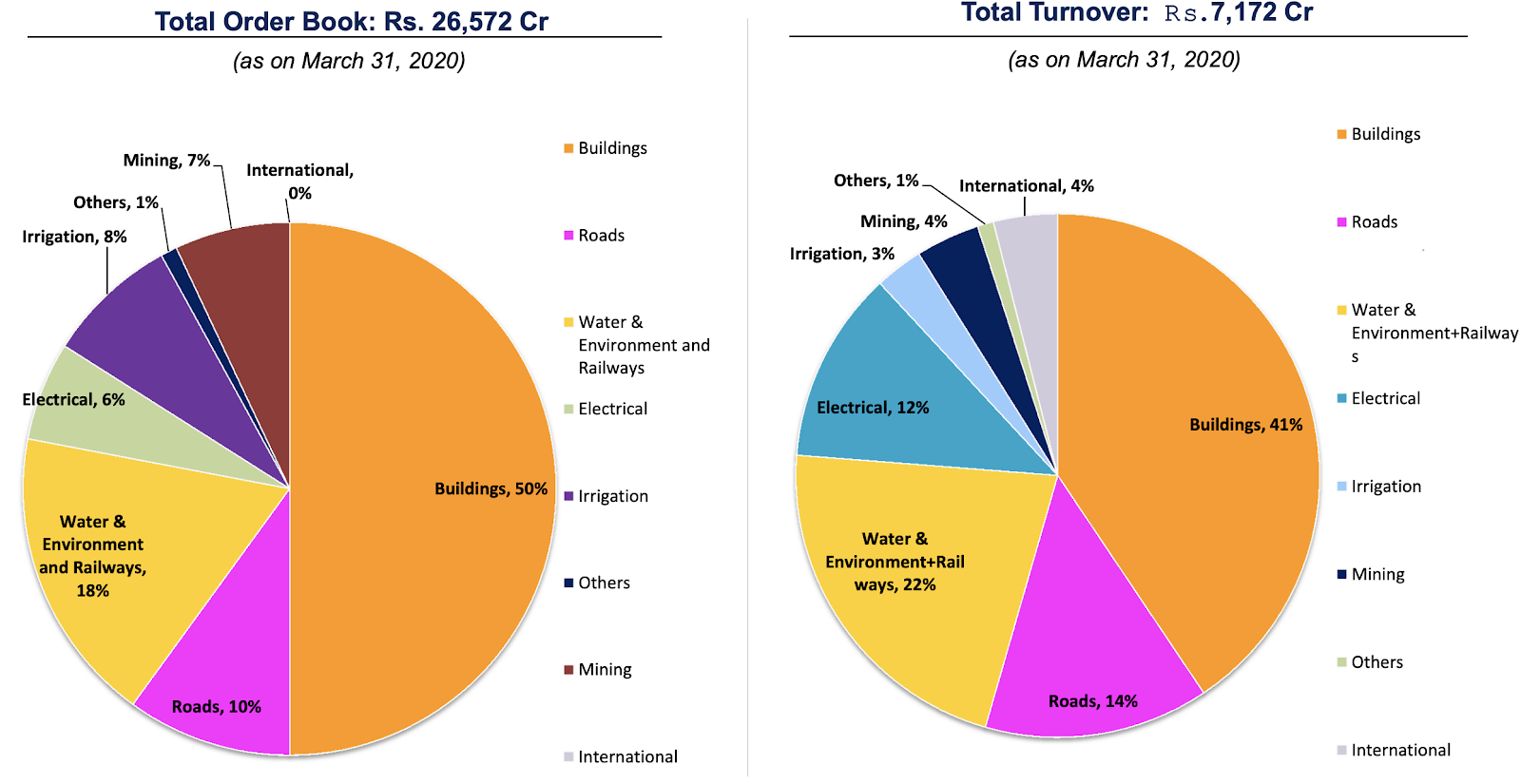

Order Book: 26,572 cr as on March 31, 2020. New orders of INR 7172 crs received up to March 31, 2020. Order book to sales ratio of 3x provides strong cash flow visibility for next 3 years

-

Geographically diversified: Key projects executed:

Agra Lucknow Expressways – Uttar Pradesh

ESI Hospital and Medical College, Gulbarga, Karnataka

Outer ring Road, Hyderabad Growth Corridor – Telangana

Infrastructure development, Ministry of Defence ‐ Arunachal Pradesh

Water Supply Project, Rajkot ‐ Gujarat

Nagpur Metro - Maharashtra

3 AIIMS - Himachal, Bihar, Punjab (page 18)

3 Airports

BESCOM, KENGERI Bangalore -

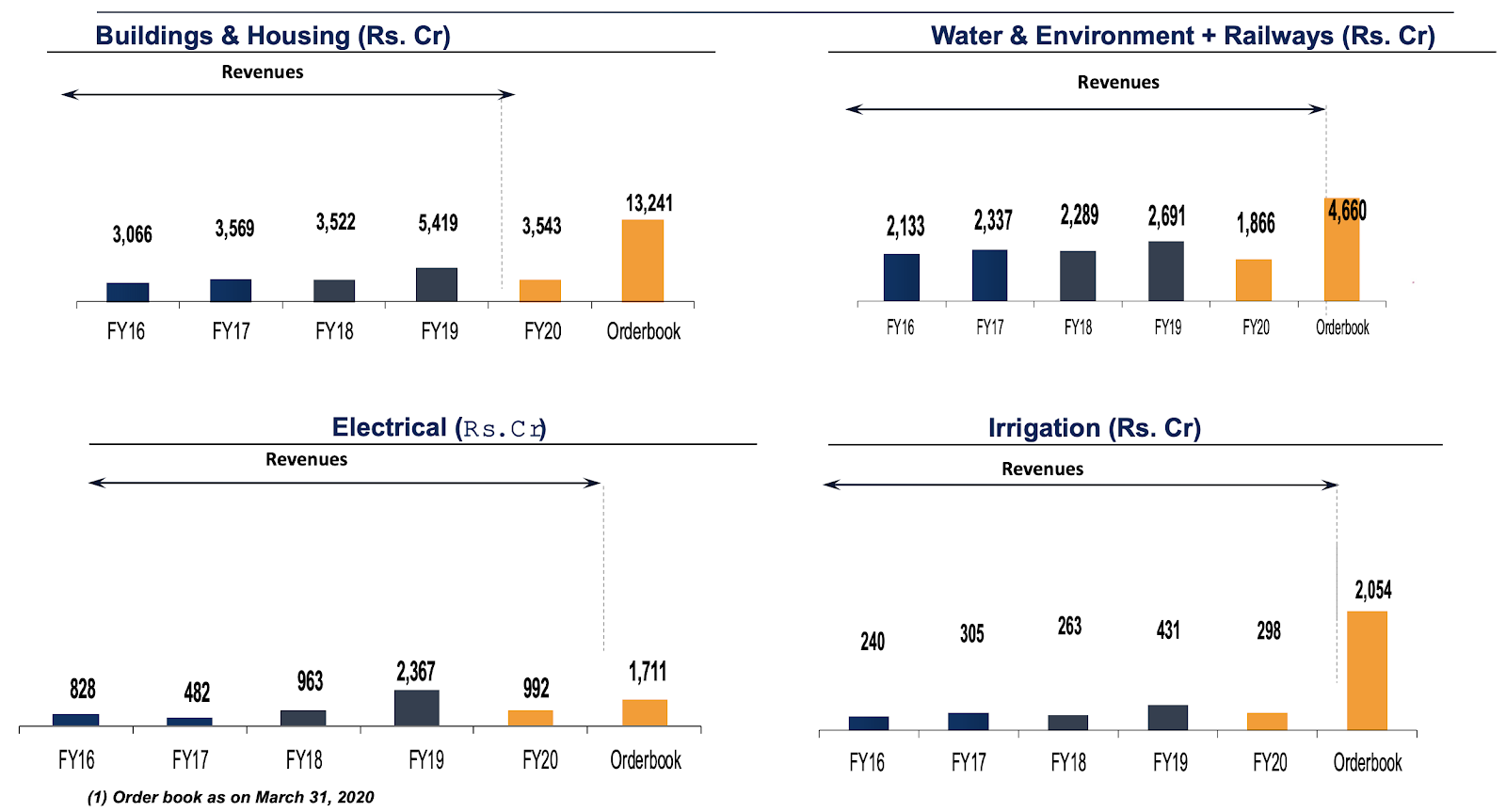

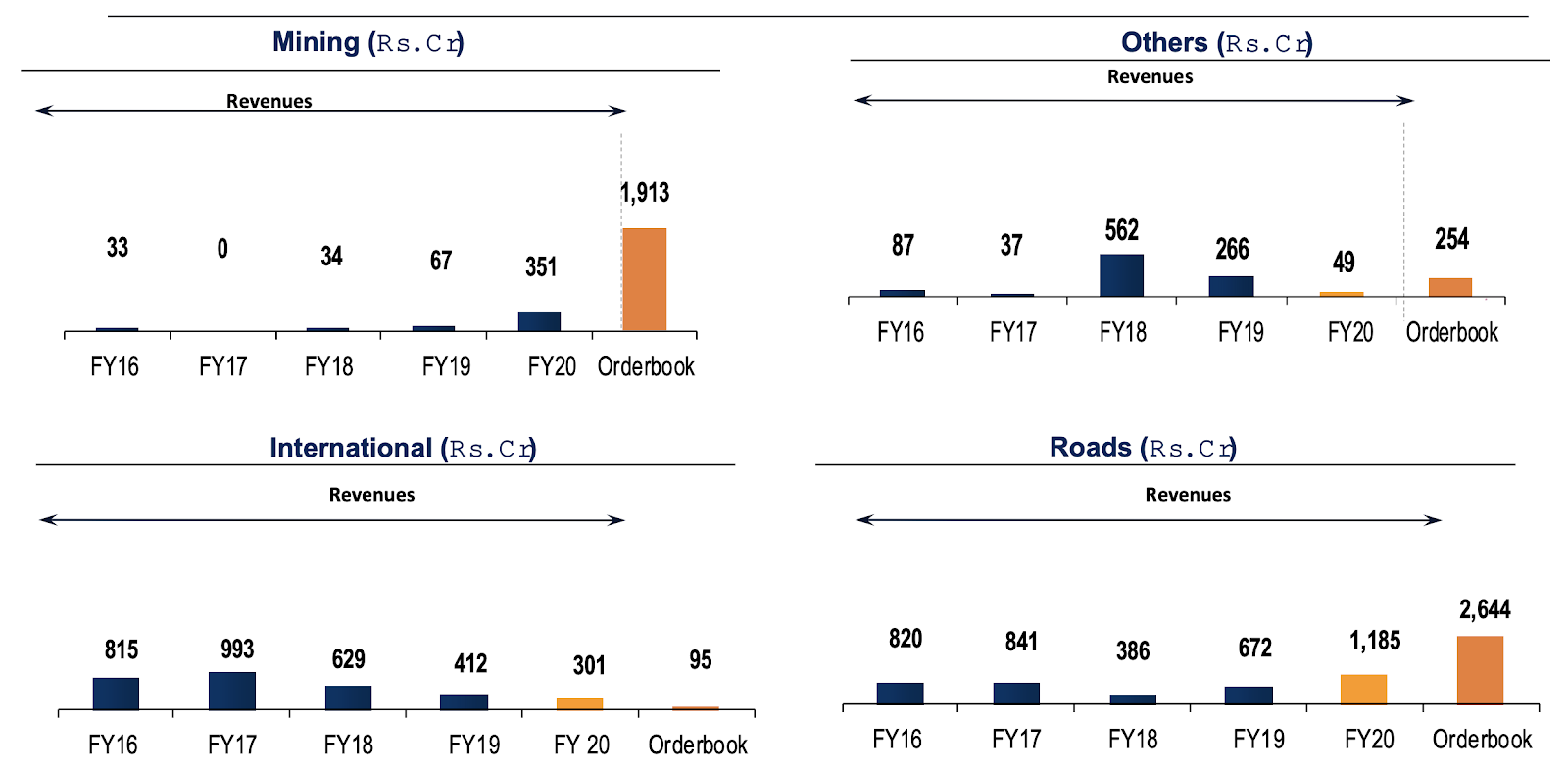

Diversified Order book and revenue stream: across different types of constructions undertaken:

- Various initiatives such as Bharat Mala, Sagar Mala, Pradhan Mantri Awas Yojna, Namami Gange Programme, Freight Corridors, Industrial Corridors, Smart Cities, etc. to provide additional impetus to Construction industry

- Divisional performance over time:

Comparison with Peers on Key Financials

| NCC Ltd | Prestige Estates Projects Ltd | KNR Constructions Ltd | Larsen & Toubro Ltd | |

|---|---|---|---|---|

| Market Cap | 2009.39 | 7594.16 | 2927.59 | 130367.73 |

| Stock P/E | 5.57 | 20.04 | 10.70 | 13.56 |

| Dividend Yield | 4.56 | 0.79 | 0.24 | 1.08 |

| ROCE | 22.32 | 10.11 | 19.23 | 13.46 |

| Sales Growth (3Yrs) | 10.62 | -2.21 | 24.35 | 11.72 |

| PEG Ratio | 0.03 | 10.89 | 0.31 | 0.95 |

| Debt to equity | 0.38 | 1.61 | 0.53 | 2.15 |

| Interest Coverage Ratio | 1.79 | 1.77 | 3.94 | 2.30 |

| Price to book value | 0.41 | 1.42 | 1.87 | 1.95 |

| Dividend Payout Ratio | 15.57 | 13.53 | 2.08 | 28.35 |

| Pledged percentage | 34.18 | 0.00 | 0.00 | 0.00 |

| Sales growth 3Years | 10.62 | -2.21 | 24.35 | 11.72 |

| Operating cash flow 3years | 1572.51 | 2347.80 | 842.15 | -8092.61 |

| Price to Free Cash Flow | 6.98 | 22.11 | 38.68 | -23.84 |

| OPM | 12.10 | 28.89 | 25.39 | 16.93 |

| Asset Turn Ratio | 1.77 | 0.41 | 1.11 | 0.75 |

| Receivables to Sales | 0.31 | 0.18 | 0.07 | 0.28 |

Key Conclusions from Peer comparison:

Things going for NCC: Low debt/equity ratio, high dividend payout, free cash flows, Asset light model: high asset turnover, low P/E and P/B ratios

Things not going for NCC: Low Operating profit margins, high promoter pledge

Reason to Invest:

- Company is extremely under-valued.

- Order book visibility (and no overhang of Amravati projects)

- High tailwinds for the sector in Long-term (Bharat Mala, NIP etc)

- The Asset Light model makes company nimble.

- High dividend payout

- Lowest Debt/Equity Ratio among peers (construction companies generally have high debt).

- Mutual funds are picking up stakes in NCC in the last few quarters.

- One of the only construction companies to generate Free cash Flows.

Reasons to Avoid:

- Low OPM: Although the OPM is low, with the exception of 2017, it has been largely stable in the 10-12% band.

- Low Interest Coverage: In latest concall company has guided for low Interest cost (as per trend in Q4 2020) if situation remains ‘normal’.

- High dependence on Government projects where things could be relatively uncertain.

- High promoter pledged shares: Need to dig deeper and find why this pledge happened and if and when it can be removed.

Disc: Invested and forms about 4% of my discretionary stocks portfolio. Will look to add more at lower levels or post Quarterly results.

Invite fellow ValuePickrs comments and thoughts.