The company has recently decided to issue Fully convertible warrants to the promoters (price not disclosed yet). As per my understanding, promoters will only pay 25% of the recent stock price and will have an option of converting it into Stocks over 18 month window.

Isn’t it a case of promoters using inside info to increase their stake at the opportune time? If the promoters want to increase stake, why aren’t they going for open market purchase or rights issue?

I also don’t understand why the company is issuing warrants right now, as neither company needs any big money nor are these warrants going to generate a lot of money (1. 8 cr shares at 25% of 60 rupees will give only 24 crores).

If anyone can throw some light on this topic, that would be great.

Company receives huge orders from govt in December…which is 3 times it’s market cap…time for re rating of this stock…low debt infra stocks are unheard of these days…

“guidelines for determining the conversion price have been specified by the Reserve Bank of India in accordance with which the conversion price shall be determined and which shall be in compliance with the applicable provisions of the Companies Act, 2013”

“specified securities so allotted shall be locked-in for a period of one year from the date of their allotment”

“guidelines for determining the issue price have been specified by the Reserve Bank of India in accordance with which the issue price shall be determined and which shall be in compliance with the applicable provisions of the Companies Act, 2013; issue price shall be certified by two independent valuers”

“Conditions for preferential issue: a special resolution has been passed by its shareholders”

“If the equity shares of the issuer have been listed on a recognised stock exchange for a period of twenty six weeks or more as on the relevant date, the price of the equity shares to be allotted pursuant to the preferential issue shall be not less than higher of the following:

a. the average of the weekly high and low of the volume weighted average price of the related equity shares quoted on the recognised stock exchange during the twenty six weeks preceding the relevant date; or

b. the average of the weekly high and low of the volume weighted average prices of the related equity shares quoted on a recognised stock exchange during the two weeks preceding the relevant date.”

So I do not understand where you are getting the 25% number from. Also it looks like they have already sought approval from all shareholders for making this allotment. What we should ask ourselves is: why did all the shareholders approve this?

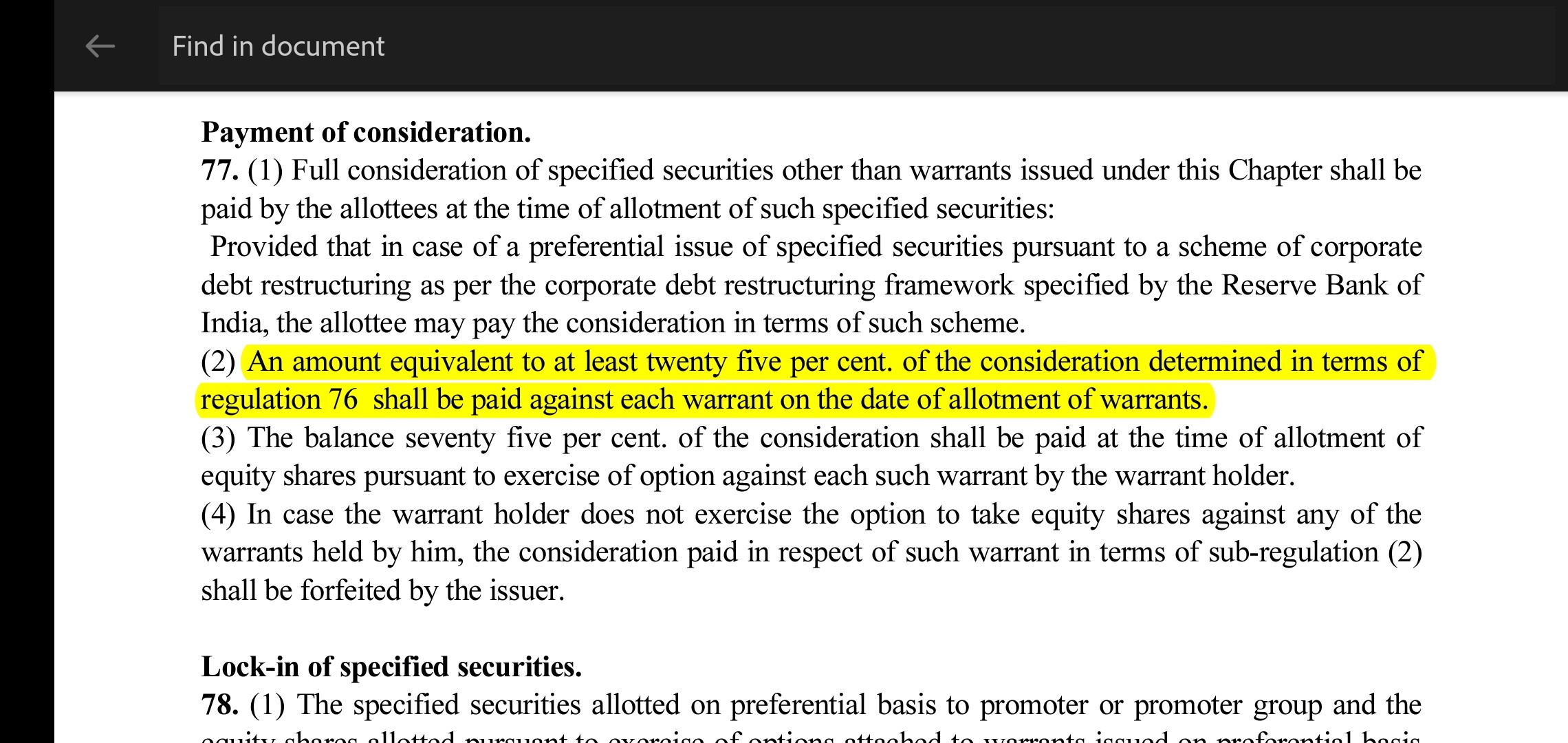

As per Regulation 77 (2) of SEBI(ICDR)Regulations, 2009, it mandates minimum 25% upfront payment. Regarding the shareholder approval, I don’t remember any such notice from the company in the past. Would be great if anyone can share the link to this shareholders’ approval announcement (if any).

Yes but wouldn’t they need to pay the difference (75%) eventually when the warrant is exercised? The 25% up front payment only seems like a minor irritant at best for the retail investor to me because the overall pricing is quite fair.

higher(Average price of last 26 weeks, Average price of last 2 weeks).

[quote=“sahil_vi, post:28, topic:38261”]

the price of the equity shares to be allotted pursuant to the preferential issue shall be not less than higher of the following:

a. the average of the weekly high and low of the volume weighted average price of the related equity shares quoted on the recognised stock exchange during the twenty six weeks preceding the relevant date; or

b. the average of the weekly high and low of the volume weighted average prices of the related equity shares quoted on a recognised stock exchange during the two weeks preceding the relevant date[/quote]

As it is not mandatory to exercise warrant, company may never get rest 75%. Even if promoters do exercise it, the major question is the need for issuing warrants. What is the benefit to the company?

If you look at any well governed company, they always go for either rights issue or buy from the open market. Both these steps take care of minority shareholders’ interests.

Issuing warrants itself is a dodgy idea, many experts have already said that it should be stopped by Sebi. On top of that, they did it just before they notified that company got 9000 crores of contracts.

It shows that promoters (holding just 13% unpledged shares) are trying to make money for themselves at the expense of rest of the investors (holding rest 87%).

Since we started this topic saying NCC is undervalued, may be its time to understand the reason behind it. Such corporate governance practices would make sure that no Institutional investor will touch this company. And my view is, while the company performance may help the share price for some time, governance practices are the decisive factor in long term wealth creation.

I agree completely. The warrants are definitely a shady way to increase holding. The quantum of the warrants is small though.

NCC is definitely not a long term secular growth story for me anyway, only an under-valuation play. Their RoCE for last 10 years is only 12% which is barely above cost of capital.

As you rightly said, I do not plan to hold it for several years, only until I feel it is still under-valued (which I do right now).

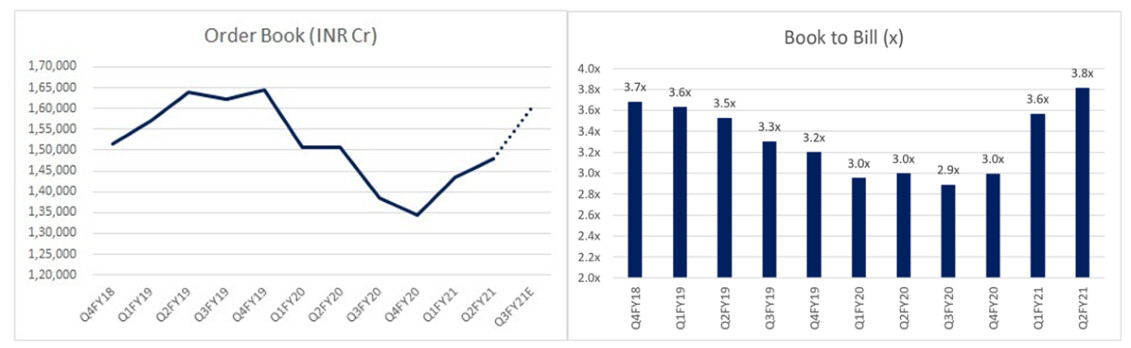

Order inflows has become very strong. And valuations for the sector seems cheap. Can it have a run up like metal sector? below is for top 11 companies excluding L&T

One significant risk that infra companies face are regime/govt change as a majority of infra orders are given by govt . There was severe cancellation of projects as well as delay in payment of receivables when TDP govt was replaced by the new govt severely denting order book then. This may happen for many other infra companies However the company did fairly well to bounce back from that point.

When both cement and commodities are on a bull run, won’t that hurt the margins of infra companies severely???

Commodity price inflation is a pass through in EPC contracts. So doesn’t hurt margins. Secondly bulk of the orders are coming from UP and states nearing elections. So atleast till 2022, these projects will be fast tracked for execution.

Does anyone have any idea why Promoters are Buying and Selling the exact same number of shares on the exchange on the same day? Is it to keep the price constant or is it something fishy?

NCC has received two new orders totaling for Rs.444 crore (exclusive of GST) in the month of September, 2021. Out of these orders, one order valuing Rs. 280 crore pertains to Water & Environment Division and the second order valuing Rs. 164 crore pertains to Building Division. These orders are received from State Government agencies and do not include any internal orders.

Any specific reasons why NCC is not able to increase their margins? Many other EPC companies like KNR etc have very good NP margins at 10% while that of NCC is around 4%. NCC is an established company, so thought the margins would be better

Any specific reasons why they are not able to improve project execution? They have a very good order book and the new order inflow is good as well. But topline doesn’t seem to increase much as seen in Q2 (Q1 had a covid impact)

I believe (not very sure) that one main reason is that NCC is mainly into government contracts, which are very low margin accretive. Given the further delay in payments, interest costs further eat up the PAT margin.

Yes probably. I also wonder why they are not able to ramp up execution. Given the strong order book and regular order inflow, there is scope for scaling up the topline. But they seem to be stuck in a range as a non Covid scenario unofficial guidance also is in the range of 3000 crores per quarter.