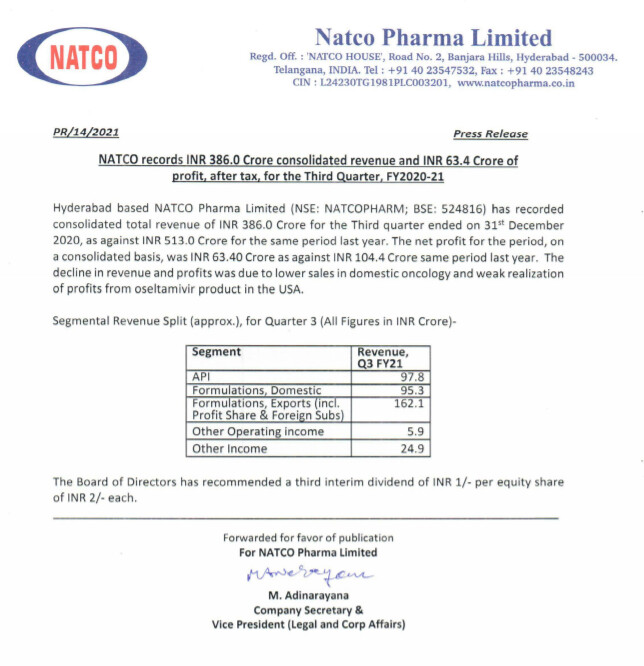

My first Concall Q3FY21 notes, excuse me for the typos / if missed some of the names wrong (Ravi from VP tribe was there on the call, hopefully he can post more here )

Oncology - Impact is mainly due to less number of patients in the hospitals due to covid

Some drugs, for example used in Bone Marrow Transplant , the sales are zero, that means there are no transplants done at all

Agro chemicals - We are aware of the strict regulatory norms against the pesticides so we would like to have basekt of all including Green Pesticides (one cannot move away from the toxic pesticides altogether but we are very much concisicous)

100 employed in this division, have many reps.

Bullish on Agrochemicals

Size of the market is 2000 crore

We are the first to launch, we are not here to do commodities business, we look for sweet spots , we look for niche areas

Agro Capabitlies :

Do your own brand, create market for yourself

Chicken and egg story (unless you don’t do it you can’t be sucessfull ), do something unqiue standout from the crowd

Regarding the marketing of the new ago chemical molecule , since court case is going on we can’t say much, it will be announed very soon about how exactly they are going to go into the market

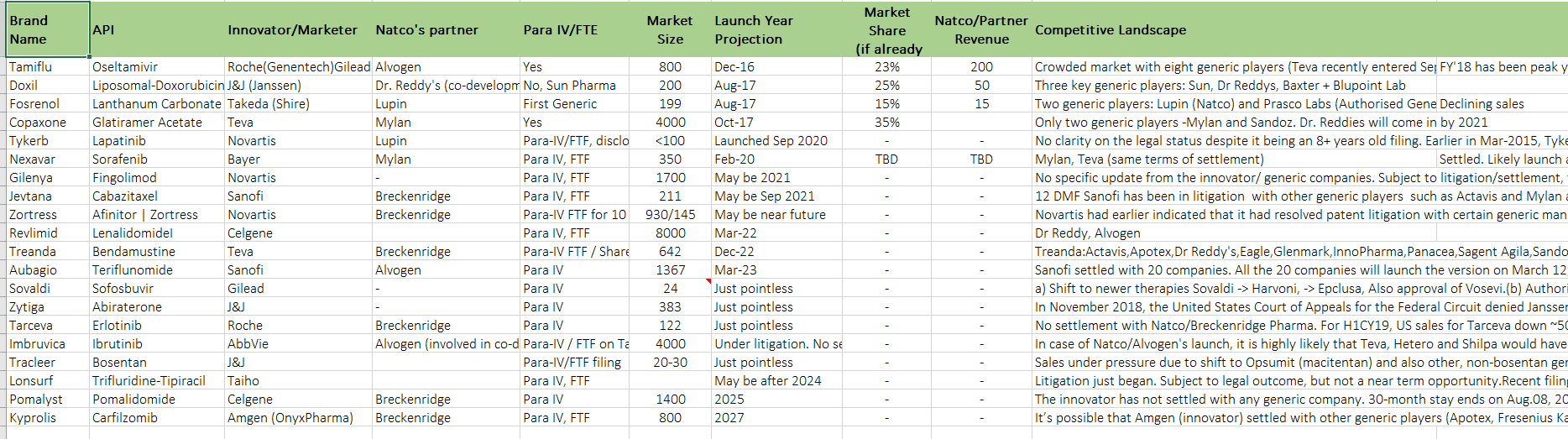

Revlimid :

There is nothing pending from our side, all the queries are answered hopefully approval come very shortly

March - 2022 (Limited quantity only we can produce to start with), pricing power good be very good

Unless we launch we can’t give any projections, we have first mover advantage

Supply side is the question (how many suppliers will be there going forward) when it comes to competetion in this space

Extremely Bullish on FY 22

Bullish on Launches Lenalid and two more

Our strength is always on niche , diversify the portfolio (agro), build the base that is steady

Core portfolio - 20% Degrowth is common in generics (Question on dips / flat reveneues isntead how can you maintain stable growth)

Brazil and Canada

Brazil - Takes longer but margins are good

Canada - Next year very good launches in Brazil and Canda

many launches in Brazil and Canada are close to approval

Oral Oncoloy - More stable compare to Chemo

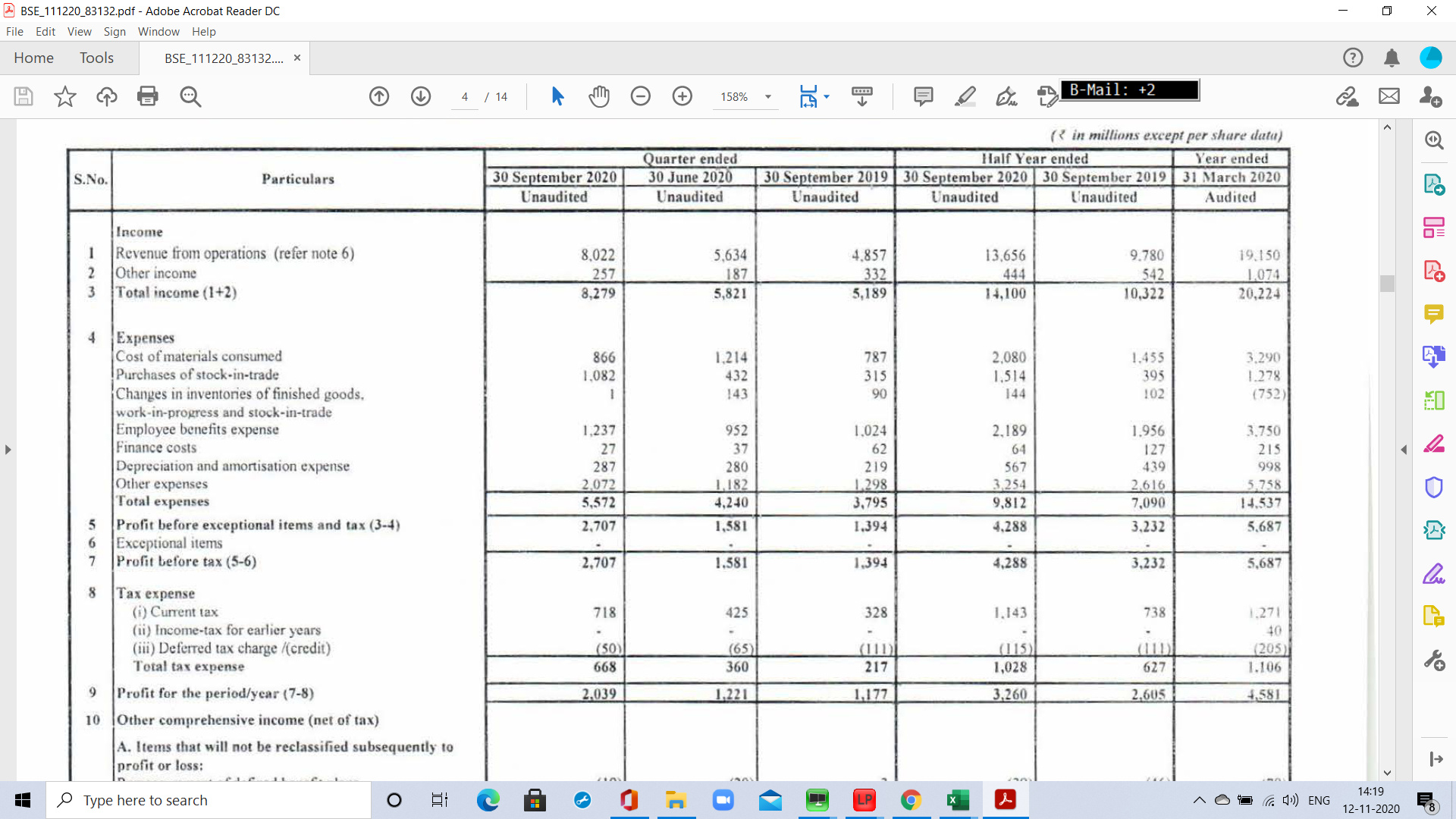

Our numbers can’t be looked at on QoQ basis , we are different business model

10 Launches in next FY in India (Oncology and Cardio)

we are more focussed on chemistry oppotunities not biotech opportunities

Immuno suprressant next year launch

Just come across this wonderful discussion between @sahil_vi @harsh.beria93 and the regulatory and compliance Expert Mr. Amit Rajan , you should listen to what he thinks about Natco ( in the entire video he never recommended or critical of any businesses )