Excellent summary Ranvir - I also listened to the concall…

Lenalidomide is the next biggest trigger for Natco for sure. Approval expected before December 2020. Sales should start from Q4 2022 (March 2022 launch as per the agreement with celgene) - stocking for March 2022 will start from Q4 2021/22 financial year…

Natco is a niche company and their strategies are unique.

Discl - invested and accumulating since 2013 - 25% of portfolio at present

Company’s profits in FY20 was Rs461crs. Guided for 25% PAT growth implying PAT of Rs576crs in FY21. So at current market cap of Rs15420crs company trades at 26x FY21. If Revlimid gets launched FY22 PAT could be Rs1400crs also. Implying company trading at 11x FY22. Stock looks quite cheap compared to where other pharma names are trading

Hi Venkatesh - I think better to describe lenalidomide opportunity as "large’, and it is impossible to put a $ value to it at this stage. There are so many variables…Also, it is better for us shareholders not to advertise this opportunity too much I haven’t finished buying, the cheaper the share price, the better it is for us…

What I understand, this drug is not going off patent. NATCO has out of court settlement where NATCO will be allowed to sell certain percent of drug every year. This market share will increase every year. So price erosion will not be there. Once drug is off.patented, NATCO is free to sell any quantitity. It is blockbuster drug having more than 5 billion dollar market 2 years before. And it was growing, I dont know the condition now.

This drug is special. Once doctor recommends, pharmacy enters the data and get approval from manufacturer, only then it is sold. So it is taken in extreme medical supervision. This will help NATCO to track the total quantitity of drug sold so that they can claim their market share.

10% of 5 billion dollar is 500 million dollar i.e. Rs 3600 crore. Here I am considering 10% market share in first year. This is the difference between reserch driven pharma company and pure generic pharma company. Patent holder is let down for out of court settlement. In court there were chances that patent was challanged.

Disclosure - No holding. May buy anytime.

Good for natco due to the accelerate clause I think - they might be able to sell lenalidomide earlier than previously agreed - need to double check this…

Discl - holding and adding since 2013. Bought few more yesterday

Nothing changed overnight… People just recalled that before Dr Reddy’s , Natco was the first mover on Revilimid And TV analysts shouting hard for market size of the drug on Twitter

Natco Pharma would be the first company to launch Revlimid (lenalidomide) in March 2022 as Dr Reddy’s settlement clears the path for the company. Dr Reddy’s would launch sometime after it (we assume 6 months) and would have market share restrictions lower than Natco in our view,” said Sriraam Rathi, analyst at ICICI Securities.

The next most important trigger is FDA approval of Revlimid/lenalidomide which is expected before December 2020 according to the management - they have to get the approval for them to be able to sell it!

I did some work on some of the molecules of the Natco. Please find the details below.

Everolimus

Immunosuppressant to prevent rejection of organ transplants.

Used for treating renal cancer

Marketed brands

Zortress - USA - Novartis

Certican - EU - Novartis

Afinitor

Votubia

Evertor - Biocon

Competition

Natco

Dr Reddy’s

Glenmark

Biocon

Hikma

Par Pharma

Teva Pharma

Exclusivity expiration date - Feb 2023

Novartis

Afinitor/Vitubia had 1.5bn sales in 2019

Zortress/Certican has sales of 485mn$ in 2019

Sorafenib

Brands

Nexavar - Bayer

Used in treatment of kidney cancer, liver cancer, thyroid cancer

Indian Patent office granted approval to Natco to manufacture Sorafenib in 2012, bringing price down from 2.8L to 8.8k for 120 tablets. Natco pays 7% royalty to Bayer

US patent is expected to expire in Dec 2020, Europe patent is expected to expire in July 2021

Nexavar has sales of approx 800mn$ in 2019

Ibrutinib

Brands

Imbruvica - Pharmacyclis Inc (acquired by AbbVie)

Typical cost in US for ibrutinib is $148k

Patent is expected to expire in Dec 2026

Sales of 3.5bn $ in 2018. Some reports state the size at 6.2bn$. fiercepharma pegs size sales at 7.2bn$

Lenalidomide

Brands

Brands - Revlimid - Celgene (Acquired by BMS)

It costs 168k$ per year in US

Celgene almost had sales of 9.7bn$ in 2018

Alvogen lauched generic product in EU. Revlimid had sales of 1.8 bn$ in EU in 2017.

Alvogen can also launch product in US from March 2022 in volume limited way

Lapatinib

Used for treatment of breast cancer

Brands

Tykerb - US - GSK

Tyverb - EU - GSK

Patent expiry - US Nov 2021, June 2023

Tykerb had sales of 300mn$ which is down to 100mn$

The key questions that needs answering are -

gCopaxone probably represents 50% of the PAT for Natco. Natco has been holding on to 30% kind of market share in this product. What happens when Dr. Reddy’s get approval for this product? Gaining market share is not so easy in this product but what if Dr. Reddy’s managed to scale it?

gRevlimid has 10 ANDA filers and we have already seen 3 approvals. The situation remains quite dynamic. Also, we probably need to do some work on how easy it is to gain market share in this product ?

The MOST important question is - does Natco have a pipeline where they can launch one large value molecule every year or does it remain a one molecule wonder? Ibrutinib is a big molecule and Natco believes it is first to file in that molecule. How about others?

Disc - Invested from lower levels, not a buy/sell recommendation

Following are the tweet info from Dr Punit Bansal (@punitbansal14). This info is on public domain and I thought this will be useful for analysis on Natco.

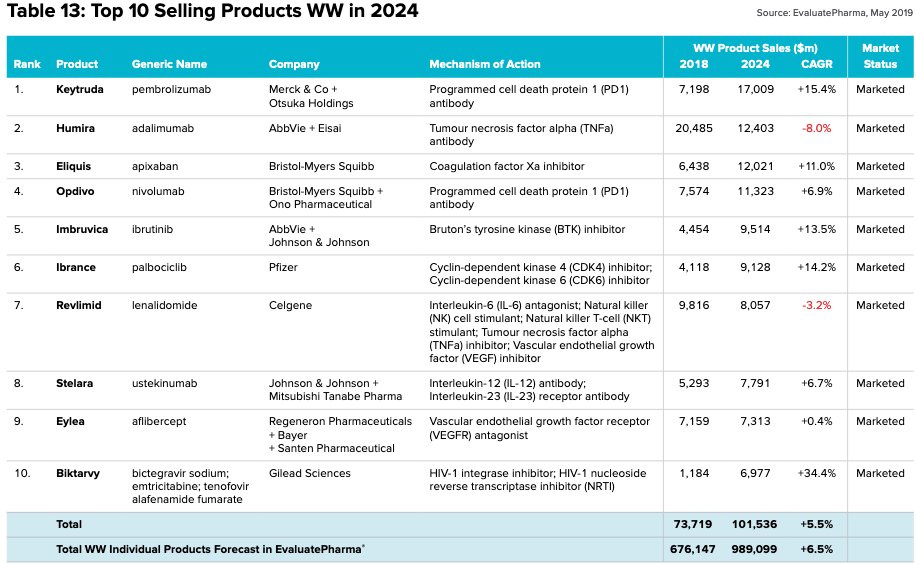

Revlimid (lenalidomide) is among the top 10 selling drugs with estimated MS of $8.0B in 2024, used as 1st & 2nd-line multiple myeloma therapy in US through REMS program.

Natco has strong 20 Para-IV pipeline & remain focused on therapies with limited competition.

gRevlimid has 10 ANDA filers and we have already seen 3 approvals. The situation remains quite dynamic. Also, we probably need to do some work on how easy it is to gain market share in this product ?

Patent for Lenalidomide expires in 2026/27 (I am not sure of the exact date) - so celgene has the exclusive rights to sell lenalidomide until that date in the USA. This is the most important point to note. No one else can sell except celgene - but, celgene could share patent rights with others…and that is what is happening here…

Celgene has settled with 3 companies so far out-of-court - natco, alvogen and dr reddys.

Natco settled first in 2015 and according to the agreement celgene will share rights to the patent with natco for mid single digit market share commencing from March 2022 and this will increase to not more than 1/3rd by 2026. After 2026 patent expires, and anyone can take the market share provided they have the fda approval. So there is certainty between 2022 and 2026…

The news article statement announcing the deal between celgene and Dr Reddy states mid single digit market share at a date starting after March 2022 (note - after March 2022). So, it is reasonable to assume that Natco got the most favoured outcome from celgene, followed by alvogen, followed by dr reddys. Hence Natco will be allowed to sell first followed by alvogen and then dr reddys (this is my assumption). Total sales allowed as per the agreement also will favour those who settled first…