ValuePickr Research

Resources

Basics

ValuePickr Forum

VijayKiran (VK) Long Term Portfolio Mistakes & Learnings

Q&A: Questions & Answers

Portfolio Q&A

Vijay_Kiran

November 1, 2020, 9:40am

44

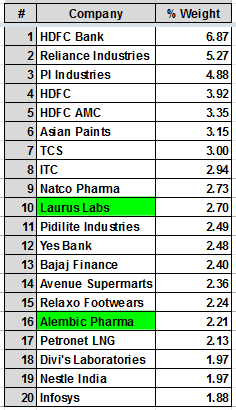

PF Stock Update as on 30.10.2020

Top 20 Holdings:

image

236×410 7.15 KB

Note: No additions in the month of Oct’2020 in core PF except for Nestle.

8 Likes

Malai's Copy Cat Portfolio

Pidilite Industry : Fevicol ka Jod

Simple Investing

Natco Pharma: Focusing On Complex Products

Relaxo Footwear: a wannabe brand play

Petronet LNG Limited - Green India with Clean Fuel

show post in topic