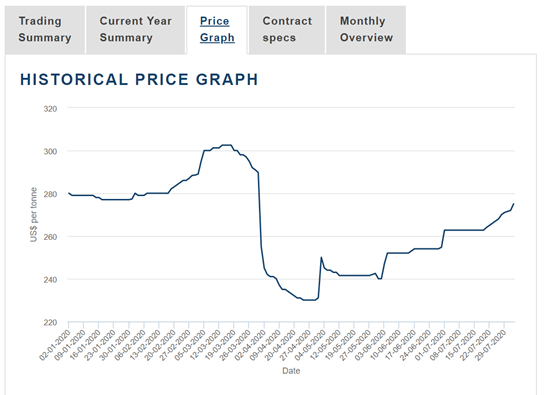

Another data point is that of alumina whose prices have also gone to almost pre-covid levels (LME 1 month forward prices)

Another data point is that of alumina whose prices have also gone to almost pre-covid levels (LME 1 month forward prices)

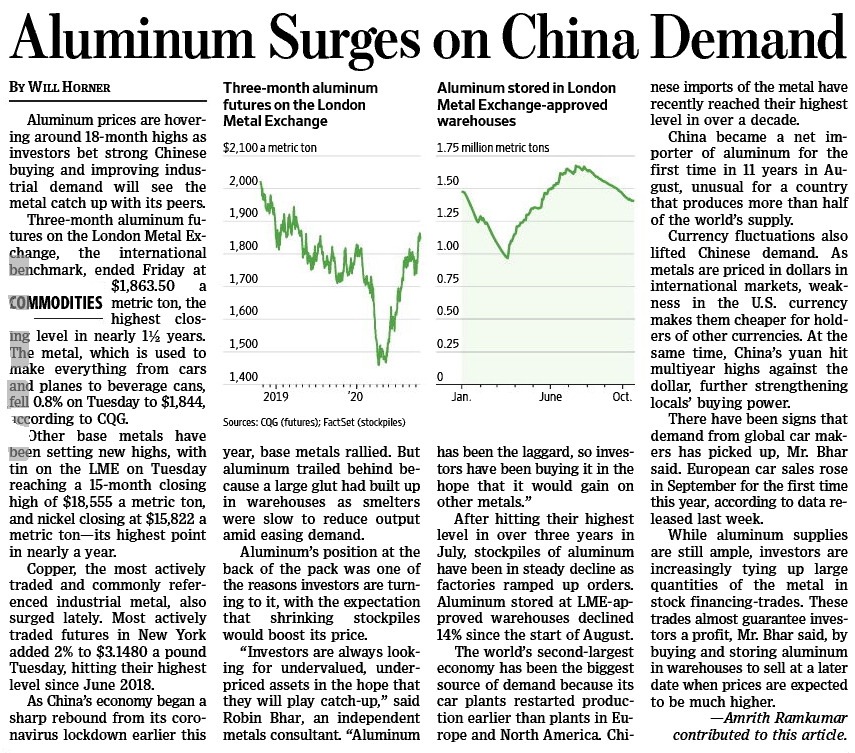

Aluminum margins for Hindalco was ~19% this quarter, demand for the aluminum division of Hindalco is at 85% pre-COVID level. Demand is mostly coming back from China, and Chinese aluminum prices have gone beyond LME prices. Average aluminum prices during the last quarter was $1490, its currently $1750. Market is unsure of sustainability of this because the LME price rise has been very sharp. Here are the two videos of Hindalco management interaction (video1, video2)

Global peer Norsk Hydro (largest producer of alumina and bauxite) has temporarily halted production of alumina.

https://seekingalpha.com/news/3606883-norsk-hydro-stops-paragominas-bauxite-pipeline-ops

Update: Nice article from BQ

Got this from the net on the temporary halt of alumina production

https://apnews.com/dca65eca5129955db192e81e8434fb62#:~:text=Hydro%20has%20halted%20operation%20of,and%20reducing%20production%20at%20Alunorte.&text=Hydro%20is%20taking%20all%20necessary%20measures%20to%20mitigate%20any%20customer%20impact.

Looks to be for a 2 months period

Its an low risk moderate return type of stock today, The over supply scenario globally expected to last for 1-2 years, bad thing about this recessions was globally central banks bailed out everyone so, demand is gone ( real economy is in pain) but supply has not diminished ( not many mining companies went bankrupt)

but anyways if one expects demand to catch up in 3-5 years you can expected to make 10-15% kind of CAGR in 5 years.

My worry is there are other ways to make these returns ( bond markets - many companies at 10%) but after 3-5 years when you sell will you have the opportunities you have today in the market ? Will you have the companies like Edelweiss , SIB trading at 10-15% YTM in bond markets ( of course risks are there) but we may have markets which discounting all the risks 5 years from now.

In short cyclicals my problem is it’s another headache to time selling and then find our new thing. ( there is additional opportunity cost involved here) .

i want at least 4-5 x from cyclicals today not 2x (in 5 years), realistically we should not expect it to trade Rs 150- 200, i think Rs 60 is a good case scenario as supply side of industry is not affected ( bailed out by central banks).

Thoughts invited.

Results declared today, aluminum division is back into black. Overall reports a small net profit of 13 cr. One weird thing was in the notes to account section containing this. I didn’t find these joint ventures in their previous annual report, so its probably a recent joint venture.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/c8c7bff5-b968-4500-8e1e-689eda705d24.pdf

CNBC interview (link)

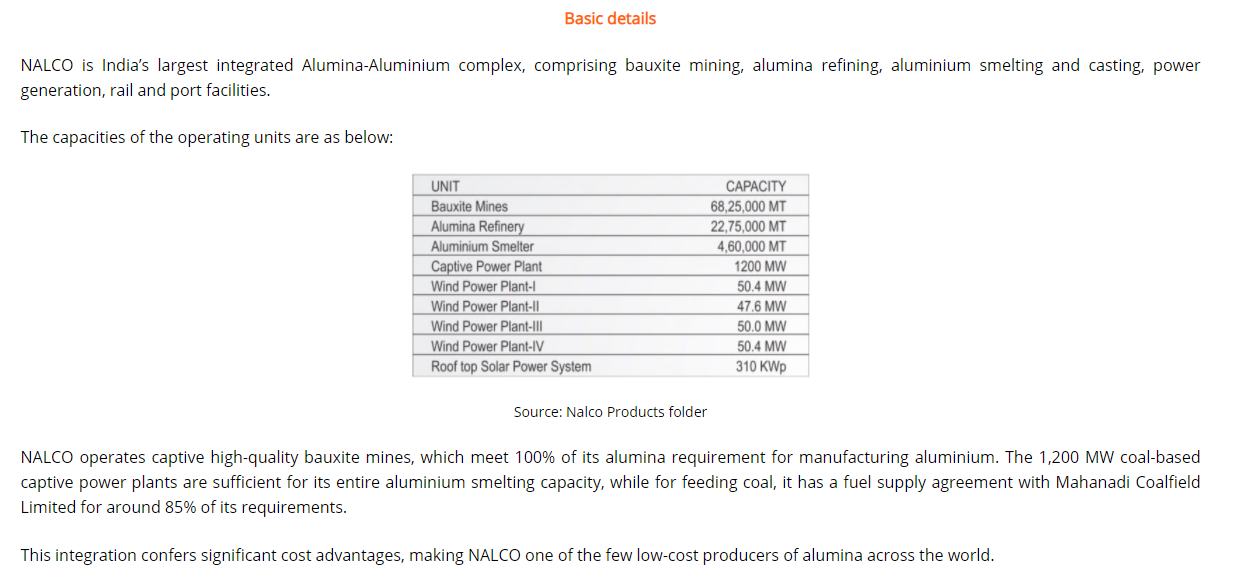

is anybody aware of the comparative cost of aluminium production for Nalco, Hindalco & Vedanta?

sorry for my ignorance - but can you explain - what all different substances do you include in ‘Commodities’ ? - - metals- Ferrous and Nonferrous… sugar … oil … - is Cement / coffee also included?

Good set of results from NALCO, aluminium division reported 14.7% YOY growth in sales. Chemicals division de-grew in revenues by 14.5%, however margins were higher resulting in similar PBT compared to last year. Both divisions are in black now. Good cashflow generation leads to slightly higher cash balance (~2090 cr.; increased by ~100cr.).

Dislosure: Invested (position size here)

Chart of AL Vs NALCO - Clear divergence currently, it tends to auto correct over time whenever it happened in past…

@harsh.beria93 - They haven’t switched to lower tax rate yet- do you know why ?

Came across some very interesting charts on twitter by Dhruva - https://twitter.com/Dhruvapandey/status/1326420389233373184?s=08

Research Report from Katalyst Wealth on NALCO for reference.

Few excerpts below:

NALCO - Last month volume in NSE is highest in the history (18 years - as per zerodha’s chart). Is it something that big players are entered here? Is there some fundamental change?

Disclosure: I have invested in NALCO.

Nalco’s Board to consider the Buyback of shares. The Board meeting is scheduled on 27th January 2021.

Company comes up with a large buyback of ~7% equity shares (~749 cr.) at a price of 57.5 via tender route. Record date is 8th February.

Disclosure: Invested