Manappuram subsidiary Asirvad results have come out and looks good https://amlcdn.b-cdn.net/img/Q3-FY-23.pdf

6 Likes

Microfinance performance is phenomenal but the standalone performance have been poor again this quarter. Gold loans at 18,614 crore against 19,190 crore last quarter which is a degrowth of -3 %. its even worse compared with same quarter last year with degrowth of -9 %. As per the investor presentation they are facing intense competition in the gold loans. Most likely by next quarter IIFL will topple manappuram as the second biggest gold lender. IIFL gold loans stands at 18,284 crores this quarter which is increase of 3 % quarter on quarter and + 25 % compared to last year.

As per manappuram management they want to prioritise yields over growth which stands at 22.5 % this quarter for gold loans. IIFL gold yield stands at 17.8% and it looks to me that IIFL is growing at the cost of manappuram.

1 Like

From the presentation “We expect gold AUM to stabilise/grow modestly in the near term”.

so it looks like gold loan AUM to remain range bound for sometime.

1 Like

First Quarter where IIFL Finance TTM PAT has surpassed Manapurram’s TTM PAT…

Industry mapping is extremely important for this reason. Given lower yield gold loans of IIFL and multiple segments they have like Affordable housing, Mfin etc. Quite surprising to see it surpass in a short span.

Disappointed how Manappurams business has evolved over the years. Had plenty of time to diversify.

Disclaimer: Holding IIFL Finance for over a year. Switching from Manappuram to this, now in hindsight seems to be the correct call.

7 Likes

Thoughts on the latest results.

Though MFI segment grew well, their GNPA is at 6.7% and this will affect profitability due to provisions. No information about the credit rating of borrowers as well.

Their top-line(Gold loan) is shrinking quarter over quarter amidst rise in gold prices. Management mentioned in previous con-call that they will not introduce any more teaser loans to retain those customers. Gold loan customers are also steadily declining.

Positives

- Asirvad MFI segment grew both sequentially 13% and yearly 22%.

- Asirvad MFI segment’s ROA improved to 3.59% and ROE improved to 20.02%. GNPA reduced to 6.7%.

- MSME grew at 23% and their GNPA is low. But they contribute only 4% of the overall AUM.

- Decent growth in Vehicle Finance(12%) and House finance(8%).

Negatives

- Top line business - Gold AUM degrew on both sequentially and yearly.

- Avg. Ticket size of loans has reduced and number of customers are also declining. They are not able to hold their high value customers. In past they introduced teaser loans at rate below 12% to retain high value customers. But they are facing intense competition from banks. Cost of funds also increased to 8.1%.

Concall highlights

Net profit of Manappuram Finance rose 50.26% to Rs 392.17 crore in the quarter ended December 2022 as against Rs 261.00 crore during the previous quarter ended December 2021

GOLD

- gold loan Target audience is the lower middle class

- Demand is slowly picking up

- We have 4000 gold loan branches and increasing around 100 branches every quarter

- high competition and slow demand reasons

-Gold loan ROA is 6%

NON GOLD

- non gold portfolio growing well and as planned moving towards well diversified company

currently gold business is 58%. In the next two years, it will be around 50-50 gold : non gold

CONSOLIDATED

-in few quarters,we are hoping to reach our target growth of 20% CGR and 20% ROE

-slowly, growth is coming back and coming quarters will be better

BANKS

-Banks and NBFCS have different advantages and disadvantages. With us the advantage is fast disbursement and Customers don’t lose a day

-Some reverse cases happening , some customers from banks are coming back to us

ASHIRWAD

- Ashirwad has capital adequacy of 21% .Aim is Keep it at around 20%.

-When Market-situation improves we may raise private equity for Ashirwad ,it may get listed eventually but we don’t know the time frame

My thoughts :

-Book value 109

-Currie price 115

-Market is not giving any valuations to its brand and not expecting any growth

-If we see growth as guided by management then may see rerating

- gold loan is operationally very challenging so competition won’t last long and on the horizon we Will soon get 20% roe and growth

10 Likes

But can’t thr be a possibility that IIFL gold loans are at an inferior quality. Probably to focus and show this short term profit, thr gold loan lending is aggressive.

On the other hand, the experienced Manapuram is proceeding cautiously and focussing on book quality rather than chasing growth??

3 Likes

IIFL has quite a different product as compared to Manappuram. They do long tenor loans as compared to Manappuram (average tenor at 2 years vs 3-6m for Manappuram). This difference also ought to bring a difference in growth and yields I believe

2 Likes

Quality doesn’t matter as long as it’s a gold loan. Npa has no meaning in gold loans

1 Like

I think quality does matter after a point as I believe upon auction, the company can only recover the principal and not the interest (someone correct me if I am wrong). So if a company ends up doing a lot of auctions, they will not receive interest and end up losing on a lot of business

3 Likes

- To ur earlier reply, that was part of my concern - longer the Loan tenure, greater the risk. And short term profits can be bumped up with cheaper avlbl debt nd reckless lending. The chickens vl cm home to roost later.

2.) U were spot on NPA part to @Souresh_Pal reply. I hv been a participant in these Gold loan auctions nd the strtng price for these is the pending amt(a.k.a recovery amt ) only, irrespective of prevailing rice of gold.

2 Likes

I have shared auction nos regularly on this thread. Whenever industry goes through headwinds, Manappuram is the first to report auctions, as their loan tenure is the shortest. Also, Manappuram’s auction are generally on the higher side over time.

The reason why Manappuram and Muthoot have been struggling for growth is they haven’t gone into colending model vs new age cos which are doing colending with banks. Banks have lower cost of borrowing and if they can find distribution partners (like NBFCs), they can offer much lower rates. Additionally, most banks only expect 2-3% ROA from this segment, whereas Manappuram/Muthoot are used to operating at 5%+ ROAs over cycles. Its anyone’s guess if this colending model is a terminal risk for traditional gold financiers.

In my personal observation, every few years lending cos come up with a new model (e.g. securitization, colending, etc.) which are considered superior, works for a few years, and then blows up.

Disclosure: Invested in Manappuram Finance (position size here, no transactions in last-30 days)

12 Likes

How we can confirm about the book quality?

Their GNPA numbers are high for MFI segments. It is around 6.7%. We have no information about the credit rating of customers in any segment.

If you have some data, can you please share?

" gold good growth yoy but flat qoq" —> no wrong. YoY gold loan also have degrown by 9%. 20,500 crore in Q322 to 18,614 crore this Q323 quarter.

Unfortuantely I dont think we have the info. remember MFI is mostly lending to people at the bottom of pyramid and most dont even have regular bank accounts let alone credit ratings. If my memory serves right, I remember that they validate customers using their cashflows/how much wage they get paid daily etc.

1 Like

Looking at all these pessimistic comments…It would appear this company is close to turn around… Company does not want to sacrifice their edge for growth. Aashirwad is a dark horse. They say they might list it or do a capital raise in future. But the bottom line is rural India is struggling which is the main customer base of manappuram for the small ticket small duration loans. Agro commodity prices are sustaining at higher levels so sooner are later demand from farmers/rural households will come back with vengeance.

Invested

6 Likes

True

possible probability of turnaround

Slowly market perception will change from plain gold business to diversified Buiseness

Gold business is a great cash cow, which can buffer the nbfc

An ideal combination

Great dividend yield

And close to book value

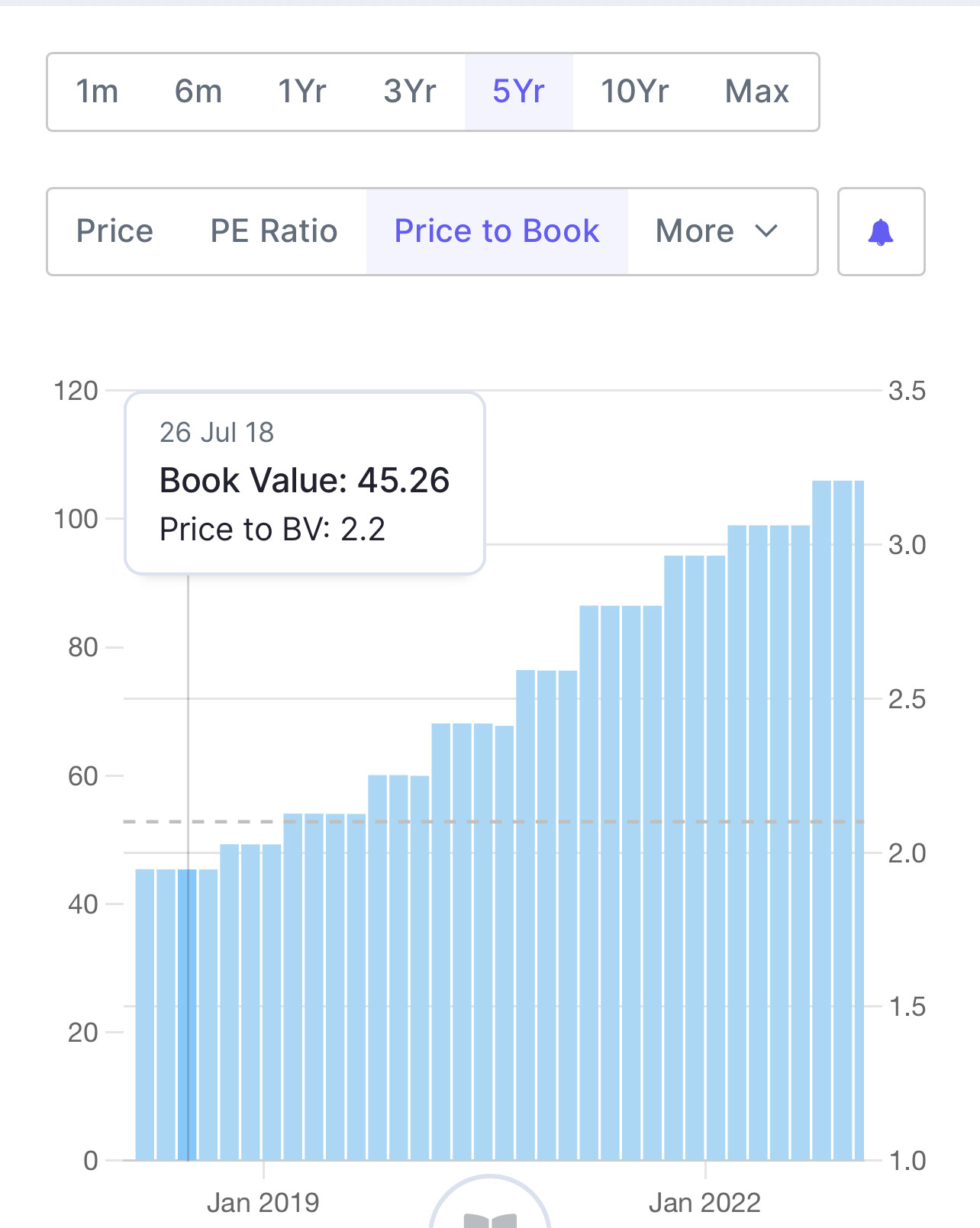

book value is steadily increasing

It was 45 rs in 2018 and now it’s 110

But price has steadily declined on background of steadily increasing book value

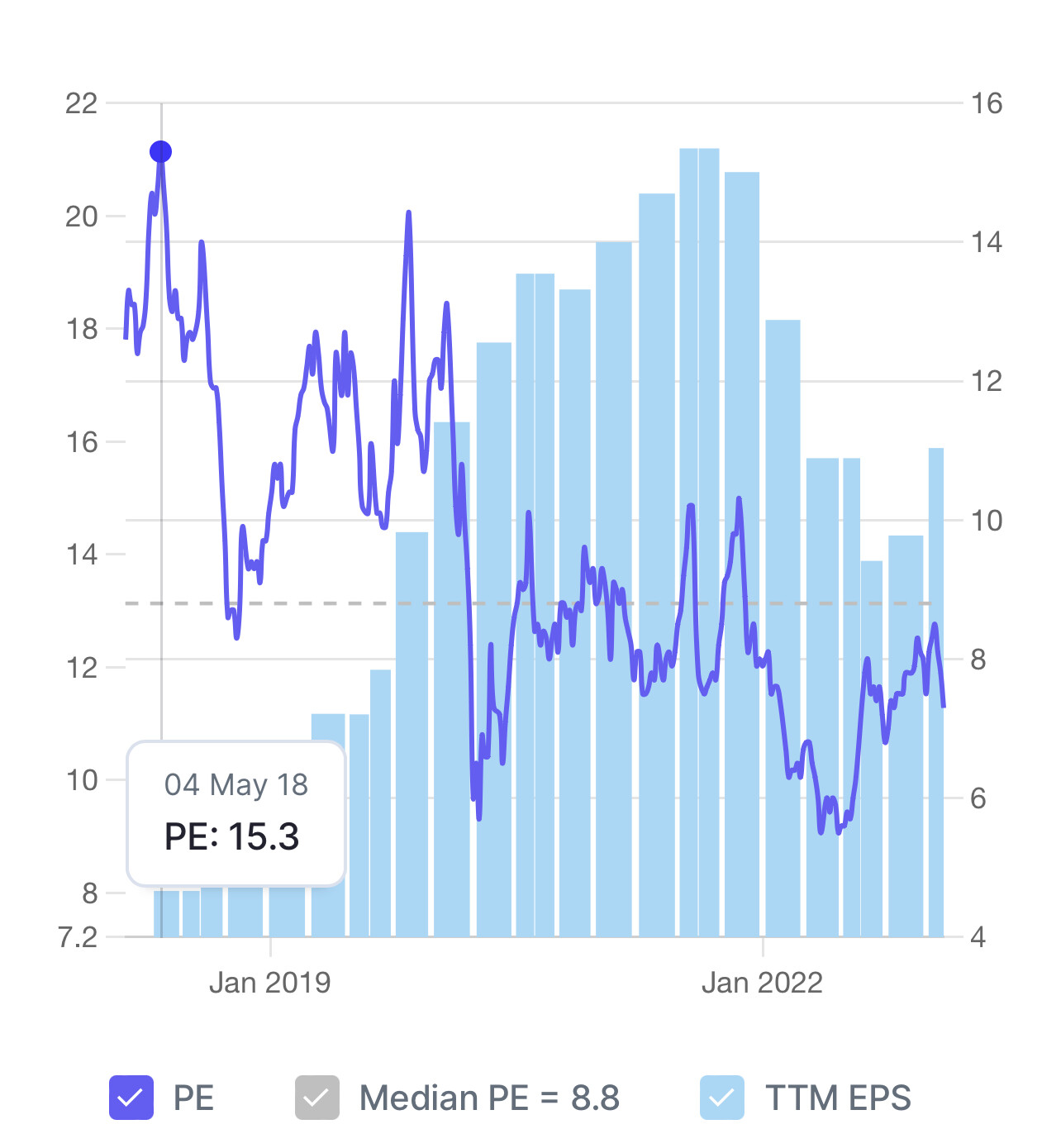

While price to earning is slowly decreasing

It decreased from 14 to 7 now

Let’s see how long this trend continues falling price vs increasing book value

Also Dividend is gradually increasing

Management is optimistic of growth coming bank from q4

1 Like

How is their Microfinance division compared to Armaan Financial?