Can someone post the cost of funds for all these entities?

Here are the updated gold AUM and auctions for FY22 and how it has varied over time across gold financiers.

| AUM (in cr.) | FY13 | FY14 | FY15 | FY16 | FY17 | FY18 | FY19 | FY20 | FY21 | FY22 |

|---|---|---|---|---|---|---|---|---|---|---|

| Muthoot finance | 26’000.04 | 21’617.90 | 23’349.90 | 24’335.50 | 27’219.90 | 28’848.40 | 33’585.30 | 40’772.40 | 51’926.60 | 57’531.30 |

| Manappuram finance | 9’945.80 | 8’155.20 | 9’269.30 | 10’080.60 | 11’124.53 | 11’734.98 | 12’961.52 | 16’967.18 | 19’077.00 | 20’168.00 |

| Bajaj finance | 37.39 | 146.78 | 543.96 | 655.01 | 853.37 | 1’557.49 | 2’239.97 | 2’047.91 | ||

| SBI | 900.00 | 2’179.00 | 20’987.00 | 37’500.00 | ||||||

| HDFC Bank | 4’042.00 | 4’057.00 | 4’531.00 | 4’800.00 | 5’500.00 | 5’900.00 | 6’200.00 | 8’300.00 | 8’367.00 | |

| Shriram City Union | 4’787.00 | 2’453.00 | 2’943.00 | 3’408.00 | 3’427.00 | 3’374.00 | 2’712.00 | 3’119.00 | 3’789.00 | 4’078.00 |

| IIFL | 3’865.00 | 3’912.00 | 3’790.00 | 2’914.00 | 2’910.00 | 4’037.00 | 6’195.00 | 9’125.00 | 13’149.00 | 16’228.00 |

| Federal bank | 6’360.00 | 5’962.00 | 6’524.00 | 7’228.00 | 9’301.00 | 15’816.00 | 17’316.00 | |||

| CSB bank | 2’958.00 | 3’799.00 | 6’131.00 | 6’570.00 |

| Gold auctions (in cr.) | FY13 | FY14 | FY15 | FY16 | FY17 | FY18 | FY19 | FY20 | FY21 | FY22 |

|---|---|---|---|---|---|---|---|---|---|---|

| Muthoot finance | 3’429.31 | 2’787.90 | 3’880.00 | 1’184.70 | 2’517.68 | 1’400.05 | 854.78 | 325.48 | 6’537.02 | |

| Manappuram finance | 1’301.30 | 2’284.70 | 1’188.00 | 1’932.00 | 929.00 | 1’204.50 | 419.40 | 116.10 | 412.25 | 3’615.13 |

| Bajaj finance | 6.29 | 18.79 | 231.12 | |||||||

| Shriram City Union | 50.21 | 17.85 | 32.48 | 10.42 | 3.07 | 0.37 | ||||

| IIFL | 139.51 | 120.03 | 309.90 | 2’114.90 |

| Auction % of AUM | FY13 | FY14 | FY15 | FY16 | FY17 | FY18 | FY19 | FY20 | FY21 | FY22 |

|---|---|---|---|---|---|---|---|---|---|---|

| Muthoot finance | 15.86% | 11.94% | 15.94% | 4.35% | 8.73% | 4.17% | 2.10% | 0.63% | 11.36% | |

| Manappuram finance | 13.08% | 28.02% | 12.82% | 19.17% | 8.35% | 10.26% | 3.24% | 0.68% | 2.16% | 17.93% |

| Bajaj finance | 0.40% | 0.84% | 11.29% | |||||||

| Shriram City Union | 0.38% | 0.10% | 0.01% | |||||||

| IIFL | 2.25% | 1.32% | 2.36% | 13.03% |

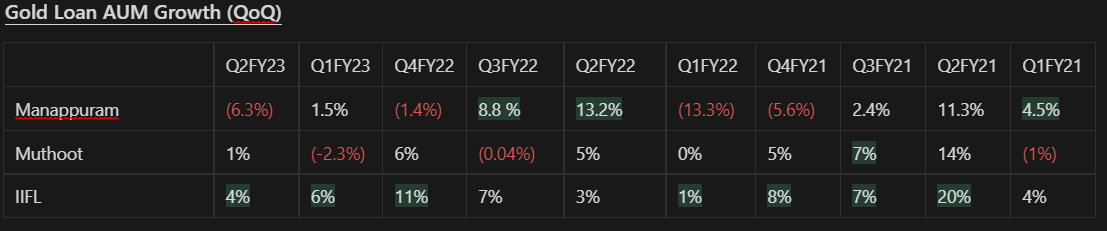

Auctions have gone over 10% for all cos which have reported nos. Auctions were highest for Manappuram followed by IIFL and Muthoot Finance. Banks are not obliged to share this data in their annual reports.

Disclosure: Invested in Manappuram (position size here, no transactions in last-30 days)

14 Likes

As a strategy, the analysts’ expect Muthoot/Manappuram to go back to their original segments, which should automatically uplift the yields irrespective of demand recovery or competitive intensity.

3 Likes

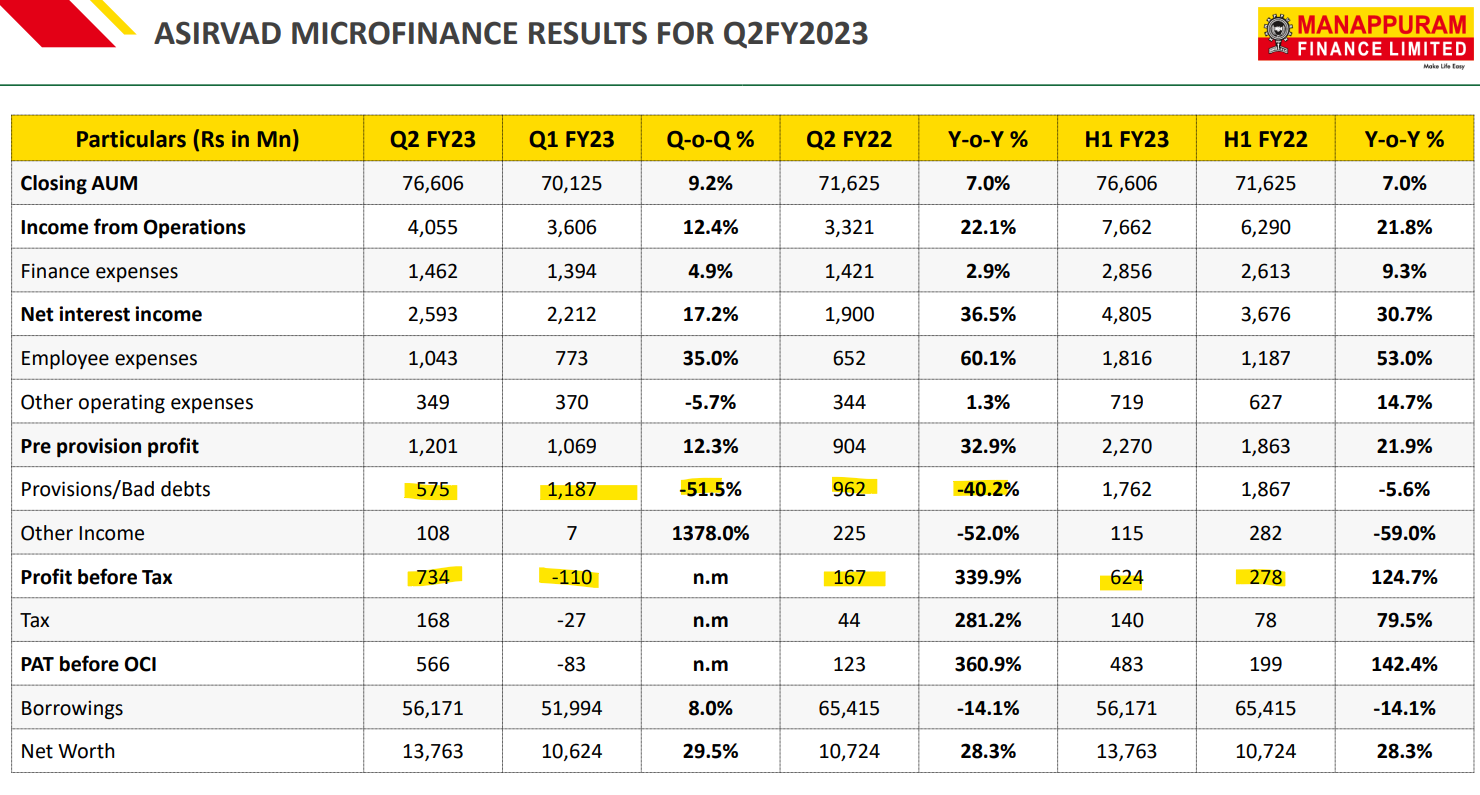

Ashirwad Microfinance

56 cr profit sept quarter vs 8cr loss in June quarter

It’s almost 20% profit addition to Manappuram

Expecting Manappuram consolidated profit should go up at least 20-30 % this quarter

It will drop PE from 7.9 to 6

Dividend yield 3%

It will bring Manappuram dividend minus PE to less than 4-5

It’s insane valuations

Looks like turn around in Ashirwad

12 Likes

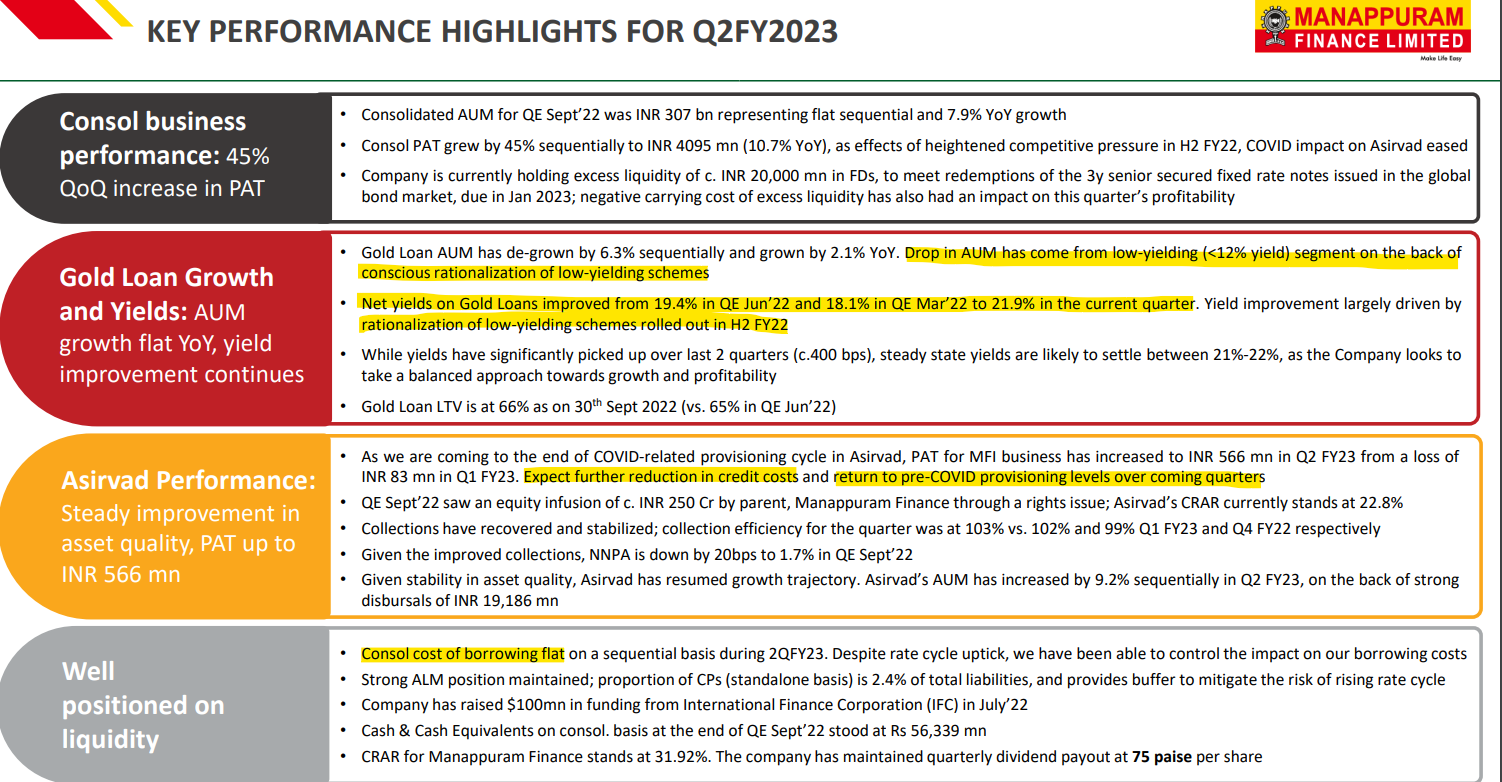

Overall decent results by Manappuram.

Rationalization of low-yield loans might be signs of competition intensity slowing down.

IIFL Finance still performing better in terms of growth among the three.

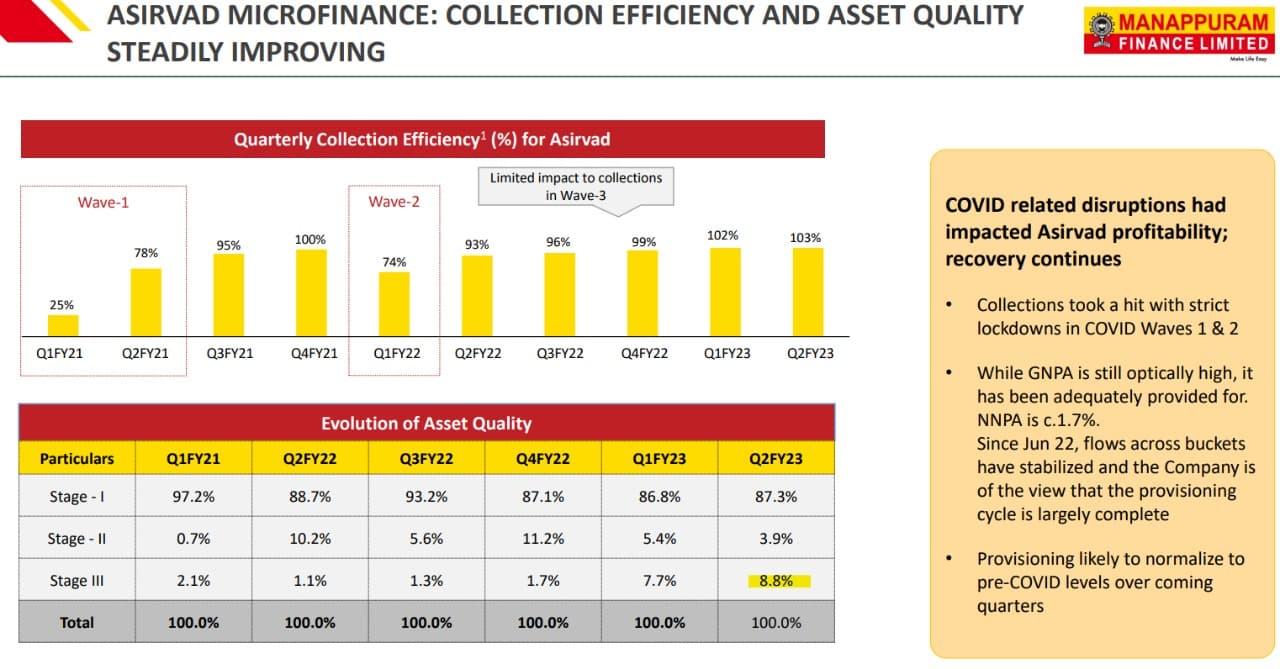

MFI business performed really well this time in terms of profitability as the provisions reduce. Sector facing tailwinds and have taken heavy provisions in previous quarters.

Need to monitor Stage 3 assets going forward:

14 Likes

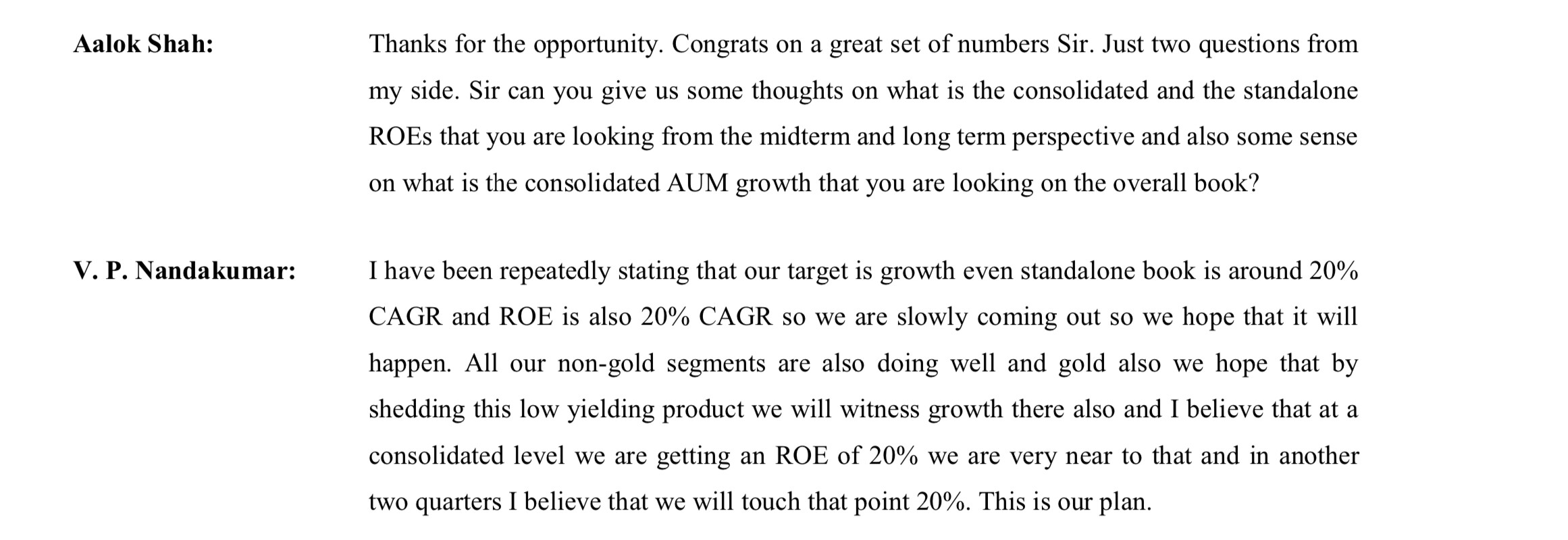

- management targeting 20% ROE and 20% CAGR consolidated growth ( this year AUM may grow 5-10% )

- slowly growth and yields coming up

-coming out as well diversified NBFC - Microfinance growing fast

- Ashirwad will contribute to gold loan

- free cash flow business

- 3% dividend yield

- PE 6

- almost at book value ( it means getting a high roe good growth business, established brand ,good management ,everything at no extra cost …free ,great bargain for those who believe in the story

… and we are missing something explanation by those who disagree with the story and don’t want to give more than book value to this business…

Let’s see which story becomes reality

- lets see by next year where the price goes and business grows

Gold business :I feel competition from public sector and private banks won’t last long ,as gold loan is a quiet tedious business with lot of operational issues .It’s better be handled by specialised NBFCs .

Demand is picking up so looks like next year will be much better

Non gold : growing steadily

Looks like eps will go upto 25 next year ,which will get the PE to less than 5

8 Likes

with FD rates going up banks are going to scale out of this gold loan business…

invested at slightly higer levels

3 Likes

I read in South Indian Bank concall that they want to focus out of gold loan and focus on their main business. This is the same thing muthoot and manappuram mgmt is telling.

Disclosure: Invested recently.

4 Likes

-Yah doing gold business for banks is not that easy operational point of view

-many banks tried in the past and couldn’t sustain the momentum and zeal for gold loans

-let’s see how long they will persist this time

-I feel banks will stop this aggression soon ,already they have slowed down

- also it’s quiet time consuming for customers to go to bank and take loans especially for those customers who are looking for short term loans

- I feel here we have risk benefit in our favour

5 Likes

VP nandkumar Q2

Switch towards high yields loans

Gold loan growth: post pandemic activities from lower pyramid have picked up and we will be able to catch up growth momentum

In past 5 years have are moving towards diversified loan company

Targeted consolidated 20% CAGR in growth and 20% ROE was not achieved due to pandemic but in coming quarters there is confidence that we will achieve 20% CAGR growth and ROE

Muthoot almost at its average PB of 2 ( range is 1 to 4.5 price to book )

manappuran

Manappuram trading 100% below its average PB of 2 Range is 0.8-3.2 price to book for Manappuram.currently Trading at lower band .

( muthoot financial and muthoot valuations are different ,while Ashirwad valuations are included in Manappuram so if in future Ashirwad demerges than it will be extra value)

3 Likes

Can you please tell from which site you got this data ?

From Screener website

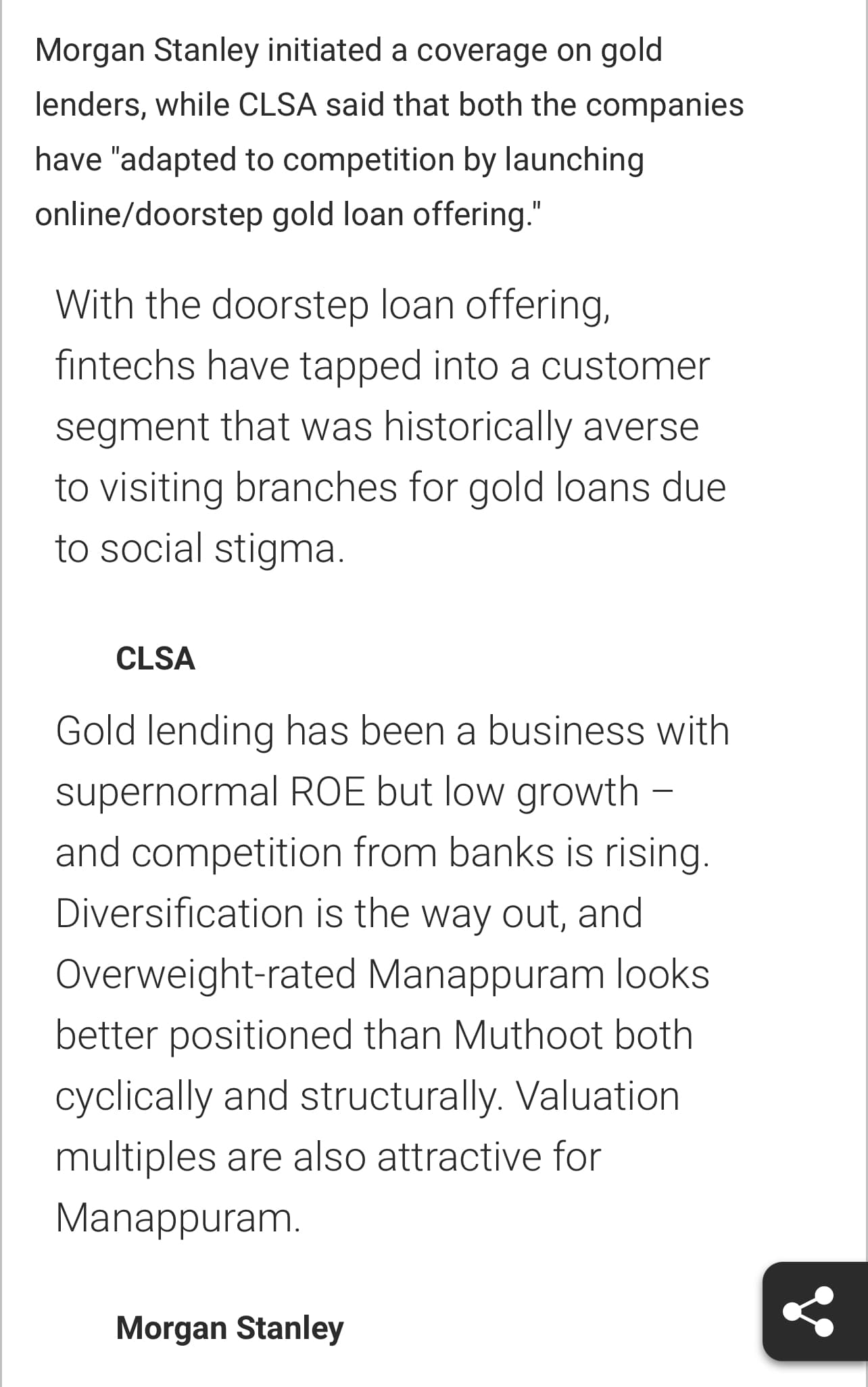

Specialised gold finance NBFCs like Muthoot, Manappuram Finance are the undisputed leaders in India’s gold financing business. Gold Finance NBFCs - Disruption Inevitable, But Long Term Story Intact: Systematix

Upbeat Outlook For Non-Bank Financiers | V.P. Nandakumar Of Manappuram Finance Upbeat Outlook For Non-Bank Financiers | V.P. Nandakumar Of Manappuram Finance | News News, Times Now

Shares of gold loan financers Manappuram Finance and Muthoot Finance rose as Morgan Stanley and CLSA upgraded the stocks. Why Morgan Stanley, CLSA Are Betting On Manappuram, Muthoot

upbeat on Manappuram due to

- diversification playing out

- multiple research reports buy call including Morgan Stanley’s overweight rating with 150 target

- very low price to book of 1.1 and price to earning of 6.8 according to current quarter eps of 4.8

- increasing yield

- turnaround in Microfinance

- increase in gold price

- management’s ability and past record in coming out of all diversities eg demonetisation,covid ,competition,yields issue

- free cash flow

- consistent good dividend

- Ashirwad Microfinance valuations not priced in current valuations

- crossing the moving averages

- 50% below it’s all time high

- good combination of technical and fundamental chart

- Nbfc as a sector is moving up with possible rerating on board with expectations of good growth in next 2 years

Muthoot has its separate muthoot finance service

But Manappuram has Ashirwad in its valuations ,it’s not separate like muthoot

But still Manappuram has lower price to book than muthoot

I feel opposite should happen and Manappuram should get more valuations than muthoot

Just my 2 cents

20 Dec

6 Likes

The company recently proposed a resolution to appoint the CEO’s daughter, Sumitha Jayasankar, as an additional executive director. It has been informed that it is with respect to the succession plans. She is a doctor by profession but has been part of the company before where she was the CEO of OGL.

What do fellow investors feel about it?

2 Likes

It’s good that it stays in family where she will keep getting the guidance

2 Likes

Not an apt comparison. We also need to look at margins generated by businesses when comparing them by book value.

Muthoot is 2x or more in those numbers to begin with. Book value will obviously be higher.

1 Like

Possible Let’s see ,but I feel sooner or later Manappuram will get higher book value than muthoot as it will grow faster than muthoot ,also ,it’s more diversified business

2 Likes