Has anyone heard of a company called macfos pvt ltd, i don’t know what is the connection between these 2 companies but whoever is thinking about investing in this, please check this angle also because this pvt ltd company is in the same business.

If you are referring to the Indiamart entry of Macfos (Macfos Private Limited - Manufacturer from Bhosari Midc, Pune, India | About Us), then it is referring to the the same company. The entry is old when it was not a listed entity.

No, it surely is not an old thing, a lot of companies who apply for refunds of gst through our firm, in their input details or annexure b for which they are claiming refund, i have seen name of a company named macfos pvt ltd, it is as recent as 1 or 2 weeks back. And these companies are mostly taking hardware supplies from this macfos pvt ltd.

I am neither invested nor interested in this company because of my lack of exposure to this hardware supply field. I can’t even feel like anything like this might be existing, thriving is a totally different matter. I am mentioning it here only because i thought i have gained a lot from this platform, so, i also should contribute to the community whether i am interested in company or not.

Please check this, this might be a mistake also from my end and those companies applying for refund also might be using its previous name, but being a bit careful won’t cost much.

3 Likes

preferential allotment

SAGEONE

FLAGSHIP

GROWTH 2

FUND - 465117

Equity

shares

SAGEONE

INVESTMENT

MANAGERS

LLP-

116280 Equity

Shares

Constituting 6.17% of the share capital

5 Likes

Sageone is a nice name, and its investment in the company is a welcome step. This investment shows the strength of business model of the company and integrity of the management. This is Sageone philosophy in a nutshell-

The company is issuing 5,81,397 shares [6.17% of the company] to Sageone at the rate of Rs. 430/- per share aggregating around 25 crores.

Issuance of shares has been on a slightly lower price, it could have been on slight premium to the market price.

But the fundamental question is as to what the management is planning to do with this capital? The founders have created this company with almost no capital. I am sure, with judicious use of this capital, the company can go much higher.

12 Likes

I have just been researching this company and want to hear the community’s opinion.

Management answers were generally good but then, i thought they were dismissing competitors altogether because of their “Solutions Provider” aspect. Does that mean they are primarily trying to focus on B2B channel and uses B2C as a lead generation platform? In that case, essentially the strategy is to replace SME company’s procurement and offer all products at a negotiated price?

If i understand the strategy right, is there really a number of electronics companies whom would repeatedly buy at scale?

The company started as E-com site, supplying both to retail and businesses. It is like cluster markets selling computer or electronics parts like Nehru Place in Delhi or Lamington Road in Mumbai. Then the company entered into branding and manufacturing of some components. Inhouse brands will command better margins.

Then the company entered into various services- PCB Manufacturing, Laser cutting, 3D printing, custom batteries. Further, they also started e-waste collection.

Thus we cannot have a pre-fixed model in such businesses moving in unchartered territory.

What does a customer look for?

Firstly they look for places when they can find all products. Thus, number of products offered by e-com operator becomes an advantage. Digikey offers 14 million products; Mouser, Arrow electronics, Farnell… they all have more than a million products forsale. Macfos have around 20k products, largest in India.

Secondly the customer looks for detailed technical specifications and data sheets for the products an e-com operator offers. Further they look for reliability and authenticity and quick shipping.

Digikey India Private Limited is there in India. I think they are the real competitor to the company. Lets us see how it goes.

3 Likes

Thanks for the good explanation, appreciate it.

Who really is their top customer profile? Will it be small-medium size business manufacturing and/or selling electronics in India?

1 Like

Does anybody have any idea, if the company has received the QIP money from the Sageone ?

The shareholding doesnot reflect yet.

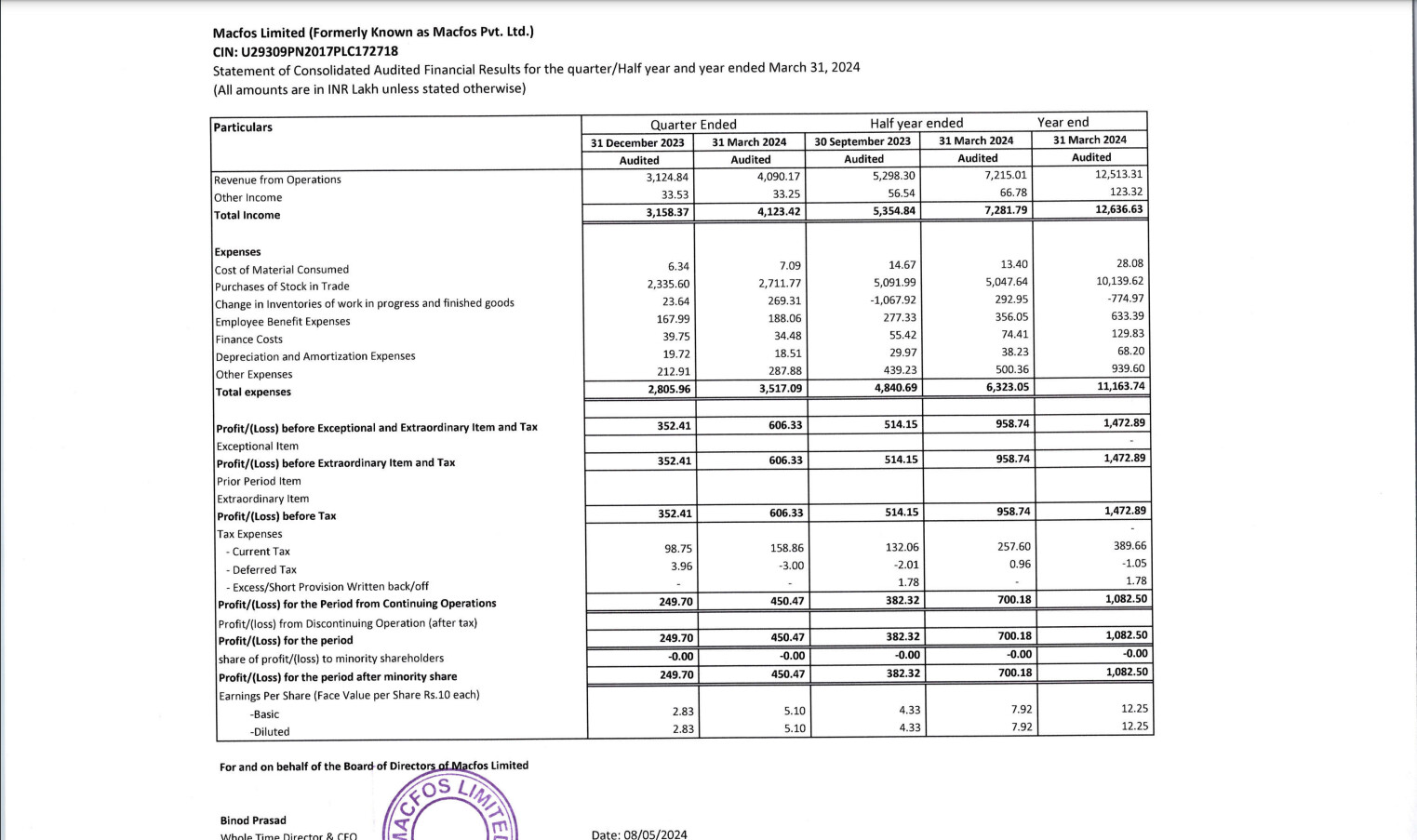

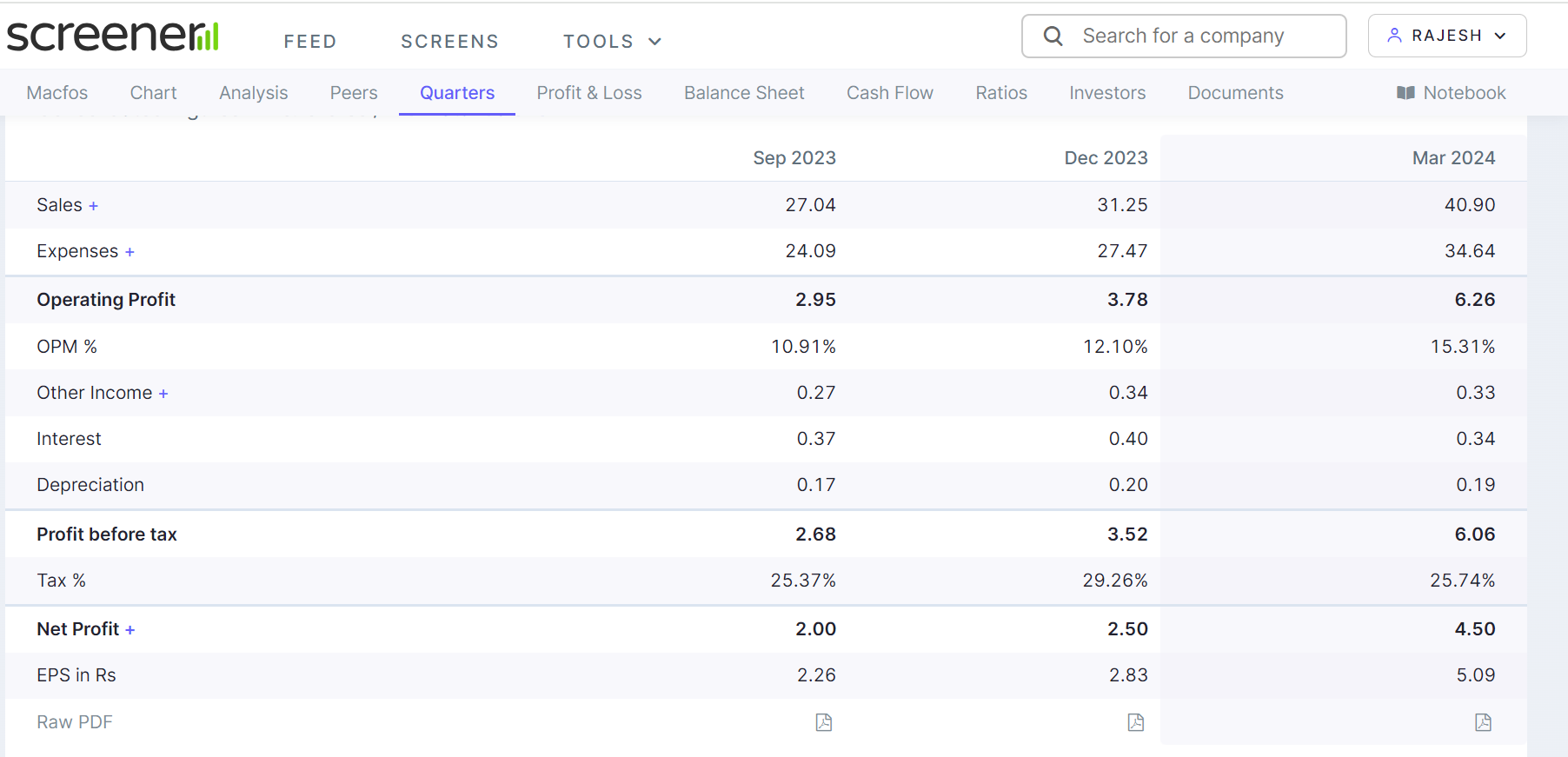

Disastorous revenue and profit figures. Last three quaters has not come even close to March 2023 numbers when it listed.

Does anyone know whats happened here.

Discl: Not Invested,

Can you please explain, result is good or bad…?

I don’t know what you consider as good & bad. Do one exercise, calculate & write the growth in the following fields between FY23 and FY24 : sales, expenses, OPM, PBT, PAT & EPS. That will help us to put some clear thoughts on if it’s good/bad.

1 Like

The result shown in the screenshot above compares the result of two quarters a year apart. So Jan-March 2024 has been compared with Jan-March 2023. Taken that way the company has experienced de-growth, which is bad.

Comparing the previous quarter (Q3FY24 vs Q4FY24) within the same financial year, the company has done good. But this is seasonality at play. Majority of the companies especially manufacturing companies, post their best quarter as Q4 of a financial year. Although, Macfos is not a manufacturing company.

As far as financial year comparison is compared i.e. FY23 vs FY24 is concerned, the company has done good and grown.

As an investor the de-growth that the company has experienced compared to last year’s quarter is a fly in the ointment, given that it is a microcap, expected to grow exponentially.

1 Like

Examining the annual results for 2023 reveals sales of 80 Cr and a profit of 7 Cr. However, when focusing solely on the March quarter, sales and profits are reported as 72 Cr and 7.93 Cr respectively. This scenario seems implausible as it suggests the company generated nearly all its sales and profits within a single quarter, which is unlikely. Therefore, it appears that the data presented by the screener is inaccurate. Despite this discrepancy, the company has demonstrated decent growth, evident in its annual performance.

That data also highly likely has some problem. Company did 80 cr. revenue in full year of FY23, highly unlikely that 72 cr. of that was done just in Q4’23.

Earlier the company was declaring half yearly results, now they are declaring quarterly results. The results has been excellent. Thus, some data services are comparing halfyearly results to quarterly results.

The company is growing at the rate of above 50%, with great margins. Recently they have also received a capital of Rs. 25 crores from Sageone for 6% stake, I hope the management will deploy the capital judiciously and does great.

9 Likes

MANAGEMENT PERSPECTIVE

As we look ahead, we foresee growing demands for our products and are confident in sustaining our current growth trends in Revenue and Profitability.

Investor Presentation is here :

2 Likes

The company is coming out with quarterly results on 29.07.2024.

33878031-7cc2-43ee-8dd0-d5ac1436f0c1.pdf (506.9 KB)

In the March quarter they did a topline of around 41 crores, with a net profit of 4.5 crores. I don’t see any seasonality in quarterly results, and thus we can expect a net profit of around 5 crores in Q1-2025. We can conservatively expect a net profit figure of 20 crores in FY 2025. Thus at present Mcap of 695 crores does not look exorbitantly overvalued on FY 2025 estimated earning.

Any views?

2 Likes