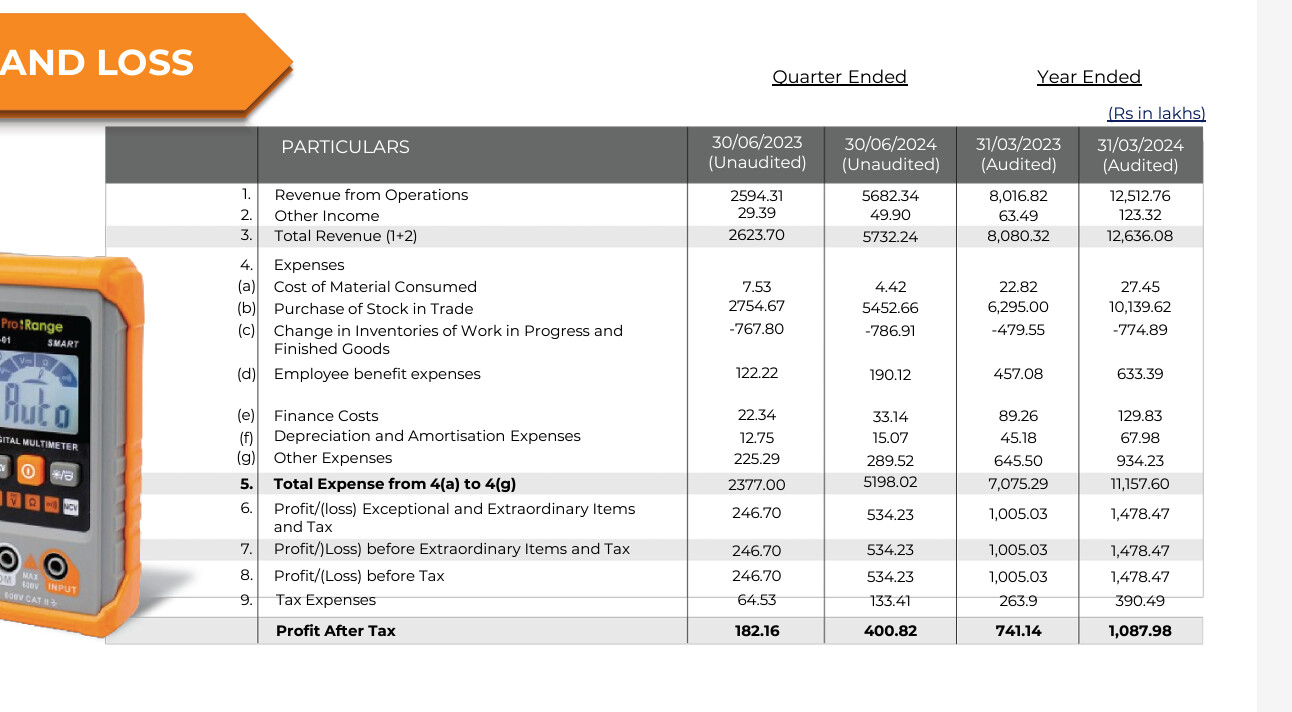

Macfos has come out with excellent results. Topline has gone up to 56 crores, 40 percent growth on quarter to quarter basis. Profit has gone up almost 100 percent as compared to last year same quarter.

8d171879-b6d2-444d-ab9b-d44aba3ba0fb.pdf (2.8 MB)

2 Likes

Dear Shareowners,

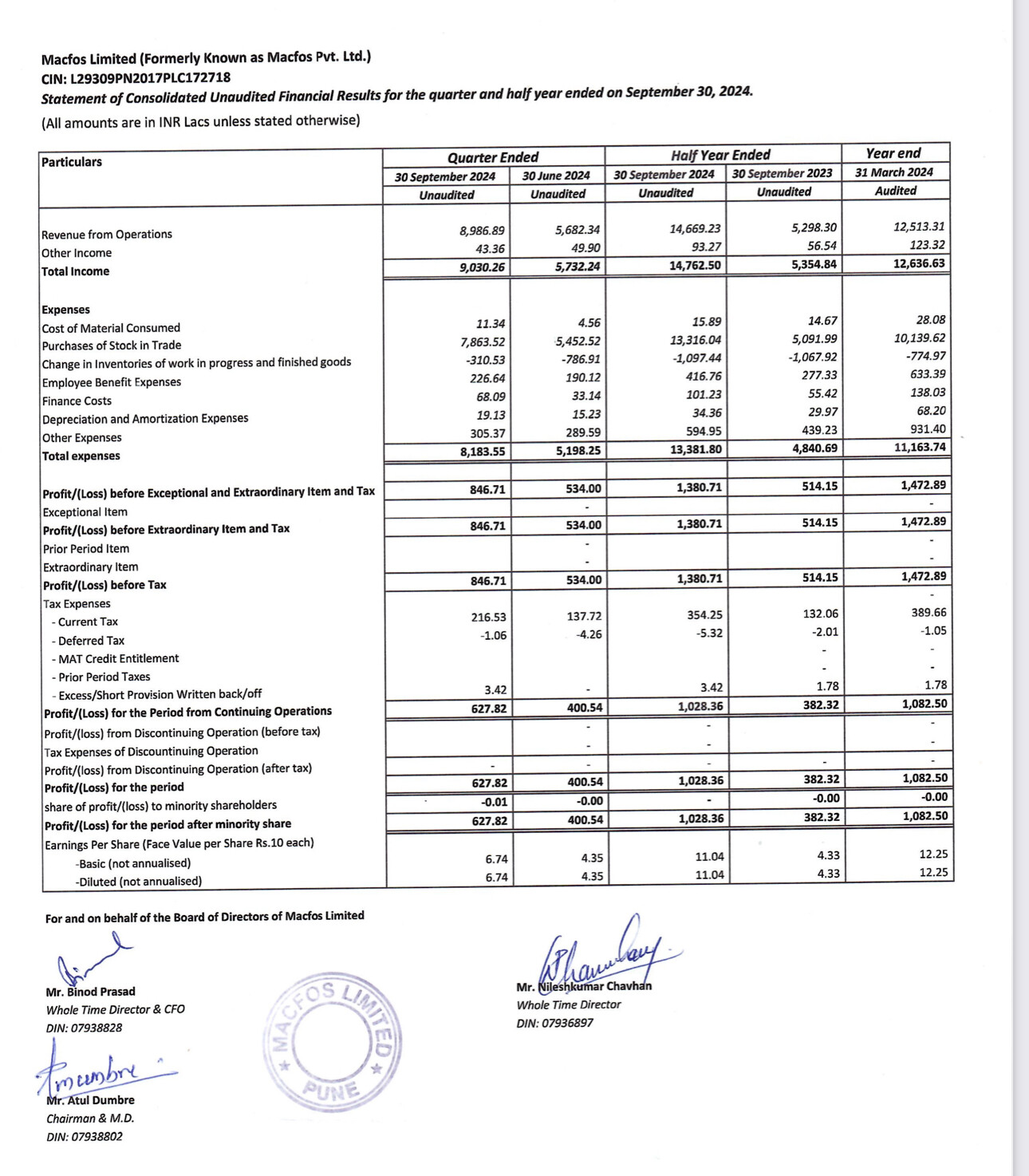

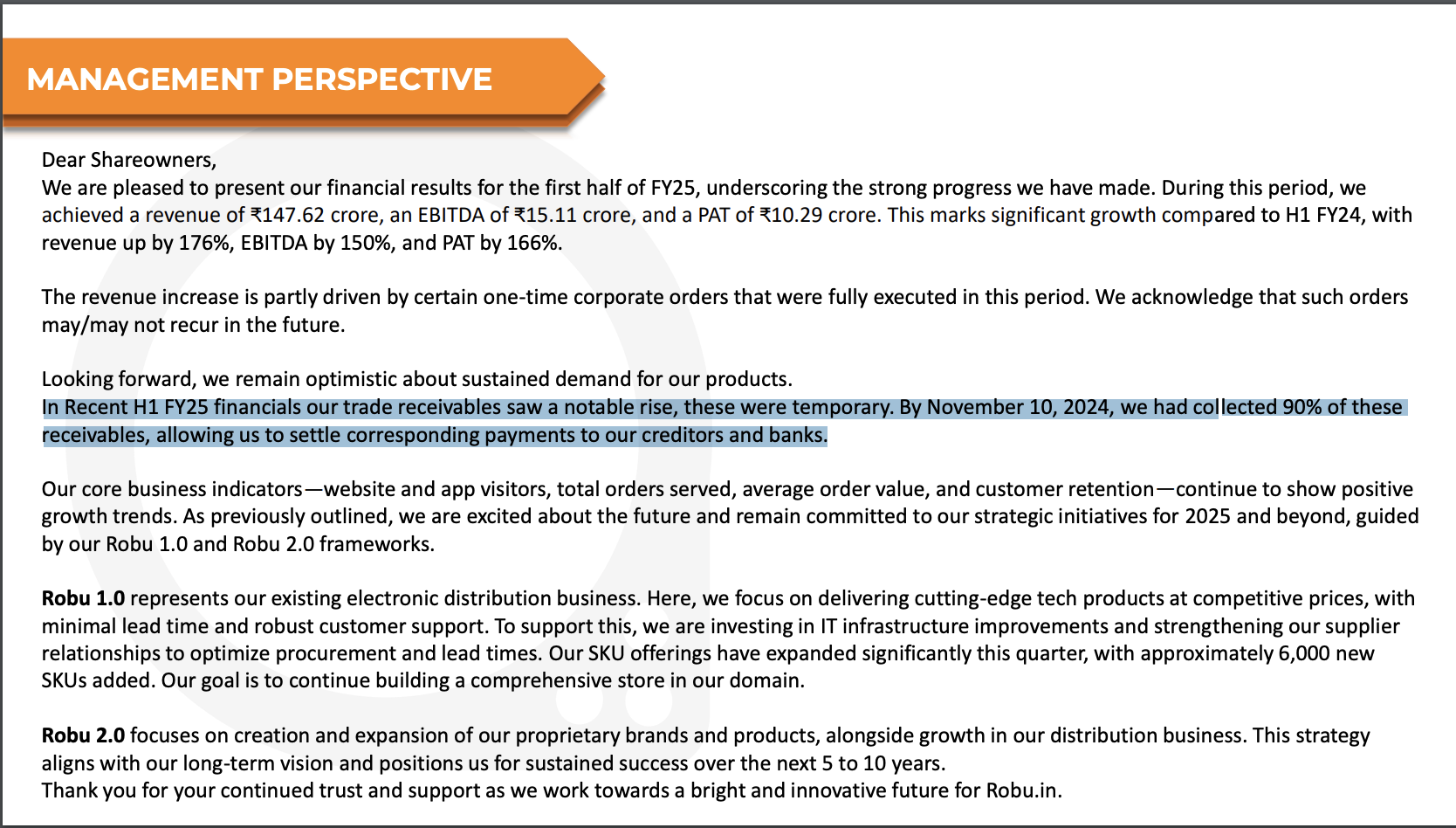

We are delighted to share our Q1 FY25 financial results, highlighting our strong performance during this period. We recorded a revenue of 57.32 Cr, an EBITDA of 5.82 Cr, and a PAT of 4.01 Cr. This represents a significant growth compared to Q1 FY24, with revenue increasing by 118%, EBITDA by 107%, and PAT by 120%. We achieved a revenue of 57.32 Cr, exceeding our internal forecast of 40 Cr. This increase is primarily attributed to several non-recurring orders, which may or may not occur again in the future. Traditionally, our Q1 revenues (current year) are lower than Q4 (previous year). However, we have observed sustained demand, resulting in steady growth for our business. Looking ahead, we anticipate continued strong demand for our products and are confident in maintaining our YoY growth trends in both revenue and profitability. Again, our key business metrics such as website & App Visitors, Total orders served, Average order value, and repeat customers continue to exhibit positive growth.

As highlighted in our previous communications, our outlook for 2025 remains optimistic, underpinned by two requirements and bring in more focus. key strategies: Robu 1.0 and Robu 2.0. These strategies are now addressed separately to cater to their individual ROBU 1.0 represents our existing electronic distribution business, where we are dedicated to offering new tech products at affordable prices with minimal lead time and exceptional customer support. We prioritize enhancing our IT infrastructure for better efficiency and have bolstered supplier relationships to optimize procurement costs and lead times. Additionally, we have expanded our SKU offerings (this quarter we have added approximately 6000 New SKU’s) and focusing on Government/Corporate Customers. ROBU 2.0 is centered on creating and developing more of our own brands and products while expanding our current distribution business. This strategic direction positions us favorably for long-term success, aligning seamlessly with our goals for the next 5 to 10 years

Disclosure: Invested

8 Likes

If you have views regarding anything that pertains to the business or the stock, you can share them for the benefit of all who are invested or interested in the company, not necessarily data-backed, even quantitative will suffice, but do not make comments like these, particularly when someone is experienced and has been an active member and who has introduced many businesses to the forum.

Members are optimistic about the businesses they are invested in, even to the point of being biased, that is it. Sometimes they might have certain exclusive views, information, which are not available in the public domain, but that doesn’t make them anything else than what they are, investors. He started the thread, he follows the business, he has his views and presented them. If you have a different view, do share, it helps.

It seems, you are new to the forum, so saying this.

6 Likes

Sorry if was offensive, he was explaining all the quarterly results so I thought he might be company person. I am new to this forum, only been here from last week. But I have a question how would I distinguish “related parties” from others.

I have also invested in this company and looking for long-term holding. I also appreciate the efforts by @rk1771 for keeping up this thread.

I have a question on how much is dependence to China and Taiwan. There is a lot of speculation that China will attack Taiwan within next few years. How much will this affect the company in that scenario, if you guys have some analysis or knowledge please share.

Podcast of founder Atul Dumbre:

An In-Depth Conversation with Atul Dumbre: The Visionary Behind Macfos Ltd (Robu.in) (youtube.com)

4 Likes

High profitability of Macfos is attracting competition.

https://nsearchives.nseindia.com/corporate/DRONE_02092024134722_DroneHubOnline.pdf

Quote “Drone Destination has launched a new e-commerce Drone Hub platform offering drones, drone parts and consumables, avionics and BIS-approved drone batteries for the drone industry. This new business vertical shall ensure timely supply-chain support to the Indian drone eco-system and offer customers with efficient after-sales service.”

6 Likes

Flying a drone is not that easy in India. If drone weight is more than 250gm it requires license in India from DGCA.

Apart from that most of the practical drones are not affordable in India, such as agricultural drones cost more than 4-5 lakhs, most farmers in India can’t afford such a thing which is expensive than a tractor.

It’s still impressive to see such growth with such hurdles. Maybe it will succeed through rental services such as drone cameramen in marriages.

2 Likes

4 Likes

The receivables have now become almost 68% of the total consolidated revenue (62 crs out of 90 Crs consolidated). This is a big red flag to me. Can someone elucidate why receivables might not be a terrible thing in such a business?

Discl: Tracking for now. Was invested in a short position a while ago.

7 Likes

Yes, trade receivable has gone up. We need to examine this aspect.

They have two verticals- B2B and B2C. In B2C business, receivable must not be very high, but it can be substantial in B2B part. Looking at TTM sale figure of around 210 crores, 60 crores receivable is not very high though substantial. As an investors, we will certainly prefer a better working capital cycle.

Margin appears to be a tad lower as compared to last year results, may be B2B business has contributed more.

Still, looks like a great number. This year they can very well generate a net profit of around 25 crores.

4 Likes

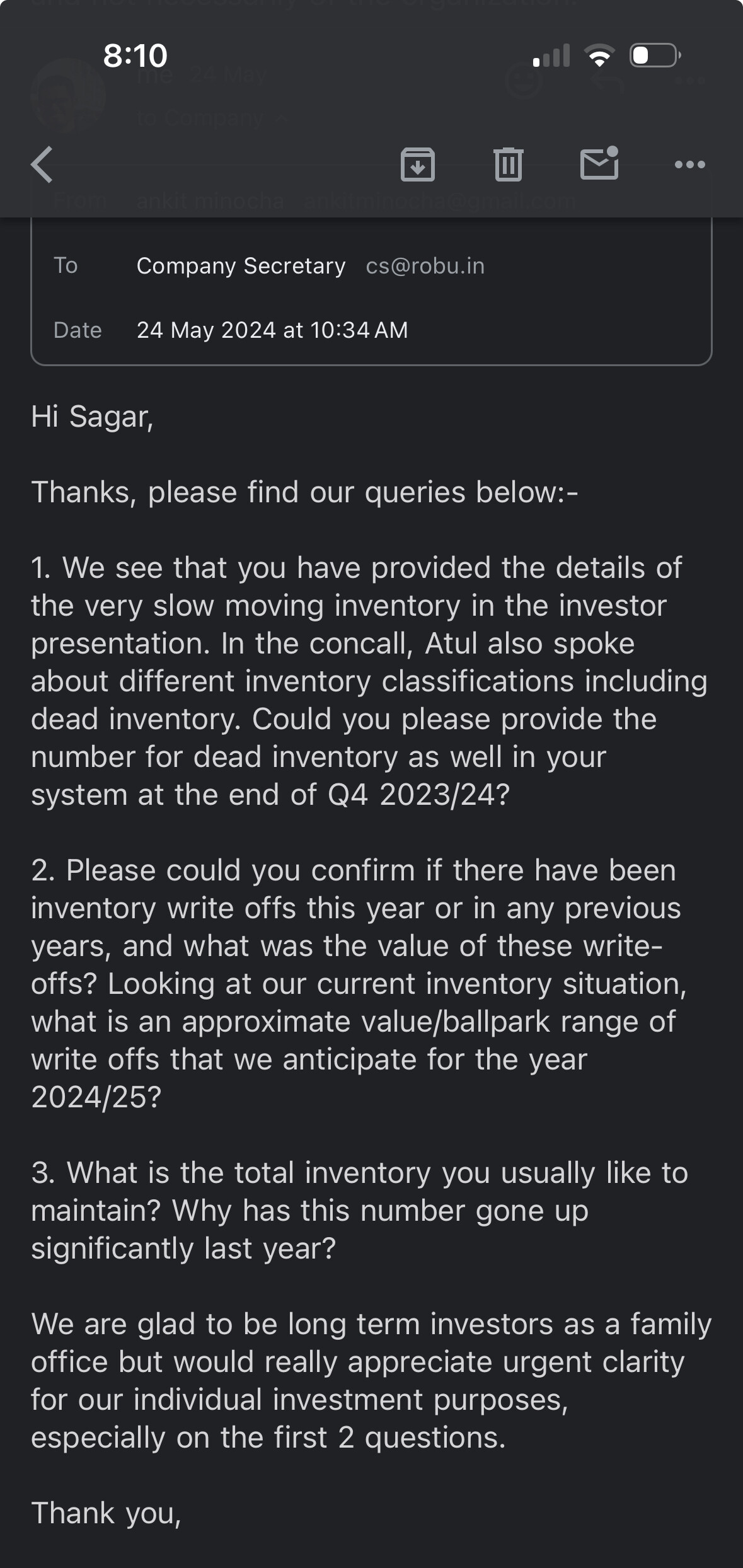

Agree that trade receivables seem to be of concern. Additionally post last concall, we had some concerns on inventory and had written to the management in end May 2024 to clarify this.

Despite an initial response, post the questions and a few follow ups we did not get a response. Basis the same, decided to exit the investment due to lack of clarity.

Mail screenshot below.

Disclosure : Were invested till this mail communication but have now exited positions

1 Like

i think such uptick in trade receivables are okay since they are in the growth face… especially B2B side…

next few results are very critical

3 Likes

Thank you for your explanation, I really appreciate this insight.

I have a slightly critical view though, I don’t think one can compare current quarter receivables to the TTM sales (when receivables were in tighter check). That way, you’re essentially saying that “Receivables aren’t a major issue right now because they haven’t been high with respect to past performance”.

Since 2/3rd of the payment hasn’t even been received this quarter, I don’t think one can be comfortable with the company doing 25 crores of net profit (when 6 Crs of money hasn’t even hit their bank).

I agree that it is very likely that entirety of the 62 Crs of receivable revenue has shifted to B2B. That itself changes the valuation dynamics, since by company’s own admission, their margins are 3/4ths of their margins for B2C. I’m not even thinking about other considerations such as client concentration (for example, what if the vast majority of that 62 Crs was owed from a single client?). I guess I’ll wait for the concall to clarify things.

Thanks once again for engaging in discussion. Really nice perspective from your end.

4 Likes

Hello,

Would anyone who was able to attend concall be kind enough to summarise it pls

Key qn i had was receivable and business direction/guidance etc…

Hi management commentary on receivables. That they have collected 90% of the receivables mentioned in financial statements

4 Likes

A nice investor presentation:

- No. of visitors are growing on web/app.

- Number of orders are growing.

- average order value is growing.

- Total SKU has reached more than 30K.

A nice read.

1586ba43-9e8f-49a9-bd4f-8328dba3a65d.pdf (4.3 MB)

3 Likes

Initial exuberance of results faded a bit after earnings call as management mentioned that 50 cr is one of bulk order. Regular business has grown to 76 with 50/50 division between ecommerce and sales team led. This is a growth of 43% YoY in regular business.

6 Likes

Highlights of Concalls

1. Financial Performance Highlights:

- Revenue: Achieved ₹147.62 crore in H1 FY25, a 176% increase compared to H1 FY24.

- EBITDA: ₹15.1 crore, representing a 150% growth.

- Profit After Tax (PAT): ₹10.29 crore, showing a 166% increase.

- A portion of the revenue growth is attributed to one-time bulk corporate orders. Excluding these, regular business revenue grew by 43% YoY (₹76.3 crore in H1 FY25 versus ₹53.5 crore in H1 FY24).

2. Key Business Updates:

- Bulk Orders:

- The bulk orders contributed significantly but are non-recurring.

- Receivables from these orders were largely settled (~90%), mitigating risks.

- Core Business:

- Focus remains on steady growth in the regular business, with key metrics (e.g., customer retention, order volume) showing improvement.

- The Robu 1.0 strategy (electronic distribution) and Robu 2.0 strategy (proprietary brands) are driving the business forward.

- SKU Expansion:

- Added 6,000 SKUs in H1 FY25, aiming for a comprehensive product range.

3. Strategic Directions:

- Continued focus on balancing risk and opportunity while pursuing one-time bulk orders.

- Long-term growth vision under “Robu 2.0”, focusing on proprietary products.

- Enhanced IT infrastructure and supply chain to support scaling.

4. Operational Insights:

- Revenue Mix:

- Approximately 50% from retail (e-commerce) and 50% from B2B.

- Procurement:

- 90% of goods are imported, mainly from China and the UK.

- Growth Drivers:

- Demand from startups, government policies like “Make in India,” and increased adoption of electronics in daily life.

- EBITDA Margins:

- Maintained around 8–10% PAT level despite one-time bulk orders slightly impacting margins.

5. Management Comments and Outlook:

- Optimistic about industry growth over the next 5–10 years, supported by increasing electronics penetration and supportive government policies.

- Regular business growth is on track, with stable operational metrics.

- No specific revenue or margin guidance provided, emphasizing a focus on consistent performance and scalability.

6. Questions and Responses:

- One-Time Bulk Orders: Addressed extensively but without client/industry specifics to maintain confidentiality.

- Margins and Receivables: Explained the impact of bulk orders on financial metrics.

- Competitive Edge: Highlighted differentiation through technical know-how and post-sale support.

- Future Plans:

- Intends to list on the main board in ~3 years.

- Planning board expansions with industry experts.

2 Likes