Has anyone tried writing to them regarding the inter corporate loans/ deposits. There is a brief mention about it in a AGM recording available in their site, where they have made some vague remarks about it. They have mentioned that those are for certain future expansions and so.

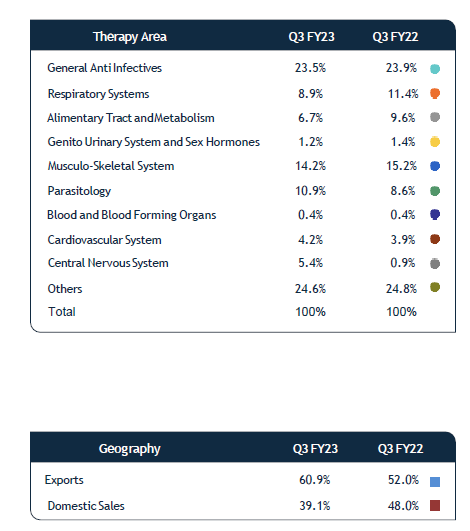

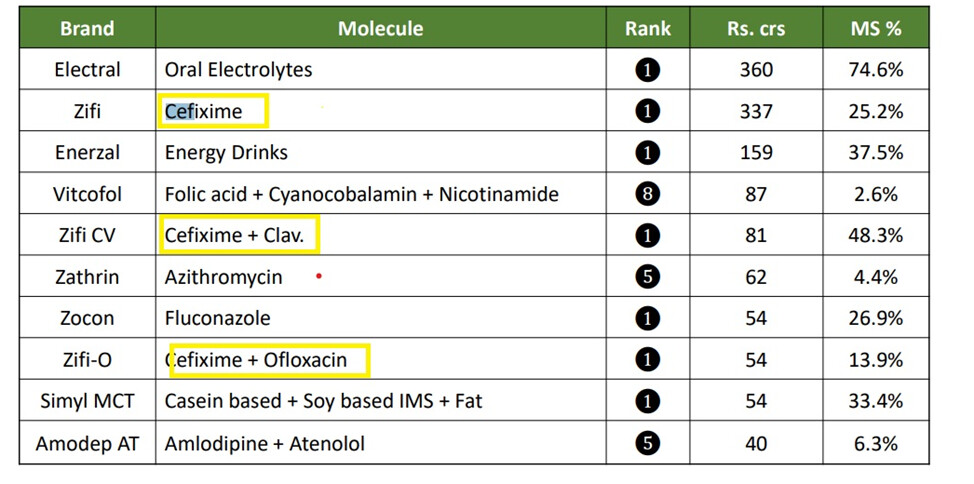

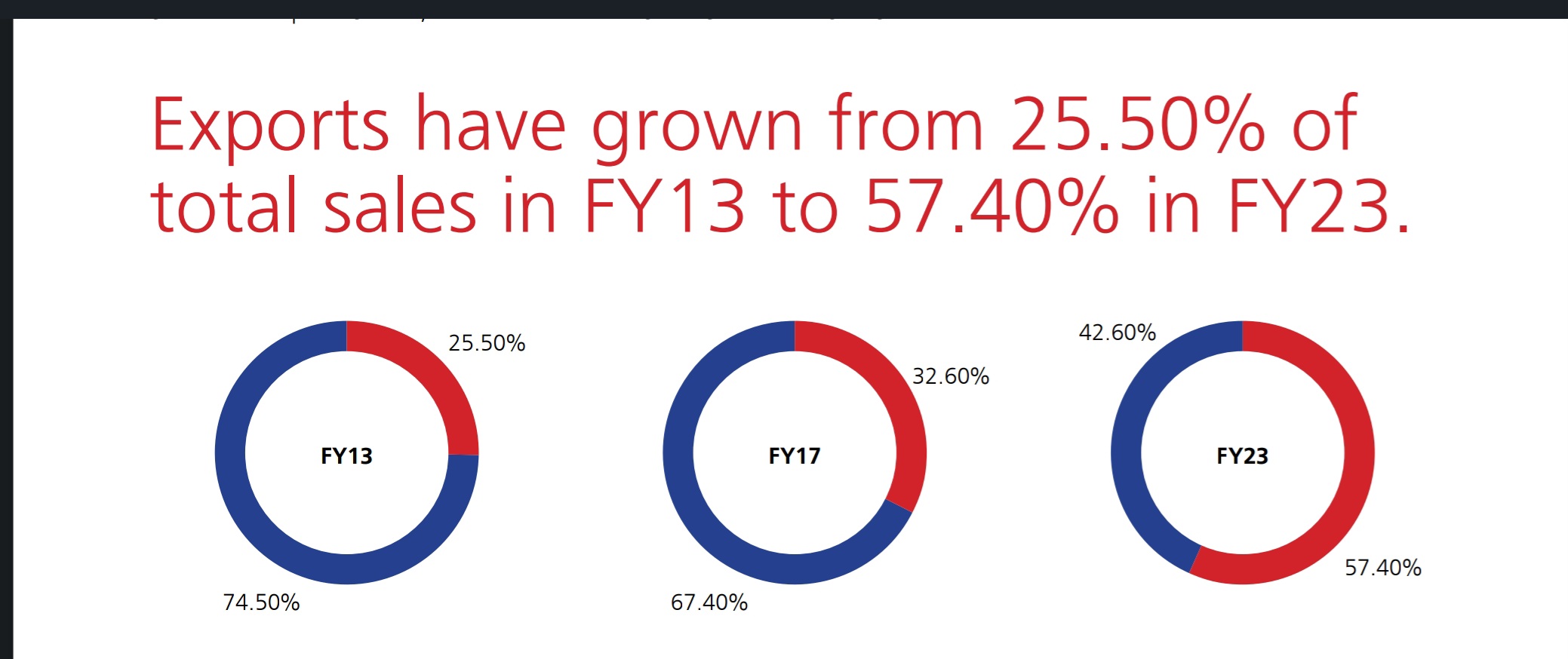

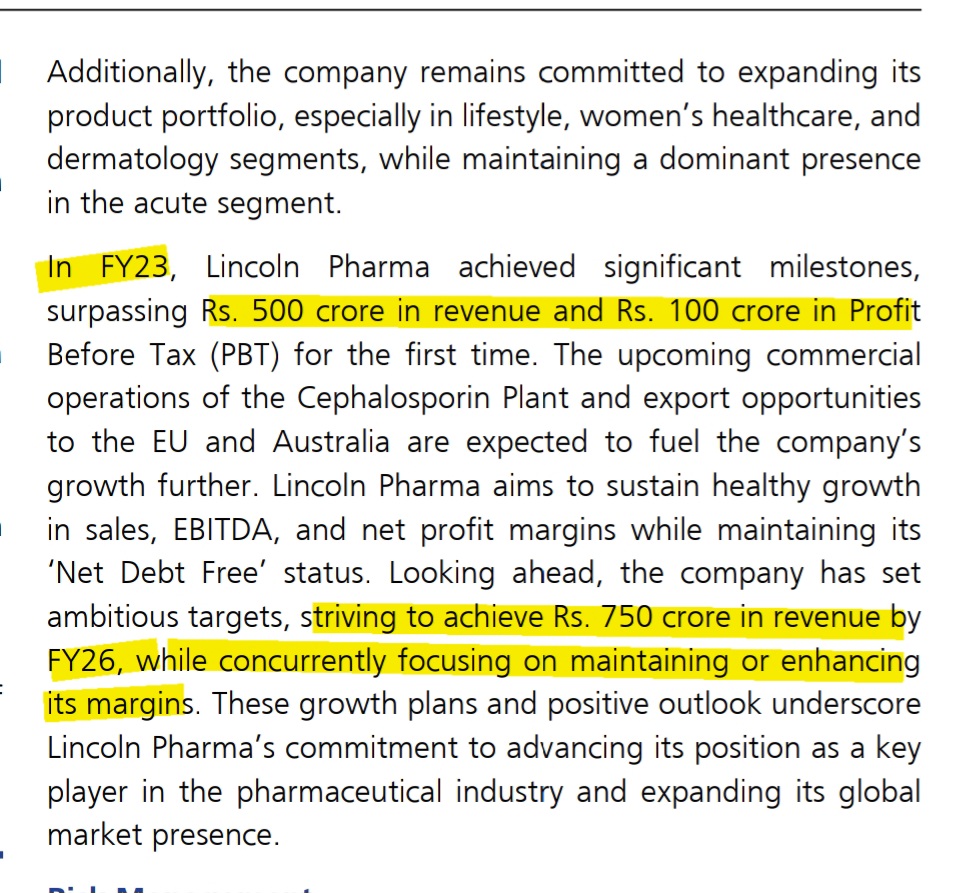

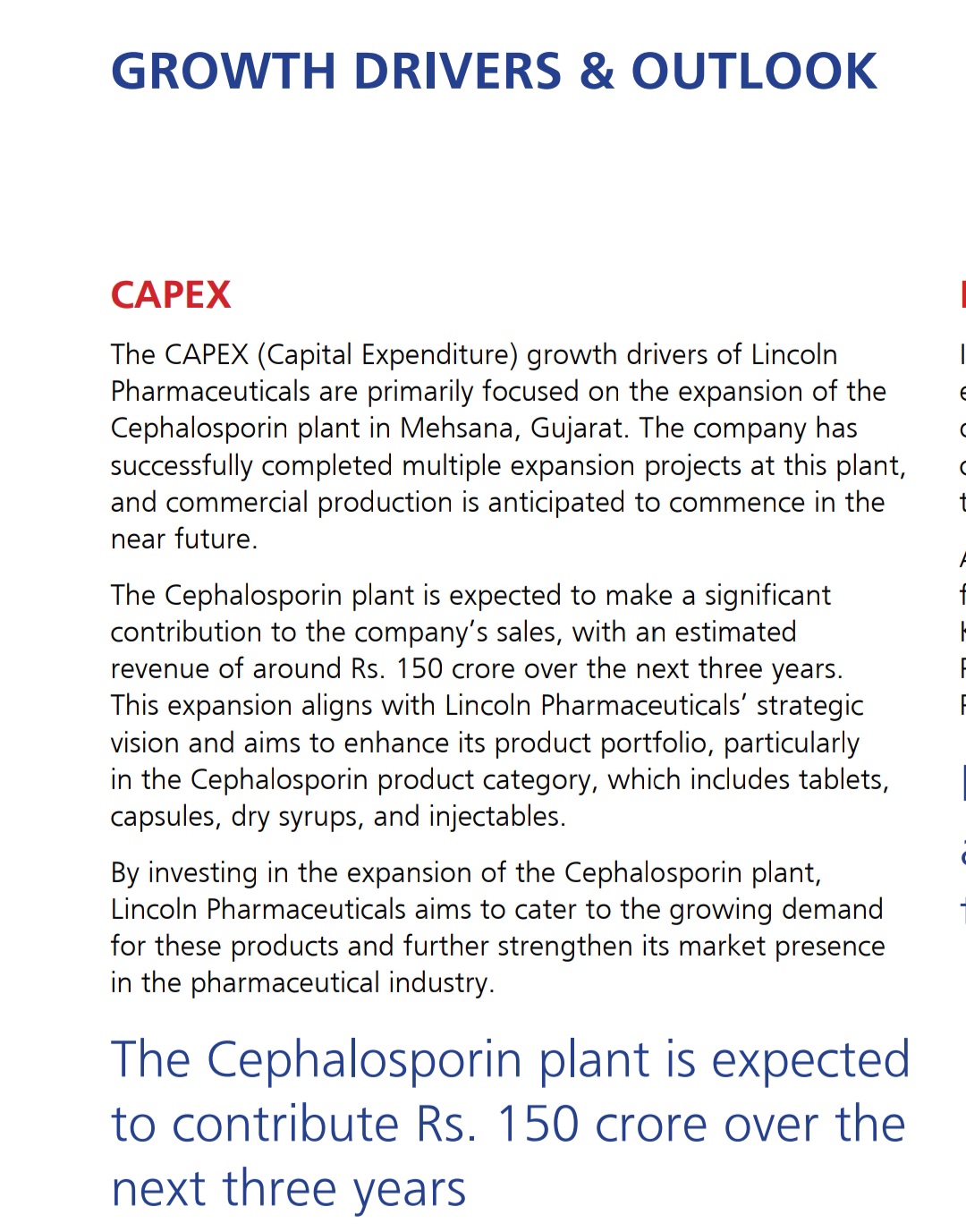

As far as business is concerned cephalosporin seems to be the near term growth driver. Export to EU and Australia to contribute to Growth. Exports contributed to 60 % of sales in Q3. Export network to grow to 90 + countries from the current 60.

Its interesting to see stable margins in a tough environment. Its good to see promoters increasing their stake in the company.

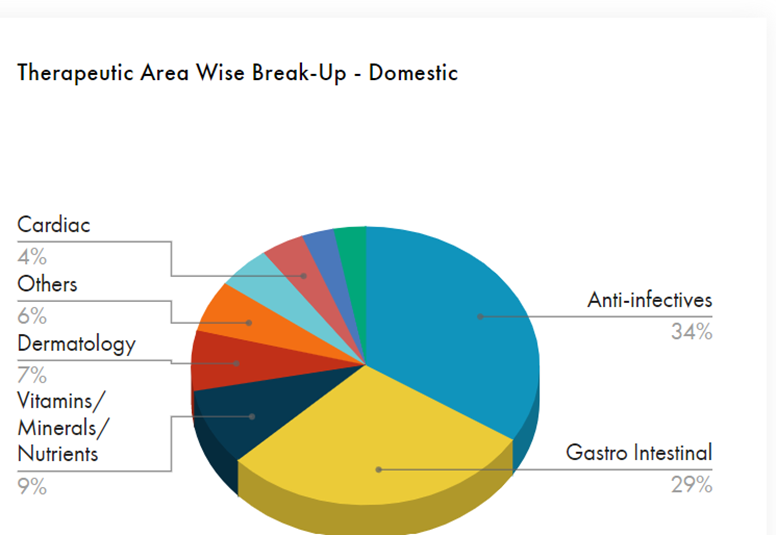

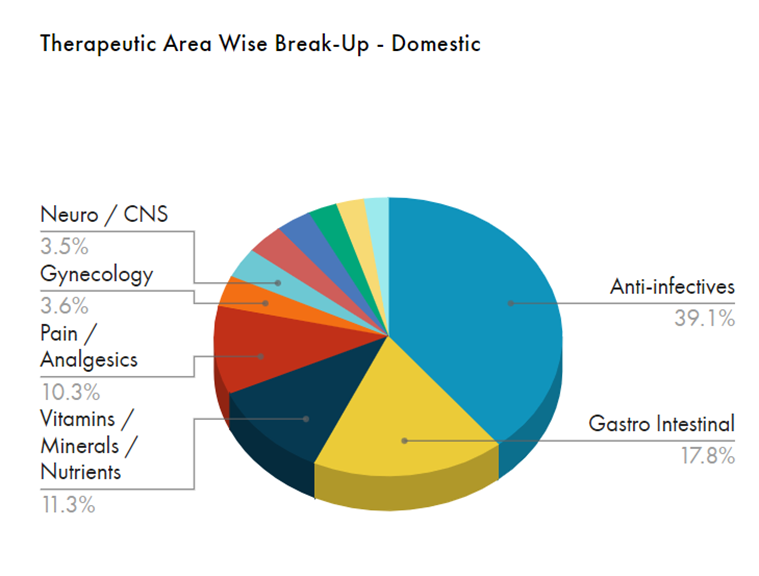

Sales contribution

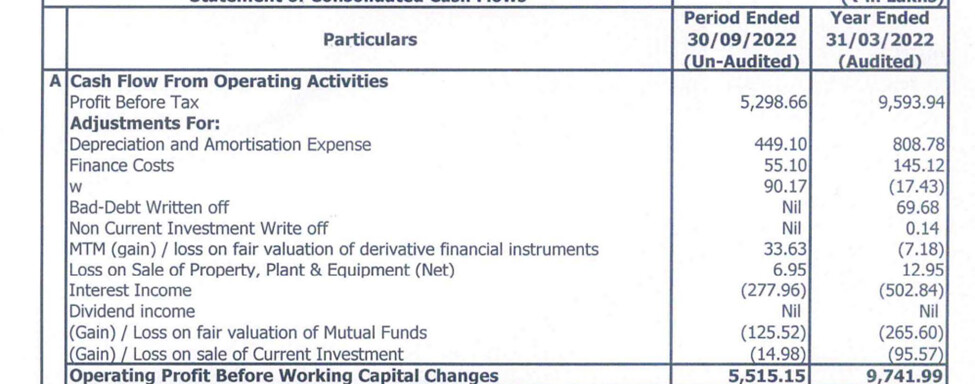

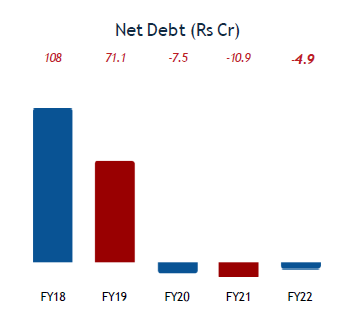

Company is net debt free

Cash equivalents

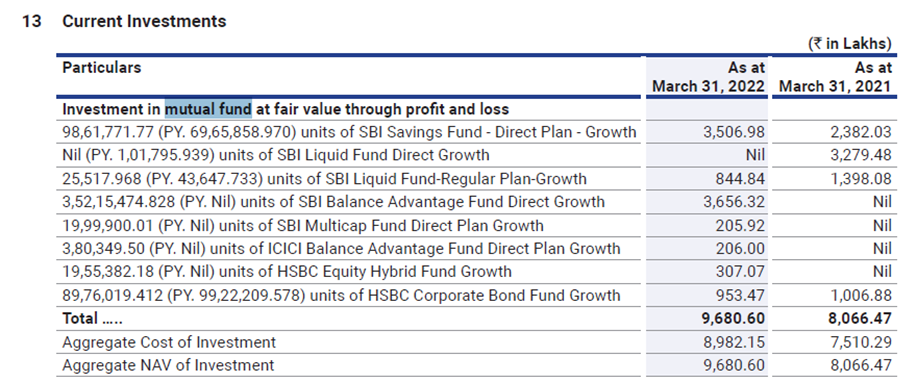

The company has cash equivalents of 21 crores and quoted investments of 101 crores as of Sept’22.

They had a current investment of 97 crores as of March’22.

As per AR’22, the following are the investments

So the cash equivalents and investments add upto Rs 61 per share as of Sept’22. These mutual fund investments are marked market to market and are liquid. I believe these can be considered very close to cash equivalents. If we consider these as cash equivalent the Enterprise value comes down further. If we exclude other income from the last quarter earnings and annualise it considering that earnings are sustainable. The current adjusted EV/ EBITDA will be 6.29 which seems to be cheap for a pharmaceutical company.

Key risks

- Regulatory risks: This is a risk common to all export-focused pharmaceutical companies. The Tanzanian government banned the company in 2016 due to some issues with its Chloramphenicol sodium succinate injection. An African Govt revoking its license could have a serious dent in its reputation. Now, that the company is getting approval from the Australian TGA and EU, I would consider these as issues of the past.

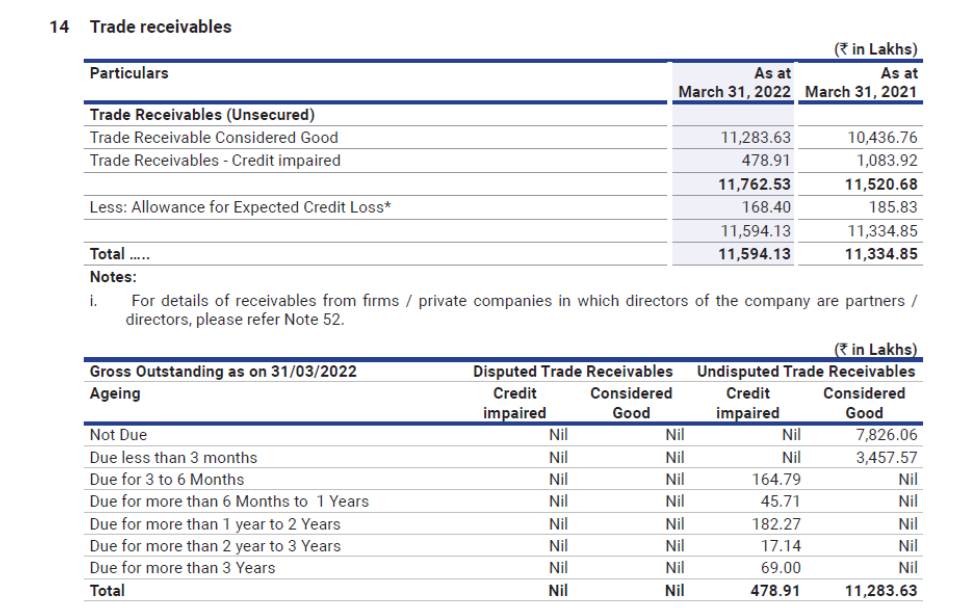

- Trade receivables:

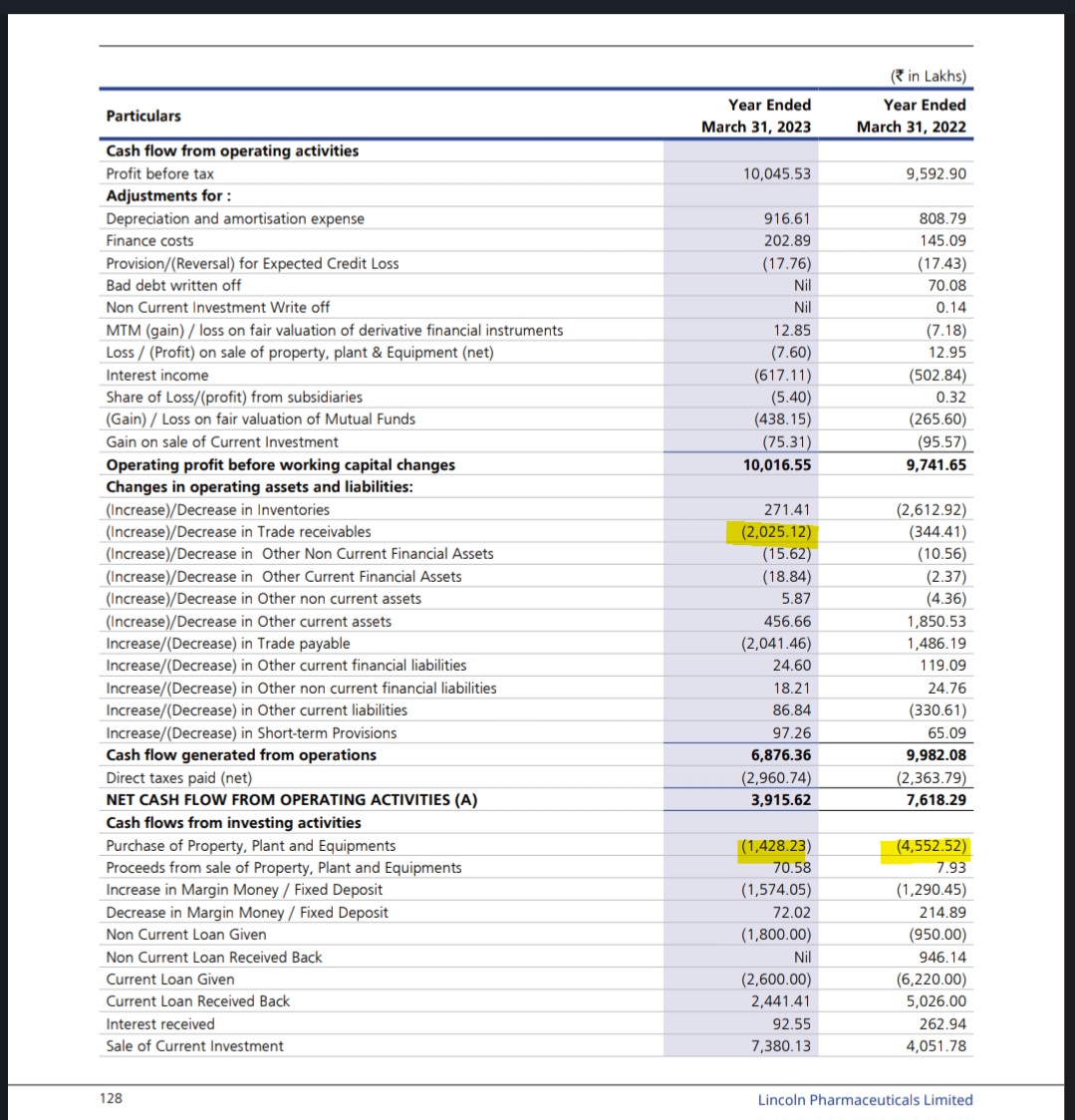

Trade receivables are seen continuously increasing over the past few years. In the HY, the receivables have increased from 116 to 174 crores. As the company exports to many African countries the recoverability of these receivables needs to be monitored.

The general credit period for both exports and domestic sales is 30 to 90 days. And the company marks all receivables beyond 3 months as credit impaired.

The company has significantly brought down the impaired receivables above 3 months considerably from 10.83 crores to 4.78 crores.

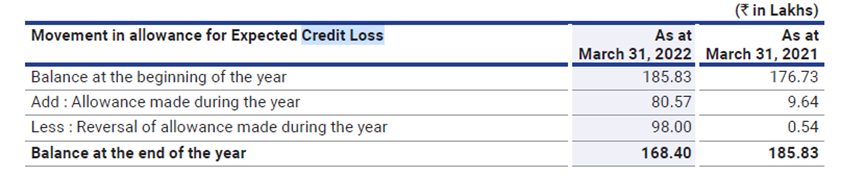

The company has a credit loss allowance of 1.68 crores for impaired receivables of 4.78 crores. The company made a reversal of 98 lakhs of bad debt allowance made in the previous years.

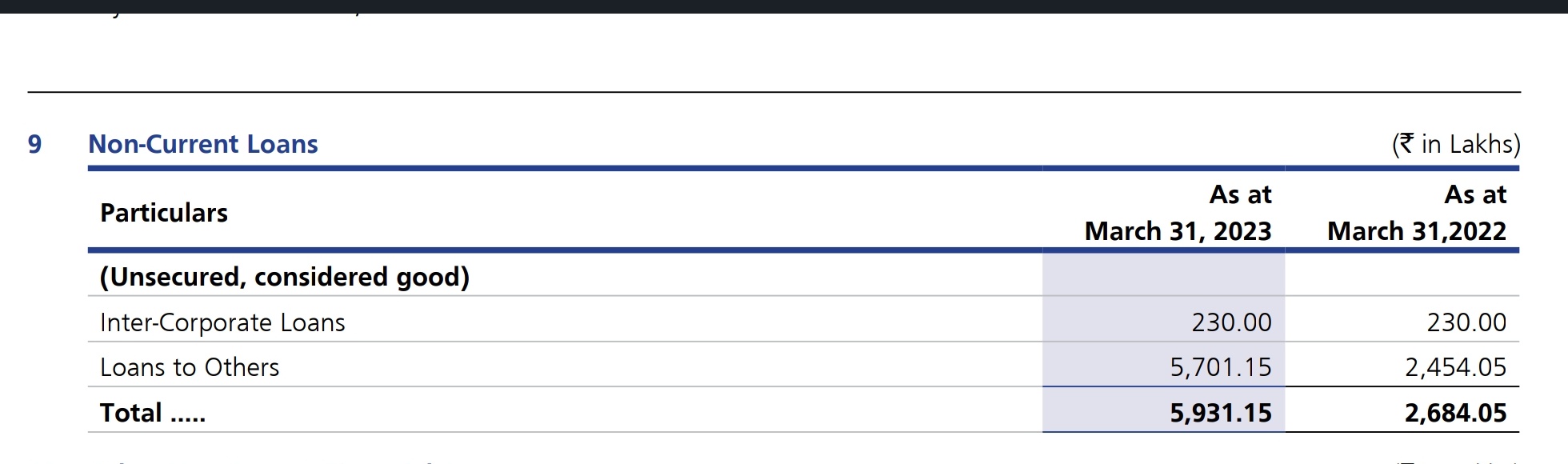

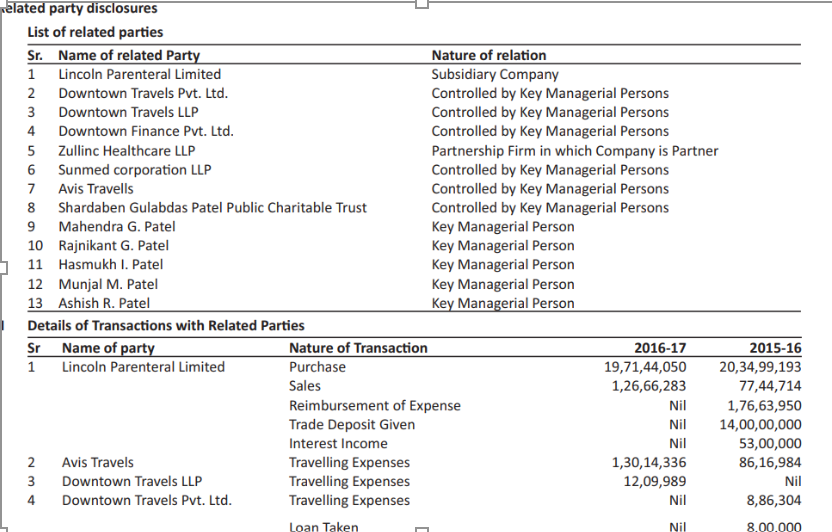

3)Intercorporate deposits:

There are large amounts of loans and advances. As per AGM recording, there was a vague mention that these deposits are charged interest and are given as part of certain expansion plans. There are not many details regarding these intercorporate deposits.

As on Sept’22 :

Non-current: 29.85

Current: 25.63 Total: 55.48

As on 31.03.22:

N: 26.84

C:31.77 Total: 58.61

As on Sept’21:

N: 27.11

C: 36.75

Total: 63.86

As on March’21:

N: 25.09

C: 18.78

Total: 43.87

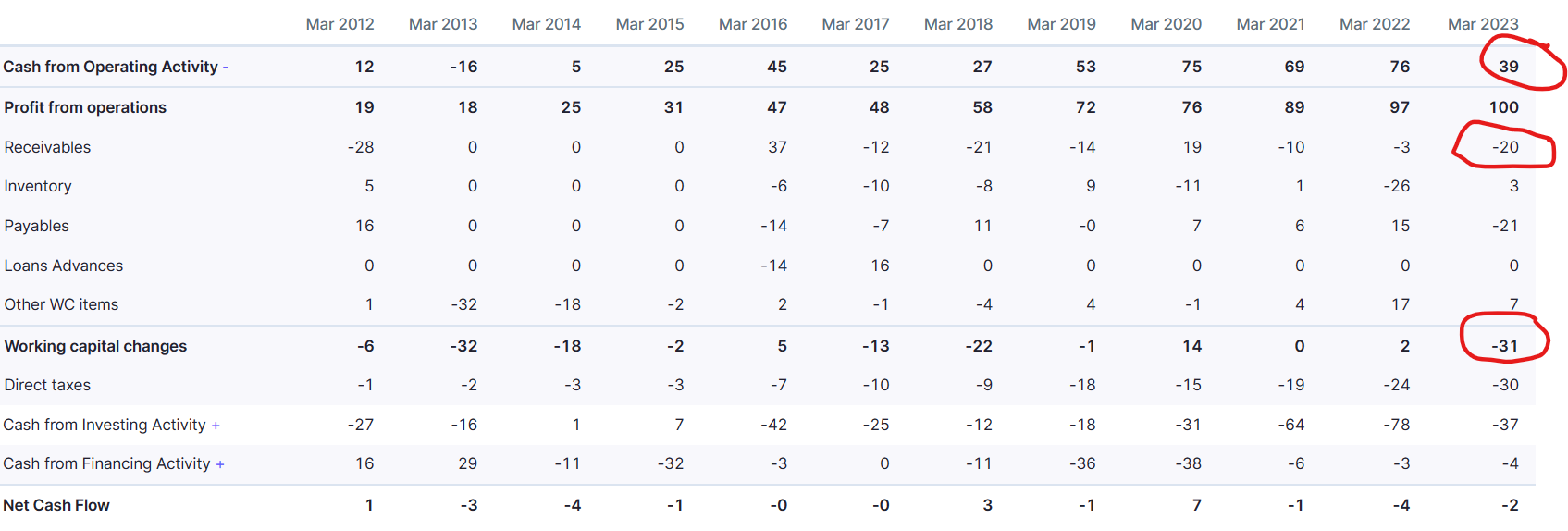

The figure in the screener doesn’t seem to match the balance sheet. The intercorporate deposits seem to be increasing regularly. Even though the current part of these deposits is reducing over the last few quarters the non-current deposits are continuously going up.

The company had 9.99 crores in other income in the last financial year. Of which, 5.02 crores were interests. 0.5 crores interest from Bank, 4.52 crores interest from others. It is possible that this interest corresponds to intercorporate deposits. 4.52 crores interest on the intercorporate deposit seems close to market rates.

In the cash flow statement, 5.02 crores are deducted from PBT to arrive at CFO. But only 2.62 crores are shown as interest received in cash flow from investing activities. I don’t know where the remaining interest went. There is an interest receivable of 34 lakhs in other financial assets.

The company has a bad debt write off of 69.68 lakhs in FY 22, but I am not able to find out any details about it in the AR.

From what I understand the company has really done well to improve its margins in a very tough cost environment. The company’s focus on exports seems to be margin accretive. Exports is 60 % of the sales as on Q3. I believe company’s focus on further expanding its network could aid to growth and margins further. Entry into regulated markets of EU and Australia can be another positive. Cephalosporin capex can be a growth driver in the near term and the company is net debt free. The reducing freight could also aid margins. With a lot of near term growth drivers it seems that the company is available at cheap prices. The company seems to be managing its receivables well considering its end use geographies.

Having said that, a lot of pharmaceutical companies have started focussing on the African markets, it needs to be seen how the competition pans out in the future. Another cause of concern is the constantly increasing intercorporate deposits. At a time, when the company’s profits are increasing and is net debt free, how will the cash flow be utilized? could be a nagging thought in the mind of investors. Will it further increase the intercorporate deposits. So a clarification in this regard could go a long way in changing the perception. Else a declining or stagnant trend of intercorporate deposits should be visible.

LPL 2022-23 , Qtr.-3 Business Presentation.pdf (1.2 MB)

Link to recording: https://www.lincolnpharma.com/Investor/Disclosures%20under%20Regulation%2046%20of%20the%20LODR/14.%20AGM-EGM%20Results/2022-23/Transcript%20for%20AGM%202022.mp3?_t=1676715362

Discl: Have a small position and trying to understand better. May be biased.