Lincoln Pharmaceuticals Limited is an India-based holding company, which is engaged in the business of manufacturing, marketing and distribution of pharmaceutical products. The Company offers tablets, capsules, liquid injection, cream in tubes and dry power injection, among others. Its portfolio of products by segment name includes Aldase, Alphaline, Anzyme, Azilin, Ceftalin, Cepy, Dermolin, Pentalink, Progut, Protosol, Robilink, Soludine, Trixon and Vivian. The Company’s plant is located at Trimul Estate, Khatraj, Tal Kalol, Gandhinagar, Gujarat. The Company has two subsidiaries, including Zullinc Healthcare Limited and Lincoln Parenteral Limited, which are engaged in the business of pharmaceutical products. The Company has presence in Bhutan, Bolivia, Botswana, Cameroon, Chile, Cambodia, Congo, Costa Rica, Ethiopia, Ghana, Hong Kong, Jamaica, Kenya, Malawi, Myanmar, Nepal, Nigeria, Panama, Peru, Philippines, Senegal, Sri Lanka, Thailand, Uganda, Vietnam and Zimbabwe

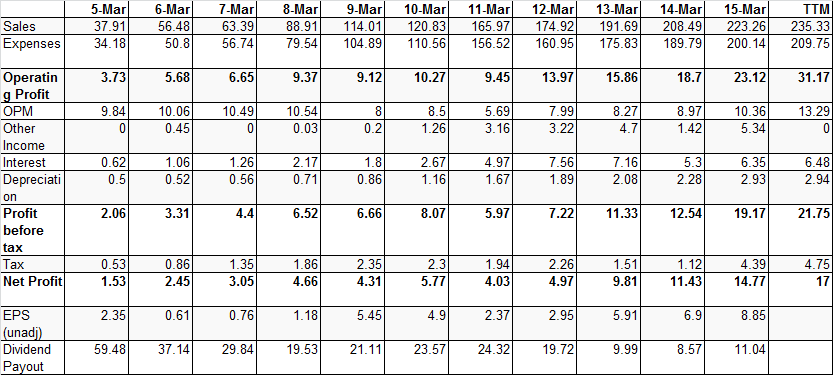

Last 10 years performance:

From Annual Report,

Industry Structure and Developments:

The Company is primarily engaged in the business of manufacturing, marketing and Exports of Pharmaceutical products. In India Pharmaceutical Industry’s continuously showing the growth rate of 20% to 22% as a industry as a whole. Looking to the Indian population, there are lot of opportunities for fast development of industries in the upcoming year also. In regulatory market the opportunities are quite open in generic products in the developing countries and lease developed country. There is lots of awareness in the R&D centres in the country’s and many new molecules as well as process are developed in the countries. Inspite of the stiff competition in the country and parallel marketing of generic products, growth of sales and turn over is assured. The financial year 2014 - 2015 has remained very excellent in terms of sales and growth of the company.

Opportunities:

There are number of opportunities available before the company in terms of products as well as sales territories in India where the growth rates are very potential. The Company is focusing on the brand image of the product as well as corporate branding in the markets. There are numbers of Pharma segments available before the company, for chronic medicines as well as non covered segments as present before the company. The company has wide opportunities for trading of products for developed countries and lease developed countires, business association in the field of manufacturing as well as marketing. The company is focusing on the new market area and other many countries by way of restructuring in the existing organization. The future of the Company and its products seems to be excellent in the coming year.

Outlook:

Company expects to increase the market shares in the exiting markets. The company expects to increase volume in the product portfolio. The company is also expects to introduce new products launched by the efforts of R&D centre. The company is expanding its marketing structure covering all geographical area. The company is focusing on the various divisions like Pharma, Teresa and Lord’s for the category of the product segment and concentrating on focused marketing by dedicated marketing teams. The Company continues to work on innovative strategies to broaden access to its medicines and strives to identify new growth opportunities to deliver strong performance.

Any views ?