The Cephalosporin capex (it was small I think but don’t remember the numbers) was announced in FY22. Apart from that company has not undertaken any major capex in the last few years.

2 Likes

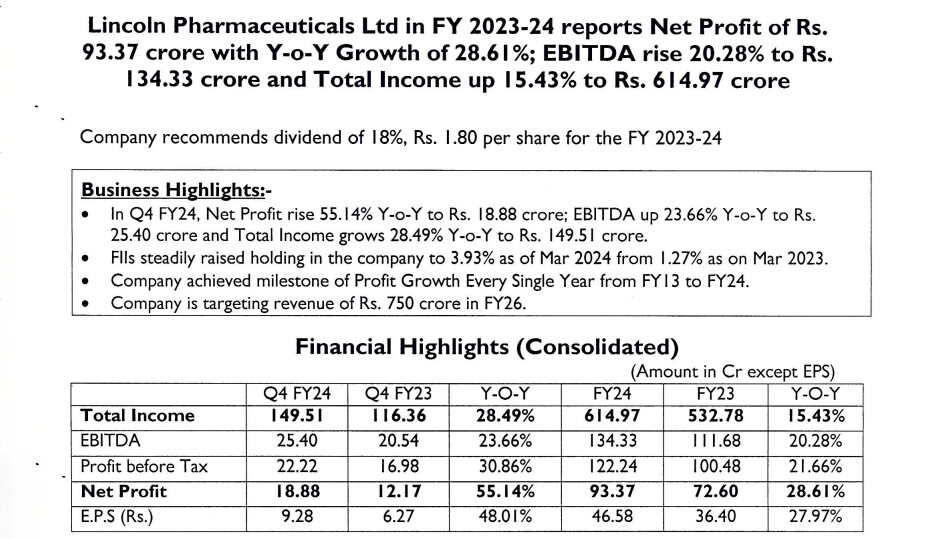

Lincoln Pharmaceuticals Q4FY24 results. Profits rise y-o-y and Q-o-Q, but margins contract. Waiting for management commentary on results before deciding whether to exit or hold.

1 Like

Company had their first conference call ever - which is a good sign!

There were few inconsistencies in the answers given by management. I hope they come better prepared next time around.

Few notes:

Company mentioned Rs 1000 Cr revenue target in next three years from current 581 Cr. That is ~20% cagr.

At some other time, they mentioned 15-18% growth year-on-year going forward.

(in previous quarterly ppt, they had mentioned Rs. 750 Cr revenue target by FY26).

Let’s see where they land in coming years.

But main message is, in any scenario, company is confident of >15% growth conservatively.

They are trying to improve the business in export markets and also in domestic market. Reaching out directly to doctors, increasing MRs etc.

New “Cephalosporin” capacity to generate 55-60Cr revenue in FY25. That alone would be 9-10% growth over FY24 revenue. Cephalosporin could generate ~150Cr revenue when utilized fully.

Company’s capex in FY25 & FY26 to be driven from internal accruals. So expect them to remain debt free.

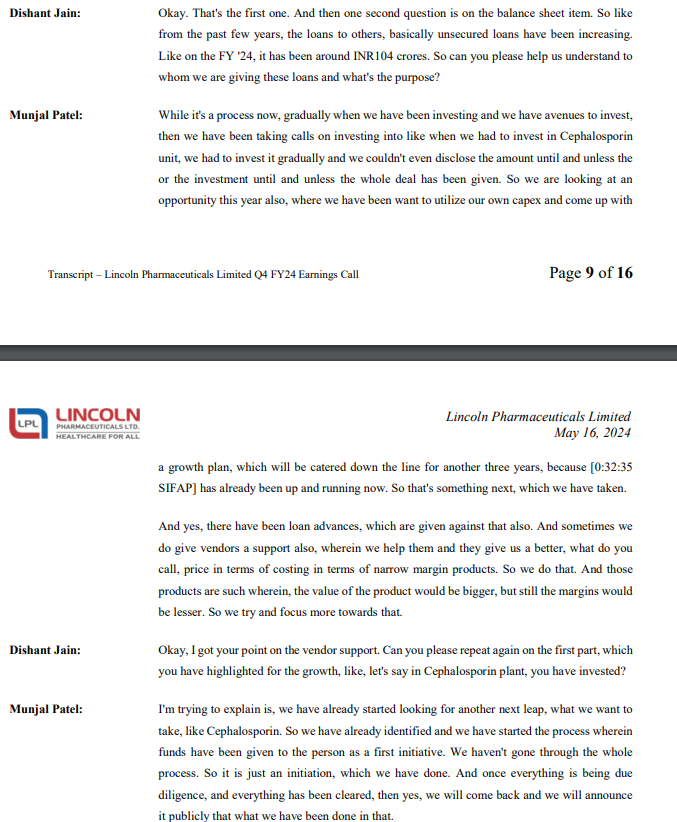

There were questions regarding loans to promoters - which could be a red flag. Needs to be checked in annual report.

Lastly, they invited investors to come and meet them in office and also for the factory tour! Seems like the company is trying to get investors attention.

Overall, company still looks decent with 12x-13x PE, debt free status and quiet grower without much hullabaloo in the current multi-bagger mania.

Disc. Invested

16 Likes

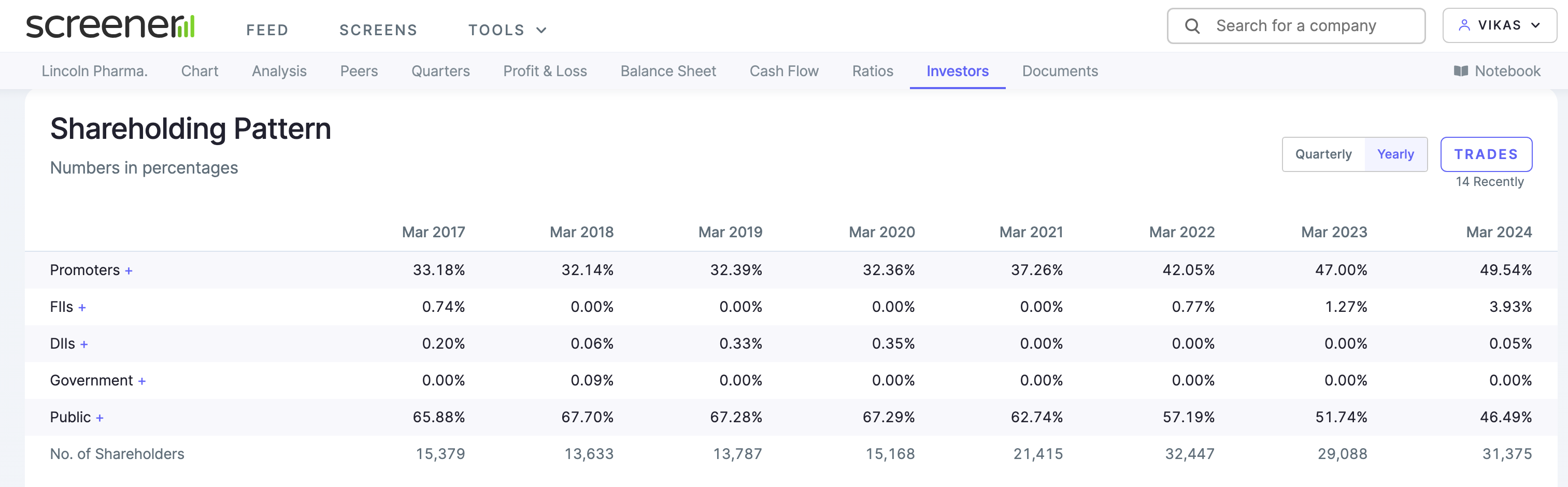

The massive increase in Promoters’ holding is Icing on the Cake.

But it’s more of an unbranded generic, not a great branded generic.

So, we need to see whether it gets re-rated or not.

Not invested. Just tracking.

dr.vikas

2 Likes

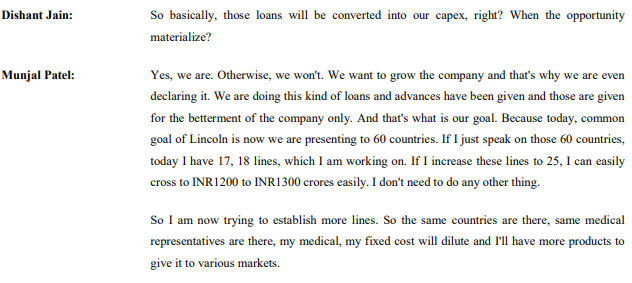

Response on unsecured loans, As per to Mgmt, this is a kind of Capex and will be announced when due diligence/everything is cleared. But still keep the question open on why the loan is fairly big esp before due diligence.

There was follow up question on same, and mgmt responded that in future they will look at being more transparent and aligned with industry practice. This will remain an area to keep a watch.

Disc: Invested

6 Likes

Lincoln doesn’t even supply to US

2 Likes

Is this branded generics or is it more of promotion of their brand? I mean they do not sell the same product with and without brand right?

I see this as more of what Caplin does in LatAm market.

2 Likes

SAST update: Promoter Munjal Patel bought 35,000 shares in the open market. I think promoter will continue to buy smaller quantities of share in the open market of the next 12 months.

Concall notes for this quarter, they are expecting faster growth going forward with improvement in margins.

FY24Q4 Lincoln concall

-

Expect to grow sales by 15-18% CAGR and reach 1000 cr. in 3-4 years at 20-22% EBITDA margins

-

Export

-

Present in 60 countries. Strong presence in East Africa followed by West Africa, Latam, Southeast Asia

-

Transitioned from B2B to branded generics in 2021, and focus is now on generating prescriptions through doctor-MR

-

Have 30-35 MRs

-

1500+ registration; 750 pipeline

-

Focus is to grow exports to Canada, Australia and Europe

-

Commercialized 4 products in Canada (19 filed)

-

-

Domestic

-

Present in 13-15 states; top 3 are Uttar Pradesh, Assam, Odisha

-

Were earlier present in Tier 3 cities and now are increasing presence in Tier 2 and Tier 1 cities

-

600 MRs which should increase by 150-200 in next 2 years as they expand to more states

-

Strong in ENT segment (Tinnex brand)

-

Entire sales are through prescriptions (branded generic)

-

20% portfolio under NLEM

-

Launched 20-23 products in FY24

-

-

Cephalosporin

-

Plant was commercialized, injectable block has been implemented. Have WHO approvals and filed products

-

Expect 55-65 cr. in FY25

-

At full utilization, can reach 220-230 cr. revenues depending on final product prices

-

Also servicing Indian market from this unit

-

-

Capex

-

Invested 100 cr.+ via internal approvals in last 3-years

-

25-30 cr. annual capex plans for next 2-years

-

Currently they have 17-18 lines, with 25 lines they can do 1200-1300 cr.

-

Solar capacity is now 4 MW (solar plant + rooftop solar). Will be saving on energy costs because of this

-

-

Related party loans

-

Loans and advances increased from 82 cr. to 104 cr.

-

Explained this as a way to do capex; current year increase was for the next big product (like they did cephalosporin couple of years back) and for getting into more regulated (and higher margins) markets such as US

-

-

Have not suffered from currency issues because of their B2B model where distributors arrange payments

-

Dermatology, cardiology, diabetes are the main growth focus, contribute 100-150 cr. (domestic + exports). Expect to grow 50% in FY25

-

Munjal Patel is looking after finance, exports and factory

Disclosure: Invested (position size here, bought shares in last-30 days)

15 Likes

Hello community,

For the past few years trade receivable growth is higher than sales growth.

Is it because of the export being 60% of the business?

please help me understand this better.

Thanks

Invested

2 Likes

Despite so much working capital stuck in Receivables, they’re able to function without racking up much debt, but definitely needs to work on bringing it receivables down.

4 Likes

The company’s receivables as a proportion of sales is around 20-25%. So I feel there should not be an issue of receivables rising at faster rate than sales. However, there is one concern of related party loans which have been highlighted here a couple of times.

3 Likes

Related party loans (unsecured loans) as per the concall they said something on the line of “we help them they help us”

Im not sure how to take this statement thought.

4 Likes

An old interview with MD

1 Like

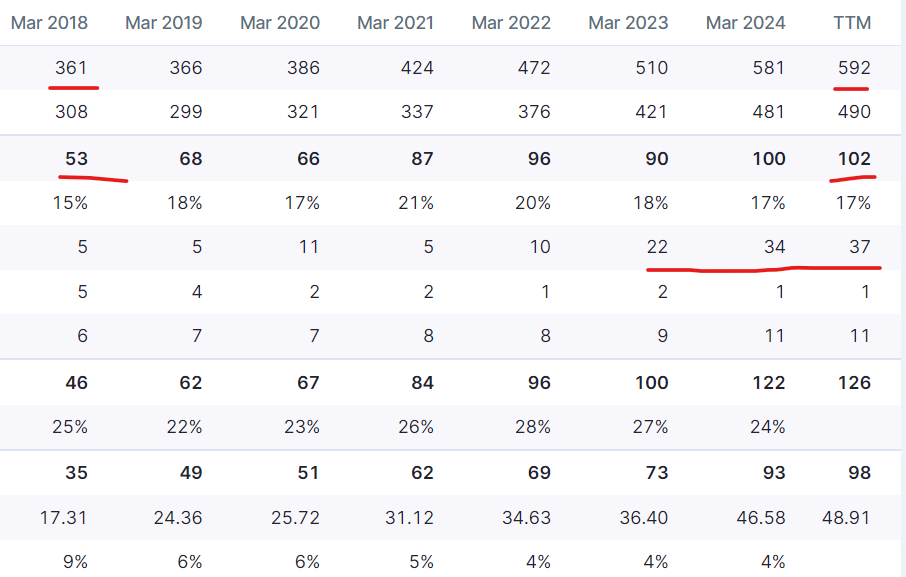

The sales from 2018 has not even doubled in 2024 in 6 years time.

Operating profit has barely doubled in the same time frame. Growth rate ~12-15%

What has been pushing the bottomline past few years is the ‘Other income’

What is this exactly? Investments? MFs? Is this expected to continue or revert back to 5-10 Cr?

Where will the 1000 Cr topline come from? Any capex or strategy shared by management?

Disclaimer: Recently started tracking due to cheaper valuation and aggressive guidance. Not invested.

7 Likes

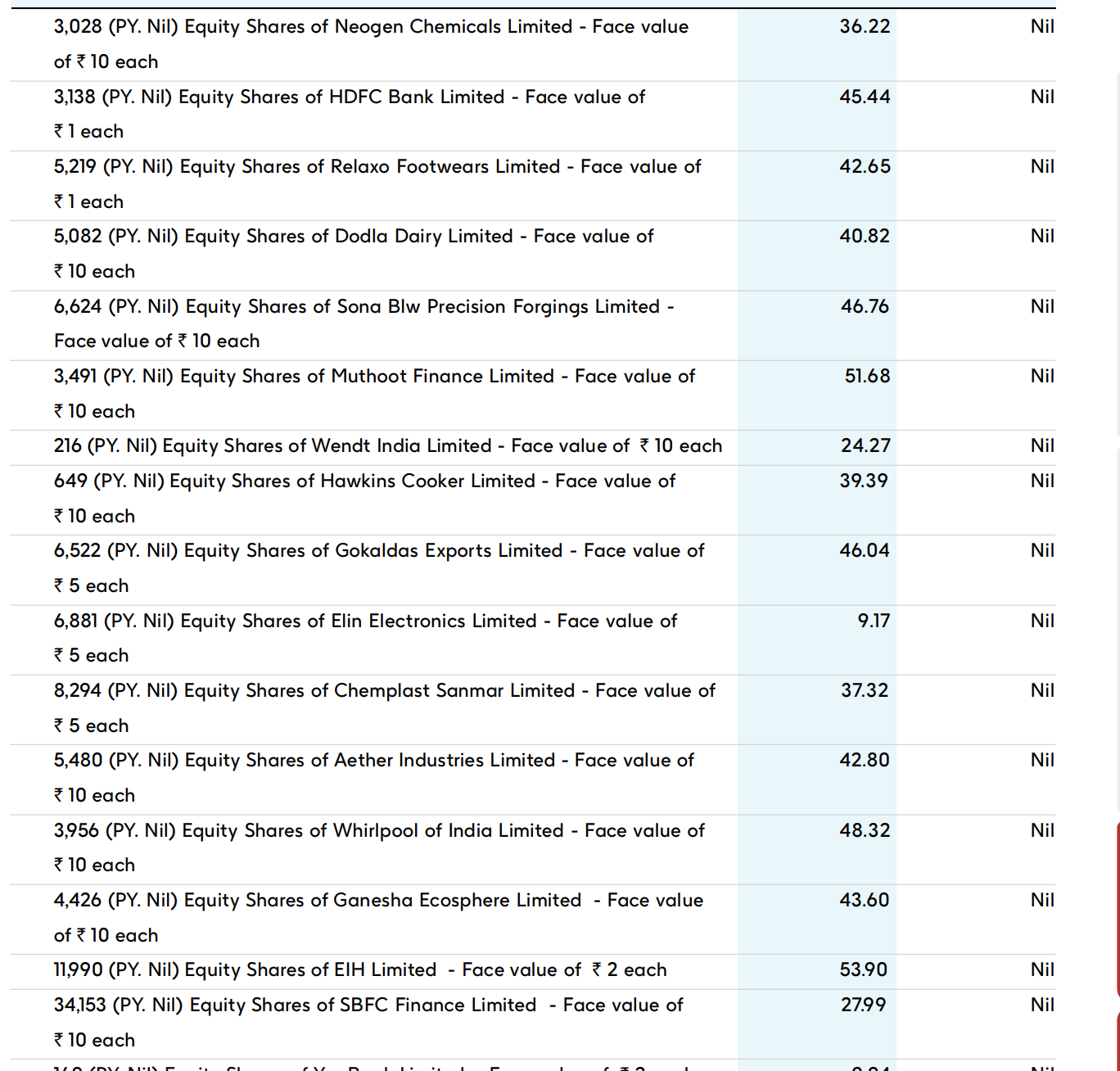

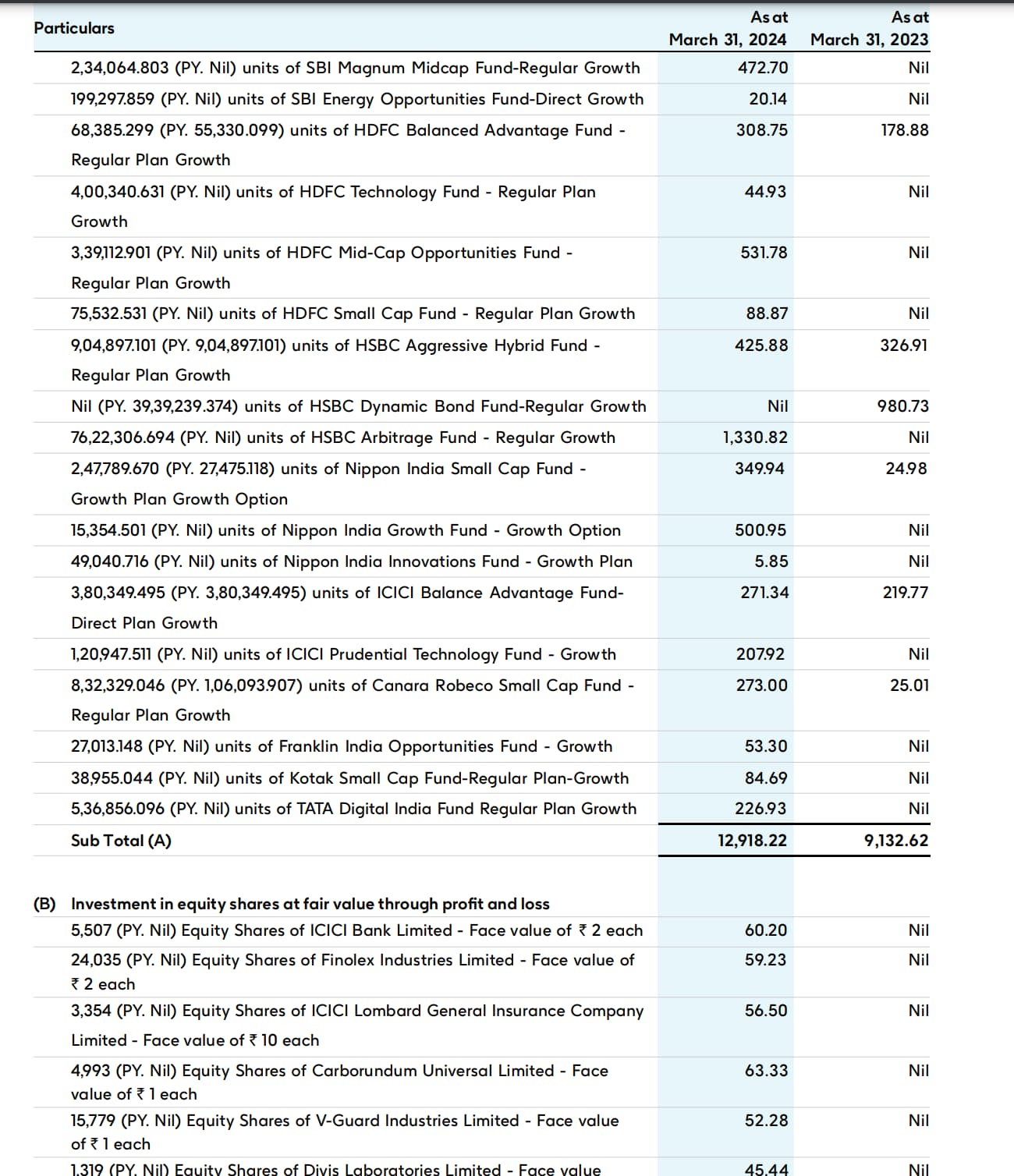

You are right. Substantial chunk is coming from equity investments. See line item “Gain on fair valuation of current investments”

There is full fledged equity portfolio in the balance sheet with several MFs and listed equities:

Disc: Invested with a small position, bit circumspect now after seeing these details.

8 Likes