Expand International Markets: Grow in Canada, Australia, and the EU by leveraging certifications (TGA, EU) and increasing product registrations.

Grow Domestic Market: Focus on high-demand cardiac, diabetic, and dermatology segments, and increase medical representatives from 600 to 800 in the next 2 years.

Maximize Cephalosporin Plant Output: Scale the plant to contribute INR 55-65 crore in FY25, reaching INR 220-230 crore annually.

Launch New Products: Introduce new products, leveraging a pipeline of 750+ products under registration.

Capex Investment: Invest INR 25-30 crore over two years to boost capacity, funded by internal accruals.

Do we know if the company gave any similar guidance in the past and walked the talk?

If it couldn’t manage 10% CAGR sales growth in past 9-10 years (on a much smaller base), I wonder if these are enough growth levers to double the topline in 3 years.

Every company makes some investment. Be it in FD or stocks. This can’t be a redflag. But the issue is, other income (mostly stock market gains) is driving their net profit and not the profit from core operations.

If we look at last year, the core profit growth YoY has been at 11% while the net profit growth has been at 22% due to the other income.

However the stock p/e excluding the other income is still around 14 (souce screener). Stock still looks cheap to me. But for a rerating they will need to show growth in core business which they have been promising of 15%+

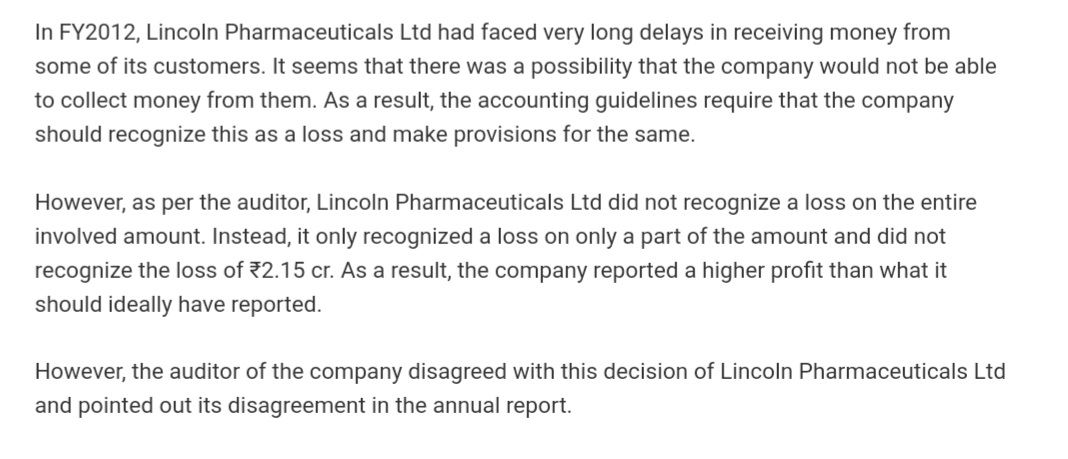

Lincoln Pharma has a history of inflating its profits, In FY 2012, the company reported a lower provision for bad debt, categorizing it under trade receivables.

With other income sources including 22 crores from share valuations related to investments or trading.

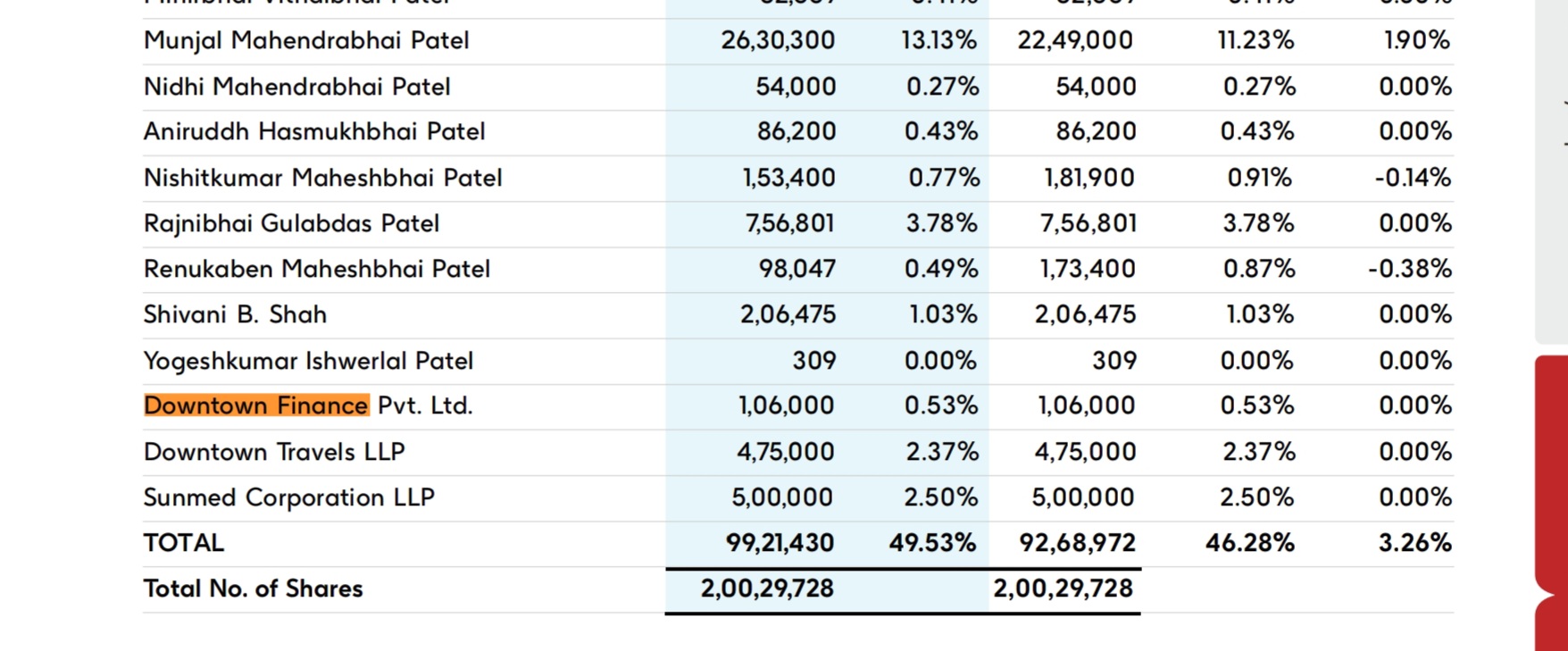

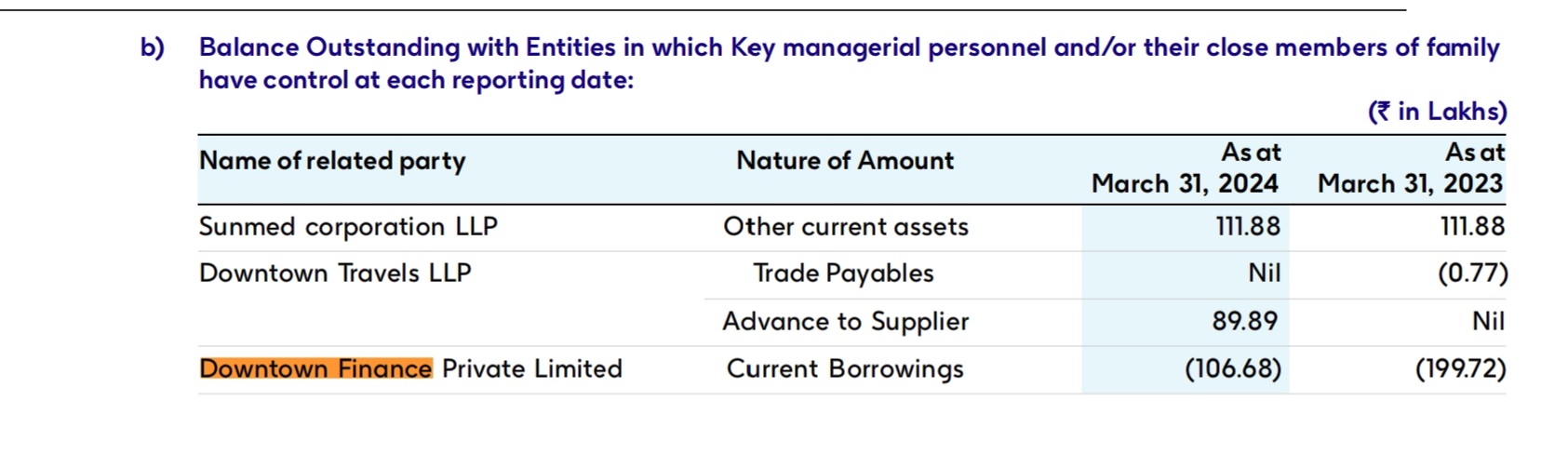

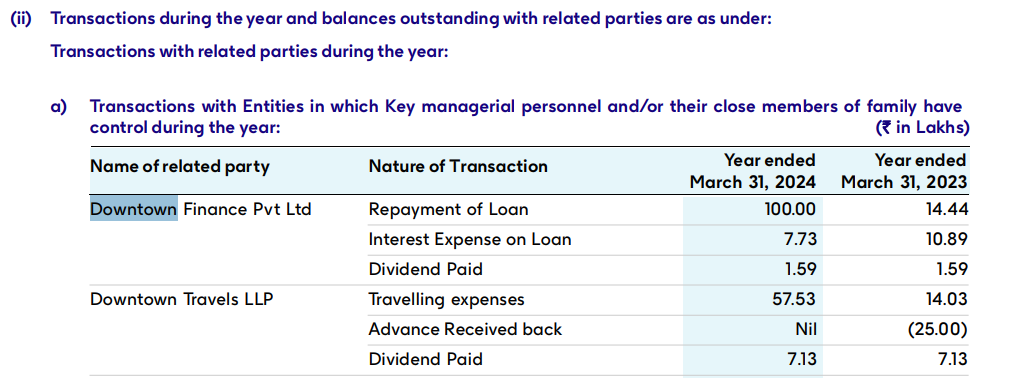

The company also lends money to Downtown Finance, managed by key personnel who invest in Lincoln Pharma shares during significant stock price declines. When asked about this, Munjal Patel stated, “We help them, and they help us,” emphasizing their reciprocal relationship.

Even after excluding fair valuations from stock trading income, the price-to-earnings ratio stands at 20, and low sales growth since 2016 likely contributes to this low P/E ratio.

[My view] Additionally, being a debt-free company, Lincoln Pharma has the flexibility to take risks and generate capital from various sources, including stock trading, which it can ultimately reinvest in its business. If revenue increases in the near future, the price-to-earnings ratio could rerate to 35 or higher, potentially pushing market capitalization beyond 5,000 crores and positioning it as a potential multibagger.

Moreover, cephalosporin developments are in the final stages and are expected to be monetized soon. According to management, this could boost revenue by 250 crores, serving as a significant growth trigger for the company.

I’d like to share a different perspective on this. If a company has excess capital, they can either return it to shareholders in the form of dividends or buybacks or park it in a safer instrument like liquid funds / fixed deposits. If they go about investing in equity, they are only broadening the risk vector (capital market downturn) beyond their inherent business risks. Our job is investing, their job is doing business, not taking undue risks in capital markets.

The pharma and healthcare sector has been in full tailwind recently.

गधा और घोडा सब भाग रहे है

One has to be very careful while investing in small caps.

Here on the chart, the volumes look good. However, Lincoln’s main problem has been its sales growth. Promoters buying from the market have been excellent for the last few years.

But unless and until the sales grow more than 15-20%, re-rating looks difficult.

@ayushmit Neuroprotective medicine of every brand are mostly always on higher side. You need to check price of generic medicine like Pantoprazole to make an assumption; for which difference isn’t much. Regards

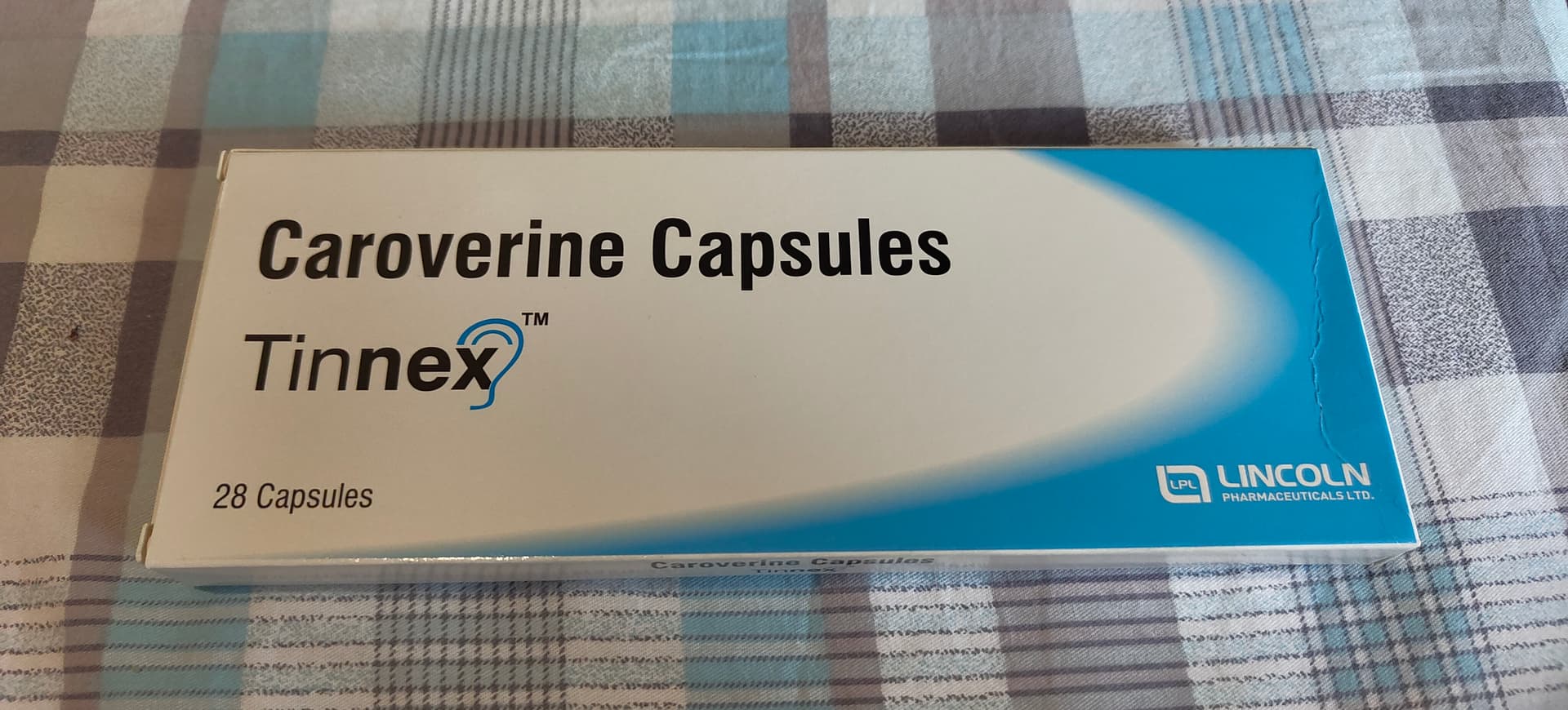

I am a practising ENT surgeon since last 15 years and do come across tinnitus patients on daily basis.

Yes. Tinnex ( Carovarine ) was the first brand for tinnitus management. It WAS kind of monopoly. But now there are at least 3/4 more big, reputed companies with the same molecule

And the molecule itself is not the perfect treatment for tinnitus.

And I guess, Tinnex is their number-1 brand.

I don’t think they have any other blockbuster brand

This was the reason I never invested in this company.

I love the way promoters are increasing their stake slowly and steadily. But their sales growth is just average.

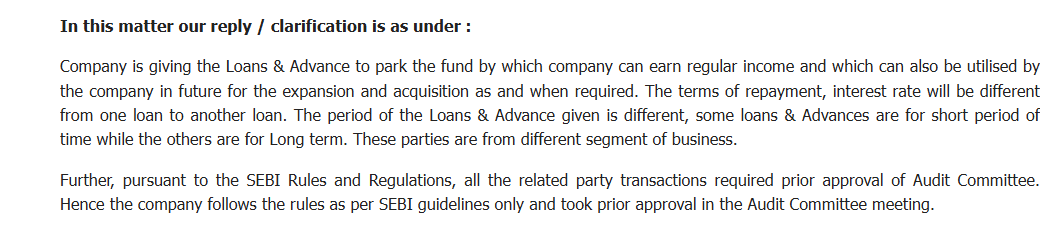

I asked the investor relations about the loans and advances significantly booming to the unrelated parties and this was their response

This was not at all satisfactory as if you want to park your funds then park them in safer options like Debt mutual funds or equity mutual funds but why to Unrelated parties ?

This company has been doing this pvt lending business for many years now. Though its not ideal, not seen any bad debts like situation. They must be confident of making better return than equity/debt funds. But agree that understanding this risk is not easy.