A comparative analysis

Financial Observations on Indian Insurers

I am new to the Indian insurance sector, but have general knowledge about how insurance works in the American context. I have observed that Indian insurers invest a very meagre amount of their AUM into equity (single digit %s) compared to their foreign (American/British counterparts). I assumed that this is because of some IRDA restrictions, but upon digging deeper, I couldn’t find any such regulation. Why then do they invest almost all their AUM into debt?

I also observed that many insurance companies consistently make an underwriting loss in India - they promptly state (in ARs) that they invest the money in order to ‘meet’ the claims. This baffles me - to set such a low bar on themselves for underwriting and investment financial performance. It appears that they are banking on the fact that Indian public is very uninsured and are willing to write business at insufficient premiums just to gain more volume.

Would anyone with experience in this sector please throw some light on this?

3 Likes

Some data wrt General and Life insurance companies -

GENERAL INSURANCE

Company…Premium Collection till Nov 20 …Growth ( YoY ) …Mkt Share

Bajaj allianz …8252 cr…(-) 7 pc…6.5 pc

Icici Lombard…9304 cr…3.6 pc…7.3 pc

HDFC Ergo…7804 cr…24 pc…6.1 pc

SBI General …4749 cr…6.7 pc…3.7 pc

LIFE INSURANCE

Bajaj Allianz …3133 cr… (-) 3.3 pc …1.8 pc

ICICI Prudential…6429 cr…(-) 8.9 pc…3.8 pc

HDFC Standard…11721 cr…8.8 pc…7 pc

SBI Life …12115 cr…13 pc…7.3 pc

LIC…115658 cr…(-) 3.7 pc… 69.4 pc

Max Life … 3475 cr…13.7 pc… 2.1 pc

Kotak Life… 2274 cr…(-) 22 pc…1.3 pc

Disc : holding Bajaj Finserv, Icici Lombard

Policy servicing complaints have become the number one grievance among life insurance customers overtaking misselling or unfair business practices…The total complaints among life insurers stood at 165,217…

.

The grievance data showed that there is an increasing trend in the number of complaints against LIC. Overall, the complaints against LIC increased from 64,750 in 2015-16 to 112,005 in 2019-20.

.

On the other hand, private life insurers have seen a decrease in the number of complaints filed.

1 Like

On one hand they say that term products are high margin products but reinsurers think otherwise and now this price hike. Penetration would further slow down after parity with MF on ULIP front.

I am also studying the Life Insurance space to find whom to bet on.

When I was reviewing the annual report for HDFC Life, I was very surprised to see the absolutely dismal amounts of money being pumped in Equities. As an insurance company, the whole idea of running an insurance business is to make money from investing in other companies cos there is a legit need to invest the hard cold cash machines that these companies are.

Berkshire Hathway generated 50% of their NET INCOME by investing in highly valuable companies. Warren Buffer and Charlie Munger understood the potential and opportunity of running these cash machines and generating higher returns on capital (consistently compounding over decades for 20% + CAGRs).

It is beyond my why the Indian counterparts are so risk averse? I am sure there is enough skill in the market to hire good CIOs to run the equity portfolio of a higher size with proper risk management procedures. I am still baffled to see such meagre numbers being pumped in equity by the insurance majors in India. It is a criminal waste of money. Why invest capital at 6-7% on Debt when a simple HDFC bank generates more on a year basis?

Experts - Please help understand this gap.

6 Likes

I think HDFC Life is investing around 30-37% in Equity (AUM Equity %). In March-2020, their AUM Equity % dropped to 29% and the reason was market crash at that time. I find HDFCLife’s AUM Equity % reasonably high. SBI Life numbers are around 22-27% as AUM Equity % in last 3 years (dropped to 21% in March-2020).

HDFC Life Annual Report FY19-20 Investment screenshots:

On Shareholder Account - Screenshot - e919f2d197abcced53b3180fc21fa022 - Gyazo

On Policyholder Account - Screenshot - 469866bf76a6c0046d486f6d3fd249dc - Gyazo

From this it seems like the investments held on Shareholders account is 6/55 i.e. c. 11% and on Policyholder account is 6.67% so not sure how you arrived at 30-37%. Even if we take Covid crash into account these %s are roughly 15% and 10 % respectively.

1 Like

I was referring to the Equity AUM % mentioned in their Qtrly Investor Presentation (screenshot below). But it seems that number in the presentation might be overstated due to ULIP investments, so shouldn’t be relied on directly so I stand corrected.

Equity AUM % mentioned on page 32 of Investor Presentation https://brandsite-static.hdfclife.com/media/documents/apps/HDFC%20Life%20Presentation%20-%209M%20FY21_Final.pdf

1 Like

Please go through IRDA regulations you will get answer specifically table 5

https://www.irdai.gov.in/ADMINCMS/cms/frmGeneral_Layout.aspx?page=PageNo63&flag=1

Thanks

6 Likes

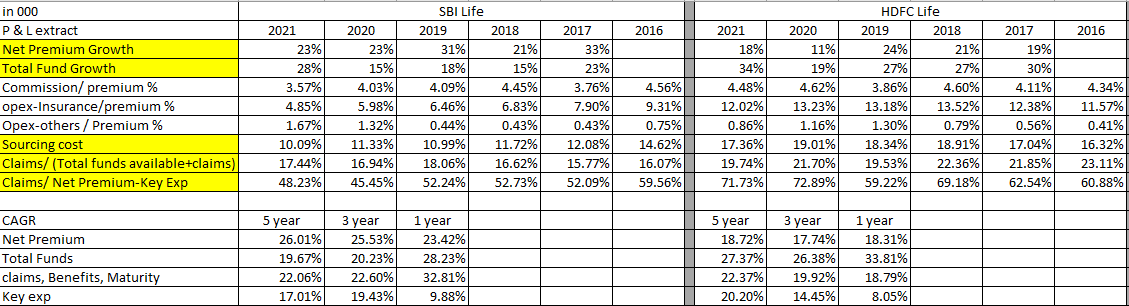

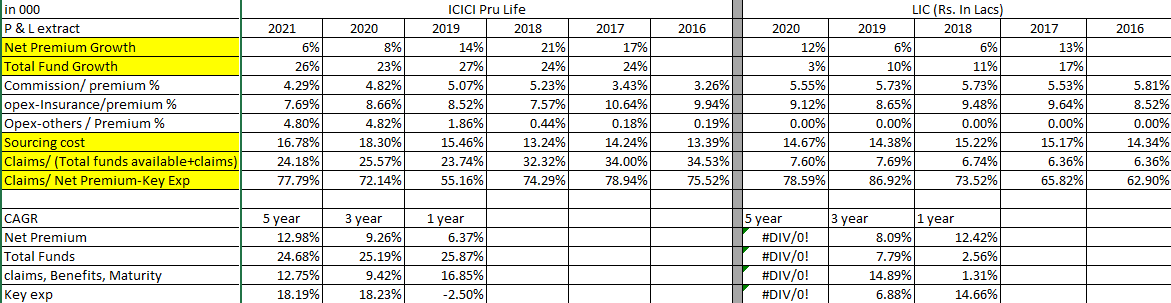

Bumping the thread as I have covered 4 insurers as prep for LIC IPO

There are 3 key factors in the Industry, which all can agree:

-

You have to get max. premium so that you can easily pay your claims while keeping cost of getting premium, low.

-

You have to be the best in industry when growing funds with very good rates of return

-

Be the best underwriter i.e. skewed underwriting where you prefer certain demographic like non-smokers, govt. employees (excl. police/army) etc.

Leadership in any 1/2 factors would make you the best in the industry. I personally prefer factors -2,3 for the sake of bad times.

On Factor -1 leadership : SBI Life

On Factor -2 leadership : HDFC Life

On Factor-3 : having low claims is the best but how do you compare it. One metric is claims/ total policies. But amount wise differences would make it a wrong comparison. Help from any of the members would be great. on this factor

5 Likes

Table 5 is for the investee company. But what we are talking here is AUM of insurers.

Listing of Life Insurance Corporation of India (LIC) is not far as BSE just introduced Policy Holders Quota.

As life insurance companies are now in a high growth phase and private companies are increasing there market share, what are the long term prospects of LIC as a business?

2 Likes

Any thoughts on the level of reinsurance and average life cover…

Hi…what is your take on LIC IPO? From long term perspective, being a market leader with still 70% market share, even after privatisation of the sector in 1999, they have been able to maintain the dominant position. If you see the gap between number 1 and number 1 players, worldwide is 2 to 3 %…but in India the 2nd player SBI life is one tenth in size compared to LIC…So can this be a part of coffee can portfolio for 10 years outlook with multibagger potential and also being part of NIFTY index? please shed some light?

2 Likes

@brijwanth could you pls update the excel as of now post IPO of LIC.

Came across this video on youtube. For those who do not fully understand the life insurance industry it is very good starting point - provides insights on key drivers of profitability, key parameters used by analyst for valuations etc.

2 Likes

First a little Context in what we are trying to do here:

-

As you must be aware that insurance is a business of taking on risk for a fee. The underlying financials of most of the insurance companies are almost like greek and latin, even for the well versed in accounting.

-

The Insurance Industry and accountants simplify the whole financials in to simple monitorable parameters like VNB(Value of New Business), Mortality Rate, Types of Policies (Participating and Non-Par) etc. These figures take some facts and some estimates to get to the right answer. The problem lies in not being able to compare these estimates.

The problem I am trying to solve is three-fold:

- Make the financials comparable across the companies in the life insurance sector.

- Take the financial parameters which are as real and not as much subject to estimates as possible. If not at least the parameter must be well regulated (i.e. if the company falsifies the parameter then the promoters should be put in jail).

- Make it as easily understandable.

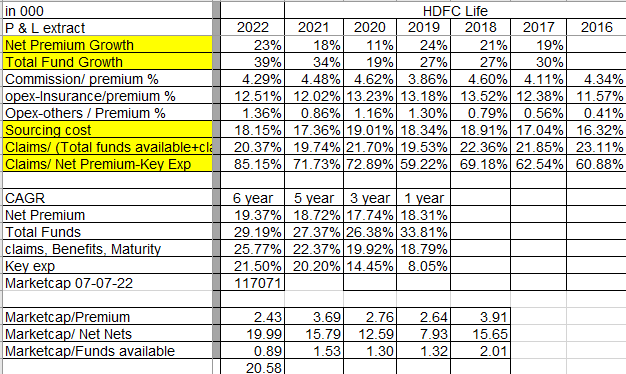

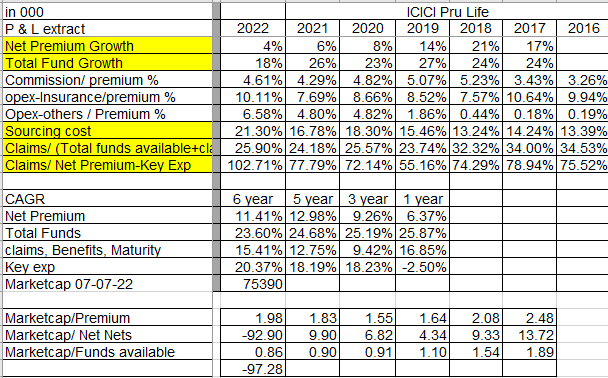

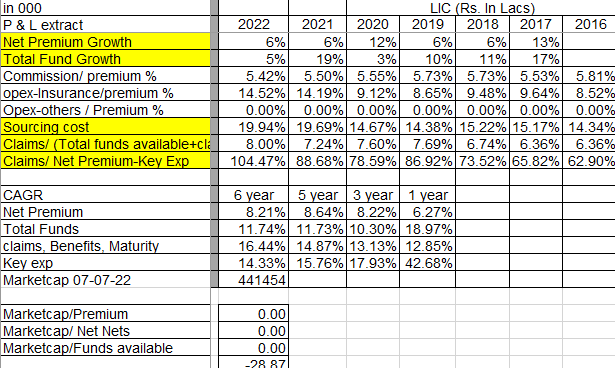

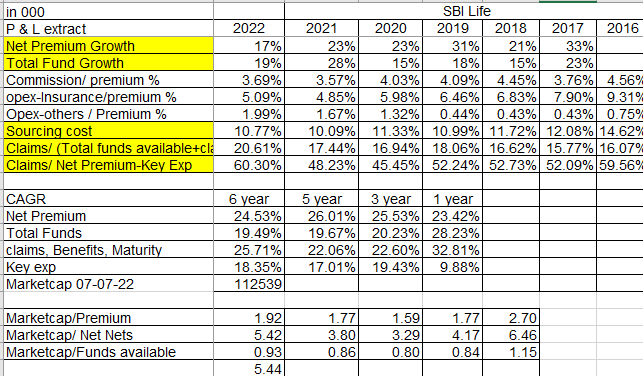

Some Context here : This year was particularly hard for the companies as the death claims during the 2nd covid wave indeed shot through the roof in India. So naturally all the companies showed record number of claims. LIC finally debuted on the exchange and it would be unfair to compare it’s Share performance.

We are evaluating the companies(SBI Life, HDFC Life, ICICI Pru, LIC) on 4 factors

-

You have to get max. premium so that you can easily pay your claims.

This Year HDFC Life was the top lead with SBI Life being in close lead at 17% -

You have to be the best in industry when growing funds with very good rates of return

HDFC Life grew very well like last year in fact it out grew every other company and ensured that the funds available for claims increased despite collecting lower premium. -

Being the best underwriter i.e. skewed underwriting where you prefer certain demographic like non-smokers, govt. employees (excl. police/army) etc.

Still no company shows such a skewed underwriting skill. In fact the regulator has indirectly not allowed such skewed underwriting. -

Low cost sourcing of policies and Low cost Operating Expenditure.

SBI Life leads the with lowest cost structure.

How did the market react to these financials in the last 1 year

SBI Life gave a decent performance while HDFC Life did have a fall. ICICI Pru Life fell.

From Market cap perspective we understand that SBI Life is relatively cheap and hence did not fall by a huge margin. SBI Life was also collecting decent amount of premium and a decent amount of growth.

HDFC Life’s fall was curtailed as it gave a top notch performance among big 4. The premium valuation came to haunt and reduce it’s price. Still HDFC life enjoys a premium over it’s peers.

ICICI Pru Life and LIC had negative Net Nets excluding taxes (Premium- Claims & Benefits - Expenses). However a look at it’s P&L does not show a Loss the reason is like banks the regulator makes you put aside provision every year, so that you can use it in such circumstances.

11 Likes

Hi All,

Recently IRDAI has announced that life insurers can now sell full fledged health insurance plans. Previously most of the health insurance were part of the general insurance division. How this will affect pure play general insurance companies like ICICI Lombard… Now ICICI LOMBARD will have competition from life insurance companies like LIC and their own sister concer life insurance division ( ICICI Pru life)…

1 Like