In this govt … most of the statutory bodies and regulators … are quite not sticking to timelines … for ex . ePFO doesn’t update statements regularly… interest credit has happened 8 months behind schedule… I’m observing this across multiple bodies

October monthly business figures were released last month itself. It was just not placed in the regular link. You can get the data from the link below (select the excel option to download)

https://www.irdai.gov.in/ADMINCMS/cms/NormalData_Layout.aspx?page=PageNo3950&flag=1

1 Like

Thanks you. Got it.

Can you let me know in which section of website is it being posted ?

Regards

Normally, the monthly numbers are posted in this link given below - https://www.irdai.gov.in/ADMINCMS/cms/frmGeneral_List.aspx?DF=MBFL&mid=3.1.8

Following are some interesting points for HY20 =>

HDFC Life

- Back book profit is basically VIF unwinding. The growth in back book profit is high at 29% for HDFC Life because we have high VNB margins and experience on assumptions has been good.

- As per some industry players, to provide a non par savings products at 6% yield, math goes as follows - 2% distribution cost, 50% has to be invested into govt. bonds which provide yield of 7%, so rest of the 50% has to provide 9% returns. The maths is really tough.

- To above, the response of HDFC Life was - we were planning for this product 24 months ago & hence we have some inventory of higher yielding govt bonds. Also we have risk management strategy of managing risk at portfolio level.

ICICI Prudential

- ICICI Bank has taken selling of protection products seriously only in last 12 months.

- VIF grew a little slow from 142bn to 149bn from FY19 to HY20 - due to negative economic variance

- LIC has cut the premium rates for protection products & the rates are comparable to private players now.

- On increasing competitive intensity in protection space, there are only 6-7 players who are meaningfully active in protection space & pie is really large.

- The company is seeing early signs of persistency challenges in higher ticket ULIP products.

- The company manages risk per product basis and does not do risk management across products. The company does not do deferred annuity products.

SBI Life

- The company did underwrite non par savings products with yields between 5.5 - 6%. There are two hedging mechanisms available for this products - partly paid bonds & forward rate agreements (FRA). The way partly paid bond works is - e.g. for a bond of 100Rs., 20Rs. payments are done every year for 5 years & interest rate is fixed at the beginning of the tenure. This is very useful for regular premium non par savings products. I have no idea how FRAs work.

- Return of purchase price (ROPP) protection plans dominate the individual protection policies the company writes.

Max Life

- Axis bank has signed up as banca partner for LIC. It seems LIC is finally becoming aggressive by reduced pricing & signing a large bank as Axis as banca partner. Max Life gets 50%+ business from Axis bank & how this impacts them needs to be seen. Also how aggressive stance of LIC hits private players needs to be seen.

- The share swap agreement with Japanese partner did not go through.

- For company to reverse merge max Life into Max Financial - company has to get closure on contingent liabilities of Telecom business in the past. The case is at ITAT (?) & the IT department has not pursued the case for 20 years.

- Another thing that we need to check is - where does accounting of 1% buyback from Axis Bank happens - in holding company or in Max Life? If it happens in holding company (likely), then certain adjustments have to be made while looking at Max Life’s numbers. Also upon every renewal, these risks will come to the fore. Will margins compress if deal with Axis moves from equity to comissions?

Disc - Invested in HDFC Life. No transactions for last 6 months. Not a buy or sell recommendation. Please do your own due diligence.

12 Likes

Impact of budget on life insurance comapnies:

- Abolishing DDT: Budget 2020 abolishes DDT and makes dividend taxable in the hands of the recipient. The budget allows for deduction of dividend paid by the company to its shareholders thus providing some relief to companies.this move reduces FY21E VNBMs of insurers (by 70bps as per HDFC equity research report for HDFC life)

2.Optional New Personal Tax Regime: individuals with income in the range of Rs 7to15 lakh will have lower propensity to invest as the tax savings on incremental investment is in the range of ~19-30%.

individuals earning higher than Rs 15 lakhs may continue to prefer using deductions/exemptions as tax reduction on incremental savings is ~43.2% - the Government also plans IPO of LIC of India. LIC will be one of the most valuable companies in India and even a 10% listing of the company will create serious additional liquidity (conservatively expected at ~US$ 10bn). This too may reduce appetite for pvt. life insurance paper.

Source: HDFC and other research report on insurance

1 Like

The Insurance Regulatory and Development Authority of India (Irdai) has mandated all general and health insurers to offer a standard health product with a sum insured up to ₹5 lakh.

While respect the viewpoint but on the contrary i feel lic ipo will increase market for insurance firms among investors and finally the increased investor share would flow to the better managed and incrementally better performing firm, whoever that may be.

Disc. Hdfc life a core holding. This is Not a buy sell recommendation

Would coronavirus, if widespread, lead to above normal expenses for life/health insurance companies?

Understanding the financial services industry is a challenge in itself for the majority of investors. The KPIs are unique, the risk on the balance is hidden and back-ended. If financial companies are confusing to understand, insurance companies are downright tough.

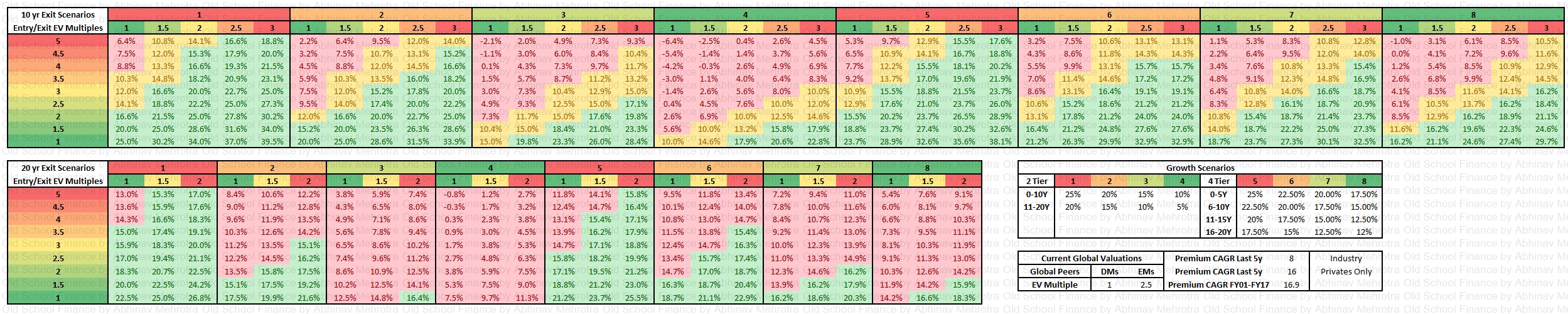

In this post I would not make an attempt to simplify the insurance industry as a whole, that is a big task for some other day. Today we will focus on what kind of investment returns an investor can expect based on one of the valuation parameters that is widely used in the insurance industry.

We will use Embedded Value (EV) to derive a return matrix based on entry and exit multiples and a few different growth scenarios. If you do not know what EV is, you should google and read up on it. As geographical jurisdictions change, calculation of EV is slightly different. Many Indian insurance companies have started reporting IEV (Indian EV) now. Research the web to know more.

EV calculation has a lot of variables in it, these variables often need to be forecasted for long time periods and these assumptions are made by the insurance companies. Is there is a potential for foul play? Yes. Just imagine this, it is already very very difficult to ascertain the true book value of a bank, NBFCs etc. because it comprises of 1000s of loans, whose value is determined by the management. It is easy to report these loans as good and maintain the company’s book value. Add to this, now you have estimations of future profits, that is what makes EV.

The avenues for wrongdoing just jumped multifold. That being said there are regulators who periodically keep a check, how effective they are is a discussion we should save for another day.

What I am trying to say is, be careful when assigning multiples to a financial company’s book value and an insurance company’s EV. Keep a margin of safety if you will.

In the table below we have calculated the expected returns based on multiples of this EV. Incidentally one can use this for Price/Book as well. The concept is the same.

Here is what we have done,

- Assumed P/EV entry multiples from 1 to 5 in increments of 0.5.

- Assumed P/EV exit multiples from 1 to 3 in increments of 0.5.

- Assumed a 10-year and 20-year exit scenario. For exit in 20 years, exit multiples have been capped at 2x.

- Assumed 8 different growth scenarios, labelled 1 to 8. Scenarios 1 through 4 are 2 tiered, meaning, we have different growth rates for the first 10 years and the last 10 years. Scenarios 5 through 8 are 4 tiered, meaning, we have different growth rates for 4 different 5 year periods.

- Growth scenarios are colour-coded, aggressive growth is shaded towards red and conservative growth is shaded towards green.

- Similar to the previous point, Exit/Entry multiples are colour-coded as well. High entry/exit multiples are shaded red and low entry/exit multiples are shaded green.

- Does not include dividends.

We start with an EV of 1 unit at year 0, apply the differing growth rates as per the growth scenarios. We get a certain future EV value at year 10 and 20. We use an exit multiple on this as per the different exit scenarios. We divide this exit with the different entry multiples scenarios. We calculate the return in CAGR form for different exit time periods.

CAGR returns above 15% are highlighted in green, between 10-15% in yellow and below 10% in the red.

Hi-Res Table: Table Image

So how to make sense of the table, which growth, exit and entry scenario to expect.

Here are a few pointers,

- Global peers in developed markets trade at ~1x EV.

- Global peers in emerging markets like China trade at ~2.5 EV.

- The Indian insurance industry as a whole has grown premiums at a CAGR of ~8% in the last 5 years.

- Private insurers in the Indian insurance industry have growth premiums at a CAGR of ~16% in the last 5 years.

- Industry premium CAGR from FY01 to FY17 was 16.9%.

I do not have the correlation between premiums growth and EV growth for the industry, I wish I had more information like these to make further decisions,

- Indian insurance industry EV history.

- Global insurance industry growth, product mix history.

- Policy Holder database, House Hold information, net worth, unique policies etc.

One will also need to link these growth assumptions of the next 2 decades with the insurance penetration levels in India. Remember insurance is a pull product, discretionary if you will. The population needs to rise to a certain wealth standard before they consider insurance as a finance tool.

I have discussed about insurance penetration in detail in the following twitter thread which I have copied below. Thread on Insurance Penetration

Insurance Penetration

Where is the under penetration in Life Insurance in India? We are neck to neck with China, US, Australia and close to Asian Average.

Sridhar Sivaram of Enam has also pointed the same. Industry growth going forward will be similar to GDP growth.

Privates taking over the market share from LIC, is that all the valuations are standing on? Can LIC compete in a similar manner for, ever younger, tech-savvy, service and time-sensitive customer?

Outliers

Here is another evidence from Swiss RE Sigma

Life insurers as of Sep. 2019 are trading at 3-4-5 P/EV while global peers are trading between 1-2.5. The industry grew premiums by 8% CAGR in the last 5 years and privates grew by 16% CAGR. Now doing an implied DCF for 20 years, assuming a generous growth 20% for 1st decade and 15% for the next decade on EV with an exit P/EV multiple of 1x, at the current P/EV of 5/4/3 the market is implying a return of 8.4/9.6/11.2% CAGR.

Even if we increase the EV CAGR to 25/20% for 1st/2nd decade, the returns are 13/14.3/15.9% CAGR.

Since the liberalization of the Indian insurance sector, the Indian insurance sector has grown from a total premium of 454 bn in FY01 to 5,494.5 bn in FY17; this translates into a CAGR of 16.9%

Most analysts cite India’s low % of the premium to GDP (~3%) against the world average of ~6% to say we have a huge runway for growth. Here is a counter - We are almost equal to US, Germany, Australia, & China. Where we are really lacking behind is in Non-life.

Yes, the world average as per IRDAI in the above tweet is at 6%, but the key point to consider is that is it a weighted average of all markets? A weighted country market size average is a much more relevant figure to compare with because individual countries which may be small in global insurance market may have outlier penetration levels, the reasons for which I haven’t yet researched but it could be due to lesser number of people per HH, regulated mandates, inequality differences, increased threat to life/property, natural disaster-prone regions, etc.

We rank low in density figures because our GDP/capita is low & if we remove rich India then the figures are abysmal. Yes, we may have 20x difference to some Developed Markets, 4x to China & 7x global averages but our GDP/capita is also lower & the densities will only increase when GDP/Capita increases.

If anyone has researched beforehand why France, South Africa, UK, Hong Kong, South Korea and Taiwan are such outliers in terms of penetration please do share your wisdom with me. Really eager to learn why this is so.

See Interest over time on Google Trends for life insurance - India, 2004 - present - Google Trends

The above google trend for life insurance is what baffles me, since 2004 we (India) have only increased our internet users and online purchase of insurance year on year, & still, the interest in the term has reduced.

Conclusion

I hope I have convinced you enough about the need for picking conservative entry/exit multiples and growth scenarios in my expected return table. As per my readings, growth scenarios 3, 7 and 8 are good starting points. Scenario 4 is too conservative. As for exit multiples, no one knows the future but conservatively one can hope for an exit multiple between 1.5-2 in a 10-year exit and 1-1.5 in 20-year exit scenario, given at what insurance companies in developed markets trade at. Anything beyond that is stretching the limits of imagination.

These are long timeframes, nothing is guaranteed, the profitability of the entire industry, let alone the growth rates could change drastically for all we know. Future product mix will also have a significant impact on the valuation of the company. The industry is notorious for mis-selling, such tactics can boost short term profits and commissions for the employees but can never build long term relationships with customers.

EV is a single valuation metric which has many many levers determining its value. If you have a look at the sensitivity tables that each insurer provides you will see that it is sensitive to equity market movements, persistency rates, operating expenses, mortality and morbidity assumptions, tax rates, and interest rates. Trying to forecast these is a tough task even for the management. Hence, the need for asking a margin of safety even in the management’s calculation of EV.

The entry multiple is the only factor in our control from all of the above. We can choose to ignore the industry/investment until the valuations reach our comfort zone. Investing is one field where it pays to stay in your comfort zone.

Caution - In the short term market exuberance could prove me wrong. Few people could still make money on recent investments in Indian listed insurers.

20 Likes

Thanks for the long write up. I will be short and crisp. According to me, penetration level for life insurance in India have no meaning at all. That’s because most of that level is achieved by years of mis-selling of type of insurance as well as sum insured. Actual Insurance is pure protection, rest of it doesn’t matter to anyone in long run, not even consumers. Life Insurance penetration have just started in India with the adoption of protection.

Regarding valuations, I will not comment as I am not sure about dynamics in other countries and you have presented a very good comparative analysis. They do look pretty high even when compared to developing economies.

Pls do share if you have anything to share on how to value Indian life insurers correctly. Also in the comparative analysis, it will be good to know the type of Life insurance being sold in UK, US, Developing countries and its ratio in terms of pure protection, market linked and the sum insured value analysis. Only then, we can do a meaningful comparative analysis I believe

Thanks

4 Likes

Thanks for sharing your knowledge about the industry with us. It is indeed necessary to look at the industry from a POV of mis-selling.

It raises a few questions to which I don’t have all the answers,

- How much of the current premium/AUM/EV/PAT is generated from mis-selling?

- The customer has been introduced to the insurance product, even if they were mis-sold the product if they continue with the right product with the industry, does that change the penetration levels of the industry? IMO, No.

- How much difference in profitability does traditional vs market-based products make for the companies? Maybe the answer is there in this forum. Any researchers who have deep-dived into the industry can help.

Combining all of the above, if tomorrow, hypothetically the mis-sold policies change to pure protection, what will be the impact on EV/AUM/PAT and penetration levels?

There are 3 scenarios to the above,

- None of the mis-sold customers come back immediately,

- Some of the mis-sold customers come back immediately,

- Most of the mis-sold customers come back immediately.

In scenario 1, what you have said would be true, insurance penetration levels today would be meaningless. It would also mean the current valuations and EV are over-stated. I am not sure of the impact of 2 and 3 on the valuations as I have not yet studied the effect of product mix on profitability.

Your suggestion is interesting that we should also do a product mix analysis for global peers before comparing EV multiples. I am not sure of the ROIT (Return on Invested Time) in such an exercise. Intuitively, with my limited knowledge, I would hazard a guess that the low P/EV multiples in DMs are more due to lack of growth prospects rather than a bad product mix.

As for the correct way to value a life insurer, I wouldn’t even dare to try it with the limited information we get from the companies and IRDA. How can an outsider value an insurer without going through individual policy-level data? It is the same with financial companies, how do you value the book without going through each loan. All we have are management’s estimates to EV and BV in case of financials.

If you mostly trust the management’s ability, one can assign a multiple to these factors, but not without a margin of safety and a basket approach.

Yes, this all leads to a very conservative approach, and I may not be able to enter at desired entry points soon, but one must remember in markets that a perfect storm is a certainty. Just as it is for financial now, I believe a similar day will come for insurance companies. Risks currently not priced in will show up eventually and will get overpriced. If the cyclical lows in valuations come with low growth scenario for the industry, I will have to validate my hypothesis on growth potential before jumping in.

2 Likes

I would again say that the penetration exercise for Indian context will not hold much value. Also, any comparative global analysis will me more meaningful if we consider product mix and various other demographics. It is sometimes thought provoking that none of us know the correct way to value Insurer but we all know that they are overvalued in India ![]()

Having said above, the analysis you have done in your blog is one of the most detailed and comprehensive analysis that I have seen so far.

Also, regarding the crash in prices - we did have a major blip in Insurance companies in recent fall, but that was short lived. Now, what can trigger major long term blips for Insurance - What are the corresponding NPA, Provisioning, Asset/Liability or Liquidity issues for an Insurance firm…is something to think on.

It can be major underwriting issues, float invested in risky assets, management playing with books…now if we think a little deeper…all these issues are majorly dependent on only one variable…that is self discipline…unlike in banking where the variables are more…a decent market leader company to which you have provided loan can go bust which is totally out of your own control…liquidity issues are also not in self control…

What are the variables for Life insurance industry which are out of control of management’s self discipline?

Thanks

3 Likes

Hack2abi

Thanks for compiling the data ![]() .

.

I am sharing some counter points.

-

You are conservatively assuming exit multiple of 1-1.5x EV after 20 years. Consider this- GDP per capita of China is 4.5 x that of India currently. Even if we grow GDP per capita at 7.5% pa for next 20 years, and China grows at 0% pa for next 20 years, we cannot cross China’s GDP per capita figure. Wouldn’t it be fair to have exit multiples closer to the Chinese multiples of today?

Growth after 20 years- Why assume growth rate of zero after that? -

Absolute valuation vs relative valuation- If you perform any companys valuation 20 years back only with the data which was available then and do a valuation for that same company now, you would notice that current valuation multiples taken would be higher. That is because valuation as an excercise is relative to the amount of asset inflation there exists in the times. The risk free rate in current times is much lower than the risk free rate say 20 years ago. 20 years from now - who knows how much asset inflation would be in place to drive growth and stimulate demand?

-

Non linearity of markets- Share price chart of most High Growth companies is not a straight line. Once a fair amount of predictability and certainty is known to the market, market keeps discounting future earnings into todays price upon every announcement of growth in results. Many examples in the past- Infosys, Page, Dmart. Hence would it not be a better way to simply keep remain invested in the stock till the time the growth falls. Many famous investors like Phil Fisher, Basant Maheshwari have shown that this strategy can produce multi year multi baggers.

-

Growth of Sector vs growth of stock- If you take the credit growth of India for last 20-25 years, it hasn’t been as high as the growth of the advances of HDFC Bank. Conversely shareholder returns of HDFC Bank have been far higher than that of the sector as a whole.

-

Premium for innovation- 20 years back who even could have thought that these companies would have a very large role to play in the pension scheme of India? Could anyone predict products like insurance against cancer and other diseases? Similarly 20 years from now we might see some of these brilliant companies innovate and launch even better products. Maybe technology will bring down life expectancy, cost of promotions, commissions.

Sure, a valuation based on some reasonable assumptions would provide some reference point so as to future returns for a business. But a rigid approach purely based on valuations and ignoring qualitative parameters has prevented many investors from hanging on to multi year multi baggers even when they were right infront of their eyes.

Disc- Invested in HDFC life since IPO.

3 Likes

Vegeta San,

-

Investors exist in a spectrum of conservative to aggressive. Maybe I am at fault for letting my conservatism bias seep into the model I built. The reverse could have been true that I would have built-in aggressive assumptions and someone more conservative than I would have called that out. I think I have explained the reason for my conservatism in the model due to the number of variables that are just so difficult to forecast. Still exit multiple after 20 years still goes up to 2x. Maybe I am right maybe I am wrong time will tell. I tend to focus more on how bad my returns in such long timeframes can be rather than how good. This gives me some control over my downside in an investment, upside for most investments is unknown and uncontrollable. We are not assuming growth will be 0 after 20 years. Exit multiple of more than 1x is proof of that. It is difficult as it is to build reliable models over 1 or 2 decades. 2 decades is my investment horizon for now. One can build a more aggressive and longer model for themselves as they wish.

-

Your point reinforces my last statement, difficult to forecast beyond 2 decades. If I understand the interest rate sensitivity in the insurance industry, it affects the future liabilities and assets similarly. In a future low rate world, insurance companies will find it increasingly difficult to generate a return on their float. This will impact shareholder returns and thus the future value of the companies. So net-net these should balance themselves out.

-

The last line of caution in my blog refers to this. I believe the probability of me being proven wrong in the short to medium term is high. But in the long term, I believe chances are in my favour that I am correct. For the sake of my fellow investors, I do hope I am proven wrong even in the long term and everyone invested makes good returns to their satisfaction.

-

You are absolutely right, there is a case to be made for value migration, and capturing incremental market share. This is a topic that would require an entire blog post in itself, we have seen only 19 years of insurance industry privatization, the dominant private players have reached a certain scale of operations that are needed to be profitable in this industry. We will have to see from here on for the next 5/10/15 years whether they capture an increasing share of the industry. The banking industry was a different game IMO where the level of service standards was starkly different between the privates and public. Another differentiator is that the public competitor is concentrated and focused in the insurance space whereas in banking they were disorganized and lacked leadership focus. The incumbent will not sleep as it loses business, it will compete to the best of its ability. Which faction and which private will beat the model, is a question to which no one can answer currently. If one does believe their investment company is the winner, they can choose the higher growth scenarios in the model to account for that.

-

You are right about innovation and disruption, but it difficult to predict and model them into a single variable. There is a great video from A16Z on youtube which discusses how fintech is altering the paradigm for the insurance industry. Very interesting stuff.

Thank for bringing in good qualitative arguments. Gives me a lot more vantage points to think from. The model I presented provides an ample spectrum of scenarios that one can use with any number of qualitative stories.

3 Likes

Very interesting Points . Some points I think are worth pondering related to Life Insurance

- Penetration : I agree with you on this. Life Insurance becos of LIC aggression and strong incentive / promotion programs is penetrated deep in hinterlands - But can it grow Yes as Income / Wealth effect grows - Insurance cover ( incl Saving led Insurance ) can grow typically GDP + Inflation Gr That is if Insurance premium had no substitutes

But Insurance premium ( saving ) competes strongly with Banks FD and Mutual Funds … The more the substitutes do well in penetration esp MF - Insurance stands to lose Saving component ( real profit driver ) -

- Market Share shifts : Private players gaining at expense of LIC like Private banks did- If one looks at PSU banks loss over long term has been becos of lending mistakes often forced by system … These lending mistakes put brakes on growth capital . While Deposit Gr was never an issue . For long term policies people will trust sovereign rated entity more than private players … So LIC has huge moat there and hence in worst times LIC will gain better than Private players … Also because of aggression / targets but policy settlement in private players has been more customer unfriendly

It is only in investment float Private can beat LIC … but private players have no performance record to boast … Lets see if Private can beat LIC with people strength … For that LIC has to do lot of blunders - I see great stability in Mks across Private and public players in coming years …

- Valuation : It is difficult to decide single metric as each Insurance is at different level of maturity curve in terms of product mix and System/ people investments - You have great job in painting various scenarios …

1 Like

Given the dynamics of the industry what should be the bull case, bear case and realistic case in the near term?

compared the quality of growth and quality of assumptions for the top 3. some obs/questions -

A) ICICI’s interest rate assumption is the least amongst the three - which means PV of liabilities is > in comparison to that for SBI, HDFC and hence, VIF component of EV maybe understated (?)

B) ICICI’s EV has grown at the slowest pace despite clocking highest VNB growth - is it due to the Product concentration effects that ULIP has (?)

c)SBI Life has seen constantly seen positive surprises in operating variances - which probably speaks about the quality of assumptions that are being used (?)

Interesting observation! Either most of fatalities are among folks who don’t care or just folks who can’t afford. It is clear that penetration is low for life insurance or I would say term insurance.

1 Like

Some key questions to those who track this space closely -

-

What happens to mortality assumptions for existing policies as mortality escalates for folks in the 40-60 age range?

-

What is the likely impact on investment portfolio for assumed long term profit growth from investments as interest rates continue to drive down

-

Impact of increasing term policies? I know this would impact their margins but overall premium collection will also weaken. I think term policies will jump substantially as Indians being value conscious will prefer low cost solutions.

-

Lockdown has been good for life insurance sector so far since well to do folks can afford to remain indoors but it is opening up and I see many healthy folks are getting this virus. I personally think mortality will jump in Q2 as infections spread becomes more widespread.

Disc: I am out of all insurance stocks and will wait for fundamentals till the first half.