I have a query about how value is assigned to life companies in the market

Among the 3 large private life insurance companies icici life looks reasonably valued compared to sbi and hdfc

Icici’s business size is similar to hdfc and sbi in terms of ev, vnb and vnb margins but it is available at a 40-50% discount.

Their share in retail sum assured is just marginally below LIC, they have build out a good agency business and have little dependency on the parent bank, doubled vnb in the last 5 years

Hdfc will have good growth because it will become a subsidiary of the bank but they will probably suffer from the same restriction that icici bank had with icici life where the bank prefers non par savings to not be sold so there is less compitition with fds

I looked over the last 3 years earning confrence calls of icici life and while they have been over cautious on non par savings ex ulips they’re reasoning was because they were worried about implications on the balance sheet. It looks like a conservative management which is good in life insurance

I don’t understand why icici is so cheap compared to the other two, if the sector itself has a massive runway of growth the top players should participate unless the management is completely incompetent

IMO no analyst, no retail investor and very few people within these organisations itself understand Life or be it any insurance business…

In such extreme uncertain scenario, valuations tend to favour groups with long term stable history or superior growth, network and backing.

Without any doubt, HDFC group has one of most stable history among financials and SBI Life has backing and network of numero uno Indian bank SBI inspite of having a somewhat private company DNA. Not to mention the superior growth so far compared to other two…

The other aspect is the kind of risk one company takes to achieve the same growth. One possible way that would be evident in Life insurance companies is via their product mix. Maybe you can get your answer by evaluating each one’s product mix and the kind of growth they achieved via same.

Disc. Invested in HDFC Life and SBI Life hence biased. Can be completely wrong in all my assessments. Above views only for academic purposes and not a buy/sell recommendation.

I have been wondering the same… My guess - a lot of people still look at insurance companies from the growth in sales/ profit (premium growth n PAT growth) and not in terms of EV or VNB added. On those parameters you may find growth to be a challenge

I have gone through the thread, but one thing I find missing is any mention of some assets which LIC has, which are ignored in our assessment of its value.

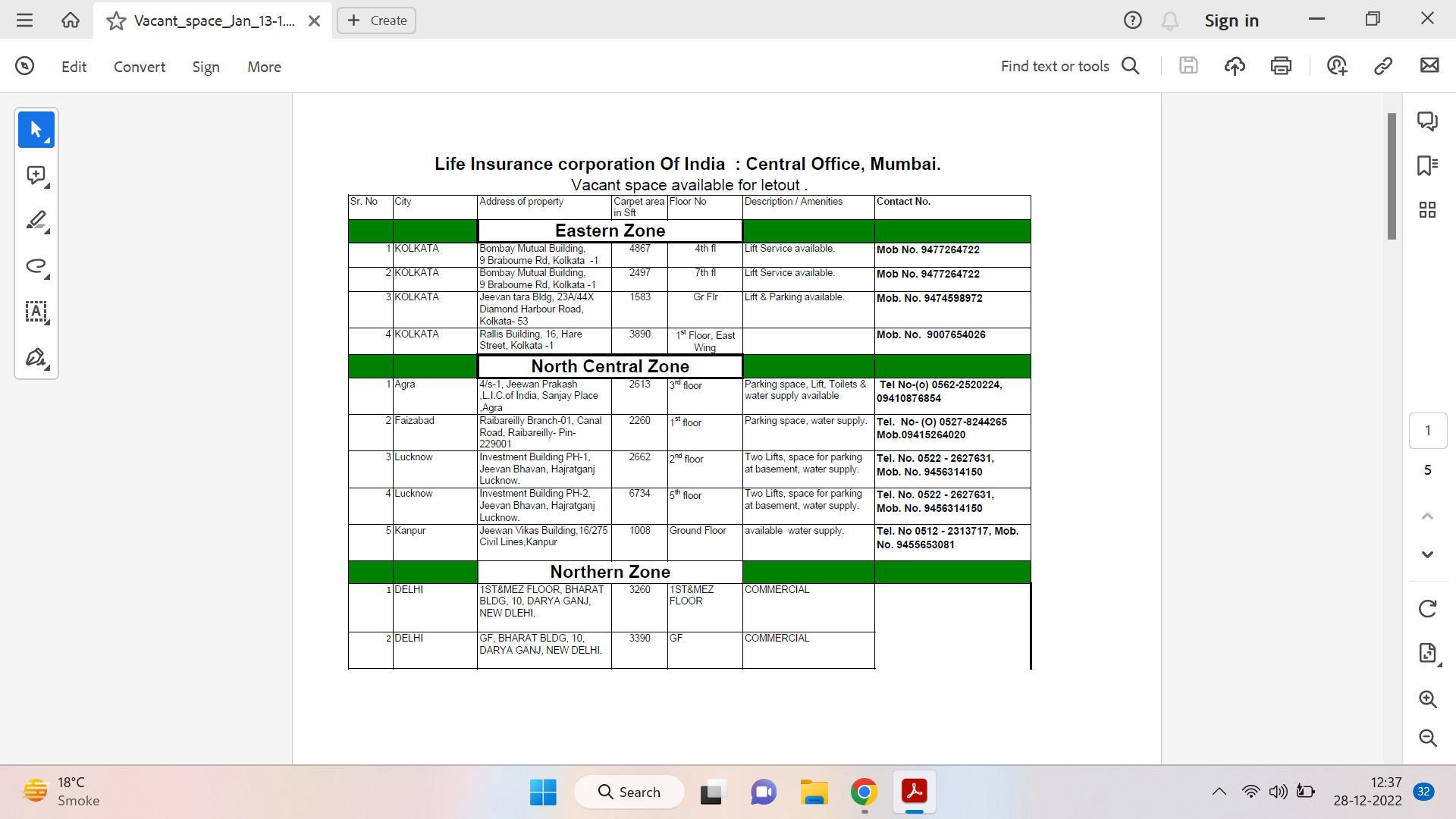

As somebody who lives in Delhi, I am familiar with many landmark buildings owned by it in prime of prime area of Delhi. Jeevan Bharti, Jeevan Prakash, Jeevan Tara for example, are located in Connaught Place, Parliament Street, and some others at Bikaiji Cama Place, and Nehru Place.

As per the ads put out by LIC, it has buildings not only in Bombay, but at as rather lesser known place like Dholi in Muzaffarpur.http://www.uniindia.com/lic-owns-186-buildings-in-mumbai-ipo-on-track/business-economy/news/2598103.html

They are everywhere, from Srinagar to Portblair.

Bombay needs another mention. It has buildings in areas that can only be dreamt of.

Such is the extent of the vast number of buildings they own that even LIC does not have a correct idea of their count, leave alone their value.

I have found a very old figure of ₹70,000 crore value put at these buildings.

Many of the buildings were constructed way back in 1950s and 1960s. LIC building in Chennai for example, constructed in 1959, was the tallest building in Madras of those times. Mind boggles at the multiplication in their value.

Of course, being a PSU, it suffers from the common malaise of inefficiency. This is what have found:

Sources said that the land was purchased to set up an `investment building’ either an IT park or a commercial complex to be rented out. While a large number of the LIC’s old properties are non-performing assets generating rentals of less than Rs 10 per month, new properties are generating decent returns.

Agreeing with LIC’s predicament, a well-known real estate consultant pointed out: “Some of LIC’s existing buildings are lying vacant, for exbut since the buildings are old and lack plug-and-play infrastructure , companies are reluctant to rent them and instead prefer new buildings coming up at Ballygunge, Lower Circular Road and even Salt Lake,” a real estate consultant pointed out.

Currently, LIC owns nearly 1,571 properties in India and some overseas. Of these, some 374-odd LIC real estate portfolios are primarily investment properties. It also has some free-hold lands in metros, a majority of which will be used to house offices or employee families. The surplus may be used to boost the firm’s rental income.

Read more at:

In addition, they have paintings, some of them by iconic names like Hussain (one of his 1958 paintings has sold for 18.5 cr recently) and Hebbar (one of his paintings was recently auctioned for ₹ 51,65,160) , bought at throw away prices long back. LIC realised their value only when Hussain wanted to buy them back.

Peter Lynch has this to say in his One up on the Wall Street:

THE ASSET PLAYS

An asset play is any company that’s sitting on something valuable that you> know about, but that the Wall Street crowd has overlooked. With so many analysts and corporate raiders snooping around, it doesn’t seem possible that there are any assets that Wall Street hasn’t noticed, but believe me, there are.

The asset play is where the local edge can be used to greatest advantage.

The asset may be as simple as a pile of cash. Sometimes it’s real estate. I’ve already mentioned Pebble Beach as a great asset play. Here’s why: At the end of1976 the stock was selling for 14½ per share, which, with 1.7 million shares outstanding, meant that the whole company was valued at only $25 million.

Less than three years later (May, 1979), Twentieth Century-Fox bought out Pebble Beach for $72 million, or 42½ per share. What’s more, a day after buying the company, Twentieth Century turned around and sold Pebble Beach’s gravel pit—just one of the company’s many assets—for $30 million. In other words, the gravel pit alone was worth more than what investors in 1976 paid for the whole company. ose investors got all the adjacent land, the 2,700 acres in Del Monte Forest and the Monterey Peninsula, the 300-year-old trees, the hotel, and the two golf courses for nothing.

…Hundreds of thousands of California commuters drive by the Newhall Ranch every day. Insurance appraisers, mortgage bankers, and real estate agents involved in the various Newhall deals certainly knew of the extent of Newhall’s holdings and of the general increase in California property values. How many people owned houses in the areas around the Newhall Ranch and saw the great escalation in land values, years ahead of any Wall Street analysts? How many of them considered researching this stock that has been a twenty-bagger from the early seventies and a fourbagger since 1980? If I’d lived in California, I wouldn’t have missed it. At least, I hope I wouldn’t have.

…Right now I’m holding on to Liberty Corp., an insurance company whose TV properties are worth more than the price I paid for the stock. Once you found out that the TV properties were worth $30 a share, and you saw that the stock was selling for $30 a share, you could take out your pocket calculator and subtract $30 from $30. The result was the cost of your investment in a valuable insurance business—zero.

Was Harshad Mehta right when he talked of replacement value? How much would it cost to build a company like LIC now?

I may be wrong in supposing that the LIC should not be valued for its premia or the investments in stocks only, but also for the large real estate and paintings it holds. Whether it actually monetises them or not may be an issue.

In many cases, its buildings are in bad shape, or in occupation of tenants who pay it a pittance. Government departments for example. So, lack of any will-power to improve and monetise these assets may be a disincentive for a prospective buyer.

Disclosure: I have a small holding in LIC.

How one forgets one’s credo written in stone! One of them has been- never invest in a public sector bank or even company.

The LICs or PNBs seem to lurch from scam to scam. Why do LIC, SBI continue to invest in Adani group, Opposition asks - The Hindu

I think LIC is done. What about the Public Sector Banks? LIC is invested in the Adani Group. However, the public sector banks have given loans to it. So, I feel both are on a different footing.

Disclaimer: I have made recent investments in both LIC as well as the PSU banks including Canara, BOB, Central Bank.

Name of Power Finance Corporation has not cropped up, but it may well have invested in Adani Power. I have that too.

There are percentages and absolutes. 80k cr investment seems a lot but in the context of the 41 lakh crore portfolio of LIC this is miniscule.

In the par policies losses are passed on to policyholder while lic keeps 10%

I have made recent investments in both LIC

Everything about adani mentioned in the report was already known and so was LICs holding so this should not have come as a surprise

However, the public sector banks have given loans to it.

As far as we know the Indian banking sector has only lent to secured operational assets of Adani and working capital

The foreign banks are the ones that have supplied adani with a huge amount of loan against shares in dollars

According to CLSA Indian banks have financed 30% of Adanis net debt and that translates to 0.7% of public sector adavances and 0.3% of private advances

All this was already know. As long term investors we should not let price influence or judgement of the fundamentals of a stock

Note: not invested in adani or PSU banks and have no plans of every doing that

Have a position in lic and not worried about the recent news

Any idea if todays mayhem on the Life Insurance companies is really called for?

So the change is, anyone paying more than 5lakh a year in Insurance Premium, won’t get tax exemption at the end of the policy period, accompanied by the change in taxation slabs and the new tax regime giving no exemption for Insurance Products.

Since there is a lot of uncertainty today, I have 2 questions if anyone can answer them.

How many people pay more than 5lakh in Premium a year? and

How much will the change is taxation regimes affect the growth of the Insurance Products?

Either way, with these changes we will know how mature is our insurance industry . This is will instill confidence of the growth of the industry going forward.

watch vibha’s interview with cnbv tv 18. you will get your answer.

Thanks for the suggestion.

Although I am no expert, but looks like there were expectations from budget by Insurance firms (have been since few years). However, there was unexpected bouncer instead in terms of fillip for New tax regime & added tax on high value traditional insurance policies. Sentiments did get damaged and market punished the stocks very well. Also, I noted that insurance stocks had been rather steady last few months compared to some other sectors, so broken down really well.

Good question. Honestly, until today, I was not aware that any insurance policy has earnings non-taxable also. If anyone aware which are such policies and under which section these are tax exempt? I was only aware some ULIPs are tax exempt under 80C and that too not the earnings from them but the sum we invest in them per year (Pls correct me if wrong).

Excellent question. And I think this is more important to me personally. Its a long journey for people to mature and look at insurance as insurance. Pandemic provided some catalyst and I think this new regime push can provide another (I may be wrong). But now, insurance firms will be forced to sell insurance sans tax benefit pitch. In long run, this maybe welcome for society. (Again I can be wrong).

That’s an excellent Bingo statement again. However, when coming to stocks & valuations, we may have to bear some pain till things clear out. How long will it take, I don’t know.

Disc: Invested (around 8-10% of portfolio in Life Insurance firms) hence biased & critical. Not a buy/sell recommendation. I can be completely wrong in all my assessments

At least the medium term outlook is not nice. Most around me invested or their parents made them invest just for tax purposes. The impact will definitely be there and one has to be conservative.

Vibha Ma’am’s interview for reference.

Only thing we can do is monitor next few quarters to see what kind of innovation do these companies come up with now.

I personally am evaluating my current holding and deeply inclined to join the sell side.

Disc: Invested.

Although I am not good in numbers, one way to look at it can be to -

- Check how much growth these Life insurance companies get in Q4 as compared to Q1, Q2 & Q3 as Q4 is run up to close of Financial year.

- Then Check, how this delta growth trend has been in last few years. Is the delta progressively reducing. If yes, that might imply lesser number of people investing in insurance for tax savings…at least at last moment at close to end of FY.

- Check the growth and mix of those insurance policies that come under 80C only as part of overall growth and product mix.

- Again check the progressive trend for Point 3 over the years.

Also, above exercise needs to be done for each Life Insurance firm individually, because the target consumer for LIC maybe different as compared to HDFC Life or rather the buyers who target LIC maybe different as compared to HDFC Life.

If someone is really able to manage above numbers, will be great insight and helpful, Thanks

Disc: Same as above

Tax benefits have not completely gone. 80C still exists. ULIP still exist. (Old regime still exist and those who want to invest for tax benefit + Insurance still have that option). As per interview, even traditional policies upto 5L aggregate premium still is exempt. Also, important point mentioned in interview is that tax benefit was not only reason for affluent Indians to invest in such policies - their another USP is certainty of interest rates. During Pandemic times, all got taste of low & volatile interest rates so I agree with Vibha ma’am in interview that affluent Indians would like some part of their debt savings to have a certainty of interest rates over very long term, irrespective of taxable nature.

Also, hypothetically, if say everyone moves to new tax regime, which have no deductions, will people stop investing completely in products that would have fallen into 80C earlier or buying Insurance? In best interest of all, consumers should be educated with benefits of each product for what they are…and each product, be it Insurance (different type), NPS, PPF, EPF, ELSS etc. have their unique advantages (and disadvantages) than just Tax benefits…and I feel Insurance firms have this task in hand now to rightly educate consumers.

Swift distribution & digital channels can be enablers. Overall I feel this is good for the ecosystem and future roadmap of Insurance in India. Also, composite license is a big welcome as well for Life insurance firms. Stock valuations is another story though, which I am not good at.

Disc: Same as above

Maturity amount of Insurance policies come under section 10(10D) of Income Tax Act 1961. Hence maturity amount is totally tax free. Currently only two Investmemt products in India are Tax free at Maturity…One is Life Insurance policies and second is Public Provident Fund.

How do i get total insurance premium data of last 5 years (Life+non life)?

You can get it from IRDA website, where all companies declare their financials.