Reserves is a non-cash accounting entry on the liabilities side of the balance sheet. The company can only use cash on its asset side for capex or any other expenses. (I too had a similar confusion about reserves when i first started investing)

8 Likes

I am bit novice in understanding Balance Sheet. So, Does this imply Laurus Labs does not have 3918 Crores in Cash as reserves?? If yes, what the point of showing some amount as reserves?

Normally, Lesser demand lead to higher Inventory build up and higher receivables. So i believe with demand returning back, the high inventory and high receivables will normalise. More, Important thing is they have used one time Covid revenues (Paxlovid sales) to build future capacities.

2 Likes

Reserves is part of EQUITY in LIABILITIES side of the Balance sheet. Liabilities side on the balance sheet shows how the assets are funded.

1 Like

This is “hey are little more conservative when projecting the future” this is conspicuous from recent concall.

Laurus has come out with a detailed investor presentation. FY25 seems to be the year when they will probably reap the harvest!

Link to presentation - here

10 Likes

My notes from the investor presentation and earnings call:

Business Moat

They are moving up the value chain quite fast. The moat is improving with their aquisitions on gene therapy, precision fermentation etc.

Their R&D investments would bear fruit in FY25.

With successful execution of a large PO worth $150 mln, they have proven their capabilities in the market to deliver high quality and large scale projects. This would enable more high value projects to come in future.

Revenue growth prospects

Current revenue growth will be subdued as they are undergoing operational deleverage. Also the previous year had a big purchase order that was executed.

In 2 quarters, this should turn around and we should see revenue and margins pick up.

Their oncology segment had seen a good growth and the run rate is expected to continue as they have order book well beyond Q4 (from earnings call).

Employee growth & review

Quite good employee growth in last 2 years. It is still close to 10% in last 12 months. Their R&D manpower has increased considerably.

Their employee review in Ambitionbox is quite good as well.

Product Portfolio

Product mix has improved considerably since FY18. ARV contribution has come down from 73% to 37% while other streams picked up, especially CDMO.

Capex

They have 500KL additional capacity coming live in FY24. Not sure if it is reactor capacity or fermentation capacity.

Almost Rs 2.5 billion is being spent between FY22-24 for CDMO R&D, CDMO manufacturing, FDF and APIs. About 60% of the capex is yet to scale up.

Margins

EBITA margins have dropped significantly from 32% in FY21 to 15% in FY24. The management attributes this due to higher upfront costs due to operating deleverage. The gross profit margins were however a little stable.

New markets

Venturing into new markets in South Africa. Won India NACO tender. However, the market size will be quite small compared to developed markets and the impact will take some time to realize.

Looking to monetize US/EU pipeline opportunity of ~US$ 80bn, majorly in non-ARV space.

More than US$35-40bn of drug brand value expecting loss of exclusivity in 2026-2033.

H2 Priorities

- Higher capacity utilization across network to support growth acceleration,

- Scale up of the new Animal health commercial asset and

- Continuous improvement initiatives

Investment hypothesis

I am expecting these to play out over next quarters.

- New capacity comes live and capacity utilization goes up

- Demand revives after destocking last year

- Operational leverage kicks in and margins improve

- CMO & CDMO pipeline picks up → higher revenue & capacity utilisation

- Share of revenue from innovations go up → higher margins, business moat

Disc: Invested

13 Likes

Dont you think business model is changing every 3-4 years and company has to re-invent itself every 3-4 years?

3 Likes

I think that is the nature of most businesses in this sector. However, I see Laurus to be a bit more aggressive in moving up the ladder and trying new things. If I look for the next Pfizer kind of companies in India, Laurus definitely comes in the radar.

The main concern is the cash burn in these activities. In that, I see two major streams of capital deployment:

-

Business model / product mix changes, requiring constant influx of capital, which can be expected and should be seen alongside the growth rate of company. I see Laurus having a good leg of growth coming ahead.

Their focus in CDMO is actually good. However, CDMO being a lumpy business can bring down the biz performance during lean period. Nevertheless, this is a good & necessary long term plan to match competition - Capex initiatives yielding fruition → This I am much keen to follow up since it has a twin benefit of improved revenue and margins (operational leverage). As per the mgmt, the demand looks good and inventory destocking should be over. So, there is a high likelihood that volume & capacity utilisation starts going up. Unless it does, we can’t expect the margins to move to a healthy level as mgmt mentions.

Snippet from earnings call below:

12 Likes

Not necessarily that all pharma companies are changing their business model this frequently.

I hold two other pharma companies :

- India centric Abbott India ltd…This company sells medicines in India. Its leader in many categories and its business model is quite robust as well as constant.

- API low cost producer Divis Labs…This company also has proven and profitable business model. Due to sudden opportunity lost of covid drug, this stock has also come down more than 35%, but its business model is intact and not much difference…Its on track…

So not all companies in Pharma sector are changing their business model so frequently like Laurus.

3 Likes

Hello.

Let me put my investment thesis for Laurus Labs. What I like

The co is founded in 2005 and has achieved a lot in last 2 decades

- Crossed revenue of 5000 cr

- Market cap of 20k cr

- Scaled up the ARV business very well

- Ventured into other businesses like Other APIs, FDF, CDMO, Bio, Other new therapies (Immuno act, etc.)

- CDMO business from marquee clients. Co, was able to win trust of CDMO clients . Speaks volumes about the quality of the capability and the leadership

How many cos can grow and create wealth this fast ? (question to self)

How the future looks. Lot of positives

- Well diversified revenue streams: ARV API, Other APIs, ARB FDF, Other FDF, Bio (mostly food grade), CDMO (Most value added), New therapies (Optionality and possible new revenue stream)

- Base is lower now considering the headwinds the co has faced last year and also at present

- Deliveries to start for CDMO projects and ARV orders in had for 2024, 2025 (2026 ?, need to check the recent investor presentation)

- Operating leverage to kick in considering some costs are front ended and margins to improve with contribution from CDMO business

- More than 50 (as per my memory) CDMO projects in different stages

What I don’t/didn’t like:

- Management not upfront about One off revenue, but now using it to their own advantage (while comparing numbers. Refer latest investor presentation)

- Going into FDF. I thinking they are filing some Para-IV s as well. Conflict of interest with CDMO customers

- Not sure about the management bandwidth to grow all the businesses. Not sure how well Dr. Chava can delegate the responsibilities

- Volatility in business and margins. CDMO revenue would also be lumpy (of course). ARV deliveries also are lumpy as per me

- IMO Valuation is not attractive even at current price

- Last 2 years co. didn’t walk the talk. Need to see how it goes going forward

Short thesis:

The co/management has created wealth for the shareholders at very fast rate. Hunger for growth is there. Good capable management (Could be better). Could be one of the biggest wealth creators in next 15-20 years. Only time will tell

Disc: Small position initiated today. I’m opportunistic with what/when I buy/sell as per mid term estimate valuation of the co. No reco my any means

15 Likes

The risk of USFDA has played out … 5 observations with form 483

check the details below…

Laurus_USFDA.pdf (390.1 KB)

7 Likes

Is there any way we can know what these observations were & there severity?

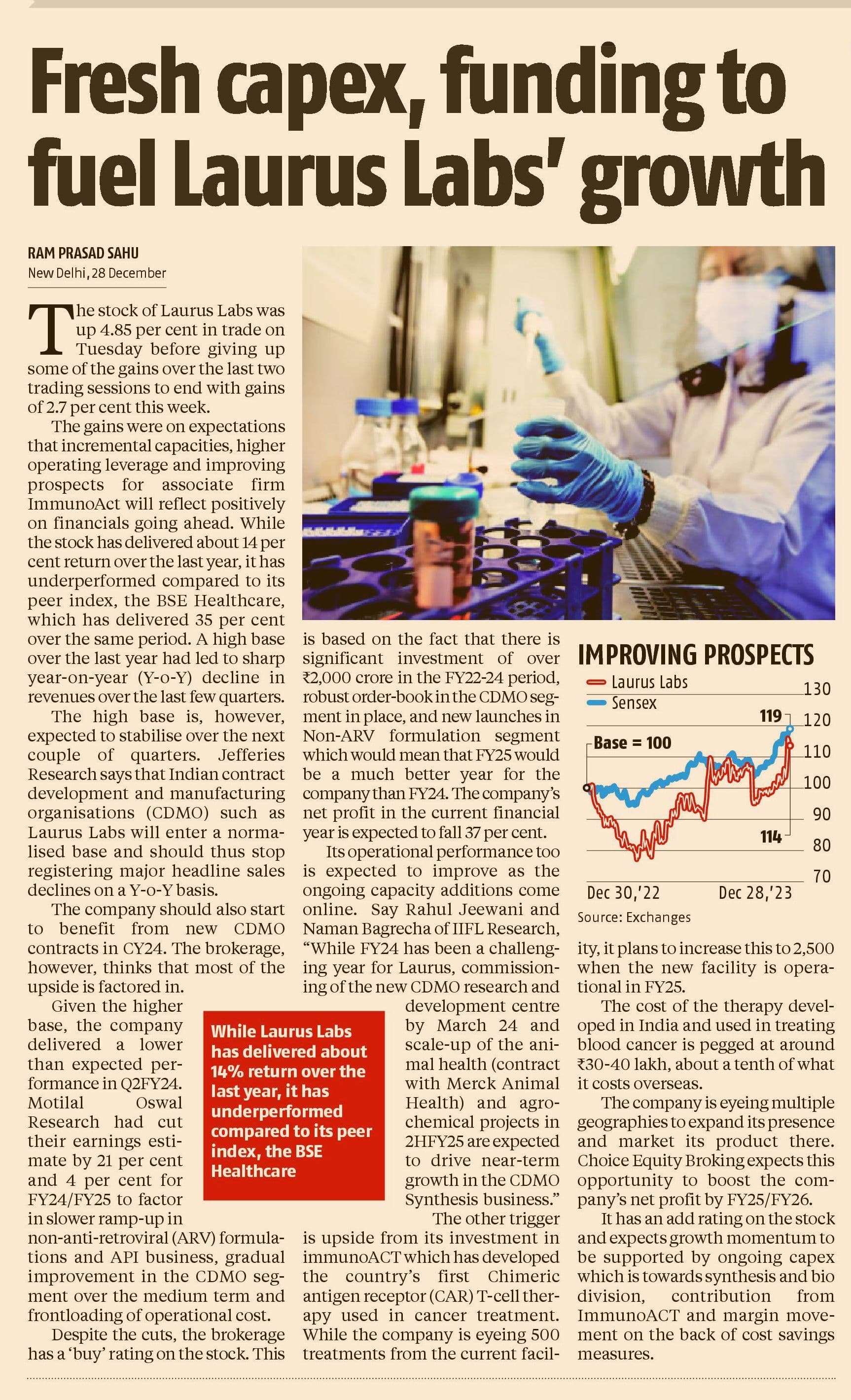

Chava is making bigger and bolder bets. In the last three years, he has invested more than Rs 2,000 crore, in what qualifies as the biggest investment in the sector, to build facilities for contract research and manufacturing services as well as put up fermentation plants for biotechnology intermediates. The only other pharma player to come close is cross-town rival Aurobido Pharma.

This bet is significant as, traditionally, large domestic pharma companies have shied away from investing in contract research and manufacturing services:

First, because the business entails large upfront investments to demonstrate capability, and

second, multinational companies have never quite trusted large Indian companies that copied and sold many of their patented drugs in the domestic.

9 Likes

Only time will tell if the management’s bet on the synthesis business will benefit the company and its shareholders in the long run ![]()

3 Likes

Laurus Labs is in the process of manufacturing medicines for sickle-cell diseases starting this year. The medicine cost will come down from Rs 2.5-6 crore a year to Rs 2.5 lakhs annually. Proud of this company!!!

27 Likes

Another subdued quarter.

5718c8f9-b420-48e0-ac33-92f4342d4e61.pdf (4.1 MB)

1 Like

Laurus labs Onco API CDMO partner.

I think we need to wait and watch how things go.

9 Likes