but the promoter itself is selling its stake?

2 Likes

Minimal. FIIs have been increasing stake since Dec 2022.

1 Like

Laurus signs pact to set up a joint venture with Slovenia’s Krka pharmaceutical.

A detailed discussion on Laurus and the overall Pharma & CDMO sector.

https://x.com/unseenvalue/status/1751024868202528774?s=20

And here is the YouTube link to the same.

Hope you find it useful.

10 Likes

This topic is temporarily closed for at least 4 hours due to a large number of community flags.

This topic was automatically opened after 16 hours.

Indigenous CAR-T cell therapy now available for commercial use: ‘first’ patient declared free of cancer

13 Likes

Does anyone have visibility into potential revenue impact of this for Lauras Labs and respective timeframes?

I am not sure about the revenue impact. Still, I appreciate that management has a vision for allocating and strategizing capital for life-changing, disruptive investments. It may not mean much in the short term, but it opens huge levers for players like Laurus in the long term, not just for economic and social aspects but also for creating a name for themselves in the space.

7 Likes

Three patients are fully recovered from cancer as per the below report using CAR-T therapy in India developed by ImmunoAct where Laurus Labs has 33.86% stake.

19 Likes

Laurus Labs - Can be a great opportunity if the management is able to walk the talk wef Q4

Q3 FY 24 concall and results highlights -

Sales - 1195 vs 1545 cr ( down 23 pc )

EBITDA - 183 vs 404 cr ( down 55 pc, margins @ 15 vs 26 pc - steep decline. However, the gross margins were at 54 pc, up 1 pc YoY )

Net Profit - 23 vs 203 cr ( down 89 pc )

Segment wise revenues ( for 9M ending Dec 23 ) -

Formulations - 984 vs 747 cr, up 32 pc

Improved business in ARVs and arresting of price declines. Developed Mkt export formulations also picked up. Multiple product launches scheduled in US in next Qtr

APIs - 1800 vs 1895 cr, down 5 pc

Sales breakup of APIs -

ARVs - 61 pc, Onco APIs - 15 pc, Other APIs - 24 pc

New capacity addition in progress in the Onco APIs segment

CDMO - 686 vs 1939 cr, down 65 pc ( steep decline due large PO executed LY. Except for that, core business grew 30 pc )

Company has 50 plus projects in Phase - 1,2,3 + 10 molecules in commercial stages. Seeing good demand/enquiries for late stage NCE molecules

Animal Health contract has commenced commercial validation batches

800 cr capex in CDMO facilities is on track

Bio - 131 vs 80 cr, up 65 pc

Total - 3600 vs 4660 cr, down 23 pc

Management commentary -

Believe that capacity utilisations should improve wef Q4 and hence the company should be able to report significant margin recovery. The same was expected in Q3 but has been pushed back into Q4. Expect capacity utilisation to pick up in Q4 and EBITDA margins to cross 20 pc. The confidence for the same is coming from the order book lined up wef Q4. The same is expected to sustain in FY 25 as well

As the capacity utilisation improves, EBITDA margins should get a good bump up. Continued interest and CDMO enquiries is a very positive sign

The Animal health contract is a > 10 yr multi product contract for supply of 20+ APIs to Intervet GmbH, a subsidiary of Merk Animal Health Ltd

Company also has a > 10 yr agro-chem products CDMO contract at hand. Capex for the same is on. Commercial supplies may begin in H2 FY 25

Disc: hold a tracking position, will add more as and when better results start fructifying, biased, not SEBI registered

13 Likes

the story would take another 6 months… management is always more positive… so be prepared for some short term pain…

1 Like

An investor need to be always watchful about positive commentary of Management of any Pharma business.

LUPIN have also gone through this phase of negative growth and Management used to always paint positive picture but execution was poor.

Investing in Indian pharma business is not easy after 2012-13-14 onwards.

8 Likes

Sharing a GROUND report by Botlivala & Karani Securities Pvt. Ltd on their Hyderbad Pharma plants visit. It covers Laurus Labs also.

Pharmaceutical - Hyderabad Visit - Flash Note - 01 Apr 24.pdf (347.4 KB)

I hope you find it useful

dr.vikas

12 Likes

Just sharing an article about the CDMO landscape in India

Hope you find it useful

dr.vikas

5 Likes

Please share the source of the above information

Thanks in advance

AFAIK that excerpts is from a research report recently shared in media.

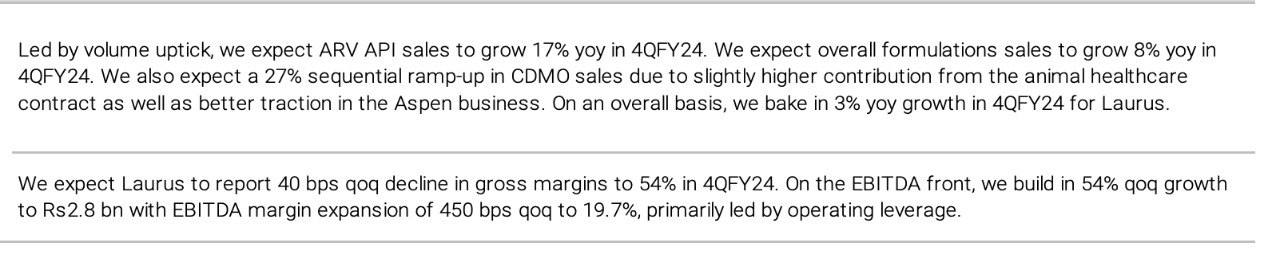

Laurus Labs -

Q4 FY 24 results and concall highlights -

Sales - 1440 vs 1381 cr

Gross Margins @ 49.8 vs 49.7 pc

EBITDA - 259 vs 287 cr ( margins @ 18 vs 21 pc )

PAT - 76 vs 103 cr

Full Year R&D spends @ 241 vs 211 cr ( @ 4.8 pc of sales )

Segment wise sales -

FDFs - 430 vs 367 cr - volume led recovery in ARVs + new launches in US

APIs - 745 vs 714 cr - led by strong growth in Onco APIs

CDMO - 236 vs 228 cr

Bio - 29 vs 46 cr

Full Year breakup of sales -

ARV - APIs + FDFs - 50 pc

Non ARV APIs - 20 pc

Non ARV FDFs - 10 pc

CDMO - 18 pc

Bio - 2 pc

Capex spends in over last 3 yrs @ 2600 cr. Currently, the company is operating at 0.9 X - asset turns vs its 5 yr avg of 1.1 X asset turns. As this improves, so shall the profitability. FY 24 capex @ 700 cr

Company’s CDMO business has -

70 + active projects under various phases for small molecule APIs

10 commercial projects

20 + active projects for animal APIs

1 active crop protection

Onco APIs reported highest ever Qtly sales at 147 cr in Q4. Cardio, Diabetic API segments are reporting good sequential recovery

Seeing greater RFPs from big Pharma for late stage CDMO products

Animal API facility has started commercial validation batches. Crop science CDMO unit is under construction. Both Crop science and animal API CDMO facilities are already fully committed with innovator companies

Net Debt @ 2368 cr. Likely to come down going forward

These days, there is greater demand for bio-catalysis and continuous flow chemistry from big Pharma due to their ESG commitments. Laurus has built good capacities for both these manufacturing techniques

Additionally, there is clearly a greater thrust from big Pharma to diversify away from China. Same is reflected in greater late stage enquiries that the company is receiving

Capex plan for FY 25 - should be spending around 700-800 cr mainly towards CDMO and Bio business

Likely to see significant revenues from animal API CDMO contract in FY 25. Expecting CDMO business to be 33 pc of total business in next 2-3 yrs !!!( this can drive significant value creation … imho )

Disc: hold a tracking position, intend to add more on dips or in case of CDMO business pick up, not SEBI registered, biased

15 Likes