I have been reading about Laurus Labs & found it interesting. I will present my findings in 2-3 posts with first post summarizing the company’s business.

Laurus Labs is a company founded by Dr. Satyanarayana Chava around 2007. He was COO of Matrix Labs & when Matrix Labs got acquired by Mylan, Dr. Chava went on to found Laurus Labs. Mr. Ravi Kumar V V also works at Laurus & he has previously worked as Vice President of Matrix Labs.

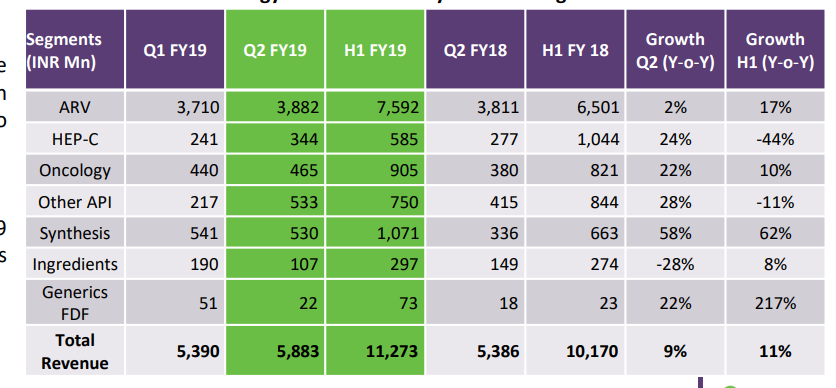

The company has 4 business lines - API, Generic FDF, Synthesis, Ingredients.

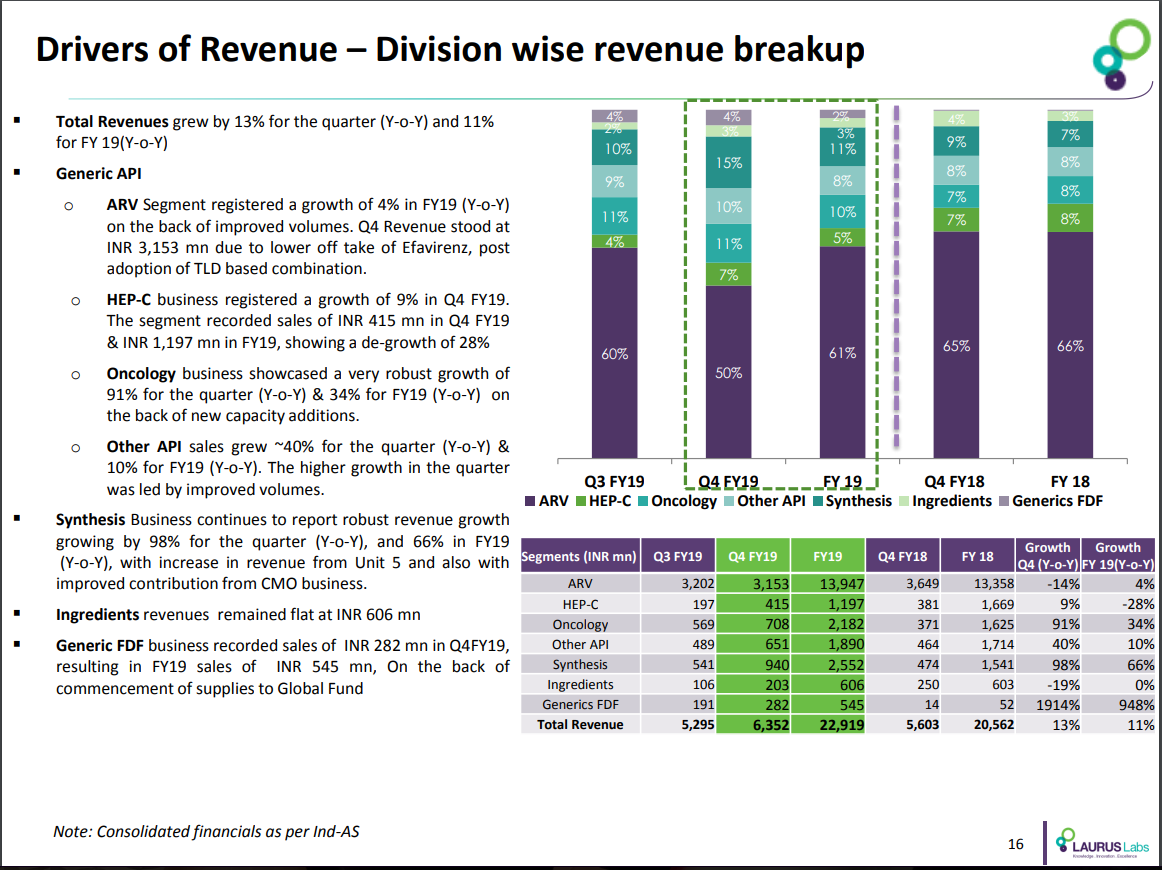

The company has strong presence in API segment with ~90% revenue contribution. The company has invested into 3 new business lines namely - Generics FDF, Synthesis &Ingredients. The contribution of new lines in FY18 was at 0.3%, 7.4% & 2.8% respectively.

The thesis for investment resolves around -

- Execution of management to scale the new business lines & transform the business from pure play API player to diversified pharma company.

- The company has invested 600Cr in the new businesses which are generating very little revenues but P&L is charged costs of ~120-130Cr in terms of depreciation & finance costs. Once these businesses start contributing revenue, operating leverage shall kick-in.

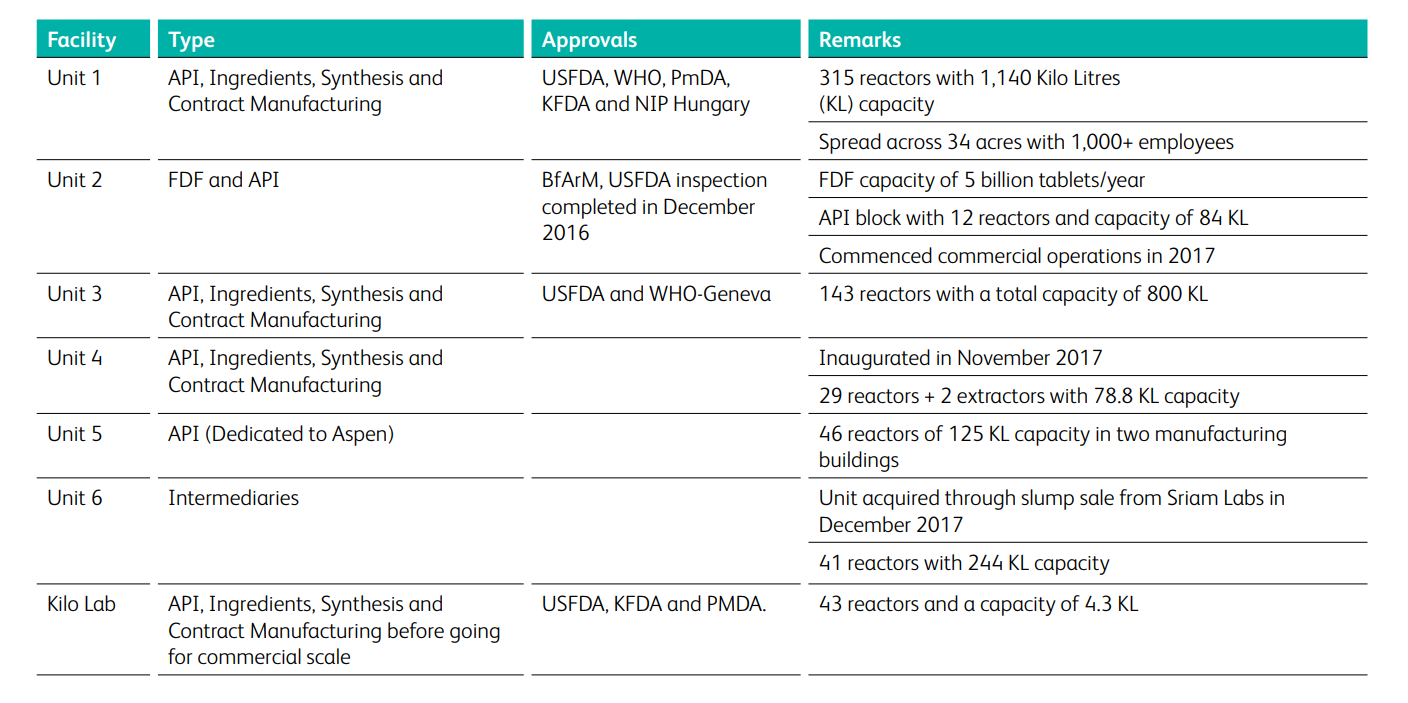

MANUFACTURING FACILITIES

BUSINESS

API

This business can be further divided into 4 sub-segments - ARV, Hepatitis C (HepC), Oncology & Others.

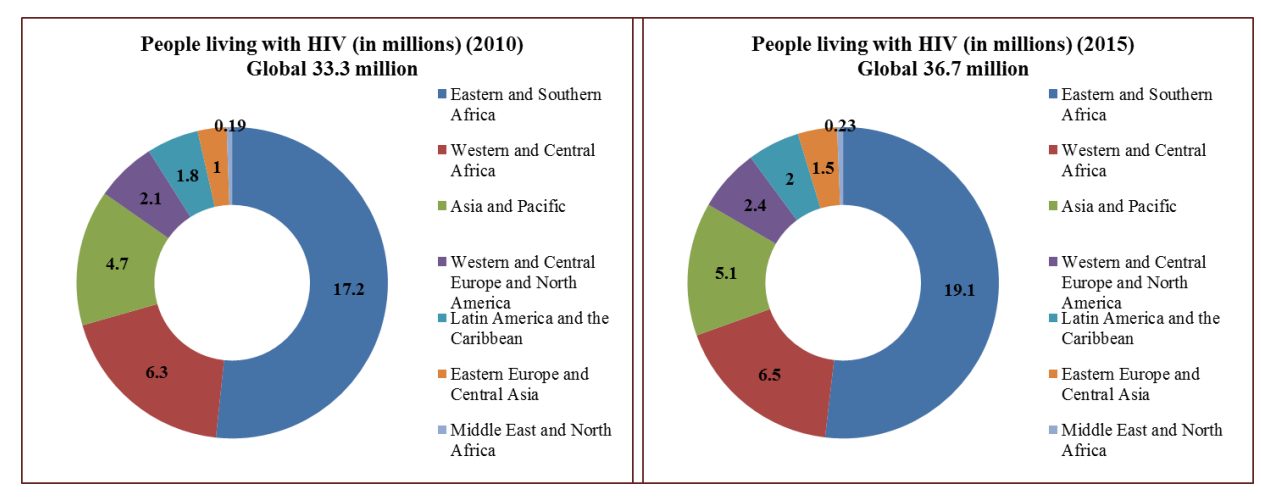

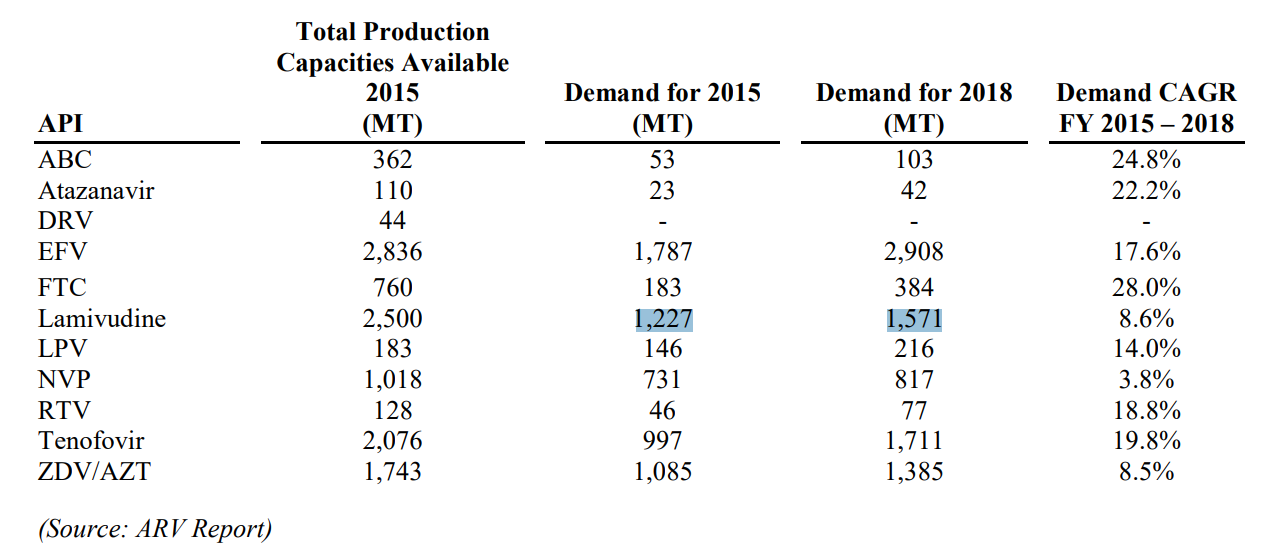

The company is one of the largest API player in ARV drugs (HIV) market. The number of patients requiring ARV treatment are expected to go up from 18 million to 23 million over next 3-4 years. A large part of these patients are in low & middle income countries (LMIC). For developed market, there are patented drugs with much higher selling price. The patents are slated to be expired (or have already expired) on ARV side in US & EU markets & that presents opportunity for Laurus.

HepC business has not grown much over last 2 years. The company is focused on trying to increase Oncology API business. The others include APIs in - anti-diabetic, cardio vascular, gastroenterology.

I will try to write a separate post for technical details & market developments in API side.

FDF

The company has increased the FDF plant capacity from 1 billion tablets to 5 billion tablets in FY18. The company expects revenue from FDF side to start contributing from Q3 FY19. The company has filed for 9 ANDAs & 1 NDA in FY10. The company expects to file 10 ANDAs every year for next 2-3 years.

The company has used partnership model to get into FDF business. They have profit & cost sharing model with Dr. Reddy’s for development & sales of ARV FDFs. The company also has 10-year agreement with Natco for supplying HepC FDFs. The brands will be jointly owned & they have 50-50 cost/profit sharing agreement.

SYNTHESIS

The company does custom synthesis for two global companies - namely C2 pharma & Aspen. The business contributed 7.5% to overall revenue & company has set target of 10% revenue contribution in FY19.

The unit 5 of the company is dedicated to manufacture custom APIs for Aspen & Aspen has issued bank gurantee of 21mil. $ for construction of this unit. Aspen is 6th largest generic player in the world. The validation batches have started from unit 5 & commercial batches are expected to be shipped over next 12-18 months. The company would be supplying 10 products - hormones or intermediates of hormones.

The company has dedicated block at Vishakhapatnam for C2 pharma to manufacture digoxin.

The company has setup a subsidiary in US - Laurus Synthesis Inc. The company has hired 12 scientists & 4 sales persons in Boston area focused on this.

NUTRACEUTICALS

In nutraceuticals, there is consolidation happening globally & quality norms as stringent as pharma are being adopted. The company is trying to seed & grow this business. Current products include - anti-oxidants, skin brightners, UV protection agents etc. The company is also trying to develop botanical extraction to target natural ingredients market.

OTHER POINTS

- The company has 587 scientists working at R&D center in Hyderabad. The company is also setting up/expanding R&D center at Vishakhapatnam.

- Customers - Aspen, Aurobindo, Cipla, Mylan, Natco, Strides Shasun

- Competition - Desano, Hetero, MSM, Mylan, ScinoPharm (Taiwan), Shilpa Medicare, SMS Pharma

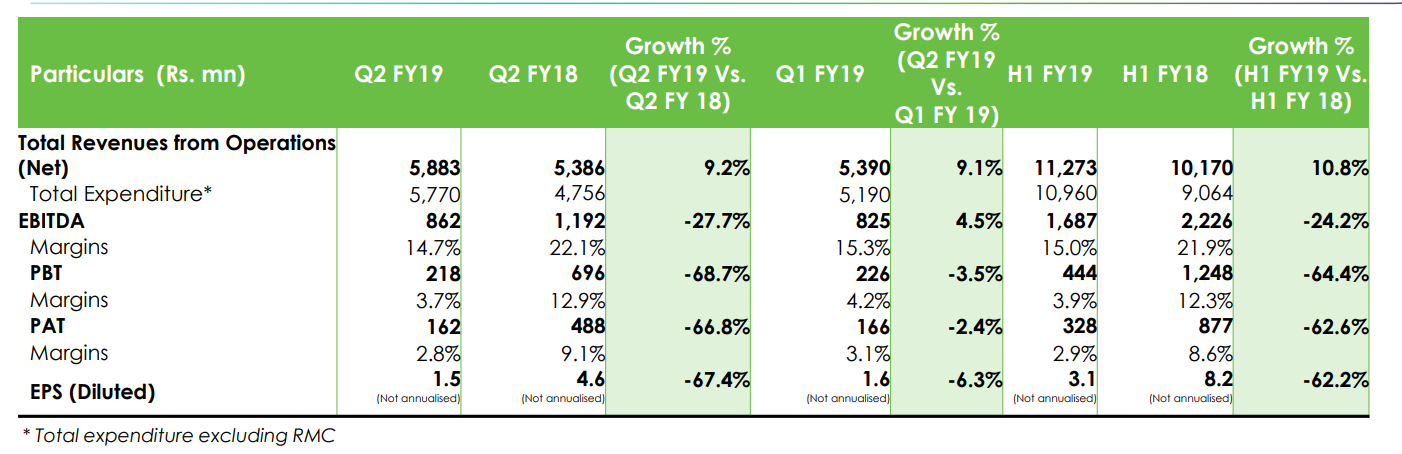

NUMBERS

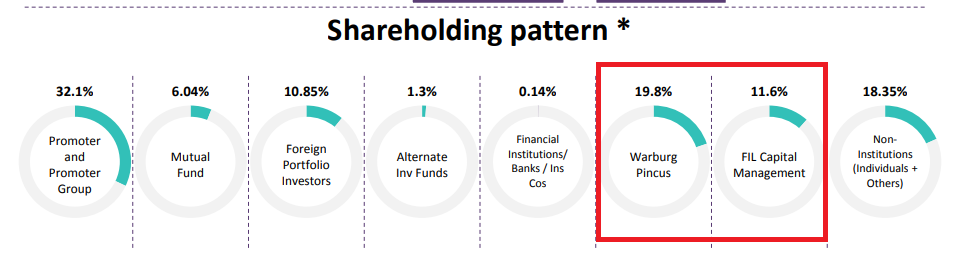

SHAREHOLDING PATTERN

The promoter has bought shares from the market from March’18 to June’18 taking stake from 30.57% to 32.06%.

RISKS

- The valuation seems to have priced in a lot of growth from FDF + Synthesis. If growth does not come through, there might be significant downside risks.

- USFDA inspections remains a constant risk for all pharma companies. Although company has cleared several USFDA inspections with no observations & even has a VP looking just at regulatory matters - they can not let their guard down.

- The company is going to compete with their customers when they are trying to move from API to FDF. JV mitigates this to some extent but combined picture of API + FDF shall be looked at.

TODO

- Build entire ecosystem landscape in terms of customers, JV partners, competition, original innovators etc.

- More details about RM, their supply-demand scenario & ability to pass on RM costs etc.

- End market potential

- Management quality

Disc - Invested with small allocation, will buy/sell as more clarity emerges on execution, above TODO items & if valuation becomes more favorable. This is not buy/sell recommendation & investors are advised to do their own due diligence.