What can one see in data source : screener

disc : invested from lower levels

I had the same doubt on Trade Receivables ( I am assuming you are referring to the same ) , their ARV is high working capital intensive, which is kind of tender business, this segment contributes significant percentage to the revenues . (Thanks to @Worldlywiseinvestors for clarifying this ) , from the investor community who track very very closely all the parameters so far no red flags. Thesis is playing out very nicely. The statement made by Mr Chava today about additional capex through internal accruals is an icing on the cake in my view

Quoting the opinion shared by Mr Sajal Kapoor ( famous pharma analyst ) -

" In the Pharma space, the real juice ( at present and for the foreseeable future ) is likely to be in the - API, Custom Synthesis and CDMO space.

I somehow feel, that most MFs / old pharma analysts are hooked onto the complex generics / specialty medicines space in the US. They keep trying to crack that code…day in and day out.

Plus most of the companies in large cap space like Sun, Cipla, Dr Reddy, Aurobindo etc are focused in that space. Only Divis, in the large Cap space is API / CRAMS focused."

It may just be the case that retailers are having a once in a lifetime opportunity to lap up likes of Laurus, Solara, Suven, Sequent, Jubilant Ingrevia etc while the valuations are still not expensive.

Plus, some in depth, non institutional analysts like - Mr Sajal Kapoor have been helping the retailers to grab the opportunity.

Disc : Have been invested in most of the above mentioned companies. Have also held and studied the large caps earlier. And I kind of agree with Mr Kapoor’s observations.

I am not invested in Laurus, so please consider my reply only from an accounting view.

It could mean that when Laurus invested in Richcore, the latter had insignificant assets and hence the entire consideration could be attributed for Richcore’s future potential. Since no assets were acquired, the entire purchase consideration was accounted under goodwill by Laurus.

A confirmatory pointer is in Dr, Chava’s Nov. 2020 interview in BloombergQuint which can be accessed here: Laurus Labs CEO Says Richcore Lifesciences’ Acquisition Will Fast-Track Biotech Ambitions

It states that for the first half of FY2020-21, Richcore had revenues of only Rs. 30 cr (which could be achieved through rented P&M) but it would receive a fillip when additional capacity comes on stream in March 2021. It also states that Richcore’s capex would be funded by its internal accruals + debt that Richcore would bear.

Thanks @vikas_sinha and @ranvir for your responses, I largely concur that MFs and DIIs are probaly not the best value finders, especially in the pharma space, and may be late to the party in API / CDMO / CRO / CRAMS.

That said, what are the perceived risks that are keeping them away is worth analysing I feel. What can possibly derail the thesis, and what is the probablity, however small, for such an event?

Q4FY21 & FY21 Results Conference Call Updates

Summary

Revenue target of US$1 billion by FY23E

Non-ARV cumulative contribution: ~60% in Q4FY21; diversification from FY23 onward

FY22 EBITDA margins to be maintained at 30%+

No significant debt to be taken for additional capex

Overall growth to be driven by market share and volume gains, not by price hikes

Formulations

Higher FY21 sales from tender business in LMIC, Europe and US

Strong order book for coming quarters

Commenced marketing of in-licensed products in the US through own front end. Two launched, remaining three to be launched in H1FY22

USFDA: Nine products have been approved, eight tentatively approved; filed 27 ANDAs & NDAs (two Para IVs, seven FTF). Expect to file eight to 10 ANDAs in FY22.

Nine filings in Europe; 14 in Canada (eight approved, four launched) and two to be launched soon

TLE400 market opportunity of US$150-200 million; currently three players approved

CMO – Mainly from Europe. Uptake from FY23 for which two validations already done

Geographical Bifurcation - Regulated: LMIC sales contribution - 1:4 in FY21;

30:70 in FY22E and 1:3 in FY23E

APIs

Growth led by higher growth in ARV API business in turn led by higher volume of first and second line products.

61 DMFs have been filed on cumulative basis

Strong demand for ARV APIs in FY22 as well

FY21 growth led by volume growth on the back of approval of triple-drug combination for which all three APIs were approved

EFV to DTG regime change led to volume increment in 3TC, DTG, TDF

DTG penetration to continue to increase in FY22/23

Oncology to grow fairly well in FY22-23

Adding capacity for other APIs (cardiology and diabetology) – to be visible in FY23/ end of FY22

OTIF score close to 100

Custom Synthesis

Healthy pipeline and good visibility; growth to outpace other divisions

Number of active projects stood at 50 as on FY21

Commercial supplies ongoing for 4 products

Laurus Ingredients to be self-reliant by FY23

Facilities – to have 3 facilities by FY23, maybe 4

Construction of Hyderabad R&D facility ongoing

Vizag facility will also support the segment

Looking to acquire land for greenfield steriles +hormones facility near Parawada, Vizag

Laurus Bio

Medium term outlook – To function as a contract manufacturer

180,000 liters fermentation capacity (four reactors of 45000 liters capacity each). Two reactors to be on line in May, two in August-September

An additional 1 million liters capacity for fermentation to be developed

Capex

Planned across segments; guidance of 1500-1700 crore over next 24 months

Asset turnover could be ~1.5x for this capex

FY21 – 700 crore capex; 50:30:10:10 split between API, Formulations, CS and Laurus Bio respectively

Future capex – Majority for API, then CS and then Formulations

Laurus Bio FY22 capex to be approximately 60 crore

R&D spend: 184 crore; 3.8% of sales in FY21

Gross Debt: 1453 crore; Net Debt: 1405 crore

Laurus Labs Q4FY21 Con Call

Business:

• Q4FY21 Revenue stood at ₹1,413 crores (YOY: 68% Growth) & Revenue for FY 2020-2021 stood at ₹ 4,813 crores (Growth of 70%). Gross Margin: 55%, EBITDA: 34%, ROCE: 30% due to operating leverage kicking in & higher asset utilisation. Capex: ₹ 700 crores which includes capital work-in- progress, Capex break up of ₹ 700 crores Invested : 50% into APIs, 30% into FDF, 20% into CRAMS & BIO (10% each)

• Formulation Division Revenue: ₹1,664 crores & Q4FY21: ₹ 434 crore. The revenue contribution from the formulation division for the whole year is 32%.

• Recently got approval for a triple drug combination Anti Retroviral Drug containing Tenofovir Alafenamide. In the process of obtaining registrations. Already got orders for this triple drug combination. Expect to service the order by the first half of FY22.

• In FY21, established a wholly owned subsidiary- Laurus Synthesis to take care of contract manufacturing for big pharma. Also incorporated another step down subsidiary known Laurus Ingredients.

• Forayed into Biotechnology space by acquiring a majority stake in Richcore Life sciences which was renamed as Laurus Bio. The current promoters will continue to run the operations. This acquisition gives Laurus entry into Fermentation capabilities as well as foray into Recombinant Proteins.

• Commenced the marketing of in-licensed products, out of 5 in-licensed products 2 products were launched & in the process of launching the rest of the products in the next 6 months.

• We have total 9 final approvals out of the 26 ANDAs filed so far

• In Canada, Laurus has 8 approvals & 4 launched & 2 more products will be launched soon

• For EU, validated additional products as a part of the contract manufacturing with our partner & expect significant upside from these products in FY23.

• Also obtained approvals & marketing obligations for bi-products, 2 of them launched. In the process of launching others shortly

• On the R&D front, Laurus continues to invest 4% of the revenue

• In the Generic API division, this year was very good for ARV APIs, achieved ₹1,850 crore sale which is the highest ever in ARV API division so far

• Due to increase in demand for third party API sale, we are still expanding the API capacity to serve the existing demand from the customers.

• In the Oncology segment, registered a growth of 5% in the current quarter

• Laurus Labs has one of the largest high potent API capacity in the country & will expanding the high potent API manufacturing capabilities in Unit 4

• In the Synthesis division, recorded a growth of almost 20% from Q4FY20, achieved a sales growth of 35% compared to FY20 & FY21

• Pursuing several projects in active late stage clinical programs

• Construction activity is in progress at the dedicated CRAMS R&D in Hyderabad.

• Also acquired land for greenfield new manufacturing site at Vizag which will cater to the manufacturing needs of this division for next 10-12 years.

• In the process of acquiring additional land for this division to manufacture steriles & harmones, high potent molecules.

• Closed the transaction to acquire Richcore i.e Laurus Bio in the month of January

• Laurus Bio is on the course of commissioning a large scale fermentation capacity 1,80,000 litres in the next 2 weeks.

• Planning to acquire additional land for Further expansion of Laurus Bio by creating close to a million litres fermentation capacity.

• Doing good number of projects in the late stage in the clinical phase for which we are building capacities especially in high potent we are building large scale capacity in NDA batches.

• Revenue break up: 40% Non-ARV & 60% ARV

• The new Laurus Bio new facility will go commercial by 15th May 2021 & Putting 4 fermenters of which 2 45,000 litres each will go commercial in may & the remaining in August-September. Order book is in place

• The one reason for volume growth- earlier the most preferred treatment was Efavirenz based where we wouldn’t have any approvals for Lamivudine & Tenofovir from many customers. When the therapy moved from Efavirenz based to Dolutegravir based. We got approvals for Lamivudine & Tenofovir from most of the customers so people started buying 3 APIs from us Dolutegravir, Lamivudine & Tenofovir from us.

• Got approvals for Dolutegravir & Emtricitabin NDA & also got order for these formulations & will service it in the next. 6 months. Also expect more orders.

• Our approach is to develop few products, maximise those products into maximum geographies & get leadership position & gain market share.

Management:

• CEO: Dr Satyanarayana Chava, CFO: Venkata Ravi Kumar

• The performance focus is on growth driven by excellent execution & creating a platform for future growth with manufacturing capacity expansions. A combination of brownfield as well as greenfield in API, Formulations as well as Custom Synthesis Divisions.

• These initiatives will bring focus to the contract manufacturing division to allocate, create & offer increased capacity to service the customer needs.

• Believe that by the end of FY23, Laurus Synthesis will be self-reliant in all respects

• In the medium, expect Laurus Bio to be vertically integrated in offering a Contract Development & Manufacturing Services in the Biotech space.

• Seeing growth in the developed markets in North America as well as in Europe

• Continue to invest in strengthening & enhancing the formulation infrastructure, capacity expansion through de-bottlenecking was operational & already commercially used

• Brownfield expansion on the same site with similar capacity will become operational in a phased manner from October 2021 & will become fully operational by the end of FY 22

• Expect to maintain good sales for ARV APIs in FY22 as well

• Expect Oncology units to grow fairly well in the coming quarters

• Seen healthy growth in Contract manufacturing of Generic APIs, Non-ARV APIs & Non-Oncology in Q4FY21 and initiated validation of several APIs- Non-ARV & Non-Oncology and adding additional manufacturing capacities for these products. This will be visible in FY 23 as these capacities will be commercially utilized.

• Expecting capex of ₹ 1500 to ₹1,700 crores in the next 2 years

• Targeting in the next 2 years to have a separate synthesis company so where it has its own production & R&D.

• We want to be vertically integrated and investing into intermediates & APIs and that is the reason why 50% of the capex is getting into API site.

• Increased the capex foray based on the visibility in the API & Formulation division based on the estimated approvals. Also considering the custom synthesis.

• Non-ARV APIs will see significant sales increase, partly in FY22 & big jump will come in April 2023.

• Goal is to double the revenues in this division in FY23 (Laurus Bio)

• The growth of the Custom Synthesis business will outpace rest of the divisions from FY23 onwards

• “If you look at our CRAMS division right now, it will become sizeable in the next couple of years. It took 7-8 years for us to nurture the division. We will start putting our resources, parts, strategy, execution into the division & will become sizeable in the next 5-6 years.”

• The growth will be driven by market share gain & portfolio enhancement.

• There is limited growth in ARV APIs right now as we are already having a line share of the market so it won’t be easy to grow beyond so we are adding diabetic segment, cardiovascular segment will be commercialised in the last quarter of FY22 & this is the reason we are investing into Non-ARV APIs.

• We do see growth in the LMIC countries going forward in FY23 but the other non-ARV non-LMIC business will grow significantly

• Asset turns of 1.5x from the capex announced

• TLE 400: $129-250 million opportunity & TLE 600: Small opportunity

• We do monitor revenue per employee, EBITDA per employee since inception& currently our revenue per employee is a little over a crore. If you look at our Richcore acquisition, we didn’t acquire the company, we acquired the talent.

Risk:

• Dependence on China for Key Starting Material

• Limited size of opportunity in the ARV space

Laurus Labs Limited on 30th April 2021 announced its Q4FY21 and full-year results.

Laurus Lab performed extremely well consecutive in the 4th Quarter of FY21. The company did a robust growth in all three segments. Having a healthy order book for FY 22. Consolidated revenue for the quarter increased by 70% driven by growth in all the divisions.

The company has been able to sustain its EBITDA margins, and profitability has also improved to Rs. 297 Crs. for the quarter. Generic API division showcased a robust growth of 61% YoY. Anti Viral segment recorded a robust growth of 70% YoY.

Revenue Showcased a healthy growth of 102% YoY. The growth was led by higher LMIC Market volumes and increased volumes from North America and EU Commenced marketing of in-licensed products in the USA to leverage front-end capabilities. Custom Synthesis division recorded a strong growth of 35% YoY.

Capacity Expansion – To cater to future demands

All the greenfield expansion has turned Cash positive in FY20 with near maximum utilization. Richcore will be renamed to Laurus Bio shortly. Laurus bio will be to cater the demands of food & fermentation and synergies are exciting for the same. With a vision of creating long-term sustainable growth, the company continues to undertake a major Capex program across all divisions. FDF - the capacity of 5 bn tablets/capsules per year. Capacity expansion initiated and will be operational by Q1 FY22.

Continue to undertake Brown Field Capex programs for Capacity addition in line with strong order book visibility and business outlook. Brown Field CAPEX in existing sites to have a shorter payback period and ROCE accretive. Acquired assets of an API Unit in Vizag to be used for backward integration and pre-clinical chemistry. Doubling their FDF capacity by FY22.

![]()

Debt Scenario

Business Highlights:

Generic FDF.

Revenue Showcased a healthy growth of 102% YoYGeneric FDF business maintains healthy growth momentum for the quarter. Commenced marketing of in-licensed products in the US by leveraging the front end. Contract manufacturing revenues from the EU region have a strong order book for FY21 and beyond.

FDF Business delivered robust growth for the quarter. This is driven by continued strong demand in the ARV segment of the LMIC region and portfolio expansion in developed markets. Overall FDF revenue for FY 21 grew by 102% YoY. Strong order book in all geographies. 2 Additional products validated as part of our CDMO expansion in EU. FDF capacity debottlenecking complete. New manufacturing block will be commercialized by Sep 2021Doubling their FDF capacity by FY22.

Synthesis & Ingredients .

Custom Synthesis division recorded a strong growth of 35% YoY. Synthesis business delivered robust growth for the quarter. Total Number of Active Projects in the CDMO division stood at the end of FY21 was 50 (vs 40 in FY20). Multiple Partnership proposals are in the collaborative phase. Created a 100% subsidiary for Synthesis business and acquired small facility at Vizag under this. Also, creating a dedicated R&D center for the Synthesis Division.

Generic API.

Generic API division showcased a robust growth of 61% YoY. Anti Viral segment recorded a robust growth of 70% YoYStrong demand in 1st line ARV API. Order book position is robust. Adding more capacity to meet the growing demand. Other API segments (incl. CVS and Diabetes) reported good growth. Under discussion with Key Generic Partners for CM opportunity. Creating a dedicated block for Non-ARV APIs including expansion for High Potent capacity at Unit 4.

Healthy Order Book

Partnership with Global Fund offers higher volume contracts with reasonable predictability in the FDF Tender business. Have a healthy order book for FY 22 & beyond in FDF CMO business with a strategic partner in the EU. Robust growth in Other API segments to continue on the back of higher-order book visibility from key therapeutic segments like CVS, Anti Diabetic, and PPIs.

Several new customers added with programs in various clinical phases. Incorporated a Wholly Owned subsidiary to give increased focus and eventually dedicated R&D and Manufacturing for Synthesis Business. Other therapeutic areas and Oncology to offer consistent opportunities to broaden the scope, with ongoing new product introduction.

Changing business mix to drive growth

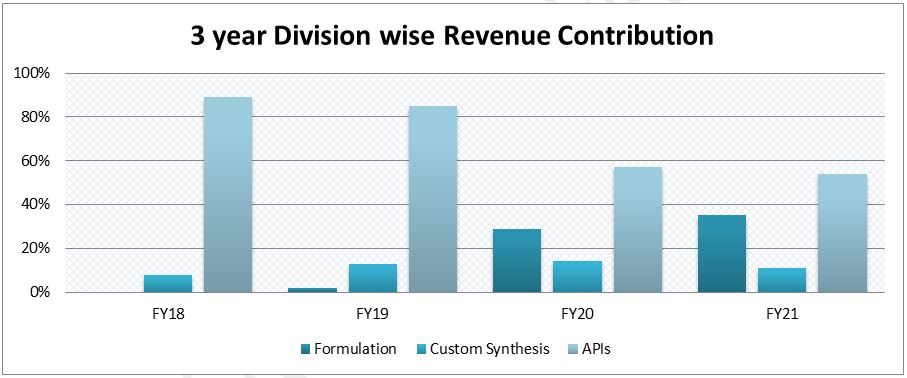

Generic FDF the segment contributed ~35% in FY 21 to total revenue as against just 2% in FY19. Non ARV API business to contribute significantly showcasing the speed of diversification of revenues.

The change in revenue & product mix to generate better profitability & margins. Synthesis business to show gains in line with new customer additions in CDMO. Acquired Aspen’s South African Subsidiary, in order to get a foothold in the worlds’ largest Generic Accessible ARV market The Richcore (renamed as Laurus Bio) acquisition will help us enter into high growth segments of AOF products, Enzymes and Biologics.

15 Years of Patience, diligence & perseverance.

Here is the summary made for a quick and better understanding of the Result update for full-year FY21 and Q4FY21 from Laurus Lab Conference Call and Investor Presentation.

The entire recording of Conference Call: https://youtu.be/GiDEPHxeMqI

Laurus Labs Analysis

CMP 477, Current Market Cap=25600 Cr, TTM Profit= 984 Cr, TTM P/E=26, Recent Qtr profit 297 Cr

ROCE - 41%, ROE - 45%, Debt to EBITA 0.9x, Net Debt = 1405 Cr, EBITA Margin = 33%

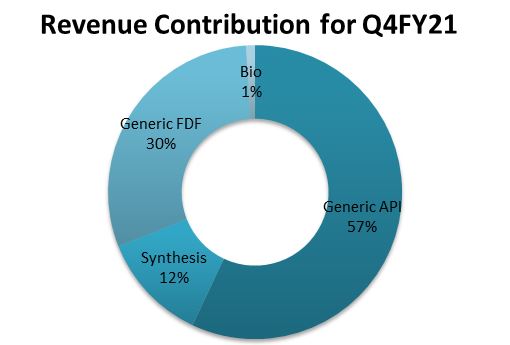

All plants in Vizag, business division -Ant viral API 38%, Onco API 5%, Other API 5%, Custom Synthesis 11%, Formulation =35%

Over the past few years, Dr. Chava founder and CEO has built very strong team. He didn’t shy away from diluting his portion of share to grow this business without thinking too much about his ownership in the company. Management looks very professional and always on the ground. They have delivered what they have promised. So not being over calculative about their business. Pledging is almost zero now

Continuously diversifying into new product and new geography. Thus, reducing the risk of product concentration. Anti-Viral contribution in FY16 was 82% and now it is down to 38% while formulation contribution increased from 0% in FY16 to 35% in FY21.

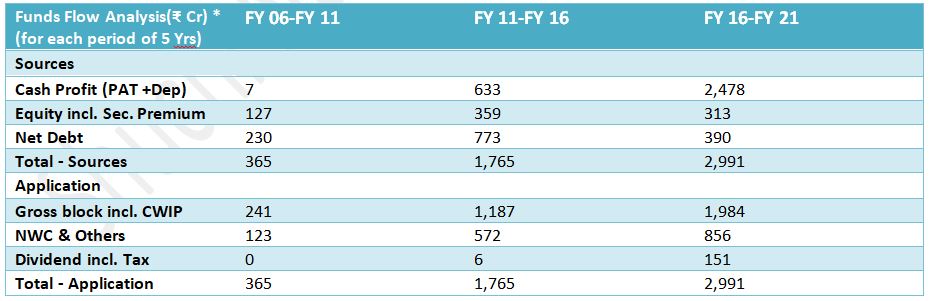

Company has very good financial profile and balance sheet. FY21 was bumper year with 984 cr profit vs 255 cr last year. Management has said that this is sustainable and there is no one-off demand because of covid situation. This means with this kind of profit; company’s fortunes will change. They can do lot more in coming years with this profit

Strong R&D focus. Company on an average spent 170 Cr per year on R&D… Compare this with their average profit of 160 Cr in last three years…So they are looking at bigger picture…investing and innovating to increase revenue. The growth in FY21 didn’t happen overnight

Capacity expansion: Done capex of 700 cr in FY21… Total 1700 Cr of capex in FY22 and F23… Asset turnover is 1.7x i.e this will add 2890 Cr of revenue to FY21 revenue of 4814 Cr i.e. Visibility of 60% revenue growth in coming years

They want to be vertically integrated and investing into intermediates & APIs and that is the reason why 50% of the capex is getting into API site

Bet on biotech - Forayed into Biotechnology space by acquiring stakes in Rich core Life science. This acquisition gives Laurus entry into Fermentation capabilities as well as foray into Recombinant Proteins.

Geographically diversified customer base with strong flow of repeat business mitigating revenue concentration risk

Management guidance of 1 billion US dollar revenue by FY23 i.e. 7400 Cr. As per management, this is possible as they have strong order book and existing capacities are also unutilized. Overall growth to be driven by market share and volume gains, not by price hikes. Management said they don’t need additional capex to achieve 1-billion-dollar revenue

Valuation: Current Market Price = 477/-

Even If we assume revenue of 7000 Cr in FY23 with 30% EBITA margin, net profit can be 1325 Cr i.e. EPS of 25. Current Margin is 33% and with brown-field capacity expansion, high possibility of maintaining or improving that by FY23.

At 25x PE = 25x25 = 625/- Expected stock Price

At 30x PE = 30x25 = 750/- Expected stock Price.

At 35x PE = 35x25 = 875/- Expected stock Price.

Divis is trading at 100x PE. Lupin at 45x, Gland Pharma at 60x.

If Laurus shows consistent performance and ROCE >30% and generates free cash flow then this stock can be re-rated to new PE multiples

What is the downside?

Even at 17x PE, stock should trade at 425/- so downside looks limited.

Risks:

• 55% of revenue still comes from HIV related drugs. Invention on HIV vaccine

Dependence on China for Key Starting Material

• Not able to timely operationalize the new capacity because of covid situation

• Succession plan for Dr. Chava

To me HIV vaccine discovery related news can be biggest hangover to stock re-rating. Can someone please help what would be the revenue contribution from HIV related products by FY23 or in next 5 years? Would it be possible for them to reduce the depedency so quickly?

Disclaimer: This is not a buy or sell recommendation. I own this stock and plan to increase my holding. Please do your research before buying. I am not SEBI registered analyst.

The only potential problem with the thesis is the market is still keen to give only a 20x multiple to company because people dont believe API players have a moat. People view Divis very differently.

Disclosure: Invested from lower levels.

Within 1 year, company has done 5x bagger, and growth is that old only, it will take time to catch-up, people are still feeling bit dizzy/vertigo-effects. Divis is 3.5x larger (book-value) and 5x older with consistent model and good results trend. It will become Divis in all probability, but that takes some time.

Disc: invested

Excellent analysis.

I however have a slightly different view on the perceived risk of HIV vaccine. It is correct that it would disrupt the market but the the vaccine itself should become a big opportunity for custom synthesis for companies like Laurus. Every country would like to vaccinate its population leading to requirement of billions and billions of doses over decades. Will it be once in a lifetime jab or a recurring jab, we don’t know. The point is, whatever happens, a strong and agile company can always mould itself to the changed scenario and start working to acquire its share in the new activities. Secondly the trials of vaccine would now ensure that no new competitor thinks of entering the HIV APIs and formulations manufacturing.

Laurus Labs 4QFY21 Earnings Conference Call

*KSM import from china is by Sea and hence No disruption is anticipated.

*Laurus Bio New Fermentation facility to be commercialised by 15th May (90KL) and balance by Sep 21 ((90KL). In the process of creation of.1 Million Litre capacity in next growth phase.

*1500-1700Cr Capex in the drawing board stage out of which 50%API,25 FDF and 25% Custom Synthesis.

*Present growth is not driven by price hike, but by volume.

*Non-ARV revenue diversification to be visible from FY 23 onwards and full benefit of diversification from FY25.

*EBITDA margin is not one off.30% margin will be maintained.

Robust Q4 For Laurus Labs, What About FY22?: Talking Point with Dr. Chava

A 2016 article (which may have been already shared in this thread) when the company was not known to many and there was no noise around. Something interesting to note -

As Laurus expands manufacturing, Chava and Chereddi say its chemistry expertise and commitment to quality are registering in the market. Bruno agrees, pointing to a flagship project.

"To deal with Gilead, they must be doing something right,” Bruno says. “The Gilead drugs are not trivial chemistry. Gilead doesn’t make products that every person in the world can do easily. But Laurus seems to be able to do it.”

https://cen.acs.org/articles/94/i15/CEN-profiles-Laurus-Labs-upping.html

“Our ability to attract NCE work comes from our ability to transform medicinal chemistry processes in early discovery to robust processes when the candidate is moved to later stages of development,” Chava says. Intellectual property generated in process development at Laurus is transferred back to the project sponsor, he says. “One of the key decisions we took is that we will not infringe on patents. Not even for generics.”

This stand of the company seems to give lot of comfort to the innovators, as one of the main concern today is about IP infringement

Majority stake in Laurus Labs was acquired by Aptuit Inc, USA, a pharma service provider during 2007 and thereafter the company was named as Aptuit Laurus Private Limited.

When Laurus Labs was came up with IPO in 2016, Aptuit Inc exited

Later it seems that Aptuit Inc, USA was acquired by German Pharma Company, Evotec somewhere during 2017

Interestingly, Swizz pharma company Lonza had eyed a majority stake in Laurus Aptuit

PS: just tracing a bit of history. Many of you would have already known. May be deleted, if found not adding any value

“To deal with Gilead, they must be doing something right,” Bruno says. “The Gilead drugs are not trivial chemistry. Gilead doesn’t make products that every person in the world can do easily. But Laurus seems to be able to do it.”

I have seen the similar setup in many of the research driven pharma companies, build the expertise and then do a tech transfer to offshore to scale it up, it is a proven and successful cost effective setup.

Similar question was raised by Mr Sajal Kapoor during Q4FY21 concall on how to asset return by using offshore capabilities (Dishman has their R&D in Swiss ) Link

I have done some google and found that the below are the only companies that are producing Recombinant proteins. This market is expected to grow to 1.7 billion by 2026 from 1.1 billion in 2021. There is a report for subscribed members of marketandmarkets website. In this report, I could see RICHCORE is the only company from India manufacturing Recombinant proteins.

List of companies for Recombinant proteins in the world:

Thermo Fisher Scientific Inc. (US)

Miltenyi Biotech (Germany)

Sino Biological Inc. (China)

Merck KGaA (Germany)

Abcam plc (UK)

Biolegend (US)

Bio-Rad Laboratories Inc. (US)

GenScript Biotech Corporation (China)

Enzo Life Sciences Inc. (US)

BPS Bioscience Inc. (US)

PeproTech Inc. (US)

Proteintech Group Inc. (US)

Abnova Corporation (Taiwan)

R&D Systems (US)

STEMCELL Technologies Inc (Canada)

RayBiotech Inc (US)

CellGenix GmbH (Germany)

ACROBiosystems (US)

ProSpec-TechnoGene Ltd. (Israel)

Neuromics (US)

RICHCORE LIFESCIENCES PVT LTD (India)

Icosagen AS (US)

ProteoGenix (France)

United States Biological (US)

StressMarq Biosciences Inc (Canada)

and Aviva Systems Biology Corporation (US)

Disclosure:

Invested in Laurus before split and would be adding more on declines. May be biased.

Hi, I was trying to understand valuation of the company on basis of their announcement that their FY23 revenue will be around 1 billon dollar(7800 cr rs). With 30% margin(conservative), their profit will be around 2340 cr. On basis of this revenue, I am expecting their FY 23 PE to be around 14. But I am not sure if I did right calculation. I just wanted to understand if company is still cheap at this valuation or not.

Valuations lie in the eyes of the beholder and are the most difficult part of any investment thesis for me personally. I have seen so many amazing businesses but given them a skip or decided to sell out because the valuations seemed stretched/not enough margin of safety. Everyone has a different way to value a company. There is no single “valuation” to speak of. Each investor must make their own decision on what is cheap, what is expensive. I can give you some guidance on how I think though note that this is not investment advice.

I personally think valuations are completely driven by (narratives around growth & unit economics) and and opportunity cost. If the collective market thinks a company will grow topline at 10-12% for 10-20 years with high and stable or improving unit economics and with some operating leverage higher bottomline growth, then valuations would remain elevated. P/E of 100 is elevated. P/E of 50 is also elevated (to most investors). Why I add opportunity cost is that some growth hungry investors (count me in this bucket) would decide to sell off their 12-15% Asian paints compounder and rather go after economy facing stocks like X,Y,Z. As long as the narrative around growth and unit economics remains, valuations would remain elevated as price discounts decades of growing stable profits.

So we must ask ourselves about laurus labs. Are laurus earnings as predictable as some of the other companies? Does market believe so? I would say no. Thus, since you are looking at FY23 earnings whether 14 P/E is expensive or cheap would depend on Laurus’s growth prospects and unit economics in FY23 and beyond. Now investor can do their own homework (by reading this VP thread, and other laurus labs material like the collaborators laurus thread: Laurus Labs: A much bigger journey ahead?) and try and understand what laurus labs would look like in FY23 and beyond. What would the growth prospects be? What would the unit economics be? Are both trending down or trending up. How stable or sustainable are they versus lumpy or one-off. Are there going to be far superior opportunities to Pharma/Laurus in FY23 which cause opportunistic investors to jump ship depressing valuations. Answers to these questions and experience based on studying evolution of valuations of multiple companies over market cycles can help an investor answer whether a P/E of 14 based on FY23 profits is cheap, or not.

PS: Since valuation is an art, all of these are just my opinions. I could be entirely wrong about everything. Also, invested in Laurus.