Thanks Sahil for your response. I agree that valuation lies in the eyes of the beholder. But I want to know how one should do a valuation analysis of such type of company with some assumption about growth. e.g. I was watching one video of SOIC where Ish Mohit mentioned about calculating Bear and Bull scenarios in order to come up with a range. So my question is mainly how should one come up with a range for Laurus Lab?

Also about growth prospects of Laurus lab after FY23 onwards, I am bullish on revenue kicking from Anti ARV API(e.g. Onco, Diabetic etc) and revenue coming from their Richcore acquisition. But I dont know how much. So if one has to think about adding to existing investment, how should we go forward? I always have this question in my mind about valuation and hence I am not able to add good quantity at a particular price. So I am seeking suggestion from the group with example in case of Laurus Lab.

Disc - Invested with largest position(around 10%) of my portfolio.

this is why valuation can only be done after developing a deep understanding of the business. And since a business is like a movie, we need to keep repeating this exercise every few months/years. Some places to start would be

In this BQ interview Dr chava gives some soft guidance on what richcore/laurus bio could look like in K years. I am sure there is much more of this in concalls and IPs too.

In short we have to consume all publically available direct evidence/sources (interviews, concalls, ARs) as well as read industry reports and understand broader trends to figure out the quantum of the growth we can expect. Also, we can track product mix change from same management commentary to understand the way unit economics and margins are headed.

There is another interesting aspect to valuations. One does not need a weighing scale to tell whether someone is fat or not. Similarly we do not need exact estimates of FY23 beyond growth and product mix changes to tell whether a P/E of 14 is expensive or cheap. We only need to evaluate whether there are enough growth and unit economics triggers to sustain or improve current valuations. Then, as a corollary, P/E of 14 on FY23 earnings would be cheap.

Recombinant protein production is not difficult. Biocon produced Insulin even back in 2004 itself using Pichia Pastoris. So that alone can’t be a scale to value Laurus.

Yes. It is a good observation. I have no knowledge of biologics or proteins. Most probably recombinant protein is only a platform from which Laurus bio intends to take off. By acquiring Richcore they have got the entrepreneurs, qualified, experienced staff, ready customers waiting to absorb ten times the existing production. This should give Laurus Bio sufficient resources and a stable platform to branch out into a more complex and rewarding area without any financial support from parent. Here I am presuming that recombinant protein may not be highly rewarding. Considering past performance of the promoter Dr Chava, it has a good chance of success. Picture should be clear by end of FY 22.

Going back to your question about 14 P/E - so considering company keeps on growing at the same rate with the same margins, and considering 14 PE, as per the above chart, it means price already includes growth for the next couple of years FY23. However considering the track record of management and how they have been executing, they can come up with something better, then the stock price and valuations will keep on increasing. Ultimately it will be your call if you can forecast basis all the information which is available …if you are good to buy at the current level or let go this to find something with little more conviction.

I just started following this thread and don’t understand Phama industry - but this is a great company with the great story

Disc: I am not invested

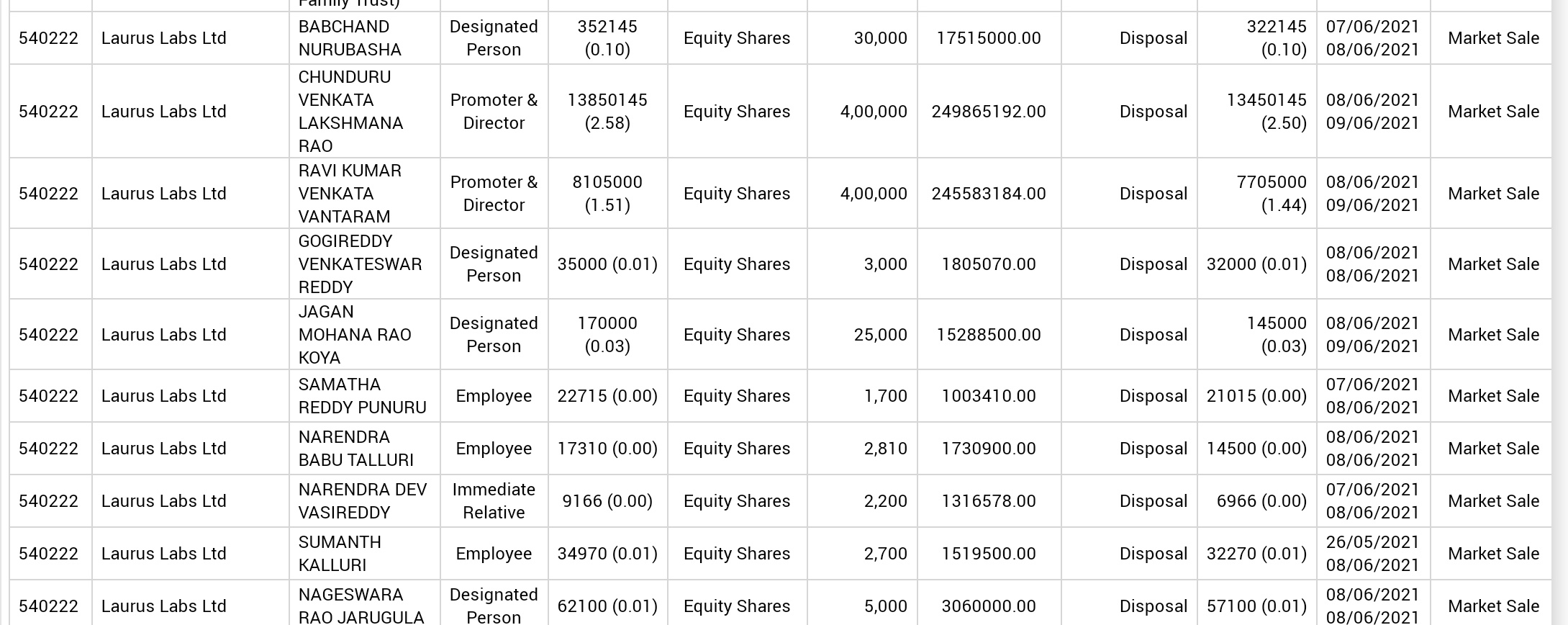

See this in the context proportionate to their holding. Its a very small percentage. In the case of employees, they seem to have got the shares in ESOPs which they have held for several years now. If you see that way, the company has created enormous wealth for its mid level employees. Nothing wrong in liquidating some parts when the stock has made such highs.

Also the company is not run by any family as promoters. All are ex-matrix lab employees, who had come together pooled in money to setup the company. Also many funds had invested initially, who exited during IPO.

After going through so many things since their setup viz. putting their own money, JV with Aptuit, raising money from anchor investors and now when they are doing so well, it is not as if they will shut shop and run away. Of course, this is the impression one will get if one is active on twitter.

Assume a situation where one gets chickened out and sells. The company may come up next month with blockbuster results, some new funds may enter and the price will go further up. No one will then remember this selling. But if one feels, its a red flag, its better to exit. After all its ones own hard earned money.

Ps: Promoter selling is generally considered as a red flag. But then I see Manpasand Beverage, which during its heydays in 2018 when both sales (which eventually was jacked up by circular trading) and stock price was making highs, the promoters increased their stake for 4 consecutive quarters. May be most of the retail need these kind of candy floss

Another thing to note is that the promoters in question still hold close to 2 Crore shares in the company, which is sizeable in relation to the 8 Lac shares they’ve sold.

Leaving out the obvious performance metrics for the year, these are my notes from the annual report:

Filed 27 ANDAs in FY21, nine final approvals, eight tentative approvals. 16% of total employee strength is in R&D.

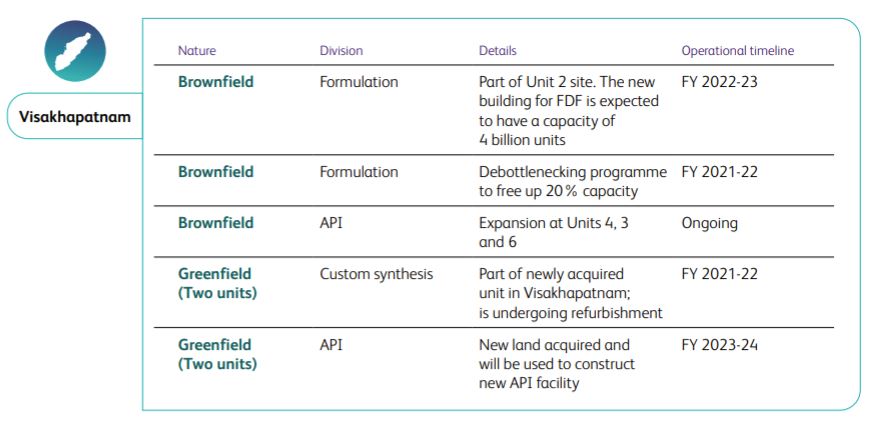

Expanding generics capacities by 1000 KL, around 25% more capacity due to increase in demand from third-party API sales.

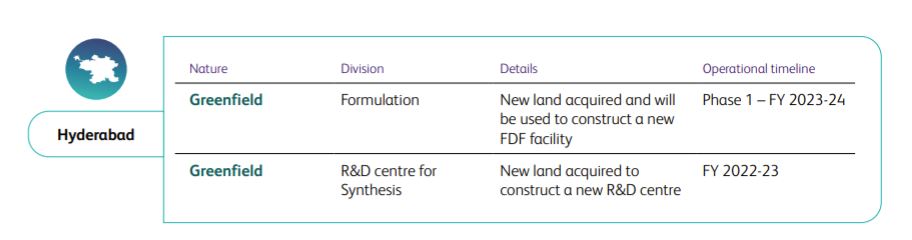

Formulations expanding to 10 billion units / year (known for a few quarters now). Expecting it to be operational in a phased manner from August 2021-22.

Commenced marketing of in-licensed products in the US by leveraging front-end, launched TLE400 in low to middle income countries, entered a long term partnership with a leading generics player in the EU for contract manufacturing.

50 active projects in the CDMO division, added two big pharma companies (overlap with EU generics player?)

Other APIs (anti-diabetic, CNS and PPI) are expected to be key growth drivers due to a robust orderbook and large capacity addition by the end of next year.

Acquired Aspen’s South African subsidiary to get a foothold in the

world’s largest generic-accessible ARV market.

Great place to work certified from Feb 2021-2022.

Raw materials consumed decreased to 44.8% in 2020-21,

against 49.9% in 2019-20, due to better product mix, backward

integration for some of key starting materials and better yields.

Trade receivables are up by 64%, but is considered good by the management and are due within 30-120 days.

On Laurus Bio’s plans:

Aimed at diversifying and entering high-growth areas of recombinant animal origin free products, enzymes as well as building biologics to CDMO at scale. In the future, CDMO will be the largest segment.

We are on course of commissioning large scale fermentation capability and are also planning to acquire additional land for further expansion by creating close to million litres fermentation capacity.

(It’s quite interesting to see what direction Laurus Bio takes by 2023 when we know the biologics/biosimilars market is expected to see huge tailwinds.)

Laurus’ client base + Laurus Bio’s expertise in fermentation likely to have synergies.

On compliance, here’s how they’re staying ahead of the curve:

Increased the level of digitisation of operations;

Facilitated real-time data monitoring and data management for environmental conditions;

Trained our team in advanced quality management with specific programmes to identify quality issues, report and rectify them.

The management commentary from page 46 onwards is a great read. It explores the various segments Laurus is in, and places its comparative advantage within context, and the different opportunities it wishes to capitalise on.

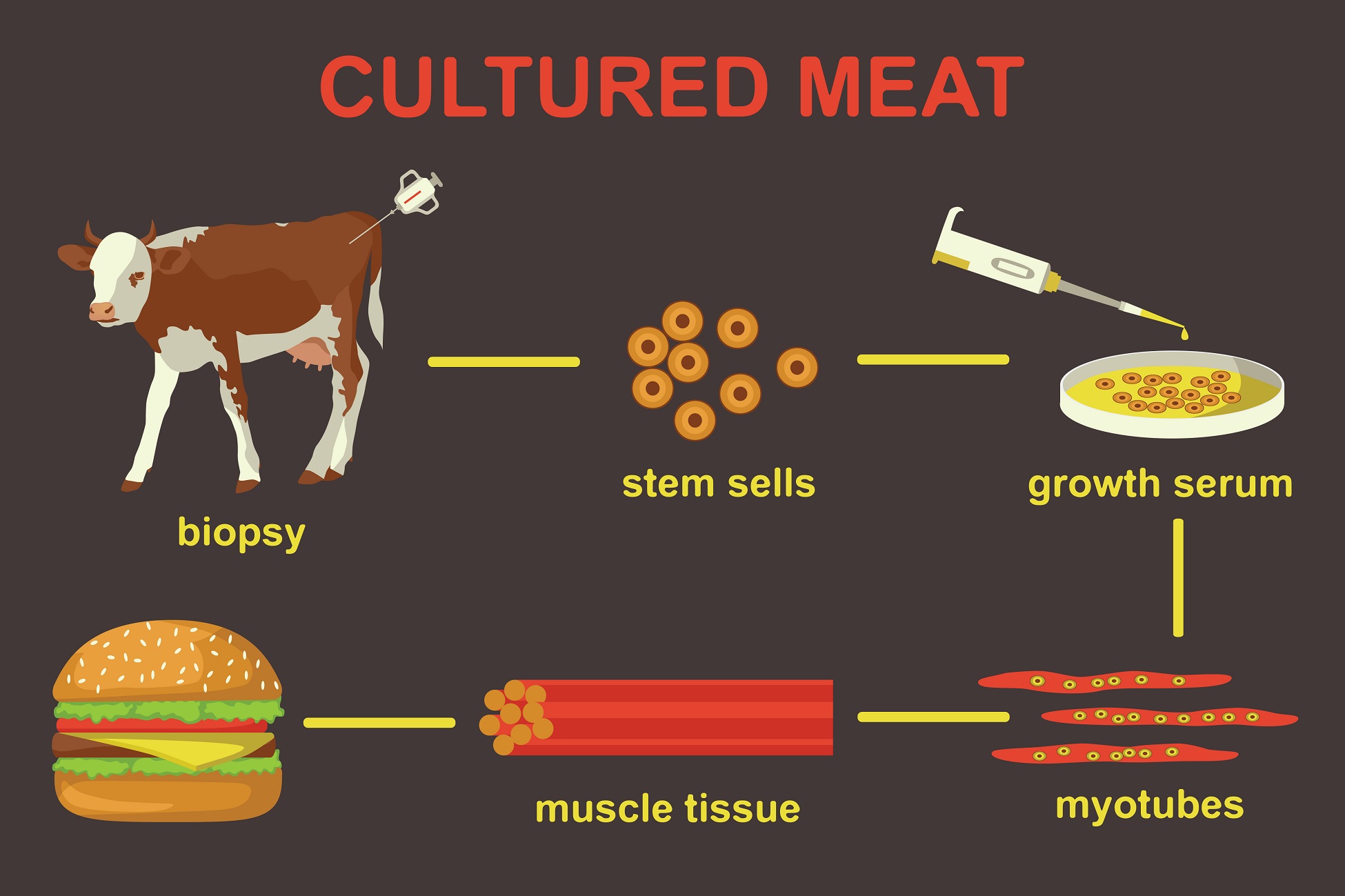

To prevent the slaughter of animals for meat, current research is aimed at harmlessly extracting cells from an animal and growing those cells in a lab into bonafide meat, which is fit for human consumption.

Growing meat in a lab isn’t just humane (thinking about the large scale farms purpose built for chicken slaughter), but offers other benefits as it doesn’t have contaminants(bacterial or otherwise) found in traditional meat.

The developer of the first cultured-meat hamburger suggested that cultured meat could reduce the amount of land animals raised for food by 98%, from 1.5 billion to around 30,000.

Before we get excited about this claim, there is history of a very similar industry to cultured meat that was completely destroyed in the past…

Cultured Meat and GMO: Lessons from the past

GMOs are typically vegetables that have been genetically altered to remove unfavourable traits. Example: tomatoes that have been modified to degrade slower, extending their shelf life.

What happened with this industry? Due to mistakes made during the development and marketing stages, public perception turned vitriolic, claiming they were harmful for human consumption. This lead to protests at international scale, despite a consensus from the scientific community that they posed no additional risk to human consumption than conventional crops. Today, there are similar debates all around us with a generally negative perception of sugarfree products. Only a single variant of GMO corn is sold in Europe today.

Similarities between the development of GMO and Cultured Meat:

Started with small biotech startups and ended with MNCs. Cultured Meat is not yet at the MNC stage.

Early reception for both is overly optimistic, non technical/popular writers make it seem like this is the solution to world hunger. Researchers’ views are restricted to the expensive journals, and write about complications in the cultured meat outlook.

Both are protective of IP as it depends on specific techniques / knowledge, biotech companies defensive of methods / discoveries.

Activists portrayed GMOs as different in kind from other foods, arguing that genetic engineering rendered GM food dangerous to consumers and the environment. The remnants of this sentiment has carried over to cultured meat.

Adoption or rejection of GMOs often turned on changes in framing and perception rather than shifts in technological, economic, or

agricultural realities.

Policy makers making decisions based on perception rather than risk hurt the GMO industry.

Differences between GMO and Cultured Meat

GMO had a culture of secrecy in development that hurt acceptance. Generally understood that cultured meat firms are unlikely to suffer from this.

Cultured meat is not yet associated with large firms. Opposition to cultured meat is currently from meat producing ranchers.

Vegan movement/climate change/ESG movement in 2021 is a new dynamic, something that wasn’t present with the same coverage in the 1990s.

GMOs were in line with / backed by incumbent agri MNCs, cultured meats threaten to disrupt incumbents.

GMO companies refused to take opposition seriously and refused to go for slow organic penetration. Instead flooded the market with their products.

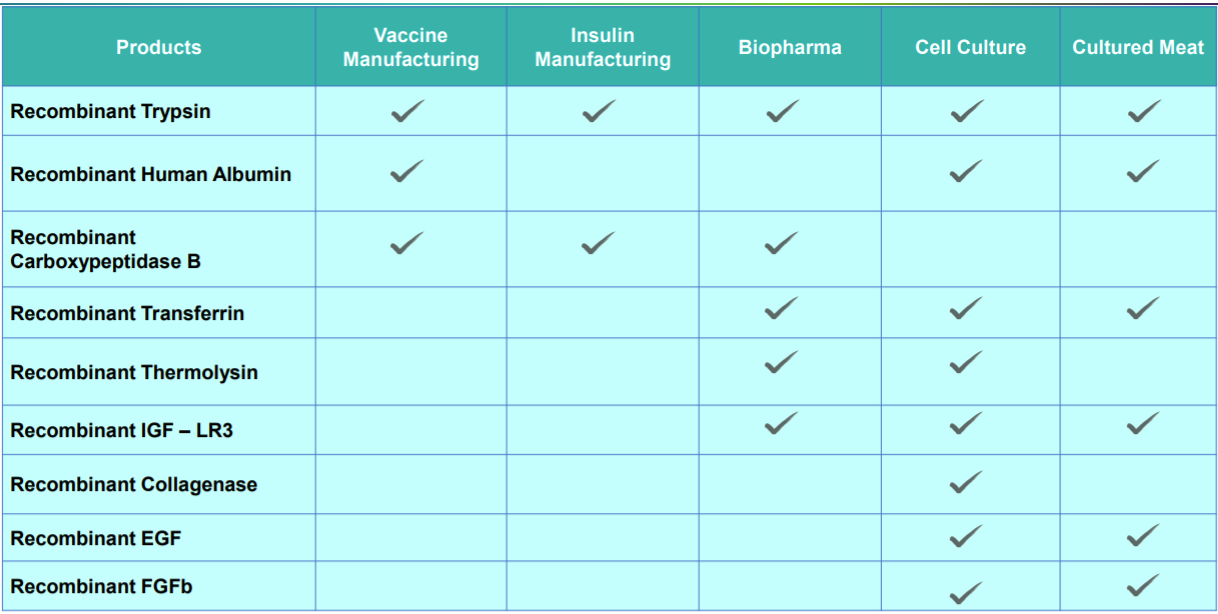

Where does Laurus Bio fit into this story?

Growth Factors

Knowing that the risks of the industry lie mostly in perception of cultured meat, here’s the value chain. (I’m not a biologist, so I would confirm this with your neighbourhood biologist)

Stem cells are like clay, unstructured and can take any shape. I think of Laurus’ growth mediums as fertilizer that helps these cells multiply:

Fibroblast Growth Factor basic (FGFb) is one of the 23 members of the Fibroblast growth factor family. It promotes growth and proliferation in embryonic stem cells, neural stem cells, mesenchymal cells, and endothelial cells. FGFb also aids in embryo development and disease progression such as cancer.

Recombinant proteins (albumin, transferrin etc) and growth factors (FGF, IGF, TGF etc), […] send signals to encourage cells to do certain things such as proliferate or differentiate.

Post this, they’re given structure through something known as scaffolding, and are put into bioreactors for scalability.

Laurus Bio works with startups and isn’t responsible for the overall product and design of the cultured meat, but the cell growth processes that they need to make their products. This means that the downside to cultured meat industry being destroyed isn’t felt by Laurus as much as these startups, but Laurus faces tailwinds should there be an uptake.

Laurus has found a whitespace/disruption in this growth factor space, and is directly addressing the major challenge to the industry. Current methods for procuring growth factors source it from foetal cows, hurting their own aim of being cruelty free(The initial stem cell extraction is harmless, but the source of growth factors is harmful). This sourcing is known as Fetal Bovine Serum (FBS). Crucially, Laurus’ growth factor is animal origin free, and this should give you context when you see these terms being advertised.

Laurus Bio helps cultured meat companies reduce dependency and eliminate animal derived serum and media components such as Fetal Bovine Serum (FBS)

Notice that in this entire write up, we haven’t come across fermentation at all. This is where I found the second disruption/tailwind that Laurus Bio is working on.

Fermentation

Fermentation is the future of the alternative protein industry…The development of advanced fermentation technologies offers food innovators a variety of ‘white space’ opportunities in the high growth plant-based sector.

From my understanding, fermentation removes the need of animal cell culture in the first place, producing animal (and other) products from plant based or non living sources. The second benefit is that it’s much faster and scalable compared to other methods of producing alternative proteins.

Richcore is in the business of developing recombinant proteins which are currently produced in animals or human and in bacterial cells such as yeast, Ecoli, Bacillus, etc. Our customers who are biologics, work with vaccines, cell culture media, or cultured meat companies, are using our products to do away with using animal or human derived products in their processes as animal derived products are subject to viral risks, lack traceability, not consistent or subject to supply demand gaps.

While tracking trends in biotechnology, startups that are going into alternative proteins, stem cell developments, etc. is interesting reading, I’d quickly feel out of my depth. To my relief, the cultured meat segment’s market size and outlook looks entirely dependent on cultural uptake. This means news on the sector should be sufficient to track how it’s evolving(or dying), and we can leave the science to Laurus.

Inviting views and those with a better understanding of biotechnology to post their thoughts on the space. This isn’t a buy/sell recommendation, simply trying to better understand their subsidiary. Can share my readings of the insulin market in future posts.

There is however a deeper question as to why loads of legacy/long run investors in both DIIs & FIIs have also completely exited their stakes over last year, such as Kotak, Sbi, ICICI, Max life, Government pension fund global, Goldman Sachs, BNP Paribas, Bluewater etc while other notable names like Societe Generale, Amansa holdings have cut down their stakes despite positive prospects discussed over the forum, these holdings have moved mostly to retail.

By 2021, the borrowings + other liabilities add upto ~2900 crores while reserves are ~2600 crores.

Could the company find it hard to somehow accomodate these liabilities and when goes seeking for refinancing find it hard to borrow from these financial institutes?

@ASPACETIMEBOT Why have the DIIs / FIIs sold? Nobody can say for sure.

Regarding other concerns, as long as their business keeps growing, everything else will take care of itself.

Their key driver have been ARVs over the last year, and this a business that could get saturated in another year or so, at best. The most important thing would be where would the next leg of growth come from? Would it be onco/diabetes segments? Would it be CDMO? Would it be Laurus bio? If one of these segments can keep the cash flows going, the balance sheet is likely to take care itself.

Thank you sharing and detailing this write up.

Will just add whatever little I have researched on this subject.

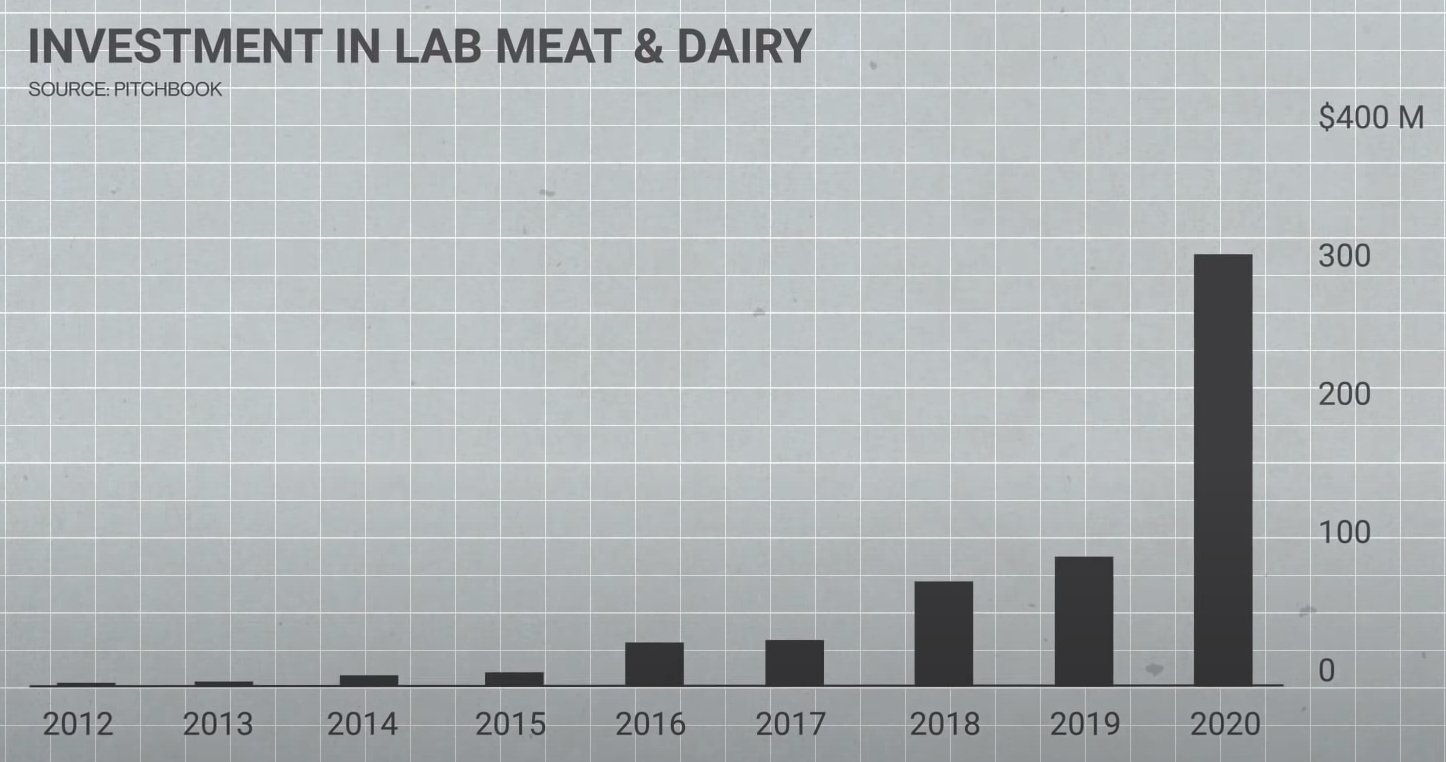

The big tailwind today for cultured meat industry is VC money. VC investments into start ups working on cultured meat has risen exponentially (as shown below).

The main problem with cultured meat (apart from the reasons you mentioned above) is the cost of growing the meat in lab is really high. This is because the growth agents (recombinant proteins) used today are pharma grade. There aren’t very many companies making non pharma grade recombinant proteins for cultured meat.

Pharma grade recombinant proteins and growth agents are really expensive and not really required for cultured meat. It’s like paying for a Ferrari or Bentley when a Maruti 800 can do the job.

This is where Laurus Bio comes in, they are making growth agents and recombinant proteins that are non pharma grade and targeted specifically towards the cultured meat industry.

A startup today doesn’t have to pay for a Ferrari anymore and can finally buy a Maruti from Laurus Bio.

Bloomberg does a very good series on culture meat if anyone is interested. Here is one of their videos from a start up in Singapore that highlights this very problem of pharma grade growth agents.