Having worked in credit on banking side, I think we need to understand few details on how bank lines work. From plain logic, a company which has short term and long term debt, wouldnt keep much of cash on its books and try using the cash generated from operations to repay debt.

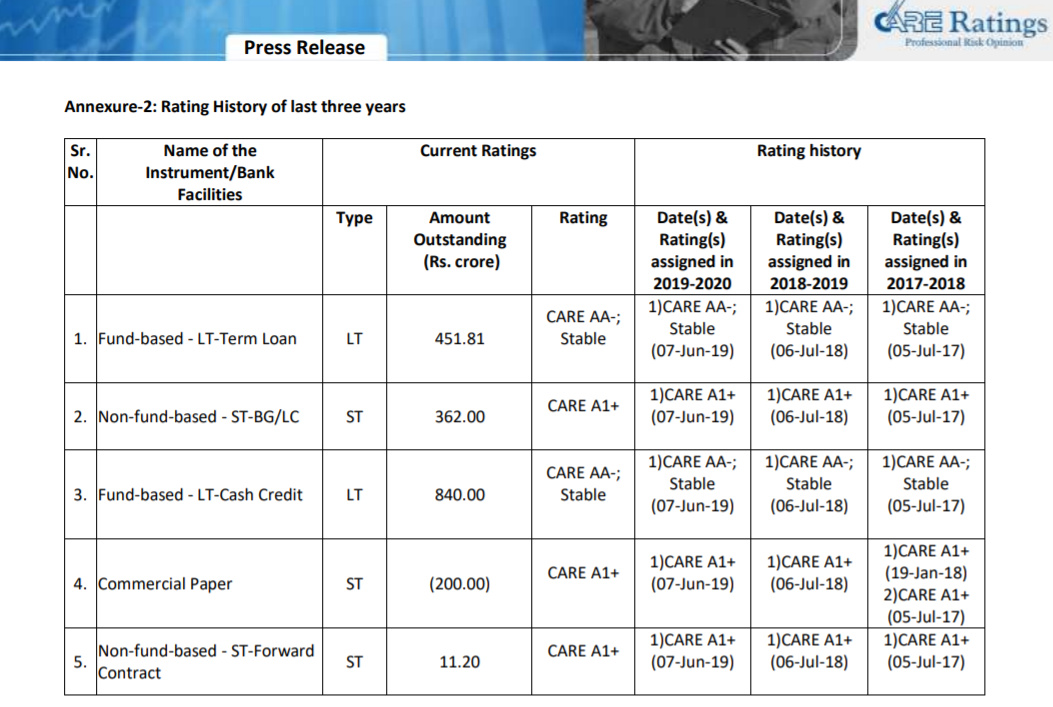

Let’s work out some number for Laurus. Laurus has working capital facility of Rs.840 crore as per the credit rating report (source: https://www.careratings.com/upload/CompanyFiles/PR/Laurus%20Labs%20Limited-06-30-2020.pdf) :

Working capital facilities are given against debtors and inventory (adjusted for payables) and a company can utilize it for it day to day needs (including paying salaries). Let’s look at the current borrowing figure for Laurus as on September 30, 2020. The company had short term borrowing of Rs.752.81 crore as on September 30, 2020 which gives it a space of around 85 crore from it working capital limits for utilization. Furthermore, the company has already approached bankers to further enhance its working capital limits by Rs.200 crore (as per CARE rating report):

Any growing company which has moderately high working capital requirements, would need incremental bank lines to fund its growth (Laurus has grown its topline by 67% in H1FY21) especially when it is also increasing its capacities. Dont think there is anything wrong with it. Laurus has historically had working capital cycle of around 140 - 160 days.

Don’t know why there is too much noise being made about the company not keeping much cash on its balance sheet whereas its unutilized working capital limits can be utilized for its any day to day requirements.

(Disclosure: Not invested and not biased. Wouldn’t like to engage in any further debate on this)

Completely agree, if you have cash credit limits you dont need to keep high cash levels in the company.

Secondly the tweet completely ignores Rs30 to 40crs in current investments (financial assets) and another 60crs in long term investments.

I showed this twitter thread to an ex HDFC bank credit head. He said when he was in HDFC Bank he had given a 500cr loan to Laurus which got paid off. Looking at balance sheet, CFO and creation of fixed assets most banks would want to lend to Laurus…

Only thing he advised me to check was margins of Laurus, are they comparable with other companies. If they are abnormally high (say 10% higher) then its red flag.

In a company inflating p&l numbers you need to show higher capex to plug the gap.

So we should spend sometime doing this exercise to remove that last bit of doubt.

I am assuming you are still invested in Laurus. I am convinced about the fundamentals and the future growth prospects. I would like to have your views on the technicals. Hows the technical chart looking? Want to understand, should I buy more now or the downfall can continue for some time.

To be fair Deepak Kapur is someone who has correctly highlighted red flags in the past in various companies . I have personally benefitted from his views and sold out early before the red flag actually came out to be true. We should always welcome negative views - and then decide our course of action depending upon our convictions and beliefs.

Disclosure : Invested since lower levels

I am aware that interest rates are reducing. But it has not reduced from 8.5% to 5.6%. Corporate lending are generally at higher rate than home loan rates for eg. Present home loan rates are at about 7% levels.

Moreover, the loans are linked to MCLR, which is presently at around 7% +/- 0.2%

So it still does not justify 5.6% rate.

Any ideas on why they have not paid appropriate tax? am I missing something?

I work in Corporate Banking and have a 10 yr+ work ex in Private Banks You are only looking at INR loans. You are right that INR loans are MCLR linked but there are foreign currency loans available as well.

If you look at one of my posts in this thread above where I have posted screenshots from the Annual Report of the company, the company has even mentioned the exact rate of interest against each bank’s loan

Citibank has sanctioned T Bill linked loans(for short term if I remember correctly).

There are FCNR Term Loans by SBI and HSBC which are LIBOR and EURIBOR linked. Depending on a firm’s imports and exports(which provide a natural hedge) and a company’s hedging strategy, the pricing comes to be much much cheaper than an INR loan.

Edit : A small recommendation(might or might not be my place) - When evaluating what someone is posting on social media like twitter, do look at the experience someone who is commenting on a topic has. There are 16-17 year olds giving 12th board exams on twitter whose advise people are taking to invest lakhs, and there are people with 5-6 years of total work experience posting confidently about everything under the sun and providing paid services for investing(all with a disclaimer that they are not sebi registered). Not to say that they can’t be better at investing, but do look at the credentials(search for them on linkedin). Please don’t go by number of followers or number of likes.

Regarding tax thing, what you are talking about is advance tax. The P&L account will only show the tax expense which is calculated separately. It’s quite complex, but in simple words advance tax and tax expense are two separate things.

Thanks for your response.

So did the mix of loan changed from say March 2020 to September 2020? All these loans you are referring to were in March 2020 as well. March 2020 average rate is 8.5% and September 2020 - average rate is 5.6%. This was my question initially. I do not deny that FCNR will be lower cost than INR loans.

Sir, Tax expense is roughly 22-23% overall, which you need to estimate for the full year and pay advance tax accordingly. They have clearly calculated their tax expenses as we can see in Q1 and Q2 financials.

Though it is not a big amount, but there is a shortfall of 40-60 Cr in tax payment.

short payment/deferment of adv tax attract interest@ 1% per month, if they are not paying advance tax upto 90% of estimated liability (For whole FY20-21). So if a co pays less tax than its tax expense (excluding deferred tax) than it can be a bit of red flag.

Post is only for academic info. Disclosure invested from lower levels

Laurus as I understand has 6 units and 4 of them are in SEZ.100% Export income generated by SEZ is wholly exempt for first 5 years of operations. Thereafter, 50% of export income for next 5 years and 50% of ploughed back export profits. They would be availing the benefit of the same. Have you factored this while saying there is a shortfall in taxes paid? If you have done, you may please put the detailed working here for the benefit of all of us showing that despite the benefit being availed, there is a short payment of tax. We can then take it further.

Edit: I understand your interest in the company and you have rightly said its bit of a red flag (assuming you have all the details that they are short paying). But if you post something without proper backing material, then it will take a completely different color when it reaches out. Your bit of a red flag will become a big red flag. Some one will add on a bit of a masala and make it a case of tax evasion. So lets not jump to conclusions without solid research or material. You know how twitter/WA works these days

Ok. Verified from the company. They did make a short payment in tax. As per email I received they paid 100 Cr by end of October (figure upto September was 61 Cr) and paid interest for one month.

Though I am not sure whether interest is only be applicable for one month, or it is applicable till Dec 15, i.e. 3 months.

There is a possibility of a change in mix loan but you can get to know that only in the next Annual Report I think, as entire schedules for Q2 results are not available(I think). You initial question assumes:

That Borrowing at Sep2019 was also the same 1000 Cr(I did not have the time to verify).

And if that is the case then MCLR/Libor rates for Sep2019 should be compared.

Also note, the reset of interest rate for all loans is also different, so it is very tough to know which month’s MCLR rate is applied to which part of loan. And hence, interest rate is not the right parameter to look at. The total debt(short term plus long term) is the figure to look at.

There has been a lot of discussion initiated regarding a twitter post, so just want to add a couple of points(would be happy to be proved wrong and if I am incorrect somewhere:) ):

If a company already has high WC, why would they keep cash and bank balance. There is no need. Companies get 0% interest from current account float(they can’t open savings accounts) and there is no point trying to make interest on FD when you have loans outstanding. All companies have a CC limit(similar to an overdraft limit), so al payments they receive reduce this limit utlisation on a real time basis. It wil be surprising to find a lot of companies which have short term WC loan and are keeping huge cash and bank balance on their balance sheet.

Company’s WC limits from their banks are sufficient to take care of WC needs and there is no emergency as is being made out. The amount of WC limit set up by banks takes into account Inventory+Trade receivables-Trade payables. All companies submit a monthly stock statement to all banks with this calculation and divides the total amount between their banks so that out of the total WC need for a month, they can’t even use more limits even if they have a 100 Cr more WC limits sanctioned. Hope I have been able to explain.

Hence companies of all sizes can operate without cash on hand if their cashflow routing is being done through the accounts with CC/WCDL limits set up with their bankers(banks even ask for exact proportion of sales as cashflow from their account). I think no one is taking out a dataset of balance sheet of all companies with WC loans and calculating how much cash and bank balance they have. Re-iterating, it makes no sense for a company to keep cash and bank balance when they are paying interest on a running CC limit.

If the WC limit utilisation is not reducing, it is not necessarily a red flag. With increase in sales, Inventory, trade receivables and trade payables will also rise hence WC needs also rise. You have to judge the corrosponding increase in borrowing. If short term WC is not increasing at a faster speed(or even at the same speed sometimes), there probably is no cause for alarm.

The company is putting in money and taking on debt for Capex, and they have high short term/W; if you are comfortable with that, invest. I am not comfortable with companies with high debt, hence I am not invested(as I have posted in detail earlier).

But panicking because there is no Cash and Bank balance for daily WC usage, when the company has enough sanctioned WC limits and their DP calculation(using Inventory+Trade receivable-trade payable) is adequate, does not make sense to me personally and I would be happy to be proved wrong if I have made a mistake somewhere

Not sure why would you compare with Sept 2019 numbers? I am just comparing with March 2020 numbers. March 2020 borrowing is 1057 and Sept 2020 is about 1015. Not much change in the borrowings.

So change in interest expense can be justified by two things:

Drastic reduction in Rupee interest rate - from last year (3%). Which I don’t think happened.

Change in the mix from March 2020 to Sept 2020 with increased FCNR USD loan and reduced Rupee loan. We will not know this till notes to accounts are available.

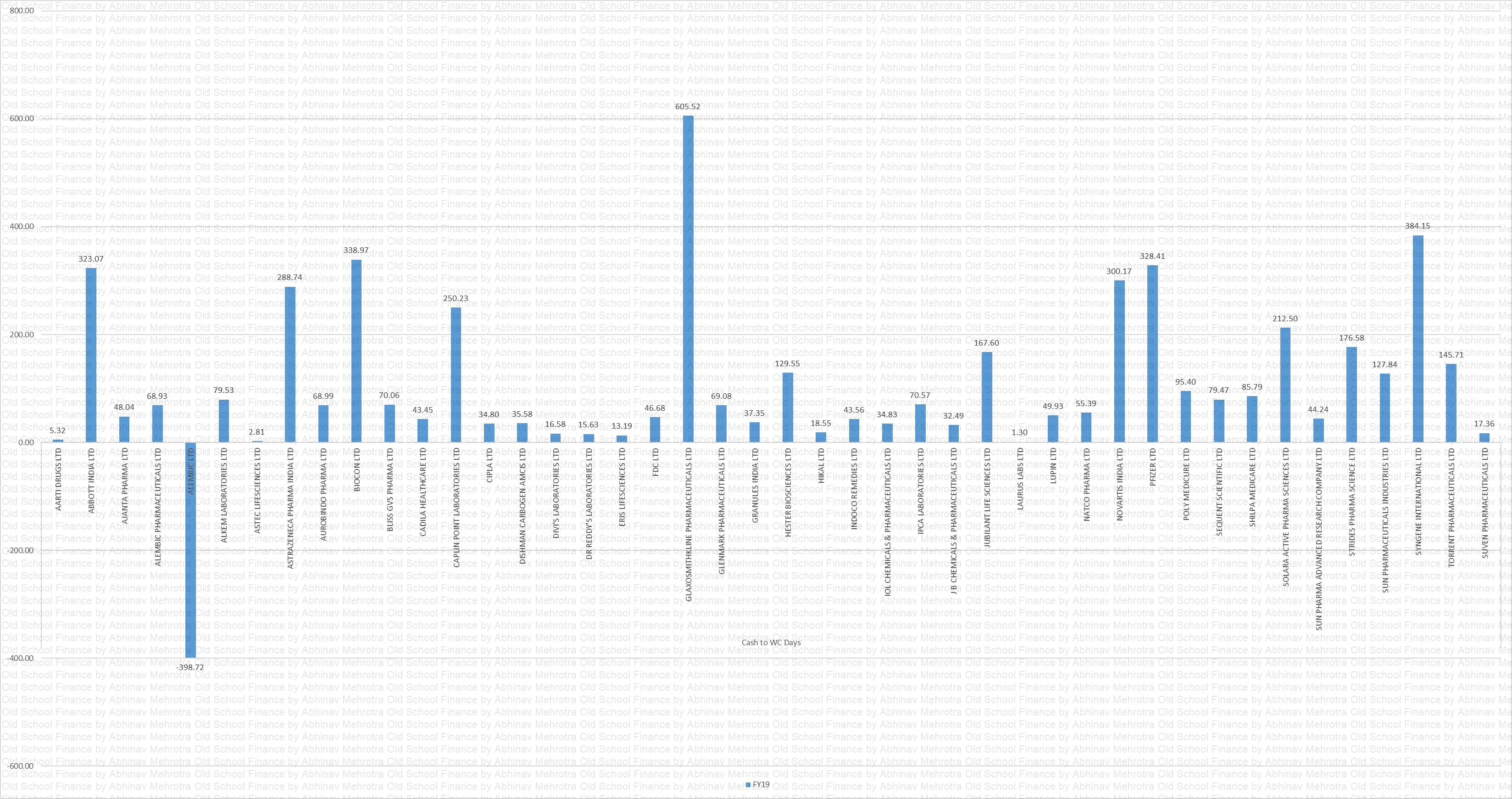

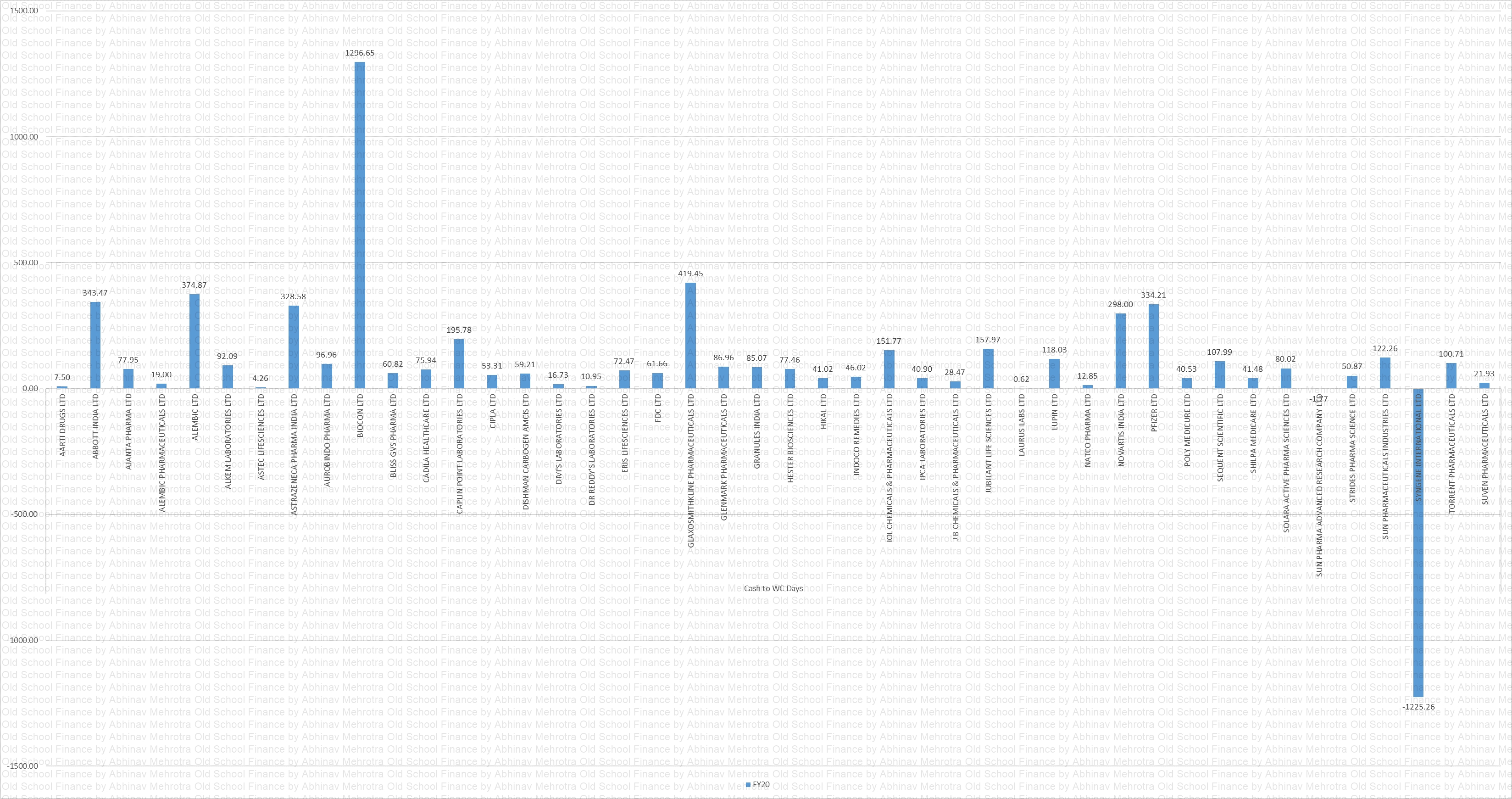

Collected some data on major pharma companies. To come up with industry-standard cash to WC metric.

I define Cash to WC Days as (Cash/WC)*365.

Data is picked up in a semi-automated way through screener website. WC definition is as per screener, other assets - other liabilities.

I can show the data in a time series as well with comparable companies together. But the chart is unreadable with all companies data, I do not know which would be the relevant companies to compare with. Tried market cap. grouping but the comparison did not feel right.

I have very limited understanding of accounting practices but usually what I remember is sometime, the hedging related gains can impact the interest cost in both ways (losses lead to increase in interest outgo & gains lead to decrease in interest outgo). I could be wrong & happy to be corrected.

Disc: Invested from lower level & positively biased

You are only looking at INR loans. You are right that INR loans are MCLR linked but there are foreign currency loans available as well.

You are only looking at INR loans. You are right that INR loans are MCLR linked but there are foreign currency loans available as well.