https://bigvisioninvesting.com/tag/low-cash/

A good blogpost by a VPer on Laurus

Chava again asserted confidence in the future growth prospects of the company.

The full report of Ambit Capital dated 3rd August, 2020: https://bsmedia.business-standard.com/_media/bs/data/market-reports/equity-brokertips/2020-08/15964424670.53106300.pdf

Hope this is of help to someone who wants to read what Ambit has to say about the business.

again promoter buying seen in Laurus

Chandrakanth Chereddi - 3500 shares on 6th November

Just for info. deleting the post in a while, as it wont add much value

No views on laurus…But sandip sabharwal used to think that Avanti is a fraud too…blocked me when I challenged him on it

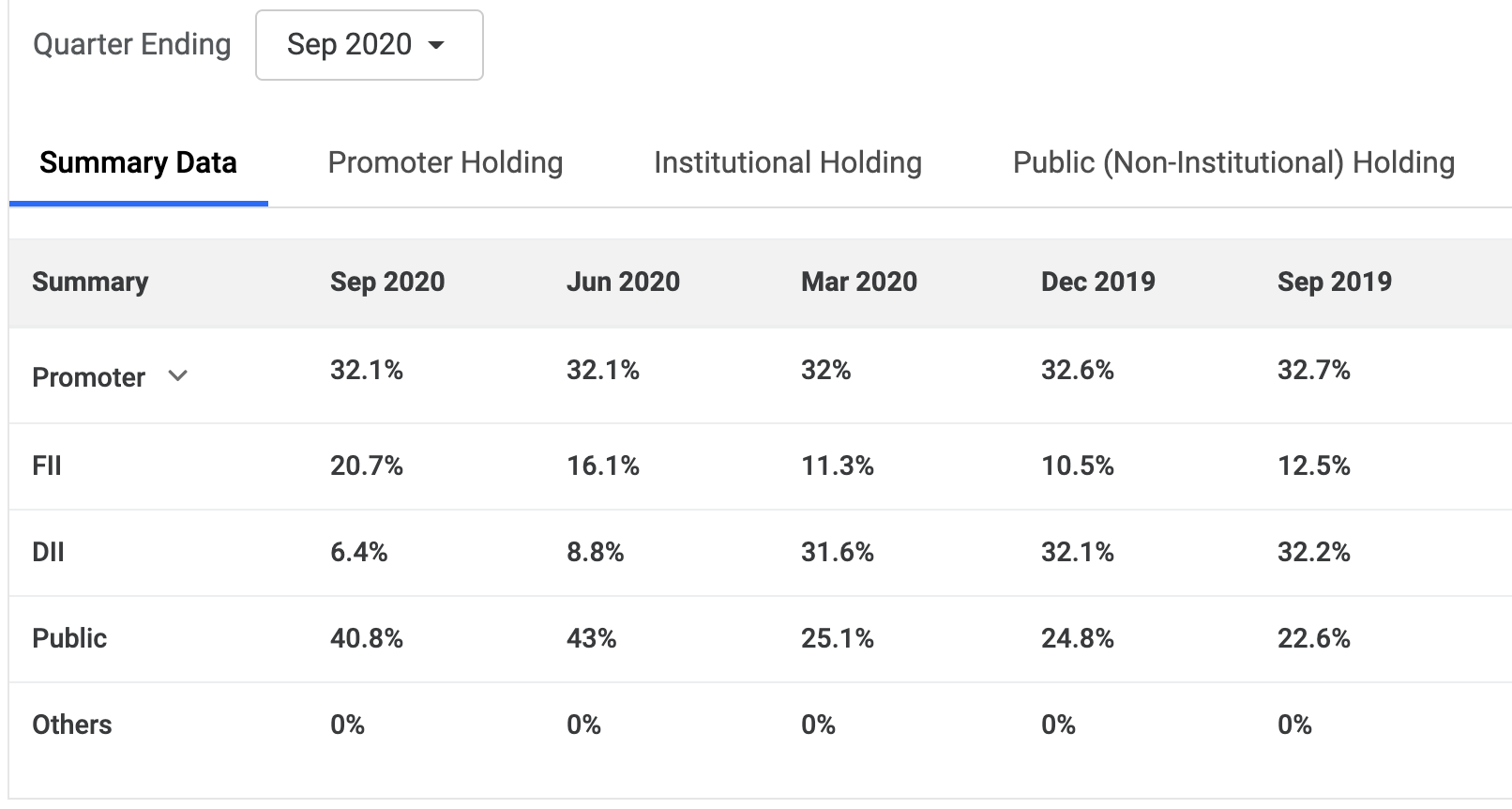

One thing that I am not comfortable is DII selling. Some promoter entity is classified as retail but I would be very cautious seeing below chart.

I want some opinion on one particular question that was asked to Dr. Chava in multiple interview (including concal).

“How much of current profit surge can be attributed to covid?”

The answer Dr. Chava gave was that it is irrespective of covid. In the concal, he also went on to say something more. He said that prescriptions are advanced now. Instead of giving prescriptions say for duration in weeks, prescriptions are being given for longer duration to avoid frequent doctor visit. but still the profit surge is not due to covid. The market was already there. I can come up with some combination (say 6 months prescriptions) of the durations were we can show that profits will be lumpy and over 2 quarters or more. We cannot say conclusively until we know what kind of prescription duration we are looking at.

I am going by what Dr Chava has said, since his words have checked out in the past. And if what he says about next 2 quarters holds, then it is undervalued even at current price in plain PE terms even current price.

Let us kindly not stop discussing the company and prospects. Weak hands will always leave. At the end of the day every conversation gives clarity. IMHO, short term market movement one can never predict.

Disclosure: I have fat money in laurus. I don’t plan on selling one bit of it as of this day. Open to exit and not in love with any stock :).

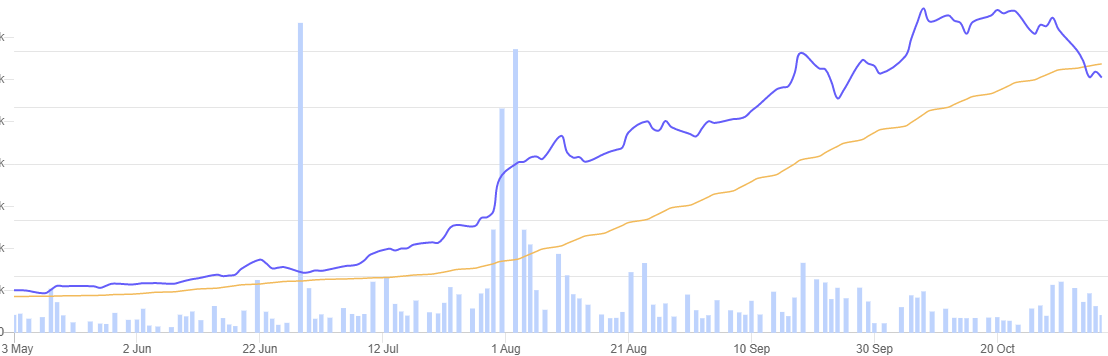

Typical scenario where promoter group has started buying, although in very small quantity, the slide doesn’t stop.

We must note that… for the first time in last 6 months, it has breached 50 DMA as well

Even though we trust management & no doubt Laurus came up with stellar numbers in last 2 quarters, but isn’t it good to have a plan B when it goes into price correction phase after more than 5x run in short time.

DII’s normally chase short term returns, otherwise they will be out of business.After massive pharma rally , the sector is in consolidation and some profit booking is happening. Also sector rotation is happening as most the the investors are short termers. Laurus has many growth verticals led by competent promoter which is visible in the results. In my opinion as an investor one needs to focus on the business rather than what others are doing and align our interests with that of the promoters in the long run will only create value. Most of the times DII and fii are forced to book profits after every rise.It’'s difficult to find a growth story like that of Laurus.

Disc. Invested and biased

Yes. Sorry, I should not have mentioned weak hands in my post. My position is irrespective of whatever kind of hands are exiting. Since I am having high conviction right now with whatever information we have in our hands.

Having said that, it would be good to know why a lot of DIIs are leaving. Though this tends to be very very difficult to know.

Can someone please tell if stock edge data is wrong here. I see quiet a few MFs buying in sept.

https://web.stockedge.com/share/laurus-labs/82380?section=mf-holding&assetHoldingDate=2020-09-30

I think posters in this forum need to ask themselves a couple of questions since it looks like many people have conviction in the stock price and not the company atm.

“It’'s difficult to find a growth story like that of Laurus”. Thanks for saying this. This is my conclusion too about Laurus. Looking at adding over the next two quarters as funds get freed. Another business with similar attributes building/converging is Deepak Nitrite though at a slower pace.

Q2 Result analysis by SOIC to clear the noise surrounding Laurus!

https://www.youtube.com/watch?v=BAx3E0rB5_g&t=3784s

Kindly recheck the data.

Retail shareholding as per SHP is 8,51,68,480 + 6,40,71,465 = 14,92,39,945

Deliverable Qty combined (BSE+NSE) 30TH OCT - 9TH NOV = 2,46,70,630

Deliverable qty is not 3.43x of retail shareholding.

interesting to see both promoter and employees buying from open market( especially when employee is VP finance )

https://www.screener.in/insiders/details/48472/

https://www.screener.in/insiders/details/48473/

Invested and adding

Small clarification: His point of longer duration medication was on HIV medication (Shift from single month dispensing to multi month dispensing. Preference for 90 day medicine at one go over 3 monthly visits for 30 day medicine.

He also clarified that they are not into Favipiravir, Remdesivir, etc - and hence no one-off elements / Covid related spike in the results

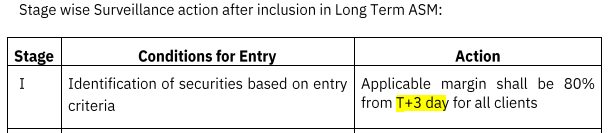

Laurus Labs has been added to the asm list

https://www.nseindia.com/reports/asm

Based on what’s happened with granules(iolcp too) there could be a 2 month rangebound movement now. Granules was my first exposure to the asm list though. So maybe someone more well versed in it can explain the nitty gritty. From what I’ve learnt sebi checks twice a month and usually removes a stock from asm after 2 months. In that period margin based trading isn’t allowed ie only 1X trading. Brings volumes down by a huge amount and sets low circuit filters and hence has lead to stagnation for a while in previous scripts with not much downside and not much upside during the period (though there have been exceptions to this for eg Adani green) but doesn’t reflect anything at all regards the actual company. Also, one cannot pledge their asm stocks as collateral for loans. So some selling pressure can be seen.

Note:

Stock moves to ASM based on few criteria… and one of them is “High-Low price variation in 3 months >150%+nifty50 variation*beta of the stock”

As everyone was aware of sharp price movement, was the recent fall planned to avoid above criteria or EXPERTS were aware (based on calculation as above formula is known to everyone) & SMART people have PLANNED accordingly.

Learning for retail : be aware if your holding moves too fast… you must calculate above & book profit before such surveillance measures strangulate the prices despite block buster results

Existing pledge shouldn’t have any impact but ASM may come in picture for fresh pledge.

More details on ASM

We must note that ASM movement doesn’t come with immediate effect as Laurus traded on older applicable margin today.

ASM stage-I refers to applicable margin and doesn’t change the circuit limit hence 9% movement mentioned is irrelevant to this discussion.

Various stages of ASM have different actions and you don’t see change in circuit limits till you move to stage-IV

Any analysis remains incomplete without support of data.