Cumulative cash from operations for last 5 years compared with the profits and as long as it is 80% or more of the profits, should be fine. Expecting free cash flows from a company which is doing capex is not feasible, so this can be ignored as long as it generating healthy ROCE and ROE. Last concall I vaguely remember they had said about ROCE being 32% and this time around 37%. Operating cash if ploughed back and healthy ROCE is generated, I think no one would have any complains.

Debt is something to be closely watched. In the concall they have said that the capex going forward will be using internal accruals and no more borrowings. Debt I think is serviced at 6% and therefore, will continue and there wont be reduction. We have seen in the name of chasing growth, capex, expansion so many cos have gone belly up. So as long as it is within comforting levels, it should be fine.

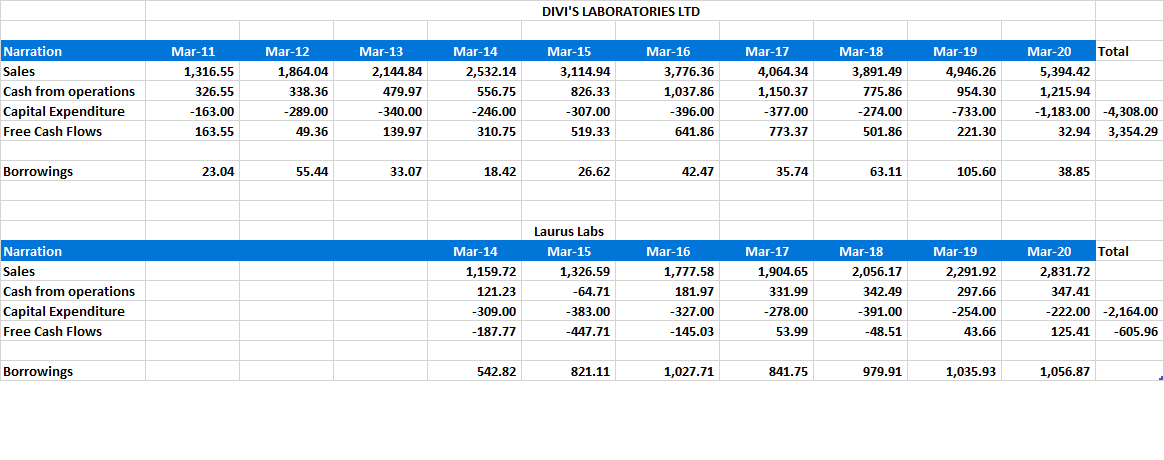

The question then comes to mind is how did Divis Lab create so much wealth without any borrowings and at the same time generating huge free cash flows. Divis though may not manufacture similar products as Laurus but is in similar line of business. The data is not strictly comparable as Laurus has been around for last 15 years and Divi’s is celebrating 30th Anniversary. Also data of Divis I could get from screener was for 10 years whereas, Laurus only for 6 years, after it came with the IPO. Strictly, I dont know how the position was with Divis when they had started say 20-25 yrs back. The other members who may have data may please help. Nonetheless, Divis has made capital expenditure of Rs.4308 crores in last 10 years.

The sales of the Divis for the last 10 years have compounded at the rate of 19%. It has increased from 942 crores (March 10 ending) to 5394 crores (March 20 ending). In this 10 years they have invested heavily to create capacities. One more interesting point what I found is that their operating margins never fell below 35% in the last 10 years and was broadly in the range of 36%-38% in the last 10 years.

If we see the last 5-6 years sales of Laurus Labs, it is more or less what Divis Labs was making during 2010-2015. But see the level of FCF and the debt levels of Divis

Divis in the last 10 years, without any borrowings (very small) has been able to create capacities of Rs.4308 crore (internal accruals mainly) and also able to generate free cash flows of Rs.3354 crores.

So the proponents of free cash flows are not completely wrong in asking for it.

From 2010 to 2015 the interest rates in india were very high. So that might be the reason divis never went for any loan. Now laurus is paying only 6 to 7 %. So I dont think there is any reason to reduce the debt as long as it’s under control.

I have not gone much into number details. So, what I say could be wrong. Would be happy to be corrected.

If you look at the history of Laurus from listing:

at the start they were pure antiviral api company, where the they grew fast but I believe the margins and return ratios wouldn’t be great.

challenge 1: then they had good revenues from hep C but the pricing and hence profitability eroded fast. This is no more an issue, I guess, since it’s contribution is low now.

Laurus had good revenues due to effiravinz api but the treatment got shifted to daultegriir for which Laurus got approval only a year back. Effiravinz dosage got reduced too. Daultegrivir story for Laurus is yet to fully play out, if I am not wrong. Unlike effiravinz, for which Laurus, supplied only API, Laurus supplies only formulations for doultegrivir, hence higher profitability.

Laurus went for huge capex along with the capex needed for CDMO for aspen. It slowly ramped up. Capex funded interest free by Aspen(200 cr). High margins but raw material price fluctuations entirely affects Laurus both +ve as well as -ve.

Laurus was affected by intermediate pricing during 2019, when already going through above challenges. It resolved these issues by backward integrating the intermediates. Key starting material is still 90% from China, which is still a key risk.

This is a hunch, but I believe Laurus might have changed the KSM suppliers too for better prices and price stability.

Laurus was expensing out lot of opex, which was not needed.

With all above challenges in last 3 years, profitability got affected. But I believe, things are going to be different now. How? Its mentioned below.

they are not pure API anymore. The antiviral formulations (especially daultegrivir) and European CDMO related formulations are highly profitable. For Daultegrivir, Laurus has same lowest cost advantage as effiravinz.

the synthesis, which is high margin business is growing well.

the high margin CDMO business, which is gaining momentum just now. Dr Chava is giving all the resources it needs like dedicated R&D lab, funding, capex etc

Laurus is able to muscle into highly competitive metformin, pregablin. This indicates good chemistry strength. According to him, they want to be last man standing in other terms “lowest cost producer” through backward integration, scale & probably some process advantage (patented or otherwise).

Laurus has in no time became one of the largest high potent API manufacturers (if I am not wrong) only during last 2-3 years. If I am not wrong, this is for high margin oncology molecules.

They are now distributing own products through their own front end in Europe as well as US, if I am not wrong. This started only a year or so since.

Edit:

14) Forgot to add the clean regulatory compliance record (FDA & others) & high focus on quality (he boasts of huge number of quality personnel he employs).

15) In his previous career before Laurus, he seems to have worked in all the divisions in the Matrix laboratories, which probably will put Dr Chava in a unique position to lead the company well.

So, I believe, the past four years are no reflection of the bright future for Laurus.

Risks like highly dynamic pharma industry, raw material dependence on China, possible customer conflict due to being in both api supply as well as CDMO, key man risk, high depandance on HIV, lot smaller than an year back margin of safety etc are still there.

All the above observations are based on the knowledge I gained from following Laurus only by reading concall transcripts. I don’t have much knowledge about either pharma or investing. Don’t base your investment decision based on this post.

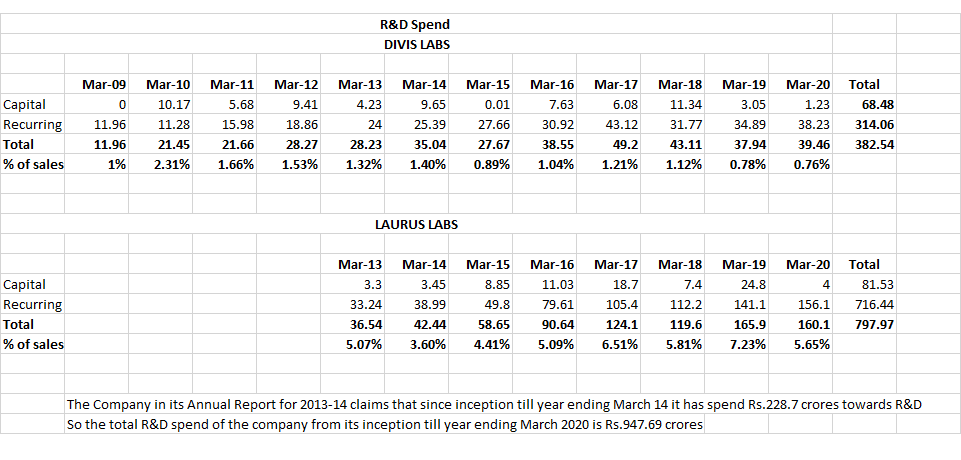

When it comes to R&D spend, Laurus is way ahead of Divis. Laurus consistently has been spending 5-6% of their sales on R&D (both capex and opex) whereas, Divis spends only 1% or even less than that.

For the last 12 years (year 2008-09 to 2019-20), Divis has spent a total of Rs.382.54 crores on R&D whereas, Laurus in the last 8 years alone has spent Rs.797.97 crores.

Asper Annual Report of Laurus for 2013-14, it has spent since inception till March 2014 ending a Total sum of Rs.228.7 crores on R&D, which results in staggering Rs.947.69 crores on R&D till date. The amount is very big for a company of its size.

The other aspect which is a matter of concern generally in most companies is capitalizing expenses and thereby showing better bottomline. But here Laurus seems to be very prudent and expenses out most of the expenditure than capitalizing. This particular para in the 2013-14 Annual Report I found very interesting and should allay most of the concerns.

“Besides, the Company demonstrated credible conservatism by consistently investing 4% of its revenues in research and development, which was written off completely to its Statement of Profit and Loss in the year in which it was expended even as there was a case for these to be progressively amortised; the Company provides depreciation with the objective to write-off all capital investments in 10 years as against the industry practice of writing them off in 19 years; the Company has not capitalised a single rupee of goodwill or pre-operative expenses”

A company can fund its capex either by (i) diluting equity; (ii) borrowing and/or (iii) internal accruals. In the case of Divis, its was very little borrowing and rest by internal accruals. If they had to borrow, they would have irrespective of interest rates. So the point I was trying to make was about how they could manage their cash from operations to fund the capex and then also generate FCF.

Also I dont think, the interest rates during 2010-2015 were very much different. You may please share details of interest rates during those years if you have. That will help all members.

Patents one of the key USPs &strength of Laurus labs. Its focus on process innovation enabling it to manufacture APIS FDFs atmost competitive rates enables its to take market share away from competitors.

Incremental ROCE much better then cost of capital .

Any scuttlebutt done on Dr Chava & Laurus wud be really useful?

During the 2010 to 2015 inflation sky rocketed, banks were paying 9%on fixed deposits. Now the interest rates are half of those days.

Ps: I’m a branch manager in a psb.

The best business - one which can reinvest profits at high ROCE. It fits with Laurus Labs. So no need to care for Free Cash Flow. But ROCE is dynamic. It is the function of market forces. Granules has been reporting excellent results continuously for many yesrs but share did not increase except in this pharma boom. So avoiding FCF might be possible for companies with Moat like Avenue Supermarket(Its moat is also dsbatable now). For laurus, nothing is protected. Patents are for Process Patents which can protect low margin business. High margin business can invite invention of other processes to dent margins. It is in nature of Pharma business in India as they are not innovators. So market may increase valuation till pharma boom is there. After that it might be the case like Granules 2015-20, it depends how high PE it gets.

Disclosure - Entered recently with very low stake for tracking position after profit booking in past.

Although the post was deservingly deleted, I had read if before it was deleted. Man… you have a career in fiction writing. This conspiracy thing ranks right up with authors like Ludlum, Grisham or Frederick Forsyth. As posters on a public forum we cannot put up gory details of hypothetical frauds without any substantiation and I guess that’s why the post was probably flagged and deleted. But I must confess you take imagination to another level.

There is a lot of negativity surrounding Laurus mainly because the stock has corrected inspite of what are phenomenally good results. There are a couple of mahagyaanis on Twitter letting it rip on the company citing cash flows mismatch and other logic calling this company names and trying to malign the company. I read some of their tweets forwarded to me by some friends (precisely to avoid such guys I am no more on twitter) and what I find is that these guys have made it their business to post cryptic posts without any data points, but alleging misdemenaours and hanky panky in companies. I would like to see these guys put up a couple of good ideas and put their reputation on the line. Its very easy to discredit someone or some company especially when you have a lot of followers based on your past reputations. A lot of guys are questioning ambit guys who reportedly had an 11% stake in laurus back in around june and now hold it no more (and still come out with a buy report on the company with higher targets ). Sometimes I think these brokerages hold positions for big traders and often sell out on getting instructions from their clients.

I prefer to rely on facts and the facts are present in annual reports, concalls and reported numbers. In the short term markets can be illogical and react negatively or not at all to great results or newsflow, but in the longer term what matters is earnings, earnings and earnings.

This is not a recommendation from my side but my viewpoint as an investor.

Ambit IMHO was just a bridge (escrow) ac for warburg stake that was sold off to dfferent entities like madhu kela Bhanshalis n few other reputed investors as per the grapewine.in Q3 FY 21.Ambit buy side had nothing to do with this

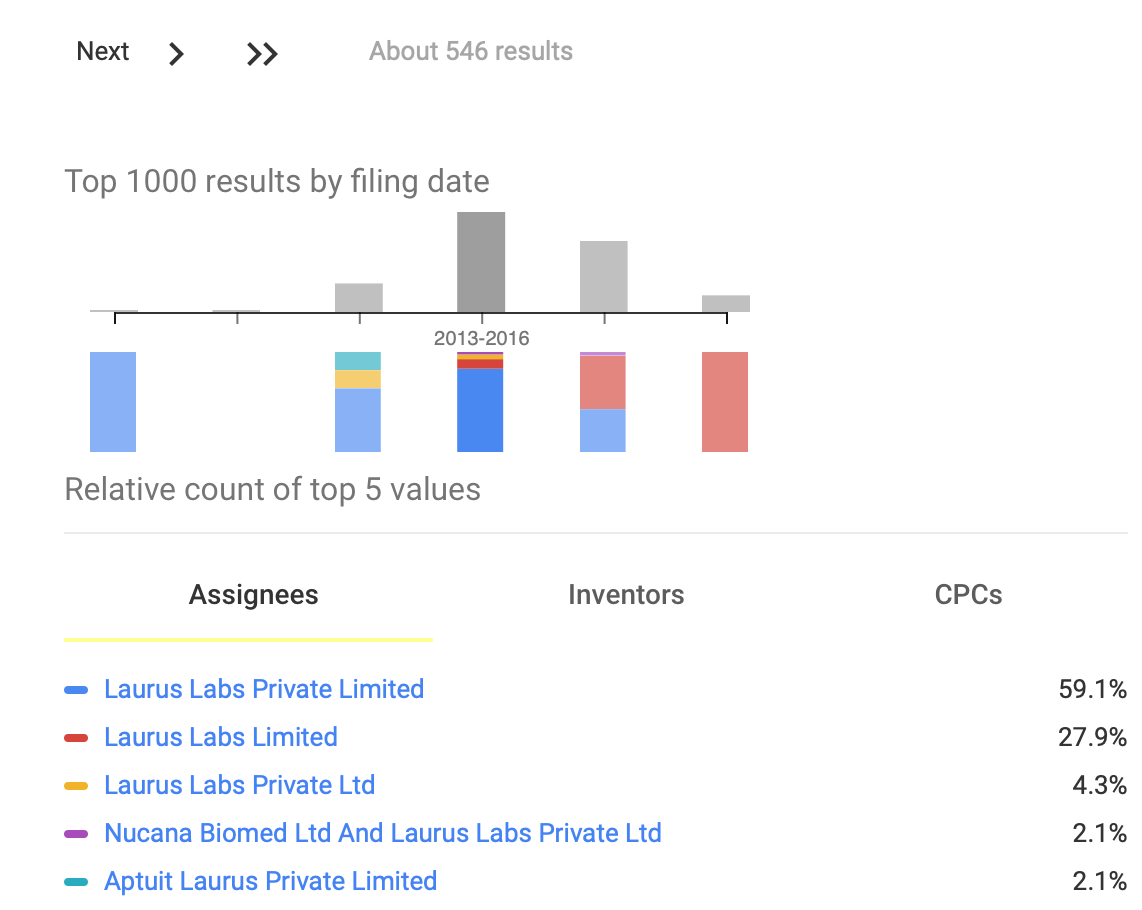

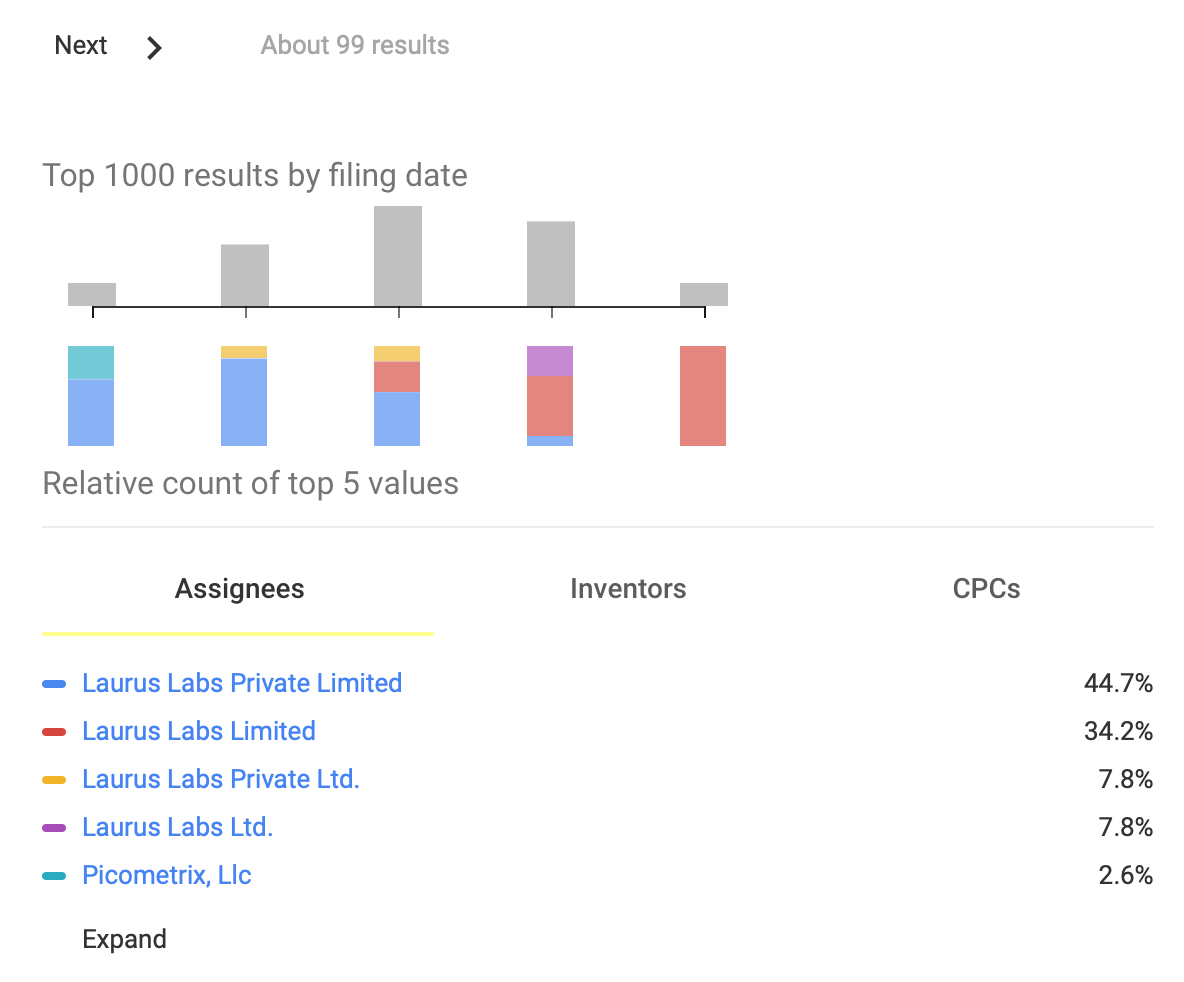

Google patent search gives following summary graphs for Laurus Labs

4 right most data point represents a 3 year period each

2010-13

2013-16

2016-19

2019-22 (right most)

2013-16 is period when they (Laurus Labs Private Ltd) filed most number of patents.

Now among the two graphs first one with 546 results have patents from different patents offices (US, JP, EU etc), mostly same patent is filed in different offices. Second one with 99 results includes patents only from US patent office.

Among these 99, ~50% are granted and rest of others are under process. There might be some which may not have got published yet for public comments.

I doubt if this patent filing is unique to Laurus, is’nt all generics companies has to go for process variation, and patent the same ( to enable them bypass drug patent, allows them to sell in markets which recognize process patents)?

I have a couple of questions regarding interest and tax:

I understand that borrowing has not reduced much and stay at 1000 cr + levels. However interest cost has reduced by 33%. Any idea why the interest expense has reduced? I arrived at the rate of interest to be about 5.6%, which was around 8.5% in previous years. What is the reason for such reduction in the interest cost/rate

The tax expense so far is in the range of 121 Cr. However, till H1, the tax paid is only Rs. 61 Cr. If we assume similar growth in the next half as well, the total tax expense will be about Rs. 260 Cr.

Considering the company should be paying 45% as the advance tax by September 15, the tax paid should be about 120 Cr. Why has the company short paid the advance tax?

This is because Interest rates are reducing across banks for Corporates(due to RBI reducing rates). Easiest way to track is to look at the latest FD rates(even if you are not tracking any banking stocks).

Hence even at higher borrowing a company might have lower interest expenses. In my limited opinion, please always look at the total borrowing/debt (short term+long term) and not at interest expenses.

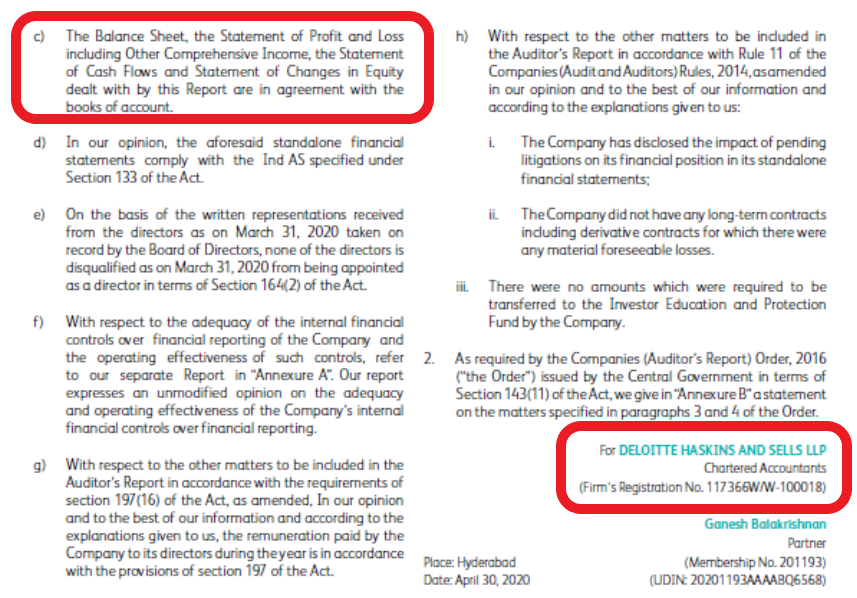

I’ll post what my limited knowledge of balance sheets permits. Others can come up with much more details. There are two red flags mentioned.

Very low cash and cash equivalents on balance sheet.

C&CE (cr)

Mar 17 - 4

Mar 18 - 3

Mar 19 - 3

Mar 20 - 2

Sep 20- 2

vs Sales (cr)

Mar 17 - 1900

Mar 18 - 2050

Mar 19 - 2300

Mar 20 - 2850

Sep 20 - 4200 (annualised)

I don’t really have an answer for this or couldn’t find. Just comparing C&CE for other API companies. We can see that even companies with clean managements like Divi’s and Aarti Drugs have very less cash at end of the year. Laurus is not the only special case. Need to find out more.

The working capital of Laurus Labs(Inventory + Trade Receivables - Trade Payables): Sep 2020: 1250 cr Mar 2020: 1080 cr Mar 2019: 900 cr

Let’s compare gold standard of API Divi’s figures. The number is almost half the sales every year and increasing. So it definitely is nature of API business and not a red flag at all.

Laurus has a long term cash credit limit of 840 crores, and hence can afford to keep low cash levels. Plus all this while, as sales keep increasing, cash flows keep on increasing.

I think this Twitter brigade seem to have started a tirade against the company. I got the same tweet as a forward from different sources and people copy paste it as their own observation.

Case is simple. Believers, stay invested. Those who doubt can get out.

In the recent past too, stock price had corrected from 249 to 210 and 310 to 251 (adjusted for split) which is 15-20% correction from top. It is not unusual for stocks to correct by that range during their upmoves.

Thanks @nikrod12 for some original work on comparing peers.

IMO i understand based on past experiences that few vested people are in mission to create doubts, confusion and misunderstanding in the minds of innocent retail investors so that those who missed the bus make killing. If company fundamentals and business are solid then there is not so much to worry in long term. I can recall how Ajanta pharma was seen from the lense of doubts couple of years ago but see the performance over the decade! It will make many stalwart company liliput when returns are compared.

Happy investing.

VK

Disc - invested in core PF and views biased.

It is amoronic argument that this guy has put forth, and twitter illiterates are retweeting it, he expects a company which has a huge working capital loan to take money out of its cash credit account and put it in a current account, just so it shows up in the cash and cash equivalents at the end of the year.

This conspiracy thing ranks right up with authors like Ludlum, Grisham or Frederick Forsyth. As posters on a public forum we cannot put up gory details of hypothetical frauds without any substantiation and I guess that’s why the post was probably flagged and deleted. But I must confess you take imagination to another level.

This conspiracy thing ranks right up with authors like Ludlum, Grisham or Frederick Forsyth. As posters on a public forum we cannot put up gory details of hypothetical frauds without any substantiation and I guess that’s why the post was probably flagged and deleted. But I must confess you take imagination to another level.