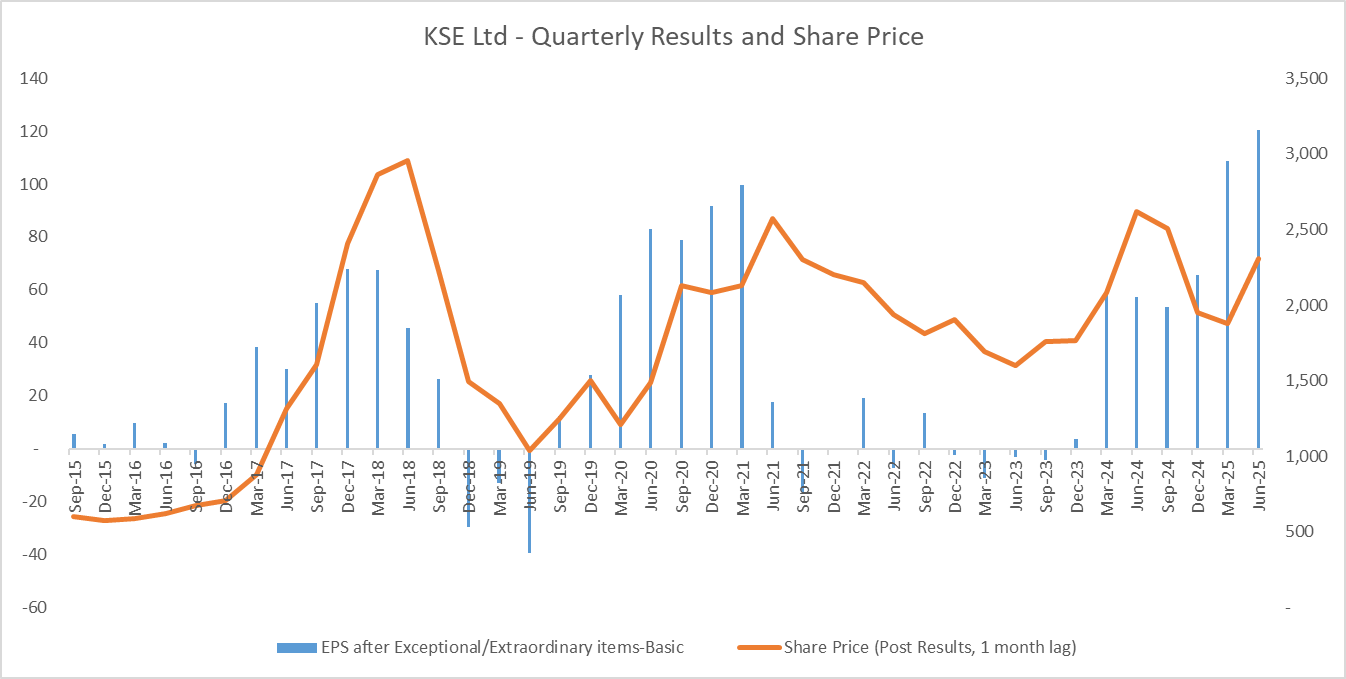

I believe that cycle could still get better. Perceptions decide prices to a large extend. It is true that the company display very large cyclicality. The current volatility in the market could also have resulted in the correction to a certain extend.

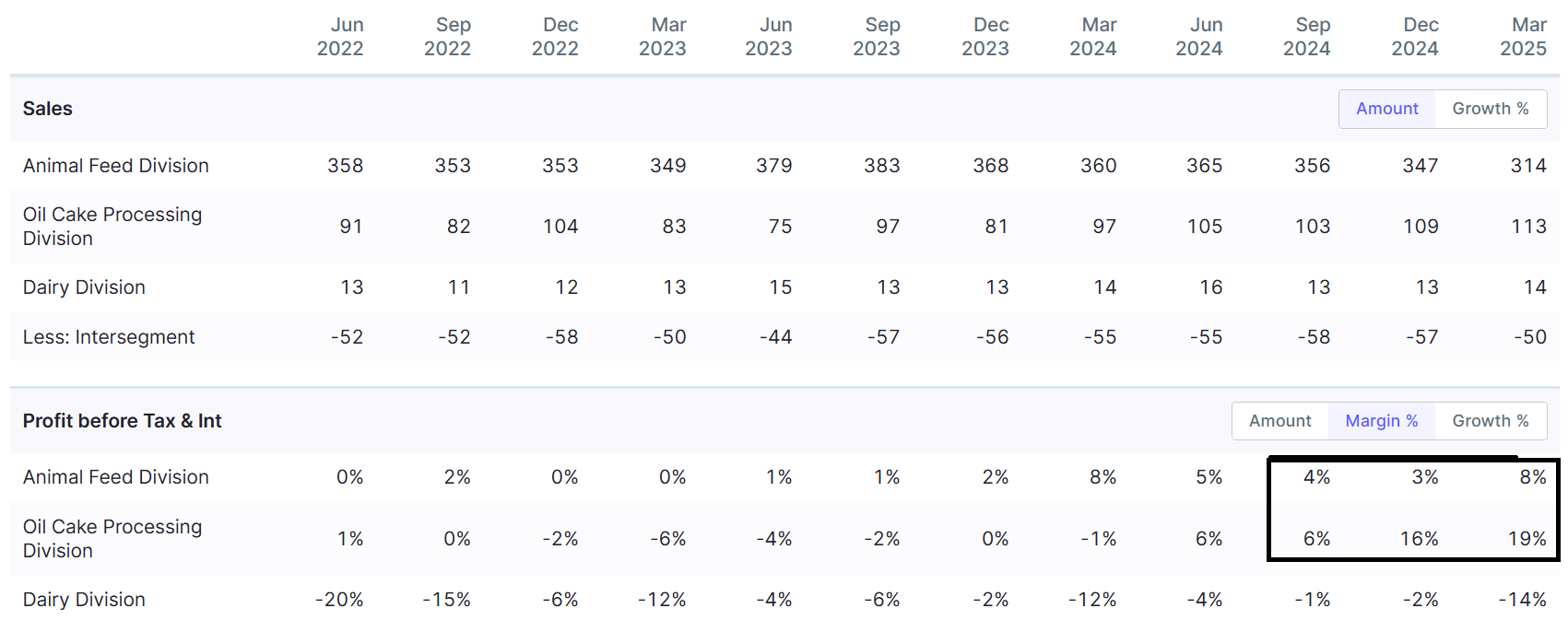

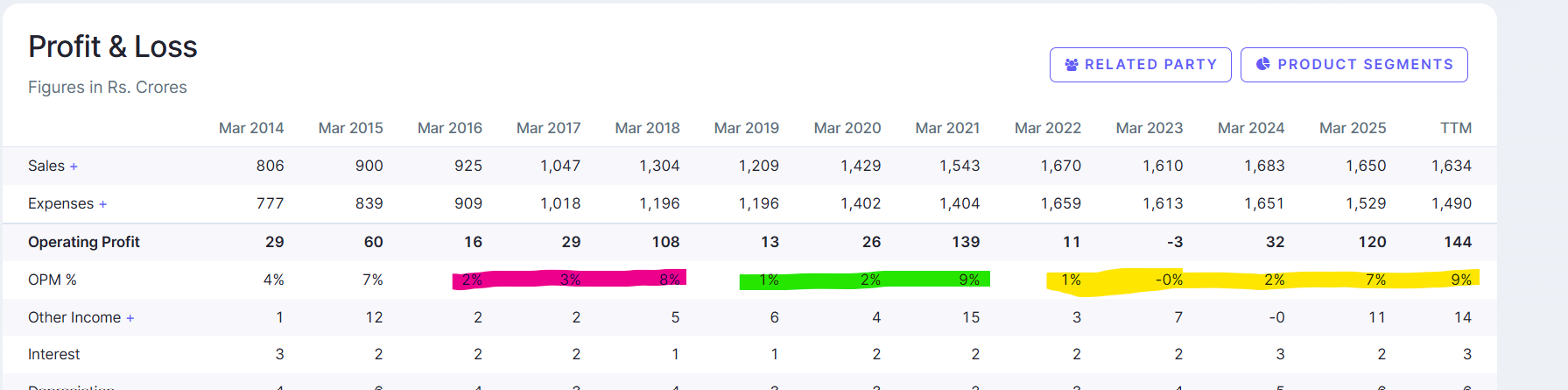

Most of the profits in the last 2 quarters have come from margin expansion from the oil cake processing division. The bulk of the sales however comes from the animal feed segment.

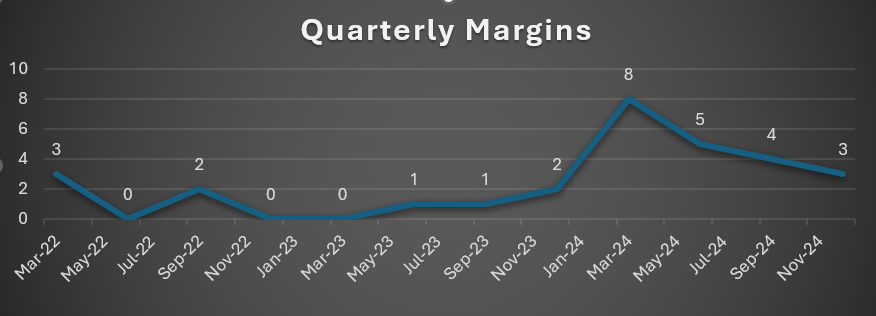

Quarterly margins have fluctuated between 0 and 8 %.

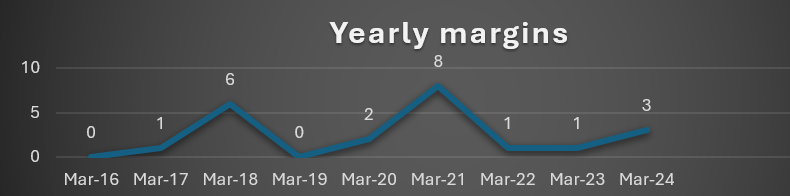

Yearly margins in animal feed have touched 6 and 8 % in the last 2 peaks.

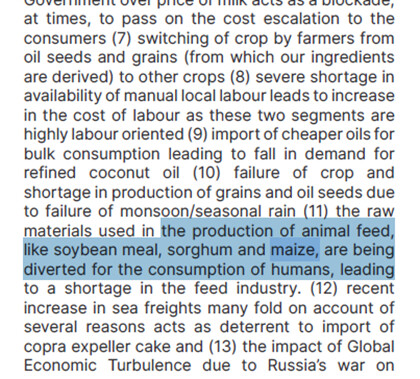

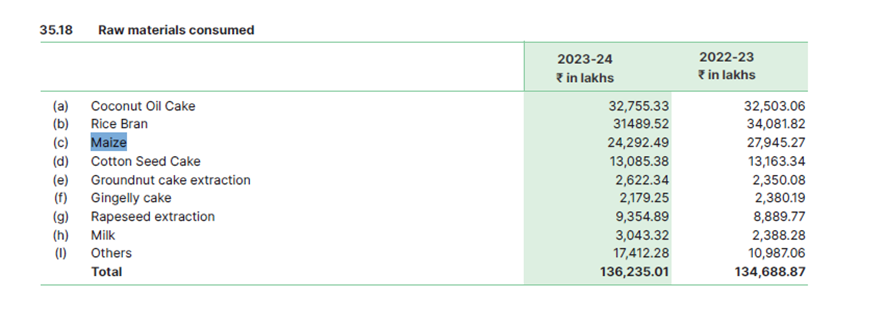

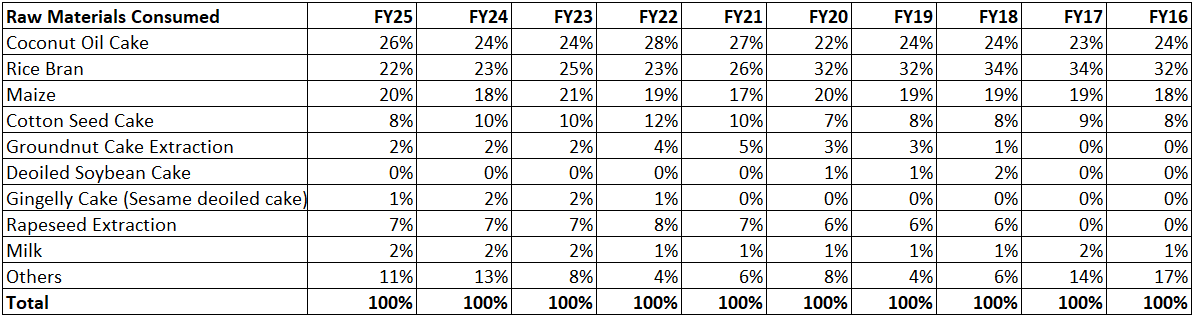

As per the last annual report, there is a shortage of raw materials such as soya meal, sorghum and maize. The major raw materials used in the last year was rice bran, maize and cotton seed cake.

So the prices trajectory of these raw materials may have a significant impact on the animal feed segment margins.

India has a good rice crop and rice prices has started to soften. Ban on export of rice is lifted resulting in increased milling and could result in better availability of bran,

Cotton prices is also down significantly. The major concern to the feed industry has been maize prices. The maize prices have seen some softening in the fourth quarter.

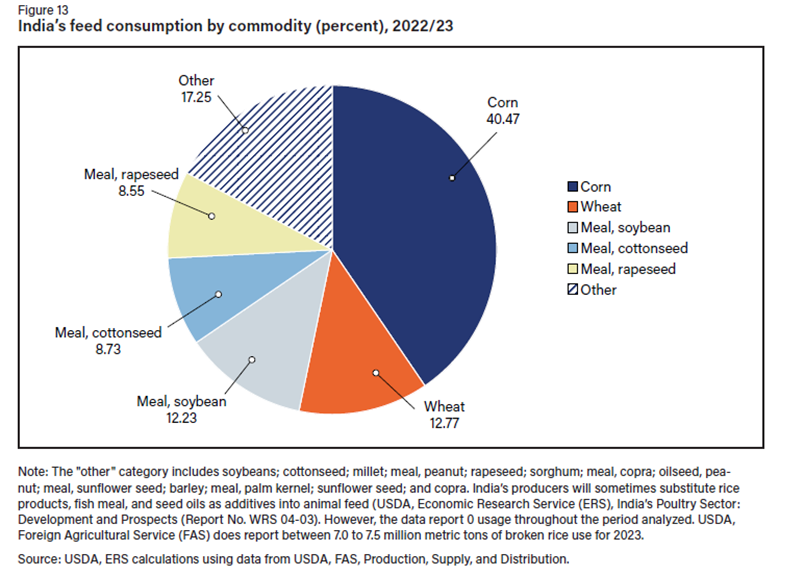

As per a USDA report on animal feeds and products, 40 % of animal feed is corn.

The Indian maize prices doesn’t align with international prices due to the large import duty.

Also, the company’s entry into poultry feed was a good idea as the poultry is one of the fastest growing sectors.

As per the USDA report India has a tariff of 39.2 % on agricultural imports. If the current talks on tariffs and trade lead to a reduction in import duty on corn and soya, this will turn out to be good for the sector. If the company is able to expand to other geographies beyond kerala, that can increase the topline as well.

The ice cream business would be a interesting segment to watch for eventhough its very small and loss making now. It would also be interesting interesting to watch how GT’s consultation could increase margins. The company paid an interim dividend of Rs.35 in the last quarter.

Usually cyclically companies are best bought when P/E is high, at times when their margins are most depressed. The margins could further expand with reduction in grain prices. If anyone is interested, I am uploading USDA’s report on growing demand for Animal products and feeds in India released last month. US may put pressure on India to reduce import duty on agri products like soya, corn and cotton.

Discl: Invested and biased.

ERR-347.pdf (4.5 MB)