It is a Kerala based 50 year old company primarily in Ready Mix Cattle Feed, the usage of in it is bound to increase in the coming days for better milk productivity and cattle health. I have an old report of FAO which is enclosed for an overall understanding of the issues.

I am tracking with small investment in this company for some time, after looking at its tremendous pricing power and very asset light model and a decent Balance sheet. The financials can be available from Screener and, for my own analysis, did a few calculation which is enclosed here. The details and challenges of the company is well documented in the 2014 AR.

@aveekmitra I am just going to play the role of the devil’s advocate here and identify what I see are problems from my very basic run through the business

The competitive nature of this industry makes outsized returns on capital a tough ask.

Government imposes price restrictions on the sale of milk - limiting what the cattle farmer can charge. Thus cattle feed producers cannot pass on any price increase to the end user.

KFL their closest competitor (KSE+KFL control 53% of the market) is a govt. undertaking and thus tends to have an advantage over the private players (distribution/ access/ pricing control).

The farmers themselves rank price, convenience and availability as the top 3 drivers of brand choice ( primary research reports point to this), thus superior quality - which KSE does offer - is not going to drive significant growth at least in the short term.

Coconut, which forms the base of the cattle feed produce is a volatile commodity and in the past KSE has had to resort to importing this from SE Asia due to unavailability in the domestic market. Copra which is the base of their cattle feed is made from coconut - however on the positive side, the coconut milk extracted can off-set the increase in copra prices to a certain extent.

KSE entered the ice-cream business 12 years ago and so far does not have too much to show for it - this doesn’t inspire much confidence for the future - though to be fair the management does appear to be earnest and making steps in the right direction (wrt to branding and capacity expansion) albeit slowly.

KSE seems to be plagued by capacity limitations in its core business. There is a demand supply mis-match and this can run both ways.

As I said, just trying to bring the obvious negatives upfront and ignoring the positives of which they appear to be quite a few as well!

If you can share with us the source from where you got the information that Cattle Feed price ceiling is imposed by government then it would be immensely helpful. Also, if you can share the present GOVERNMENT IMPOSED CEILING PRICE of Ready Mix Cattle Feed (RMCF), that would put things in perspective vis a vis the price of KS Feed as prevalent presently.

If my understanding is correct then price of Milk is fixed by government and this indirectly affects the price of feed. Milk price has been continuously revised upwards in TN and Kerala in last few month. Also, in future, I think most products would have market based pricing …

RM has highest criticality in the story … But the linearity of the issue may or may not be there if a particular Feed Mix find acceptance among breeders … But it needs lot of further probing … Just a pointer…

If you have gone through the excel file attached with my opening thread you would have realized that RM as % of sales is remaining constant for last 6 years. So, any price increase of RM has been passed to consumer.

If KSE can pass on entire price increase for last 6 years: can take advance or buyer’s credit from consumers (as evident every year) and can sell with zero credit (as evident from working capital cycle) and at the same time keep increasing the sales volumes as they have done, how important the competition is in this situation?

Growth would come if milk price is market driven (as it is gradually happening) … Farmers would be focussed on quality over price unless KSE price itself out of the market. From their volume growth, it doesn’t seem to be the case.

RM of KSE… 35% Rice Bran and 25% Coconut Cake. Yes, the possibility of scarcity or unavailability of Coconut Cake may be there in India and it is risk … Unless there is wide disparity in price, it can possibly be passed on but a risk nevertheless.

I am totally discounting Ice Cream adventure … if it happens it would be a bonus. I think it is hard business and KSE doesn’t have any encouraging track record.

Capacity limitation is handled by third party production — Read AR

Milk prices are regulated and with feed their is limited pricing flexibility

this is paragraph from CRISL study

Margins influenced by volatile raw material prices and limited pricing flexibility Raw material prices have been increasing due to stagnating food grain production, use of grains in the manufacture of biodiesel and ethanol, failure of crops, etc. The willingness of key competitors – Kerala Feeds Ltd and Kerala Co-operative Milk Marketing Federation Ltd or Milma (who are not driven by the profit maximisation motive) – to hold cattle feed prices and regulated milk prices restrain KSE from raising realisations to combat the pressure from rise in raw material prices. Hence, margins have been volatile and are expected to remain so.

It is competeting with a non for profit govt organisation with marginal ability to increase prices.

My conclusion from the same set of information is very different

I think these non-profit / cooperative etc can’t build a brand and over the period of time they will gradually be uncompetitive … Their cost structure are generally uneconomical and hence gradually in a free market scenario they will be weakened …

I can always be wrong in my analysis and understanding … And I am holding no candles for KSE but giving my very subjective and fungible opinion

About 12000 shares were reduced by promoters group … But no announcement given in BSE / NSE … I found, NRI and Clearing Member shares were increased proportionally

Also, till previous quarter, there were 143 names in the promoter group. But in this quarter filing, some of them are being showed as having zero shares … Though the number is still 143 (it is quite big list!)

Most probably some of the Promoters ceased to be so and hence there name shifted to other category.

You may write to secretarial department of KSE for more clarity.

I have taken a small position in this stock.Something that was interesting that i understood was they have some kind of a barter system. They exchange the cattle feed for the excess milk that cannot sold by the cattle owners which is a win win situation model. Allso i feel they have a good brand image. Based on talking to some people in Kerala they have a good brand image. I dont agree to the fact cooperative society’s cannot build brand, the good example is AMUL.

That said if it can build more milk based product with greater profitability it can be be multibagger.

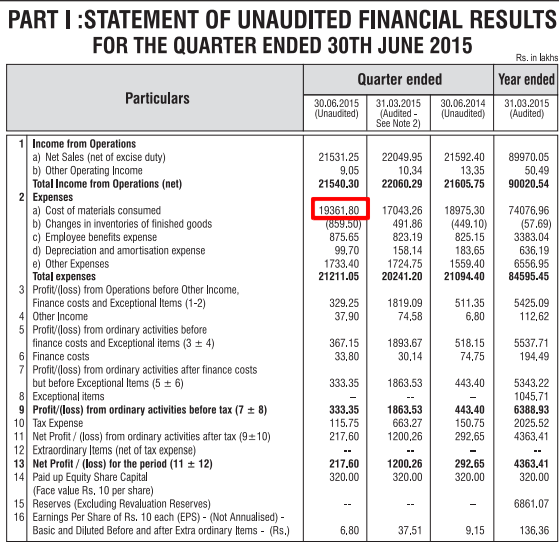

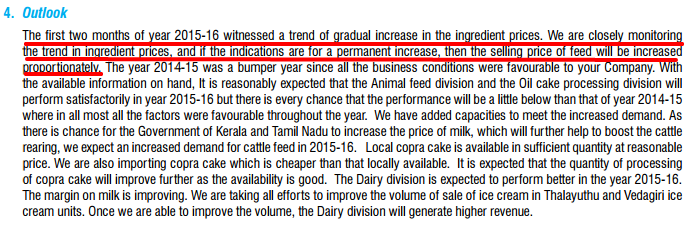

KSE reported a poor set of numbers this quarter, mainly due to increase of raw material prices in its cattle feed division. The company has said, if raw material prices continue to rise, they will increase the price of feed proportionately.

Does it have sufficient pricing power to increase costs with RM price rise?

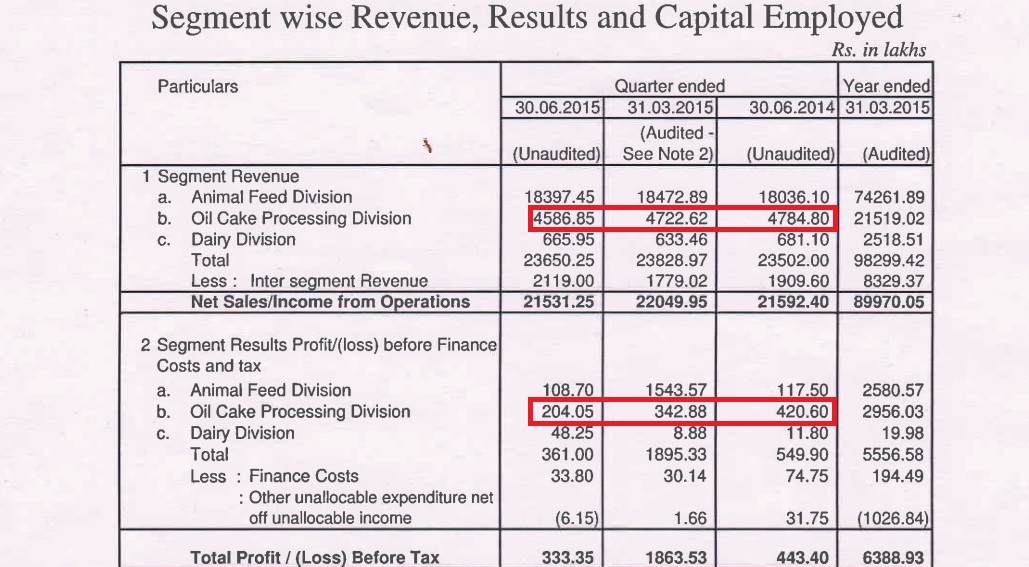

In my view its not the raw materials in the cattle feed that caused the poor result. If you look in to the segment revenues you will find that the oil cake processing margins have halved while that in the animal feed division is flat to just negative. I am finding it hard to understand the oil cake processing margin fall as kopra prices have fallen very much in comparison to coconut oil prices.

TOP LINE and bottom line is increasing consistenly … Scaling up will be difficult … But still i think at least for the next few [ 4 - 5 years ] years the growth will continue …

Sir recently when in Kerala I visited there kanjigode factory extremely good excellent mangement the June qtr result was poor because there was a big ticket new raw material purchase for there new animal feed product and a huge copra purchase at a very lower price the new product for animal feed is already in market and lucky it does not come under the government price control because it is launched a milk enchanter feed and also they have launched exculsiive ice cream outlet in Tamil Nadu also and brand visibility is improving and the ice cream and coconut oil division will give a excellent result this qtr so I think with price bottoming out we can start buying before the result