and Cash tax Paid/Reported PBT -

Variations a plenty ranging from 34% to 6% between 2019 and 2023 - wonder what lends to such volatility

Disc - noticing plenty of amber flags, hope fellow community members can help wrap our heads around this

and Cash tax Paid/Reported PBT -

Variations a plenty ranging from 34% to 6% between 2019 and 2023 - wonder what lends to such volatility

Disc - noticing plenty of amber flags, hope fellow community members can help wrap our heads around this

@dsaraf I have recently studied Krsnaa and would like to add my two cents here. Hope it helps.

1) Promoter dilution: During FY16-19, the company issued CCPS to three investors including Somerset, Kitara and Phi Capital (raised around INR 165 Crs). Last round (Series C) was from Phi Capital Growth Fund I in Dec’18 wherein the company raised INR 100 Crs (reflected in the cash flow statement of FY19). Now, in DRHP shareholding pattern before listing shows that promoter and promoter group held ~69% of shares in the company and rest was held by individuals. The dilution to ~28% happened primarily on account of conversion of CCPS to common equity. DRHP mentions that these CCPS carried a condition of convertibility on IPO.

2) Capital intensity: To participate in big ticket PPP contracts, one needs cash. The company raised INR 165 Crs from the aforementioned PE investors during FY16-19. Roughly this business generates 1 rupee of revenue against 1 rupee of investment (fixed asset + working capital). There is another way of looking at this. A CT scan machine costs ~ INR 2 Crs. If you divide their radiology revenue by no. of CT/MRI centres, it comes close to INR 2 Crs. So the business is inherently capital intensive and the growth during FY17-23 has predominantly come from incremental investment (INR 165 Crs from CCPS and INR 400 Crs from IPO. Noting that half of IPO proceeds were deployed for retirement of long term debt).

If we see unit economics, a CT/MRI centre gets around 20-25 scans a day which is roughly 800-850 scans a month. If we take average realisation of INR 2,000 per scan the same comes to INR 16-17 lakhs a month and roughly INR 1.9 - 2 Cr a year. So, I didn’t find anything unusual about their topline growth. Yes, the pace of growth has been higher but they also deployed higher capital during this period. To my understanding, this business requires continuous capital infusion to grow beyond 9-10%.

3) Management: Overall experience in diagnostics seems low but also noting that PPP and B2C diagnostics are different games. The way I understand it, PPP requires more project execution expertise than building testing capabilities, scaling labs, brand building etc. That’s why their foray into B2C is a good optionality but the journey will be hard for the company to crack the B2C market.

Hi Yash, you seem to have got me on the other side of the fence with your arguement already! Thank you for this detailed response ![]()

Indeed, I am just looking at this story from a different lens now and as you rightly pointed out, this business is all about execution and time management - as Pallavi Jain herself puts it in her talk at a US College

I have been tracking this for a few months now. I got interested in this due to Aditya Khemka sir.

It is a low-margin and high-volume game. That’s it.

I am an ENT surgeon practising in a tier 3 city. And I am sharing my perspective here.

In the case of Pathology, I always wonder how one can do such blood tests, etc, at such a low cost. They are targeting mainly government and municipal hospitals. But how can one maintain Quality with such high volumes?

It is the same with Radiology also. It’s again a number game. Krsnaa charges are nearly 1/3rd of market charges. If you are admitted to the government hospital ( where Krsnna is attached) for one day, the scan is free ( Govt. pays for it). How can you charge so little with such huge capital expenditure on machines? Again, it’s a volume game. So here, one of the significant ways of cost-cutting is reducing the payment per CT to the radiologists. But obviously, senior and experienced radiologists will not do it. The recently passed-out junior radiologists mainly do it.

I have been tracking this from 400 levels. Invested and again sold out with marginal gains.

The above points always confused me.

The other issue is the Promoter’s holding of just 27%. So, other major stakeholders have the upper hand. And they have invested for returns and not for any charity. So, they will push more and more for margin improvements. All this will again question the Quality.

So, to clear this confusion, I asked myself this Question. “Will I ever go to Krsnaa Centre for my own pathology/radiology tests?” And the answer was - HELL NO. ABSOLUTELY NOT.

Since then, I have been only tracking this stock.

The only thing that excites me is their (?) future use of artificial intelligence in radiology.

The use of AI will, of course, improve the Quality with even higher volumes. Again, implementing and maintaining AI may be capital-intensive.

So, I am just tracking this as of now.

All these are my thoughts.

I am not invested in this stock.

dr. vikas

The labs are NABL accredited and i guess the test cant be manipulated or be of inferior quality. Also, you should visit the Kurla or any of its labs near you, it might give you a different perspective.

Thanks for your view @vikasbargale. I am curious on certain aspects.

As per my understanding, the efficiency came by tele reporting that allows full utilisation of radiologist’s time across multiple machines. This means, the cost per CT scan will be lower, but the radiologist will earn more in total due to increased efficiency.

Also, the cost is primarily the machine itself. Krsnaa’s utilisation rate is much higher than other players since they also optimized the process of onboarding patients. I think their utilization is 3 times that of competition.

The business model is with scale, efficiency and reduction in costs. I see this as a speculation on key investor behavior. However, I do agree that we should monitor company’s execution record. Even if they don’t run it as a charity, they still might have an edge as long as they can manage to scale reasonably.

This is very interesting. Do we have any evidence that Krsnaa’s results are inferior to competitors? I see an assumption that their pricing comes at cost of quality. But wouldn’t efficiency also bring down price?

If I am going for any CT scan or pathology tests, I will try to use Krsnaa and other competition to see how results turn up. If anyone here has done it, would love to hear from them.

Once again, thanks for your views @vikasbargale. It is a good counter view for an overall bullish sentiment on this stock. We need more of this.

Disc: invested

Have used Krsnaa services for Pathology and Xray scans and they have been accurate, my doctor dint have a problem with the results.

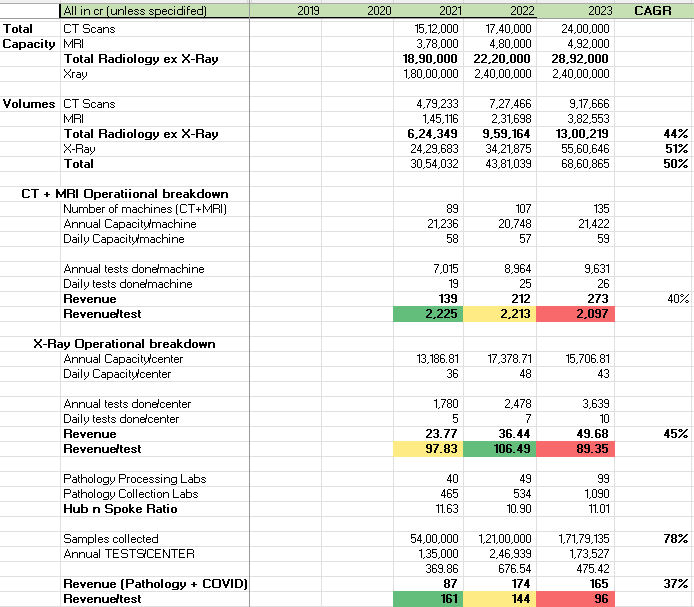

tried going into the nuts and bolts behind the machine, and here is a small snip of that. What i notice is that the realization / test, especially for Pathology (this is ex COVID), has been under some pressure - what does this point toward?

Heartning to also see radiology realizations stable as this segment is where Krsnaa differentiates itself from others

I am a doctor working in govt hospital.Reagrding the quality of CT scansn and MRI s of KRSNNA I can surely tell that it’s much better than some of the other pvt set up centre s…and my specialist s friends in private sometimes refer their cases to KRSNNA for better quality scans…

Not invested.but following

Hi Dhruv,

Had looked into this as well. In one of the con calls, management mentions that when contracts do come for renewal, government can ask for lower pricing given negligible requirement for additional reinvestment. For example, in Assam teleradiology, Krsnaa quoted lower prices with the rationale that initial investment was already recovered. Not only renewals, this can happen for initial period as well. Take Punjab for example. The payment cycle for this radiology contract is 15 days (essentially cash). In exchange for this, government can ask Krsnaa to lower their pricing. That’s the reason for drop in radiology realizations in FY23.

For pathology, this risk is even higher. Pathology contracts are of shorter duration. Generally three years and then they might extend it for another two years or so. In addition, the competition in pathology also tends to be high. I suspect that this situation can force Krsnaa to quote lower pricing for new contracts or during renewals.

The company often highlights 3-5% price escalation in the existing contracts. While that may protect the realisations during the tenure of contracts, things can change on renewals. That’s just one of the difficulties in dealing with the governments.

@yashrachh could you help me also understand this expense that Krsnaa shares with hospitals? Is it basis/test or is it as a fixed fee or a fixed %age of revenue?

Also, if you compare the number of CT/MRI machines owned and the number of CT/MRI Centers operated theyre the same. Hence, Teleradiology to my interpretation is essentially XRay machines installed at Primary/Community health centers wherein these scans are sent to the hub in Pune. Also, teleradiology realizations of 90-100/test point toward that. And something I believe, will not be the needle changer in this story

Good point on the teleradiology. Yes, it’s essentially x-ray (they mentioned x-ray against teleradiology in DRHP and later changed to ‘teleradiology’ in presentations but it remains the same). Agree on the view that this will not move the needle for them. They recently aligned the reporting so now the CT/MRI centers and no. of machines are the same. It’s good that they made it easy to understand now.

On the sharing with hospitals, I think it’s basis revenue (they have mentioned in one of the presentations). Their pricing for private hospitals also go up by 20-30% to cover this revenue sharing.

Yash bhai, there is an expense line item of ‘payment made to hospitals’ if you see - which has been in the range of 80-100 crore over the past 4 years. What would this be for?

Yes, it includes two things. 1) the revenue sharing with these hospitals 2) they work with the local partners in remote areas on revenue sharing model. Management had clarified this in one of the calls. I suspect that out of INR 80-100 crore, second portion (revenue sharing with partners) would be more than revenue sharing with hospitals.

On this accounting policy, i think it’s standard across diagnostics companies. Even for franchisees, they recognise the revenue on gross basis and record the revenue shared with them as ‘Fees to channel partners’ or something like that. Krsnaa also has similar revenue recognition policy for hospitals and business partners channel.

Hello All. Sharing my condensed investment thesis & notes on Krsnaa. Most are based on discussions in this thread. Thanks to all contributors.

Business Model Strength / Moat - 7/10

Seems to have cracked the formula for efficiency, thus becoming the lowest provider of services. They have focussed on digitisation and automation from the start. For example, they use SigTuple for automated microscopy process that can also be done remotely.

This moat is hard to replicate as it is a organisational setup.

There is still some uncertainty due to the B2G aspect. However, the company seems to have managed it well.

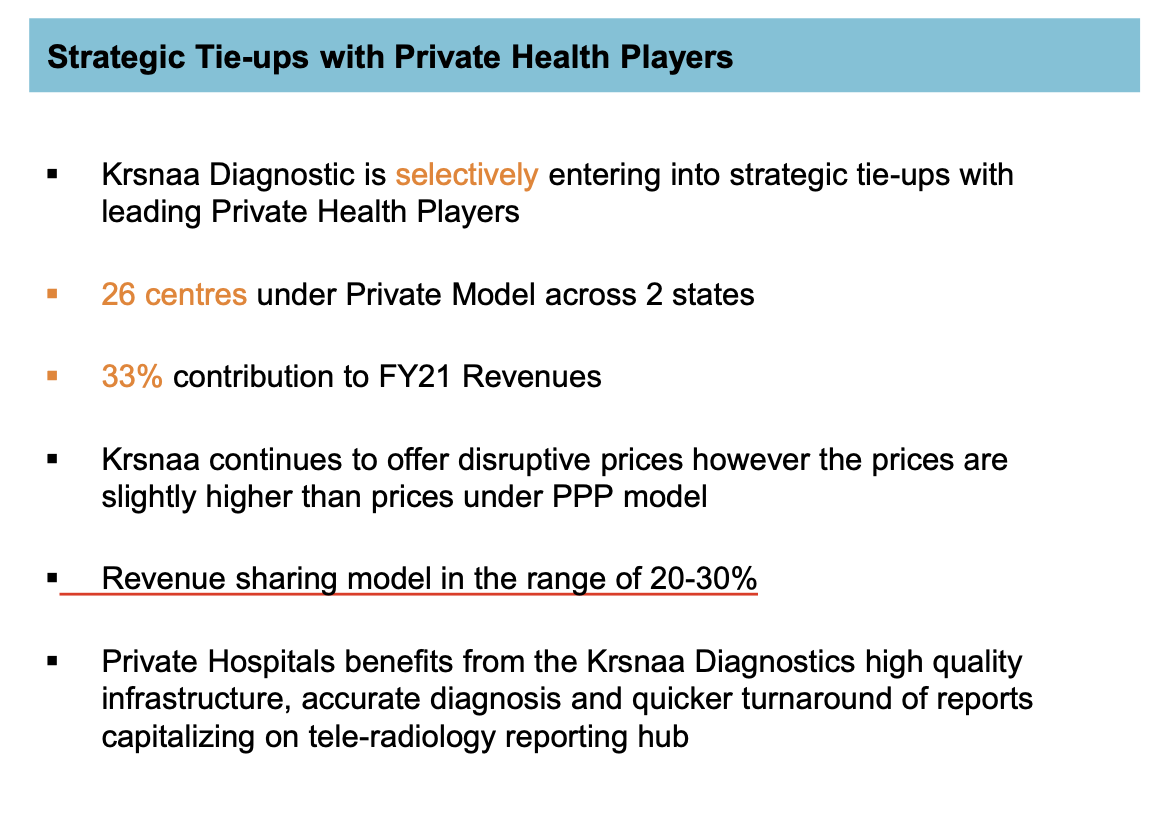

They are tying up with private health players on a revenue sharing basis. Not much info is available other than Q3FY22 presentation.

Their centers are also NABL accredited which makes sure that the quality is not compromised.

So far, the scuttlebutt by some fellow investors point that Krsnaa’s services are good and might even be better than smaller service providers.

Profit & Margin Sustainability - 5/10

The margins are a bit low as many new centers are being established. They have been falling continuously for a few quarters. This is expected to improve as they become live in FY24. Further, economy of scale is expected to lift the margins.

Pathology division is being scaled up more rapidly. Though the margins are lower in pathology compared to radiology, the capex requirement is lower and hence the ROCE is expected to improve.

Recently CGHS rates have been increased. This would result in hikes in Krsnaa’s diagnostic prices, which is expected to improve the margins going forward.

Since this is a high volume & low margin business model, there is a bit of risk when the operating cost & expense increases.

Competitiveness - 8/10

They have almost no competition in the B2G space. Even in private hospitals, they might be able to replicate the same model and be the cheapest. With their pricing significantly lower, there is no strong competition yet.

Another aspect is that they are present in Tier 2 and Tier 3 cities where the population is very cost sensitive (no problem for B2G). There is only smaller players in those areas and they have a big room to grow.

Management Capability - 8/10

The story of how Krsnaa started is quite heart warming. It is good to know that these promoters are still at the helm of the company and are intending to build the business as they had done so far.

They intend to focus on reducing the cost for the end consumers and figure out how to make the business model work. This focus on customers would definitely ensure a longer leg of growth as well as being competitive as they scale out. They also have managed B2G contracts quite well. In the context of India this is something that is commentable and can’t happen without a very good management team at the helm.

The management has been quite transparent with shareholders and seem to be humble. The interview of Pallavi Jain is a very good one to watch and understand the thought process of promoters.

Governance & Promoter Integrity - 8/10

Even though they are in B2G business we do not hear any issues regarding governance or promoter integrity. There are some related party transactions regarding the rent paid for the office. This doesn’t stand out too much as of now. However, we will need to monitor related party transactions a little closely. There are already some discussions on this topic.

There is always some governance or political risk when dealing with numerous government contracts. So, this needs to be continuously monitored.

Financial Health & Asset Quality - 6/10

They have used the IPO proceeds to pay off the debt and now have no debt in their balance sheet.

It will be interesting to see how they are funding their expansion going forward.

Since they are asset heavy, it is important to track the health of their assets. The outcome of this would typically reflect as increased depreciation and a pressure on ROCE.

Macro & Sectorial trends - 9/10

Indian market is severely under serviced when it comes to healthcare facilities. With the government pushing through many initiatives we can see a good level of tailwind in B2G segment.

India stands to benefit from increased purchasing power and growing middle income category thereby providing more room for premiumisation of services.

With increased penetration of insurance schemes we can also expect high volume and high margin services coming up in healthcare sector.

There will be migration from unorganized / small players to organized players as healthcare ecosystem matures over the next decade.

Recent advancements on AI tech would favor large organized players who are geared to leverage these automations at scale.

Growth prospects - 8/10

The company is poised to grow at more than 20% CAGR over the next few years. This is dependent on growth of B2G segment, expansion into pathology and scaling out their private service offering. So far that doesn’t need seem to be any blocker other than capital requirements in growing their revenue. We will need to keep track of their contract wins and expiries over the next few years.

From LinkedIn insights, the last 12 month employee growth is at 28% which supports the growth story.

Also need to watch how the capital is deployed and utilized for growth without having a significant impact on cash flow & balance sheet.

Stock valuation - 5/10

At current PE of 40 and a potential growth rate of 25%, the stock seems to be fairly valued.

In terms of risk, it is a bit on the high side given that they haven’t yet shown the turnaround in terms of margins. In case the margins keep falling, the cashflow will severely be affected and the company would stagnate quickly with depreciation cost eating up all of the profits.

The risk reward ratio is decent, but not very comfortable at the moment.

Some of the hypothesis / follow-ups:

Disc: Invested from lower levels

Today’s news in Himachal:

Krsnaa has closed around 650 labs in Himachal as the government has not paid an amount of 50 crore to Krsnaa under national health mission.

Due to this Krsnaa has not been able to pay salary to its employees working with them.

Disc: Invested

Source: Punjab Kesari

Hi, it seems the company has finally announced the receipt of order for the first one you mentioned - do you happen to have the Tender Document?