Operating margins are understood. My point were gross margins. May be product mix playing here.

1 Like

Does anyone have an idea why the number of Tele-reporting centers reduced from 1528 in Q4FY23 to 1372 in Q1FY24?

I guess I got the answer. The Odisha tele-reporting contract expired and the tele-reporting centres are now 0 from 156 before. This equates to the reduction in tele-reporting centres.

I have got a few more questions though -

- When was the Maharashtra Radiology Contract awarded? It started appearing from Q1FY2023 Earnings Presentation. I could NOT find any announcements?

- When was the Rajasthan Radiology Contract awarded? It started appearing from Q1FY2023 Earnings Presentation. I could NOT find any announcements?

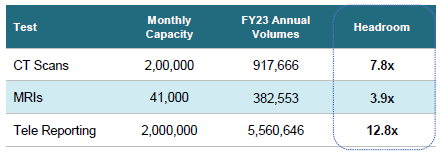

- The Headroom capacity table in Slide 14 of Q1FY2024 Earnings Presentation does NOT make any sense.

CT Scans = (12 * 200,000)/917,666 = 2.62

MRIs = (12 * 41,000)/383553 = 1.29

Tele Reporting = (12 * 2,000,000)/5,550,646 = 4.32

- What are the Tenures for the Assam and Rajasthan Pathology Contracts?

4 Likes

Pipeline update:

There are a few large tenders being floated by governments:

-

A tender for 17 CT centres + 17 MRI centres in Maharashtra that could generate around 75 Cr. of revenue.

-

A large tender encompassing CT, MRI, pathology, ultrasound and x-ray for a few large districts in Andhra Pradesh. Could be worth over 100-150 Cr. once the government discloses more data.

-

Several smaller radiology tenders that could sum up to around 50 Cr.

The first two have closed and are going through the technical rounds. The Andhra Pradesh is an extremely important tender to me. When I last met Krsnaa’s management, they explained how AP is one of the states that is yet to outsource a major portion of their healthcare under PPP. This could be the start of a series of tenders floated by the government. Furthermore, the winner of this tender would be placed in districts that compete with Vijaya Diagnostics.

27 Likes

Where could we get this information? Is it part of the company’s website or part of any recent concall, presentation or AGM

Why is Krsnaa traiding at such low premium compared to peers which is at 55, 60 PE?

Hi

@SKMohite Karsnaa operates largely on B2G model while others have largely B2C model hence better margins & cash flows.

e.g. Cash conversion cycle of Krsnaa is ~60 days while that of Dr Lal Path Labs is -87 days.

5 Likes

Tata small cap fund acquired more shares. Holding is now at 6.6%.

ICICI smallcap fund is also adding slowly as is now at 5.4%.

3 Likes

JM Financial gave a target of Rs. 1050.

https://vid.investmentguruindia.com/report/2023/September/KRSNAA_Update_1Sep23.pdf

2 Likes

Q2 FY 24 :97 Receivable Days H1FY24 (H1FY23: 87 days)

Key Highlights of Q2 FY 24:

1.anagreement for the Assam Pathology tender, a significant opportunity that

encompasses 10 Labs and 1,256 collection centers. This development

significantly enhances our presence, covering all districts of Assam.

- Mumbai Facility: 15000 Sq Ft area in Kurla, current capacity 40000 tests per day, 6000 patients per day which is scalable upto 100000 tests per day, 15000 patients per day.

on Margin subdued on current quarter

Management reply: "It is important to acknowledge our profitability margins,

were impacted in comparison to the previous quarter. This impact can be attributed to the additional costs incurred for the on boarding of teams and operation and management of our newly established centers. We anticipate a positive trajectory in margins as these centers mature over the upcoming quarters.

4 Likes

For last three quarters there has been only 1 center addition in CT+MRI from 133 to 134.

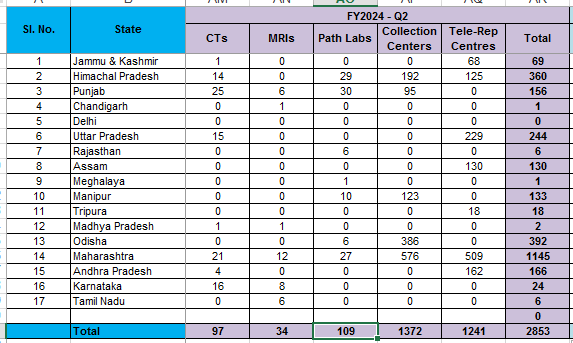

I see a discrepancy between Slide 5 and Slide 21. As per the Slide 21 there are currently 131 CT/MRI Centres, 109 Pathlabs, 1372 Collection Centres and 1241 Tele-Reporting Centres in operation. These numbers do NOT align. Will you please also check if I am doing any mistake.

Company does add lot of data for year ended FY23 as you can see even assets/lab classification (mature to new)- they update every year and not every 3 months. sometime they also move CT/MRI to tele reporting center category so difference could be due to that. Thanks!

1 Like

3 Likes

Some Q2 highlights

- Margins: The company expects to sustain EBITDA margins between 26% to 28%, with aspirations to improve them. It was noted that margins might vary in quarters where expenses are frontloaded due to new tender wins, as initial expenses (like setting up equipment and infrastructure) do not immediately correspond with revenue. However, as volumes increase, revenue and margin are expected to improve.

- Rajasthan Tender: The revenue potential from the Rajasthan contract was revised from Rs. 150 crores to Rs. 300 crores due to the addition of 17 more districts. However, delays have pushed expected revenues from this project into the next fiscal year. Despite this, the company remains confident about its growth momentum and expects other projects to compensate for the delay in the Rajasthan revenue contribution.

- Revenue Guidance: The company is aiming for a 30% Compound Annual Growth Rate (CAGR), excluding the impact of the Rajasthan project. This growth is expected to be driven by various projects across different states. For example, projects in Assam, Odisha, Punjab, Himachal, and Maharashtra are anticipated to bridge the gap left by the delayed Rajasthan project. The company also expects significant revenue growth from new tenders in the next fiscal year, projecting about Rs. 140 crores of additional top-line revenue, potentially rising to almost Rs. 200 crores as the centers mature.

- Project Implementation and Impact on Margins: The implementation of projects like Assam labs and others may impact margins in the short term due to high initial expenses. However, from the fourth quarter onwards, these projects are expected to contribute positively to revenue and margins. The company is actively engaged in various Public-Private Partnership (PPP) projects to bolster its presence and growth. It also focuses on the B2C segment with cost-effective wellness packages to cater to diverse customer needs.

- Investments and Expenses Related to Rajasthan: The company has not made significant capital investments in the Rajasthan project. Operational expenses and basic setup work have been expensed out, with no major investments recorded on the balance sheet for this project.

- Other Operational Highlights: The Punjab tender is on track, with revenues ramping up and operational challenges resolved. The business in Punjab is primarily cash-based, different from other PPP projects. The introduction of home collection services in Punjab is expected to further increase revenues.

- Current Projects and Future Plans: The company is working on installing 39 CT-scan units across Maharashtra, with revenue projections expected in Fiscal 2025. Additionally, their project in Odisha has commenced operations and is poised for substantial revenue growth from the fourth quarter of Fiscal 2024.

- Private Hospital Partnerships: The company’s relationships with private hospitals and Krsnaa business associates are increasing. The contracts with private hospitals are typically long-term, similar to PPP (Public-Private Partnership) projects. The key difference is that in private hospital partnerships, Krsnaa Diagnostics pays a revenue share to the hospitals for operating out of their premises. The prices in these partnerships may be slightly higher than PPP projects to accommodate the revenue share paid to private hospitals.

- BMC Contract: Krsnaa Diagnostics has rapidly expanded under its BMC contract, operationalizing around 462 centers. The volumes they expected to complete in four years were achieved in just 6 to 9 months. The company is also expanding its Mumbai lab, and they anticipate increased revenues over time.

- Home Collection Services: BMC has mandated Krsnaa Diagnostics to start home collection services across the Mumbai region. This service allows them to charge an additional convenience fee for collecting samples from homes or other locations. The monthly revenue run-rate from these services, initially in the range of Rs. 2 crores to Rs. 2.5 crores, is expected to increase to Rs. 4 crores to Rs. 5 crores.

9 Likes

Interacted with an employee at Dharamsala Zonal Hosp…

customer engagement per day has doubled over one year

Avg billing is INR 2000 per customer

The setup looked professional…

4 Likes

- Krsnaa’s foray into B2C underway in Maharashtra, Punjab and Rajasthan

Pathology Collection Centre in Jaipur

Pathology Collection centre in Nashik

Interestingly Krsnaa’s partner in Nashik Suryaj Pathology Labs has been a Dr Lal Path Lab franchisee/collection centre in other locations.

Lots of sales people being recruited, presumably these are for the B2C initiative

Large state of the art lab in Mumbai

If anyone is in Nashik/Pune, it would be useful to get a comparison of Krsnaa rates vs other private diagnostic chains.

-

Lots of hiring, +15% in the last 6 months

-

Interview mentions they have setup a centre in Maldives and bidding for one in Ethopia

8 Likes

I have recently started studying this co and there a re a few things I could not wrap my head around -

- How much did the Promoter dilute to PE in 2015 that his stake came down to 31% Pre IPO?? Seems a little off to me given that Vijaya for instance, diluted to Kedaara and yet promoters held 54% post listing

- Co began in 2011, raised PE money in 2015 - which means within 4 years of beginning operations, they were technically qualified to bid for large B2G Contracts (these often come with a minimal technical qualification rule)

- co was doing 40-50 crore of rev till 2017, what exactly happened between 2017 and 2019 that revenues tripled, co filed IPO Papers all in the same period ? (this should be the quickest that a startup has began operations and filed for IPO - 8 years)

- ZERO management bandwidth when it comes to this space. Apart from the COO who is ex Metropolis, I dont see any top management guy who has any experience in the healthcare space. Infact, Yash Mutha has spent 15+ years working at CS backend + top 4 accounting firms. Wonder what experience does that lend to in managing such a complex, government oriented biz

4 Likes