I’m not interested in Metropolis or Dr. Lal, and I don’t think Krsnaa is comparable as it has a completely different target market, and diagnostics mix.

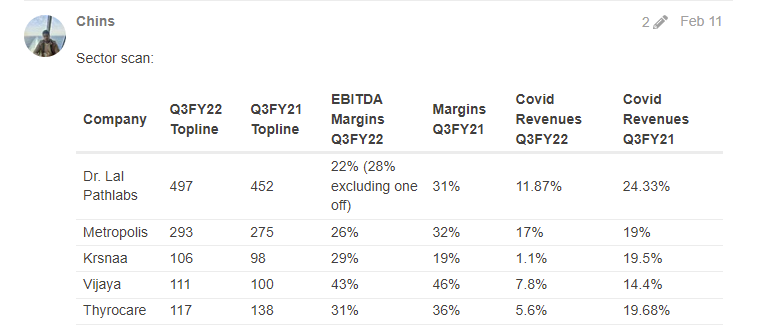

This post examined the exposure different companies had to covid allied diagnostics in Q3, and the sharp correction in diagnostics is due to the realisations of covid related tests falling off a cliff.

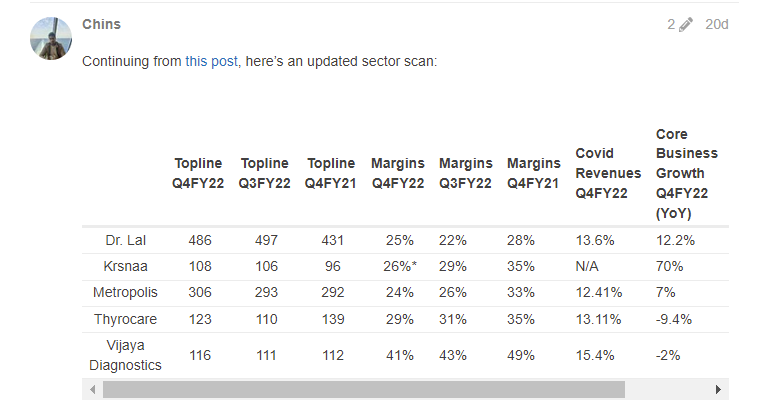

The argument from four months ago was that precisely the two companies you named have the most to lose going forward. Flash forward to Q4’s results, and this thesis played out:

I hope the core business growth in Q4 stands out, along with the exposure to covid revenues these players still have. A part of our thesis for Krsnaa is that we’re already at steady state margins without one-offs. (Except OpEx related items that will lead to a difference in standalone and consolidated margins.)

Something I think is Twitter narrative at the moment (or that current analysis excludes Krsnaa). Krsnaa prices its tests lower than Tata 1mg and puts out 28% (adjusted) margins. If this is a surprise, please see this post, where I’ve covered this in detail, and also addressed how price may not be the sole determinant for success for any new entrant.

Yes, but there’s a significant difference in valuations between all of these players and Krsnaa. More than growth, I think the risk Krsnaa has is a perception risk, where investors may never think a B2G facing company is attractive enough to deserve higher multiples. It’s still early days for the model; for Krsnaa to prove it can get its receivables; and ultimately when PPP tenders are renegotiated / extended; and its B2C rollout.

Please see Hitesh sir’s response on his thread on this point, and on how it may take time for the sector to regain the market’s fancy.

If you’d like even more detailed thoughts on Krsnaa, please see the thread where there has been wonderful collaborative work done on the company in the last six months: