Have been studying the co all day. Also talked to a few seasoned investors to understand why they have it a miss.

The thesis pointers are clearly standing out: differentiated lowest cost business model .perhaps one of only few instances where a private party might have leverage or position to negotiate with governments since healthcare is something which impacts populace directly (as against infra or defense). This reflects in their relatively strong working capital position currently. This lowest cost is aided by unique business model where owner of the healthcare center provides rent free space, electricity, electrical equipment like step down transformers, water etc. Captive patient supply is maintained & co does not need to spend on marketing. In addition their scale enables them to do bulk purchases which also enables them to get good costing on the MRI/ct machines. All of these enable a cost which is 20-30% lower than CGHS rates at least. This is a win-win-win.

Government gets to save on capex & opex & deliver quality healthcare to people.

People get good quality healthcare at affordable rates.

Company gets to make decent margins.

I was actually surprised to see working capital cycle being quite mean. For around a 400cr runrate their wc is hardly 30cr…this is quite low. The receivables are almost completely offset by payables which makes the wc lean.

Actually I did my own roce computation and it seems to be around 30%.

300 cr fixed asset. 30cr wc. Around 25cr ebit per quarter. This works out to around 30% roce. Am I missing something? We have to take the normalised interest cost since lot of interest in older Q was due to debt which has been repaid.

A couple of other things which I could understand which are very interesting… The radiologist are employed on a variable pay wherein they get paid per test analyzed. That is amazing because it does 2 important things :

- Incentivises radiologist to analyse more tests. Aligns them to companies growth.

- Converts a fixed cost into a variable cost so that any disruption does not lead to large depression of margins. In a way the doctor is a DAAS : Doctor as a service. Pay as you go model. That is nice.

- Their Pune tele radiology hub enables their radiologist to monitor & diagnose many many cases which enables them to improve their precision. 190 radiologists all learn from the cases which are complex & enables company’s quality to go up significantly. Lot of focus on machine learning these days. Human learning is actually the bottleneck in radiology. And krsnaa seems to be solving for it. Will be interesting to read the technical papers they have published just to see what their key learnings have been.

Let’s also look at the anti-thesis pointers which imo are keeping valuation depressed.

- Government is perceived to be a fickle player. Just because no problems have come in last X years does not make the business model robust against failures. The perception of government being fickle in payments sticks. & For good reasons. In a b2c like Dr lal your customer is a retail person who does not have option to pay or not. In some of krsnaa contracts the customer is govt which might wake up one day to decide previous govt contracts were too liberal & need to be revised downwards. If we see a latest example of meituan in china & take rate capping by Chinese government we can immediately see some evidence for government across the world not being behind in taking a bad idea to it’s logical conclusion. That risk will remain imo. The absence of evidence is not the evidence of absence.

- Scuttlebutt talking to doctors tells me today it’s very easy to set up diagnostics centers. Anyone with 2cr rupees can set up a lab. Barrier to entry is low. Dr lals return ratios & valuations are seen. Competitive intensity needs to be monitored like a hawk as stated by someone else in the thread.

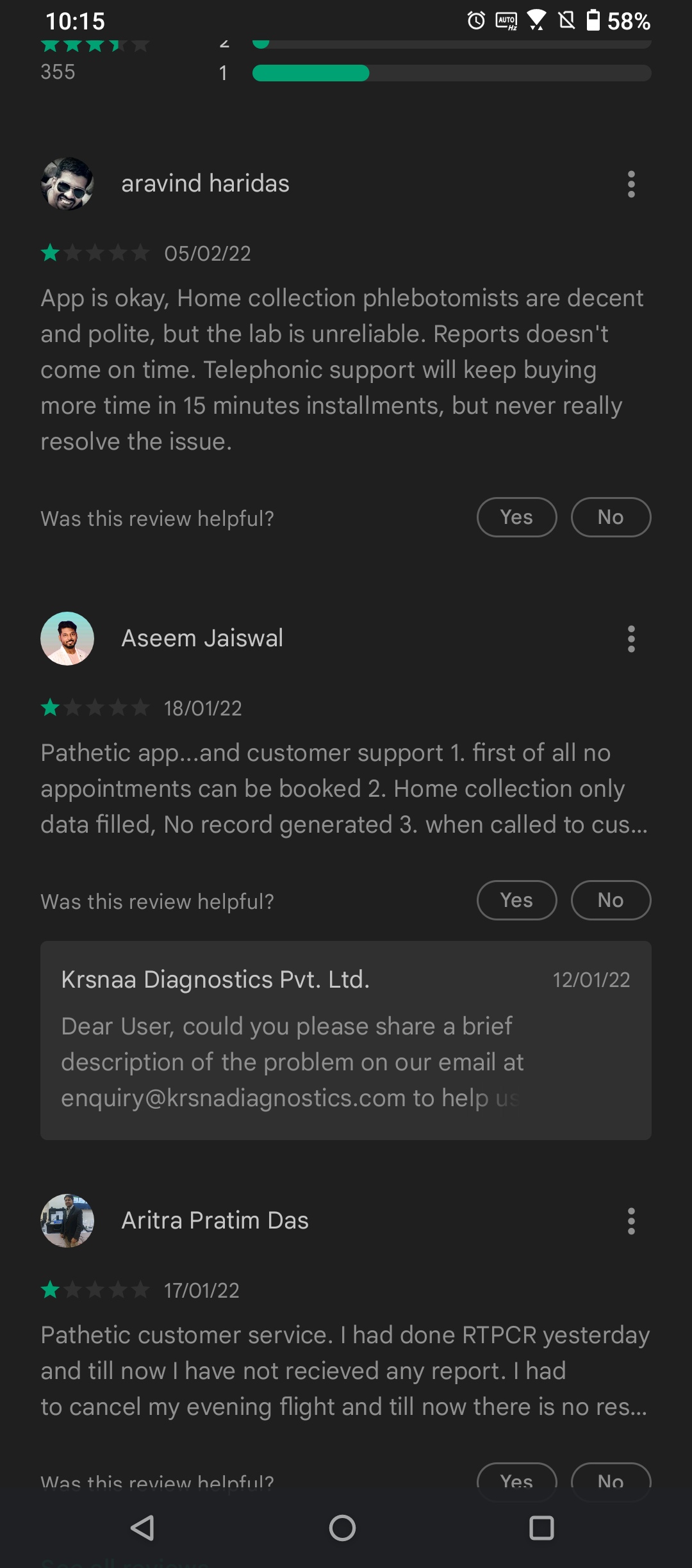

- Look at krsnaa diagnostics rating on Google Play. You will find many reviews which talk about their horrendous experiences. Attaching a few.

The backbone of a b2c brand is good customer service. In the absence of that, you are simply waiting for someone to come & offer a better service than you do & poach your customer. They don’t have that yet, as far as my digital scuttlebutt tells me. Dr lal is way ahead. Hope that are learning from their experience & understanding what it takes to crack b2c. The biggest trick of b2c is building reliable processes which ensure low Variance of outcomes. Customers want reliability. Trust. If i do my rtpcr yesterday I want my results today.

4. Some of the payables could be channel financing for vendors in which case the roce could be lower. Need to dig a little deeper to understand this better & get an accurate picture.

All in all looks like an interesting co worth studying deeply & understand the picture more clearly.

Disc : own a small quantity bought today for tracking & to ensure I have skin in game while I research.