So I just did a quick research, Q1 is the summer season. Hence according to Google, almost half of the field crop seeds portfolio that Kaveri has is not suitable to grow in summers in India, hence summers may be more export-dependent. However, their vegetable portfolio has covered all major vegetables that grow in summer in India. This may be one reason for such skewed numbers.

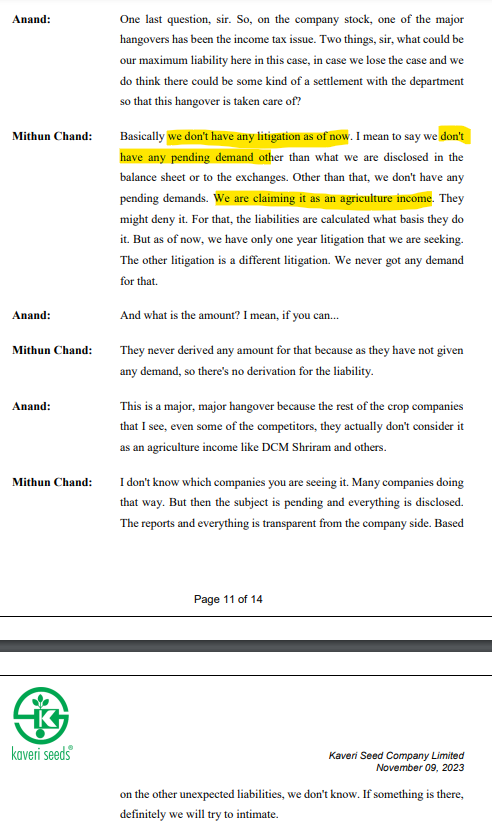

My concern with Kaveri Seeds is related to the Income Tax. Here is a notice they received on 30 September 2022. If the Income Tax liability is applied for previous years then the market value will be affected materially. If the income tax is applied prospectively, then the profitability takes a hit but will still be manageable. Doesn’t anyone have any insight into this aspect of the business model where currently it’s working in the income tax free space but maybe not for long?

The key question is - Will they be able to increase prices in the future if tax is levied considering it as non-agri income. As it will be applicable to all players there will definitely be some price increase to farmers to protect the margins to some, if not the full extent.

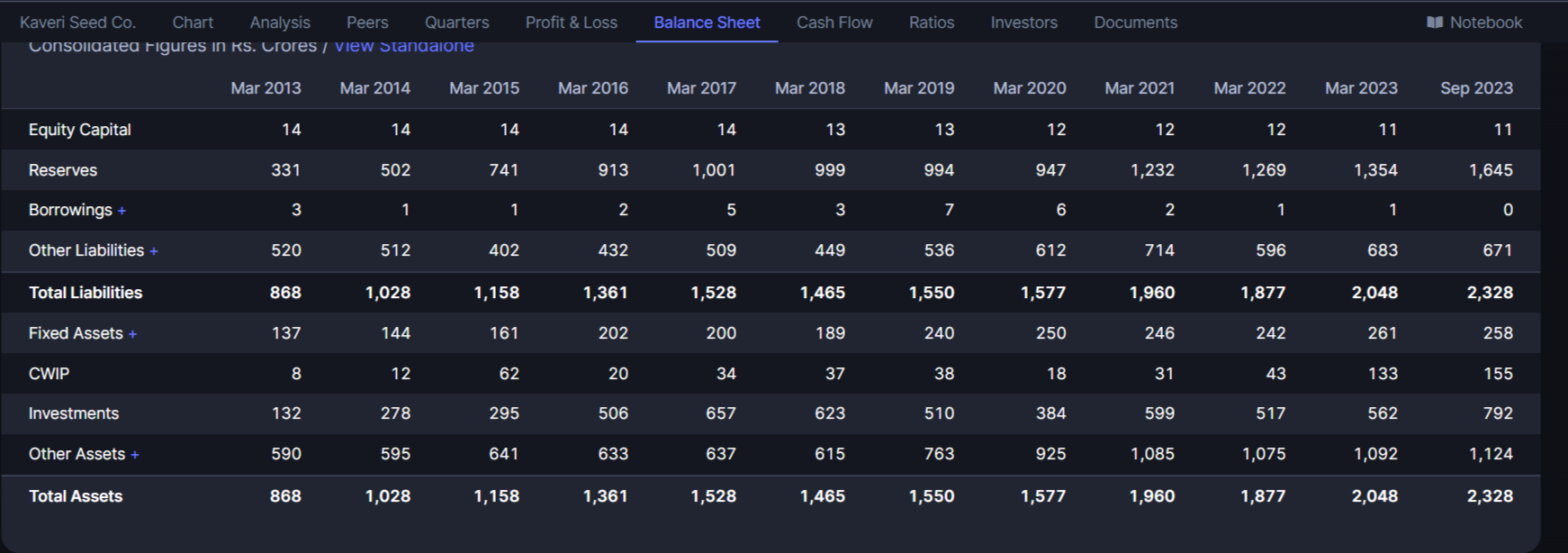

I was having a look at this company on screener can anyone help me understand why is the inventory day shown so high in screener whereas it is roughly only 250 days ! turnover of approx 1050 cr and inventory of 745 cr avg , how can the inventory days be 517 days ! if anyone can help it will be great

Kaveri business has a seasonality element wherein first quarter of the year, i.e June quarter is the heaviest. Rest of the quarters are much smaller in comparision. So inventory pile up is because of preparation of seeds for next June quarter, or sometimes for the Dec quarter when the Rabi crops come into play.

There was a good recent report on Kaveri seed by LKP.

15.01.2024 LKP report

Network of ~60,000 distributors (direct & in-direct) and retailers

Company has 1 million sq.ft warehouse facilities

R&D

** Increased from 3 cr. in FY21 to 17 cr. in FY23 (165 scientists). Setting up R&D biotech plant for 25-30 cr.

** Implemented standardized breeding processes for various crops, which have helped acquire germplasm with disease and pest tolerance and stable yields. Multiple breeding locations are used to identify tolerant lines, resulting in the development of superior hybrids that can withstand diverse conditions

Average lead time from R&D to commercial introduction is 7-8 years

Distributed 920 cr. as dividend and buyback since their listing in 2007

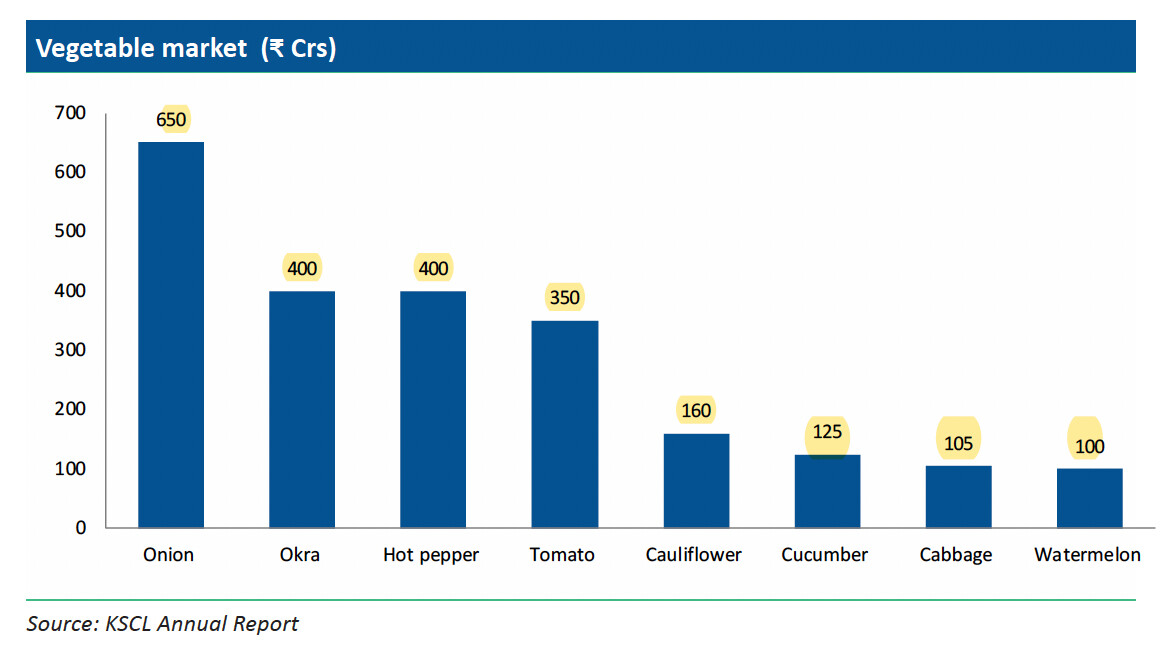

Hybrid vegetable seed is one of the fastest-growing segments and estimated to be 2,000 cr. Kaveri has built an exclusive sales team of 20+ employees

@hitesh2710

Agree, but average inventory days of 500 days means Kaveri stocks seeds for roughly 18 months? From sowing till harvesting, seeds cycle take more than 1 year, is this how it should be interpreted?

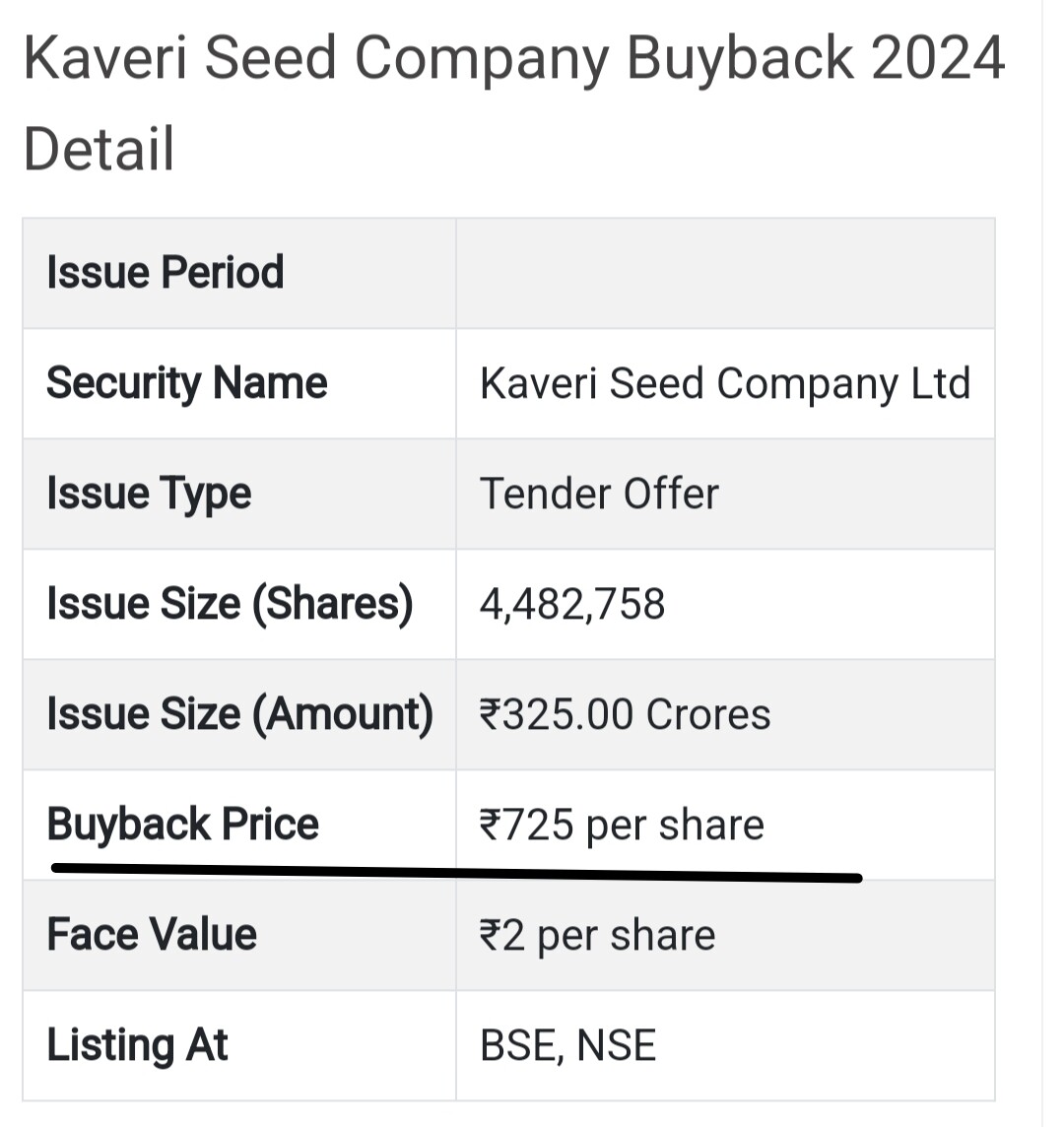

With Kaveri Seeds price almost reaching the buyback price of 725, would it also be forced to increase the buyback price just like L&T did a few months back! and then we saw the hard follow-on buying in L&T.

I liked this point.

In fact, I am doing research on finding secular growth companies for investments. I believe that, in long term, downside can be protected to some extent if one can identify secular growth in sales and profits and EPS all.

Many times, earlier secular growth story may turn non-secular and that impacts stock price on a larger scale than secular growth story.

Stocks which do not demonstrate secular growth in sales and profits, often have deep corrections from time to time. Slow growth is also sometimes acceptable but negative growth in sales and profits generally creates more deep corrections.

This point is not applicable to Kaveri Seeds but a generic point which I am mentioning here.

I was looking for any mention of them keeping an option to revise the buyback price one day before the record date (yet to be declared as share holder voting is currently on) but did not find it. I saw in Bajaj Auto case, they have kept this option. Any experienced person on buybacks may shed some light on it.

Disc: Bought the shares for buyback arbitrage immediately after the announcement.

Though Berkshire did not purchase shares of either company in 2023, your indirect

ownership of both Coke and AMEX increased a bit last year because of share repurchases we made

at Berkshire. Such repurchases work to increase your participation in every asset that Berkshire

owns. To this obvious but often overlooked truth, I add my usual caveat: All stock repurchases

should be price-dependent. What is sensible at a discount to business-value becomes stupid if done

at a premium.

Kaveri Seed should be buying back only when the share prices are trading at a discount. It is unfortunate that they keep choosing the tender route.

P.S. Kenneth Andrade is a known value investor, he has previously worked with Kotak and IDFC managing a couple of funds, till recently he started his own.

From Annual report Fy 22-23. “In recent years, the Company has

intensified its focus on R&D, recognising its

pivotal role in driving innovation and growth.

In line with this commitment, the Company

is currently in the process of establishing a

state-of-the-art R&D biotechnology plant.

The projected capital expenditure (capex) for

this venture is expected to range from Rs 25

crore to Rs 30 crore on a year-on-year basis. By

investing significantly in R&D, the Company

aims to enhance its research capabilities

and propel the development of cutting-edge

seed solutions, ultimately contributing to the

advancement of the agricultural sector and

the Company’s sustainable growth”

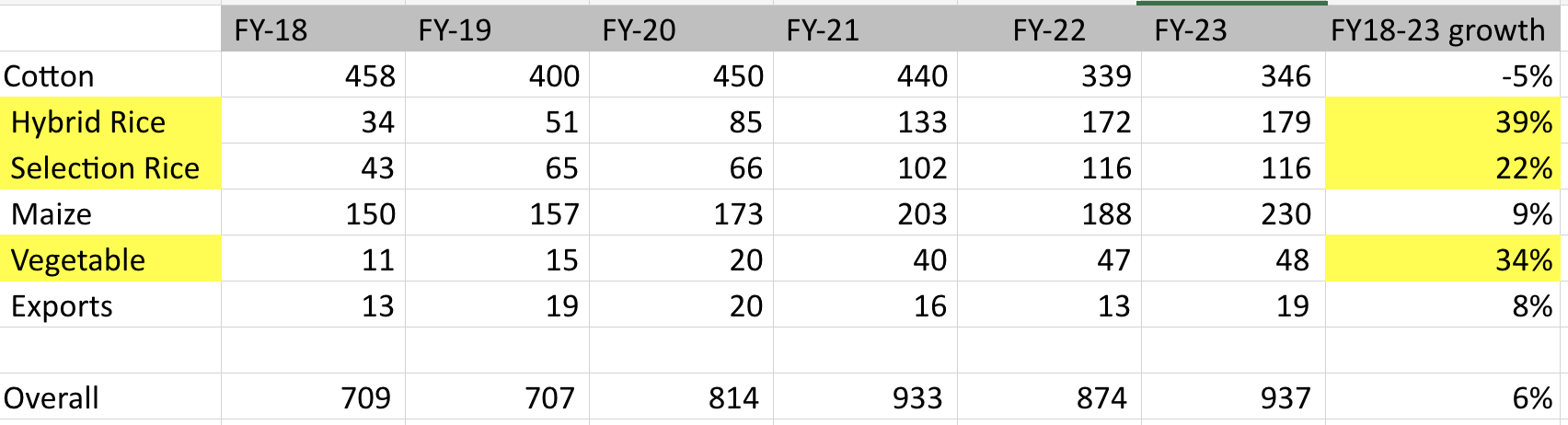

Kaveri had a decent FY24, with slow sales growth of 7.5% but margins improved resulting in higher EPS growth by 19.5%.

There has been a marked shift in their product mix, where higher margin crops like rice, vegetables have grown significantly whereas lower-margin crops like cotton has degrown. Concall notes below:

Incorporated subsidiary in Bangladesh as they want to develop own brand and dedicated research. Currently they are doing white labeling where distributors are selling seeds in their own brand names. Do not plan on entering cotton segment in Bangladesh

There has been large increase in cost of production of cotton and have not seen commensurate increase in realizations

Have 7-8% market share in maize (in top-5)

Vegetable crops contributed 60 cr. and they expect 20%+ growth

Seeing good traction in all crops except cotton, where their production lags demand. Expect 4-5% decline in cotton volumes in FY25 due to their lower inventory and shortage across industry

At peak, their cotton market share was 17-18% which has reduced to 12-13%. Cotton market size has also reduced from 5-5.5 cr. packets to 4.5 cr. They have lost market share especially in Andhra where they had 40%+ market share

R&D expenses: 57 cr. (vs 45-47 cr. in FY23). Includes recurring expenses

Disclosure: Invested (position size here, no transactions in last-30 days)

Two cents on why this space is getting me interested -

Potential IPO of Advanta - New kid on the block after a long long time

BT Cotton 3 and its impending launch

Traction in Hybrid Maize which has been a stagnant second largest segment for the company

Option values are any positive move towards BT seeds

Besides, I am not sure why this company is looked at from a forensic lens. Over the past six years, theyve made 1700 crore in cumulative PAT and have distributed 1300 crore out of it as either buyback or dividend. Would love to engage with boarders here and take the discussion forward