From social media posts, observe that Kaveri has a new corporate office. So the capex partly went to fund the new corporate office also.

The difference of 400 crores would shrink by another 175 cr after accounting for 20% buyback tax + surcharge/cess on 4 of the 6 buybacks.

Maize boosted by ethanol demand is a big positive.

BT 3 - cotton seed price control’s by government need to be removed as well to enable entry of BT 3 cotton seeds. Whenever that happens, it would be positive - but very low probability with wafer thin majority government for next 5 years - same government buckled down in front of farmer agitation when there was comfortable majority.

Advanta seeds - value unlocking may lead to value unlocking for Kaveri seeds. The very low valuations of Kaveri Seed will tend to stand out vs the valuations for Advanta in an IPO as most IPO’s are happening at mind boggling valuations. KKR owns 13.3% stake in seeds platform of UPL - paid 2,460 crores in Oct-2022 (Making then equity value of Advanta at 18,450 crore).

6 Likes

Q3 FY 25 results were better than expected as last year base included one-time export.

This year they seem to have good crop and inventory for next year also maybe sign for potential good next year.

Disclosure: Invested and biased

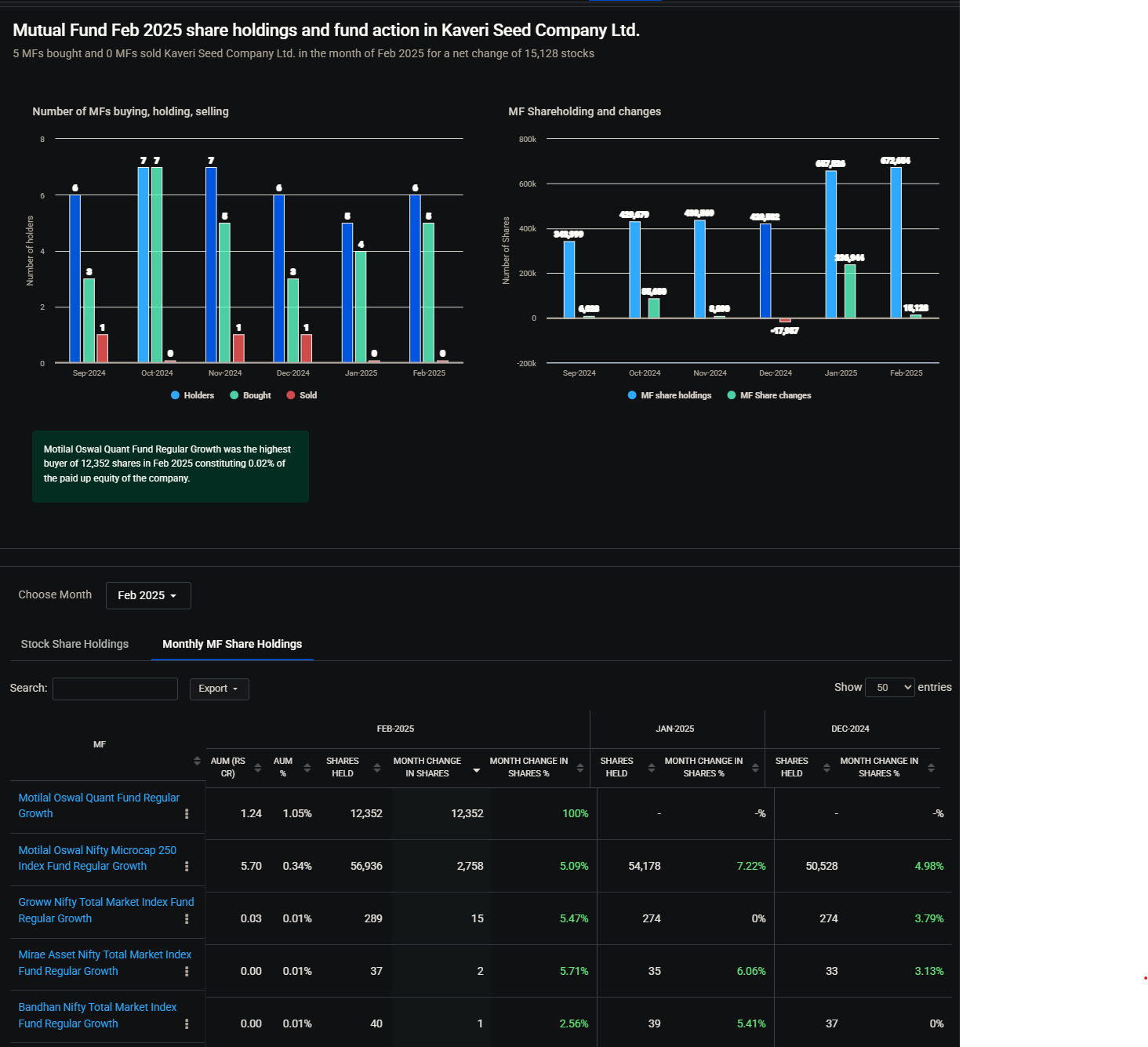

solid mutual fund buying in both jan and feb Mutual Fund Feb 2025 share holdings and fund action in Kaveri Seed Company Ltd.

1 Like

Disclosure: Invested.

Growth from Maize and Rice has been good and Seed Replacement rate (SRR) is high in both these crops. Pray for good weather conditions and Kaveri will have a breakout sales and profit this year.

Risks include Contingent Tax liabilities. Income tax and company seem to have a difference on how seed income should be treated. This difference is totalling to around 130-140 ccr.

[Great article on the company, recently read on substack.] (Why Kenneth Andrade is buying Kaveri Seeds 🌱)

2 Likes

https://x.com/amanagarwal/status/1907617217690349594

No Better opportunity to expedite BG3 and do whatever it takes to become efficient in Cotton production and textiles.

2 Likes

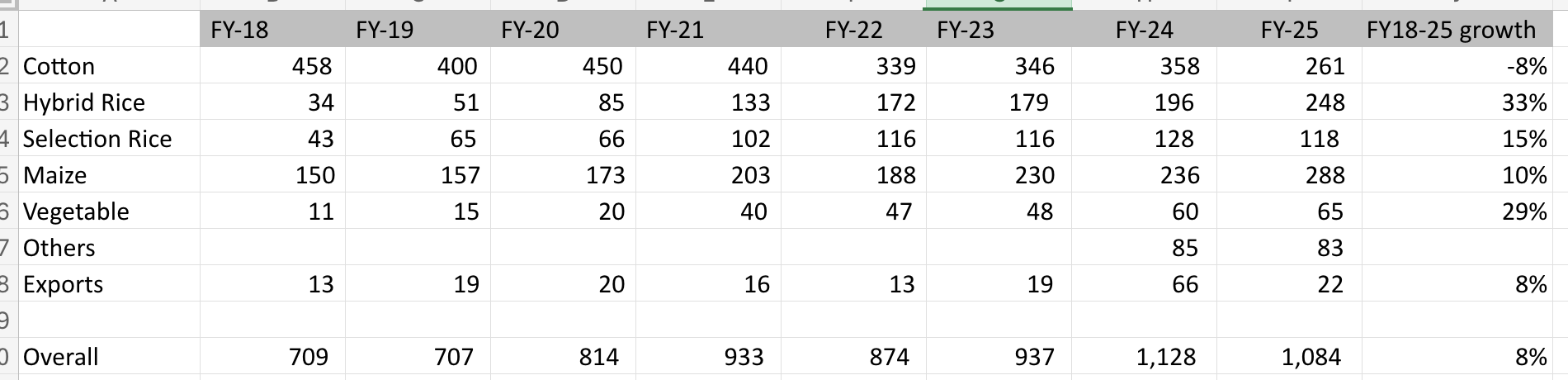

Kaveri is seeing good traction in maize which has grown well based on the ethanol blending program. Now, maize is their biggest seed followed by cotton.

Cotton has remained subdued. In FY25 in addition exports were bad which resulted in muted nos.

FY25Q4

-

Lower PAT due to 8.85 cr. interest on loan to employee trust and increase in employee costs due to increase in ESOP valuations + 5.68 cr. Increase in depreciation from addition of new office

-

Didnt get repeat order of 24 cr. from Tanzania (last time in Q4FY24)

-

Exports reduced from 66 cr. to 22 cr. due to political unrest in Bangladesh (and no repeat order from Tanzania). Added new countries in Africa and Southeast Asia. Target is to reach 150 cr. exports in next 5-years

-

Building up inventory (38% higher YOY) as channel inventory is on the lower side and they are expecting a good season. 20-25% of inventory is buffer stocks

-

Acquired 30% remaining stake in Aditya Agritech for 23.6 cr. increasing their stake to 100%

-

Sold 3.6 mn packets of cotton

-

They have in-house production facility (one of the largest in India) and are not impacted by external challenges in processing and packing of seeds. Maintenance capex will be 20-30 cr.

-

Expect static cotton acreage, but good growth in maize acreage

-

Government gave 4% price increase in cotton price realizations, however cost of production increased much more

-

Including fixed costs, R&D spends was 8-9% of sales

Disclosure: Invested (no transactions in last-30 days)

8 Likes

hi harsh

looking at current result of highest quarterly profits of 327 crore and improved operating profit margin of 39 % , but looking at annual sales of 2015 and 2025, there has not been much growth in the revenue in the company. can u please throw some light on how to judge the coming guidance for coming quarters. can we expect some good growth of 12-15 % atleast in next 3 years annually

1 Like

Look at the management’s ability to fill the loss of revenue from Cotton seeds with Hybrid Rice and other vegetable seeds

2 Likes

correct. new segments growth seem positive and that indicates strength of the management

Any reason anyone can find for such a discrepancy in Standalone and Consolidated numbers of Q1FY26 numbers?

1 Like

MY interpretation from Q3 FY26 Concall:

- It takes 7 to 8 years of R&D to produce a hybrid seed. The gestation period is huge in hybrid seed industry.

- Maize , Cotton and Rice (Selection and Hybrid) constitute 80% of sales of the company. The non cotton segment is growing fast, and management expects it to contribute to the growth in coming years.

- The running price of the crop and monsoon are the two major factors, based on which farmer decides on which crop to sow.

- Maize was in major demand last year, and based on it, entire industry accumulated huge inventory this year.

However, the demand for Maize this year did not panned out as expected, that led price competition among seed players and unsold inventory.

Having said that, the seeds can be used for 3 to 4 years, hence there is no problem in holding the inventory. - While company distributes entire cash generated in the form of buyback, this year, it was not done as entire cash generated was used to build inventory.

- Company will take decision of buyback in calander year 2026, after Q1

- R&D investments form 10% of sales, which is going to reduce going forward.

- The Income tax demand of tax on Seeds profit is going through appeal in the court and yet to be finalized.

Disclosure - Invested.

2 Likes

Tax demand overhang is getting resolved of around 129 crores and balance around 72 crores might get resolved in few days as the Appellate Authority has given judgement in favor of kaveri seeds.

Question was whether income earned shall be treated as Agriculture Income?- Appellate Authority favors the tax returns and treatment filed by Kaveri seeds co ltd.

Disc: Invested and biased

4 Likes