Kaveri Seeds Q1 FY 24 concall highlights -

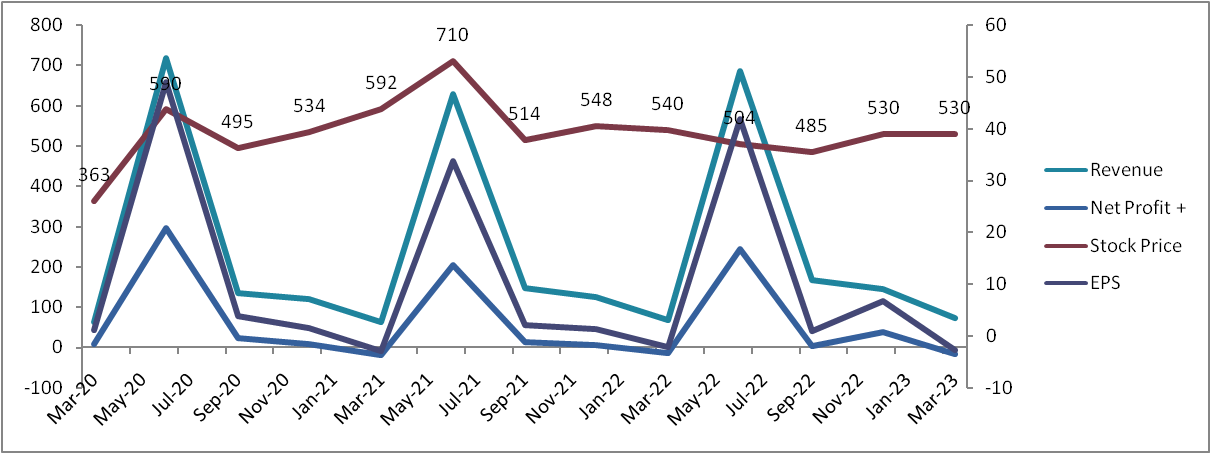

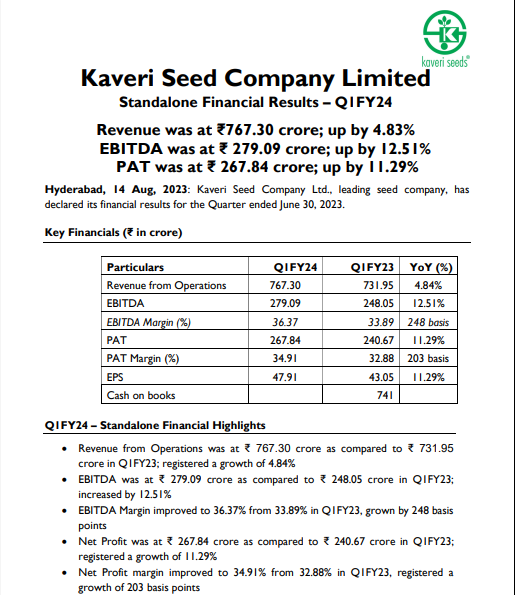

Sales - 736 vs 686 cr

EBITDA - 278 vs 247 cr ( margins @ 38 vs 36 pc )

PAT - 275 vs 245 cr

Cash on books- 741 vs 560 cr

Q1’s PAT > FY 23’s PAT

Delayed monsoon impacted sowing of Maize. Expect maize sowing to pick up in Rabi season

Sunflower, Mustard seed exports to start from second Qtr. Expect Maize, Vegetable seed exports to grow in Q2

Company banking on new products to boost profitability

Company’s export focus is on - Bangladesh, ME, Vietnam, Cambodia, East Africa, Phillipines

Company’s products (seeds)-

Cotton, Maize, Rice, Bajra, Sunflower, Vegetables

In Q1, cotton volumes were stable, revenues up 9pc

Bajra, Hybrid rice volumes were also stable

Contribution of new products in Bajra at 68 vs 52pc YoY

Hybrid rice revenue up 9 pc due price hikes

Maize volumes were down due delayed monsoon. Expecting pick up in Q2

Vegetables volumes were down due fall in output prices. Key products - Watermelon, Okara, Tomato, Bitter Gourd, Cauliflower, Cabbage, carrot

Launching new varieties in Mustard in Haryana, UP, Rajasthan

Kaveri has expanded its vegetables seed business team along with the offerings in the vegetables division. This team is separate from the staple crops team

This business is difficult to crack. However, company has been at it for over 7 yrs now. Continue to be very bullish here

Expect this ( otherwise stagnant ) business by 25-30 CAGR over next 3-4 yrs. This is a high margin business

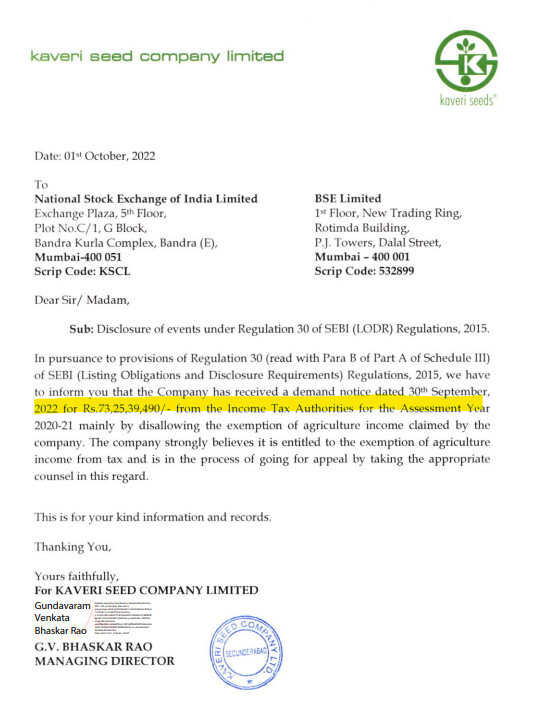

No new update on the 73 cr Tax demand notice received by the company

Spending a lot on vegetable seeds R&D

Segment wise revenue break up for Q1 -

Cotton- 348 vs 319 cr

Hybrid Rice- 181 vs 165 cr

Selection Rice- 110 vs 90 cr

Maize- 87 vs 96 cr

Vegetables- 18 vs 18 cr

Aim to take Vegetables sales to 150-180 cr/ annum in 5-7 yrs

Likely to catch up lost volumes in Maize in Q2, Q3, Q4

LY exports were 20 cr. Expect to do 30-35 cr this FY

Chilli, Okara and Tomatoes are the biggest and most profitable vegetable mkts. EBITDA margins vary from 30-60 pc !!!

Aim to clock 100 cr revenues from Mustard in medium term. Its also highly profitable product

Have a partnership with Monsanto for some GM crops. Waiting for Govt approvals for launch

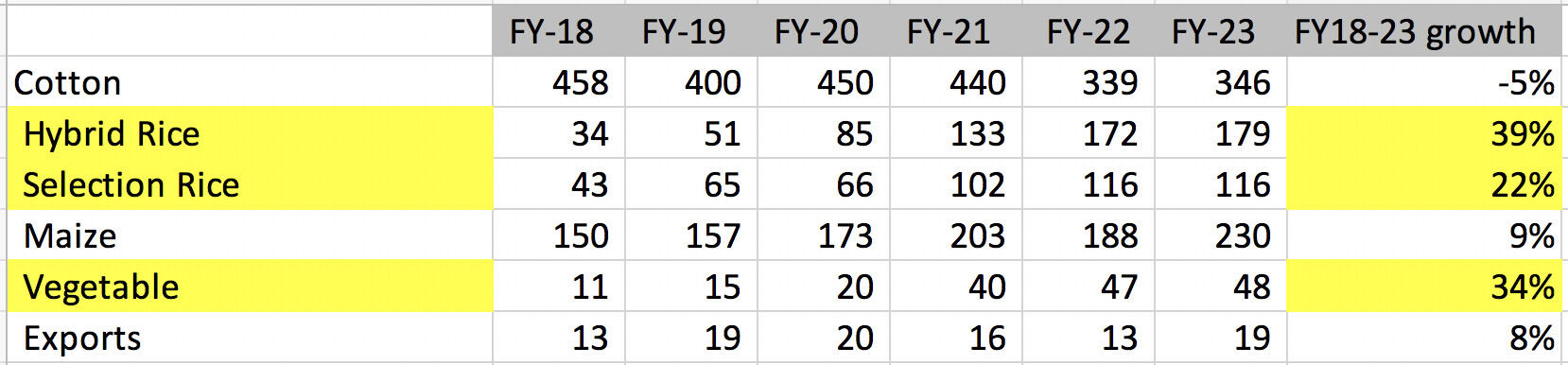

Last 5-6 years were years of consolidation. Company has reduced its dependence on cotton to a large extent by investing a lot on other crops

Growth should pick up from this yr onwards

Aim to do 200-250 cr export revenues in 4-5 yrs

Disc : initiated a tracking position after 8 yrs