@i_mustafa : Hi Mustafa, as you are tracking this stock since long; just a quick question on their network strength. If I have a look at the Q1 (FY 23-24) investor presentation, the slide states 300 sales force, 10000 active retailers and 3L carpenters.

And, if I Iook at investor presentation on 27th April’21, their network strength was 300 sales force, 10000 retailers and 3L carpenters. In spite of great performance in the last two years, why these numbers stand stagnant?

Would like to know others’ opinion as well, if they are keeping a track of the company. Thank you.

I don’t think the reach or network strength is a problem. It’s actually the execution piece, which is still underway to bring maturity in the states where they are currently present.

To highlight, they have recently entered into new two states (Delhi & UP with five branches), making the state count as 14 from the earlier reported 12. They have been good in tier 3-4 cities (smaller cities as per their IP), and when the states remain similar, the retailers and selling executive count have not grown much, mainly for these smaller cities/town. But if you check the numbers for operating branches (for bigger cities) has grown from 20 to 35 in that period. Even if you take growth from 20 to 30 (reducing the five new branches), this seems to be one of the drivers of topline growth.

Between the June 2021-2023 period, the topline growth & EBITDA Margin expansion, in my view, is a degree of three factors:-

Increase in companies’ operated branches, resulting in better working cycle metrics

Increasing brand awareness and the demand outlook in matured states, mainly - Gujarat (the company claims 30% Market share), Maharastra, MP, Rajasthan, and Karnataka.

Favorable crude prices were reducing the RM Cost (which is changing now).

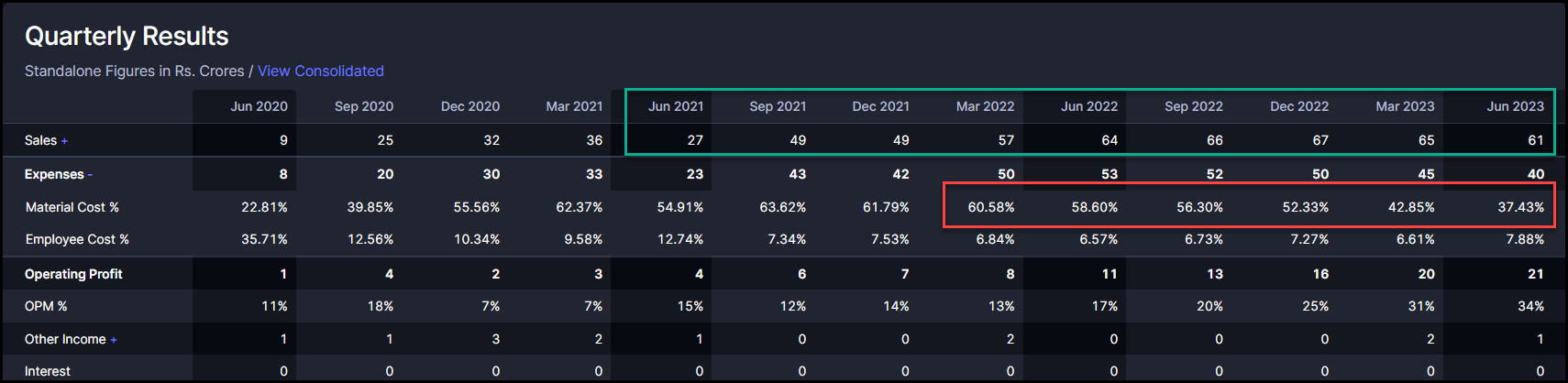

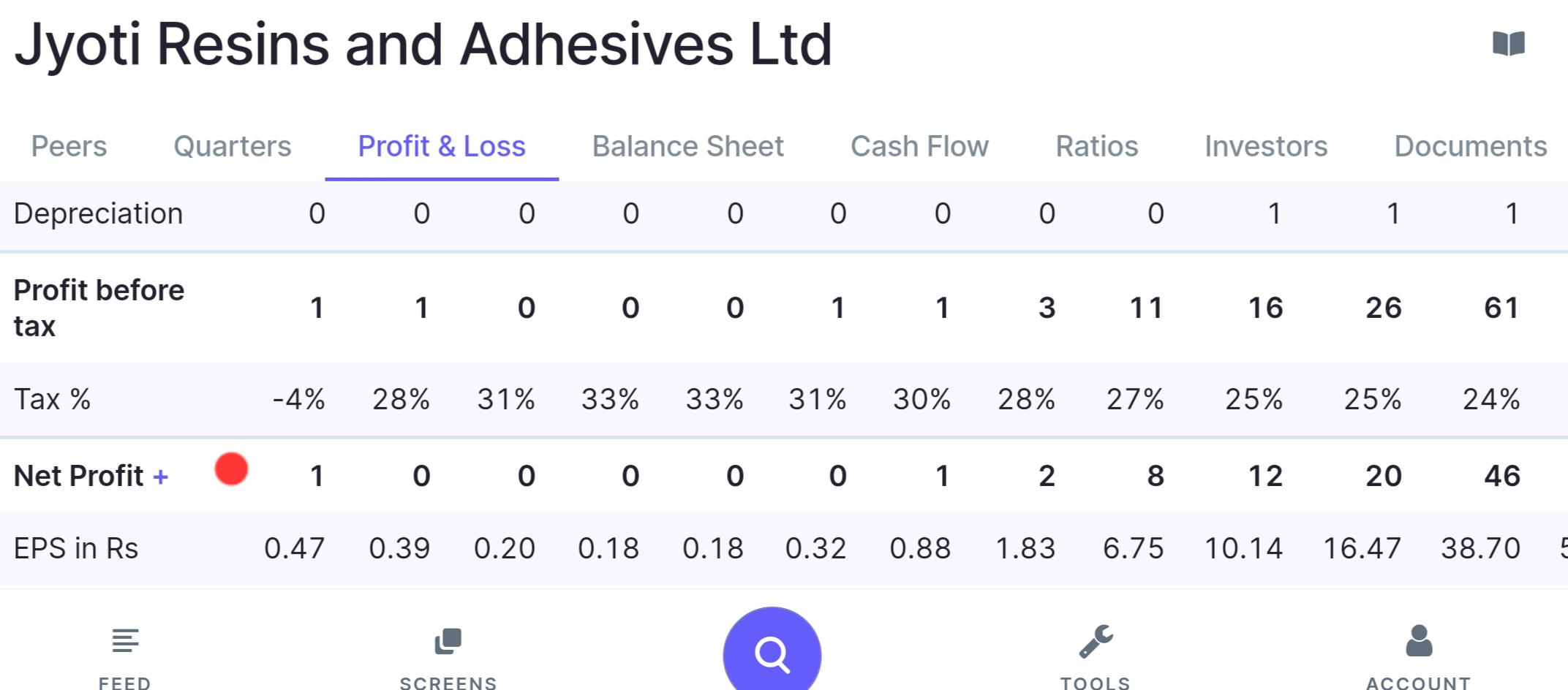

The other thing, that is making me sweat is the Margins (from 15% to 34%). The company said the ideal range should be somewhere between 22-23% which I earlier assumed to be 18%. 3 things that you should be aware of:

Rising Crude prices are bad for the company’s RM cost.

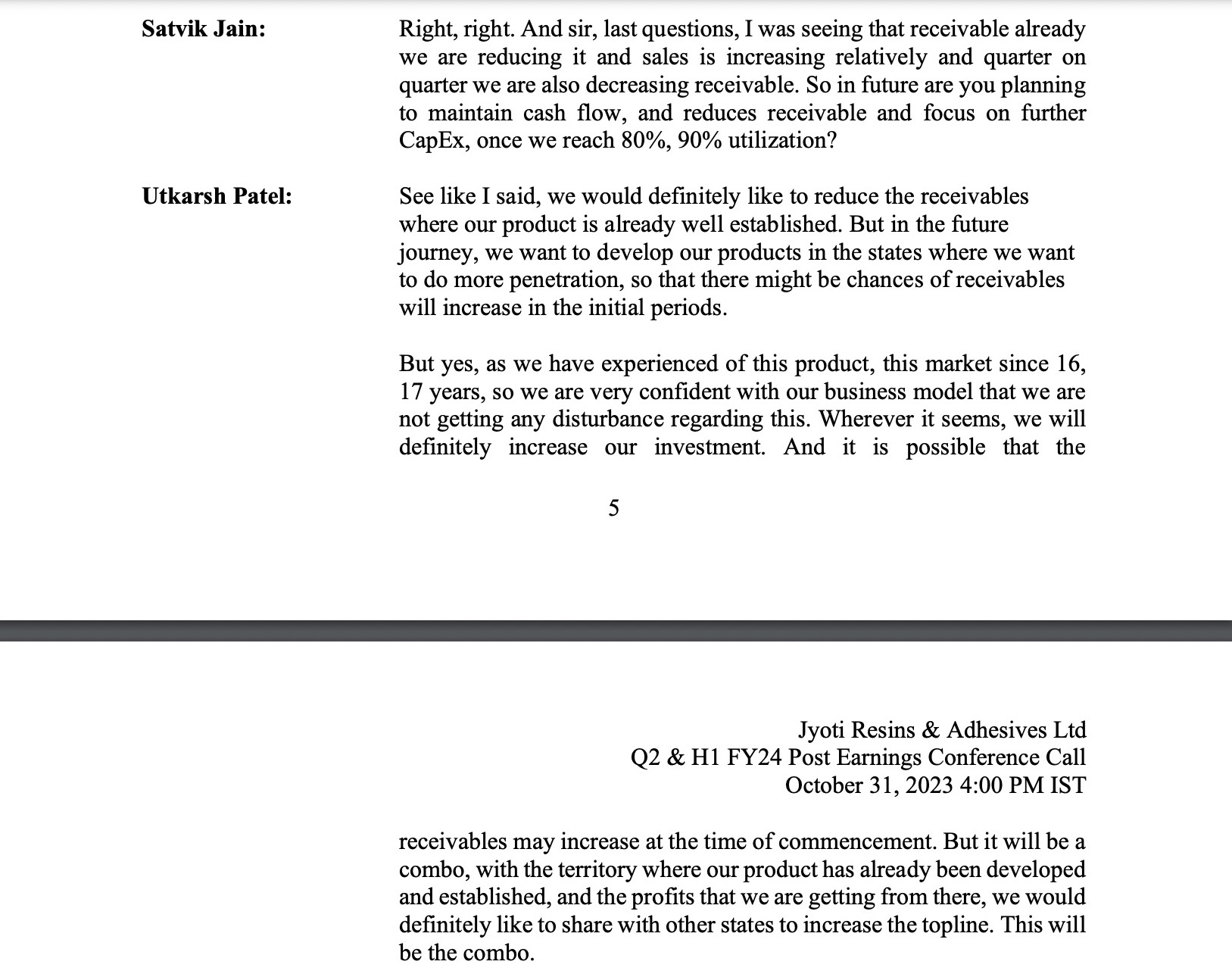

Their volume growth may not be reflected in their topline due to the accounting related to their carpenter reward policy. (this also answers the question raised by someone previously and is available in the concall for more details @ 20:30 - https://youtu.be/zbwvNoa4Gus?feature=shared) Once the carpenter starts claiming the rewards (I think in Diwali and the ongoing season) the company will book it both as Revenue and same time in expense) inflating the topline but affecting the EBITDA margins.

Increasing the maturity and penetration in states or increasing brand awareness in newer states will have positive benefits on the EBITDA. This is also the reason why I think, the company margin profile is a bit superior to the previous range of 15-18% the company used to operate in.

However, at this point, a better judgment would be to expect the margins to revert back to the 20-23% range and some topline growth incoming. The million-dollar question if you’re investing currently… is it already built into the price?

Company guided 25% CAGR growth for next 3 years as per their investor presentation https://euro7000.com/wp-content/uploads/Investor-Presentation-Q1FY24.pdf . Over the last 5 years, Company have grown at CAGR of 38%, 103%, 113% on Revenue, EBIDTA, PAT. They are number 2 in white glue(product Euro 7000). Not sure if any of you have used their product. Management is conservative and going into 1-2 new state every year. All ratios are excellent. ROCE 70%, ROE -50%, 0 debt, last 5 years sales growth > 50%, OPM 23%. Company is now in 14 states and have opportunity to go into other states and open more branches. Also company has recently increased capacity to 2000 TPM which will increase revenue.

I am not sure why this stock keep going downward irrespective of good numbers and available at 25 PE for such high growth company. Is there anything I am missing/not seeing which market is seeing. Currently I have 2% allocation, but I want to make it to 6% as soon as stock moves to upward trajectory. It seems I am more bullish on this company than management But I dont want to be wrong to lose big money as I am already in 10% loss in this company.

Any thoughts from anyone who is tracking this company closely. Any risk/negative news on the company? I heard company hired professional CEO also. But I am not confirmed on it.

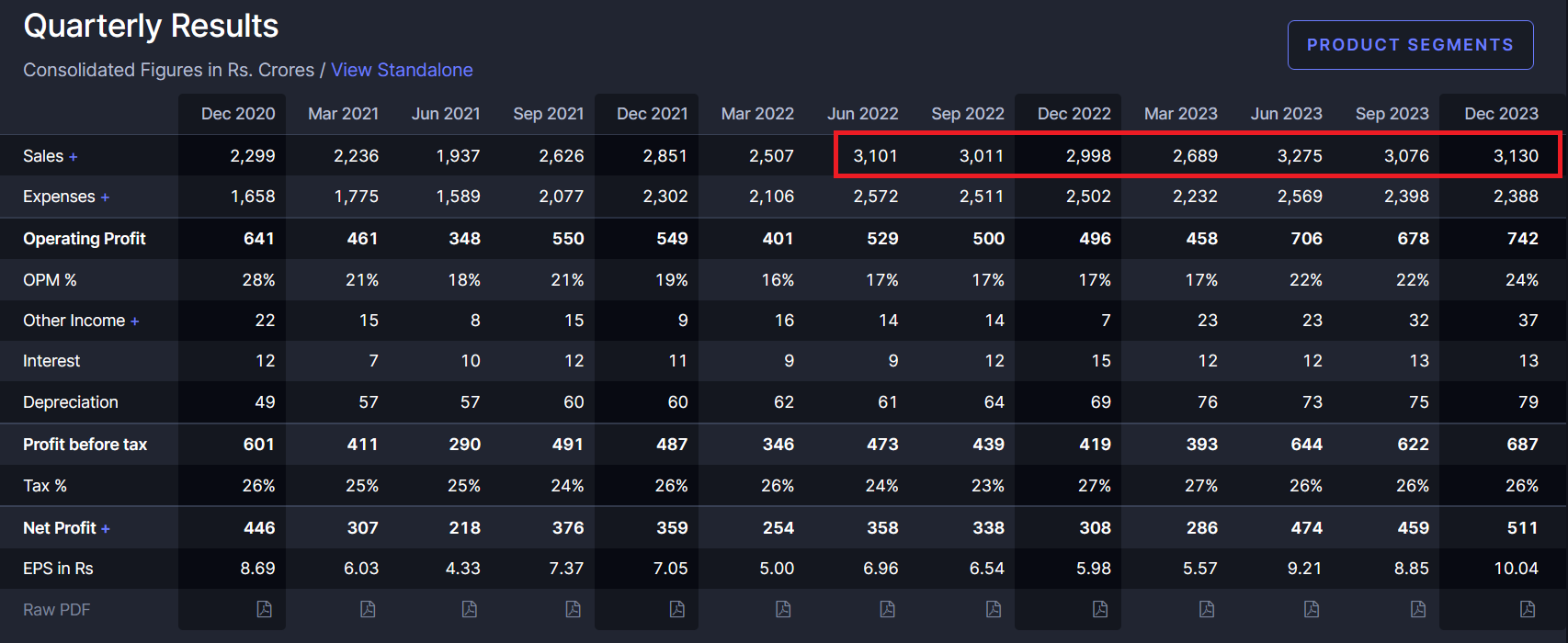

The problem is not with just Jyoti Resin, but at an industry level. The companies are having a hard time increasing their top line due to sluggish demand. The only saving grace for all the companies is the drastic fall in the price of raw material which is propelling them forward in terms of their EBIDTA and PAT margins and more or less keeping EPS flat since more than a year now.

Thank you for sharing industry level perspective. I should have looked at other players as well. One question that is coming to my mind is that Infra and realty sector is growing. That should result in increase of demand for proxy play as well like adhesive in this case. I can understand about Piditilie that is is such a big play and can’t grow much. But companies like Jyoti Resin has enough runway to grow for next 5-10 years considering they are only present in 14 states.

Per my understanding growth for adhesive companies, particularly these days, is coming from rural and semi-urban areas. The growth in these areas has remained muted until now. That’s now picking pace. The reason behind my thinking is that urban villas and apartments hardly have enough space for discretionary furniture, and due to paucity of time and space, most customers opt to get readymade furniture. Majority of furniture sold in cities, particularly from the likes of IKEA and Amazon’s Solimo brand requires assembly via screws and bolts rather than via adhesion. Yes, pasting mica on pressed wood and natural wood still requires adhesive.

Per Pidilite, in their latest concall, they mentioned that they should see better numbers in the upcoming quarter subject to a lot of ifs and buts (general election requires a lot of transportation eating up capacity for orgs to transport their goods, geo-political affairs etc.). They also mentioned that raw material prices appears to be bottoming out.

My belief is that for Jyoti Resin, the numbers should be better than industry average due to their smaller size (require less transportation, less raw material required etc.) and a favorable base effect.

The biggest concern is volume growth.

The management has on a shareholder concall denied to share the breakup for competative reasons. Realizations are good for now and if prices of VAM come down can get better but to sustain and create economic value, they need to penetrate new states .

Let’s see if the New CEO can create a turn around and scale from here

Great work guys…very interesting research on the company. On the concerns raised on the financial statements, I have two cents to add:

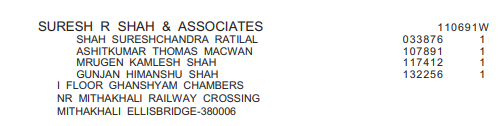

Auditor: Suresh R Shah & Associates, the company auditors do not have a website and cannot find the name of any other listed company, this firm audits. I was able to get the list of partners from ICAI website, and looking at their membership no. it can be said that the four partners and good years of experience…20+ years. So it cannot be concluded that the auditor is shady and they are more experienced than Adani Enterprises auditors for sure.

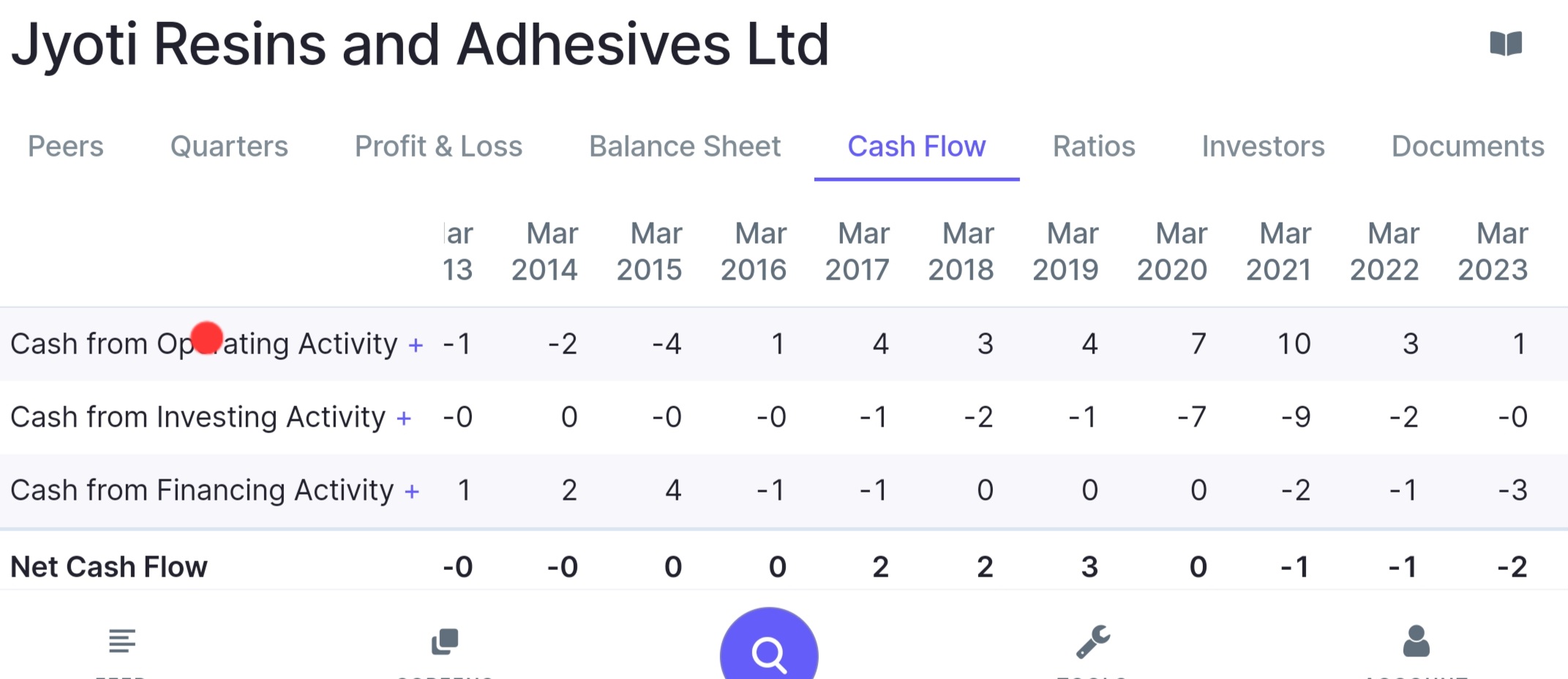

Cash Flow Statement: It is baffling that the company has not generated any cash flow in the past 10 years. A closer review of the Cash Flow Statement reveals that the company has been investing all its earnings into working capital, which is possible as the company has not raised any capital, does not have any debt or even short-term loans and has been growing revenues for the past three years at 50% plus. Everything put together, it is possible for such a company to not generate any free cash flows.

That’s due to high receivables and working capital. Since they’re in expansion mode that’s understandable. They are entering newer states and debtor days and receivables on higher side is natural. Historically there have been very high debtor days which I can see is declining since 4-5 FY. Since they are second largest player in White glue segment, the gap between Fevicol (1st) & Euro 7000 (2nd) being wide, they have huge scope and market to grow.

Huge TAM open for them!

Disc - Invested and optismistic about the sector and company.

The company is working towards creating strong relations with the dealers and its customers, i.e. the carpenters. Therefore they are working with a longer working capital cycle, as their receivables days are currently high. One may argue, that it could mean that the sales have been overestimated as the stock might just be lying with the dealers and has not yet reached the final customer.

It is an industry wide phenomena. Look at the quarterly material cost of Pidilite, HP Adhesives etc. and you will see a declining trend. Since Pidilite is well diversified, the trend is not as deep as it is in case of Jyoti Resins.

The raw material under concern that adhesive companies buys which has gone down in cost is Vinyl Acetate Monomer or VAM. This raw material is also used in decorative wall paints. Hence you will also be able to see a declining trend as far as material cost is concerned in quarterly numbers of paint companies like Asian Paints, Berger, Akzo Nobel, Shalimar, Indigo etc. Of course, it is not as pronounced due to a different mix of raw material required to manufacture paints.

Annual P&L of Pidilite, Material cost has remained at about 55% on the upside and 45% on the downside and other things remains same in terms of percentage except Manufacturing cost (which in on reduction trend due to economies of scale).

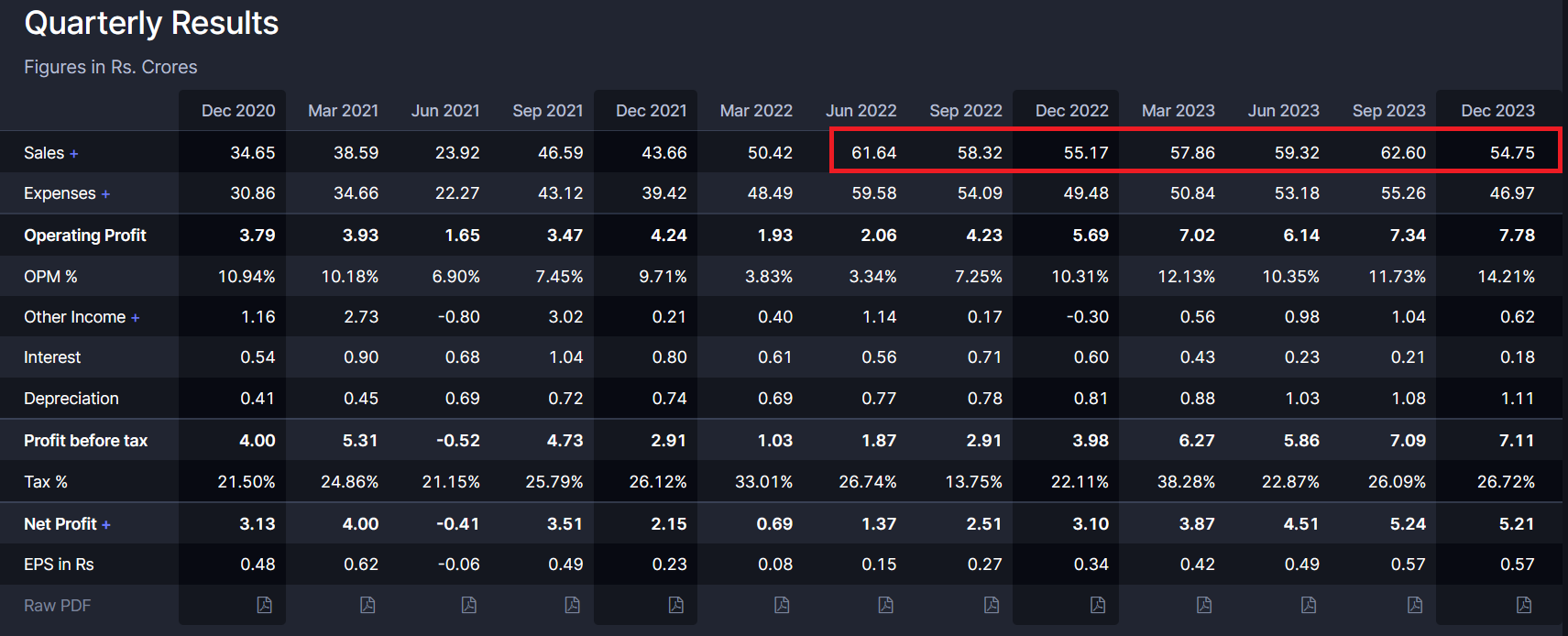

Look at Material cost how it has fluctuated over the years.

Manufacturing cost went as high as 20% and as low as 1% (doesn’t make sense at all).

Employee cost reduced to just 6.79% (this might happen due to economies)

Other costs fluctuating very much as well

As per quarterly trends Material Cost has dipped below 30% now and employee cost is now again rising to around 15%.

This literally means that the raw material prices have halved for Jyoti Resins which for Pidilite they are coming back to the lower end.

Doesn’t make sense to me.

Someone is manufacturing a chemical worth INR 100 where the raw material was earlier close to INR 60 and now it is at INR 30 without any change in manufacturing process or chemical properties of the chemical.

Thanks a lot for the detailed analysis. Following up on @Parakh’s point that the cost of raw material has gone down. I looked up the price history and see that the price has dropped from a peak of Rs.194/Kg in July 2022 to current levels of Rs.68/Kg which is a 65% drop. Hence a 50% drop in material cost is in line with this data.